Week of June 22, 2026 — CI Markets Weekly Outlook

Global markets are moving through a significant macroeconomic realignment. While headlines remain fixated on the ongoing rotation within the tech sector, deeper structural forces are actively reshaping the flow of capital. The primary driver of this transition is a strengthening US Dollar. This move is fueled by Federal Reserve policy adjustments, most notably indications of balance sheet trimming, alongside escalating trade frictions between Europe and China, and projected US policy strength following the G7 summit.

Meanwhile, international markets are moving independently of US indices. The Bank of Japan’s recent, highly anticipated rate hike was met with a weak response. This outcome has cemented expectations for a persistently soft yen and altered the outlook for Japanese equities. In the energy sector, weekend developments regarding Iran peace negotiations are overriding localized geopolitical noise in the Strait of Hormuz, leading to a downward adjustment for crude.

CI Markets signals a week defined by capital reallocation and currency dynamics, where a rising Dollar reshapes commodities and a weak yen supports export-driven growth in Japan.

Subscribe to CI Markets Alpha for Daily-Interval Forecasts

No contract. Cancel anytime.

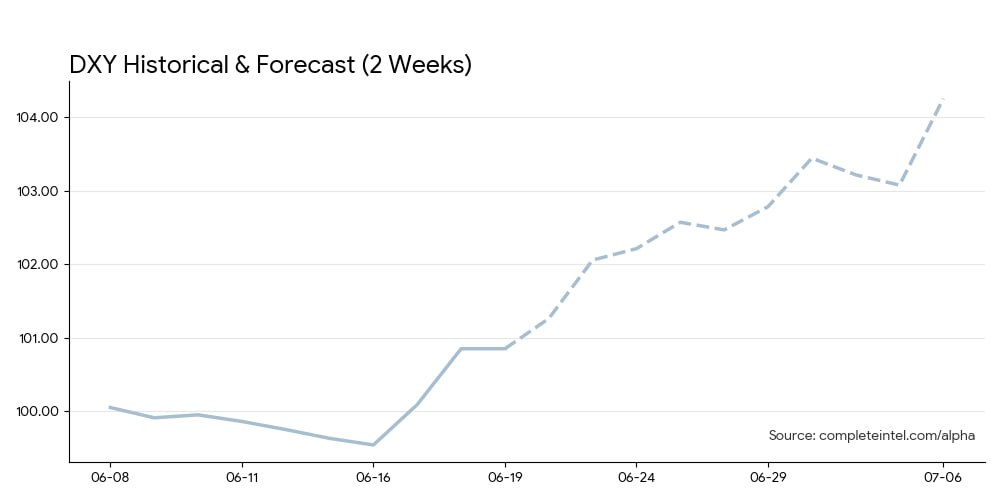

The Dollar’s Growth 🔼

The US Dollar is establishing steady strength over the currency markets. CI Markets forecasts the US Dollar Index (DX-Y.NYB) to open the week higher and sustain a persistent upward trajectory. This strength is not simply a byproduct of an equity rotation, but a direct reflection of tightening liquidity. The Fed’s signaling of balance sheet reductions is actively pulling dollars out of circulation. When combined with a depreciating yen, European trade anxieties, and projected US policy strength post-G7, the Dollar is operating as a clear anchor for global capital. This rising greenback will act as a structural headwind for global commodities and multinational earnings.

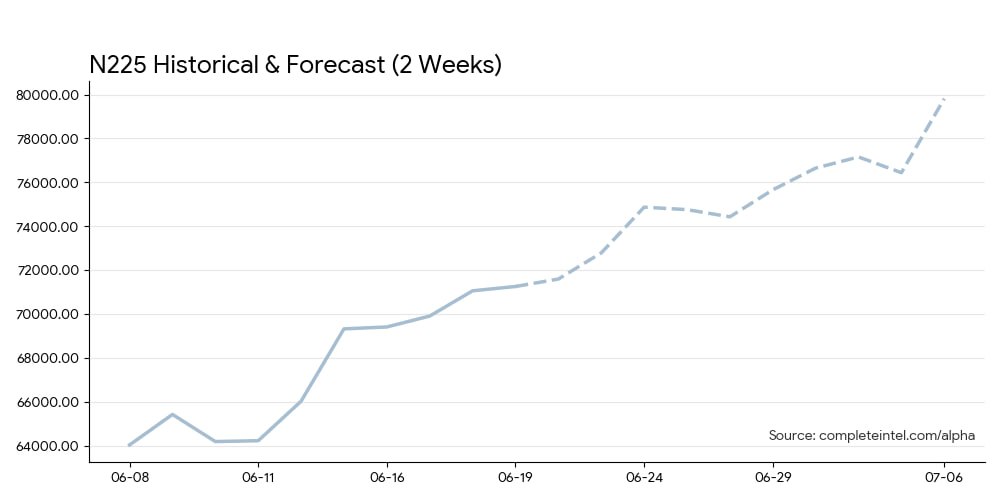

Nikkei’s Export-Driven Growth 🔼

While US equities wrestle with policy uncertainty, Japanese markets are poised for a steady upward move. CI Markets projects an upward rise for the Nikkei 225 to open the week, followed by a sustained climb. This move is deeply rooted in the Bank of Japan’s perceived weakness. Despite a recent 25 basis point hike, the lack of market response has cemented expectations that the yen will remain soft. This dynamic creates a tailwind for Japanese corporations, making their exports competitive against Chinese and Korean alternatives, while global consumers continue to prioritize the reliability of Japanese products.

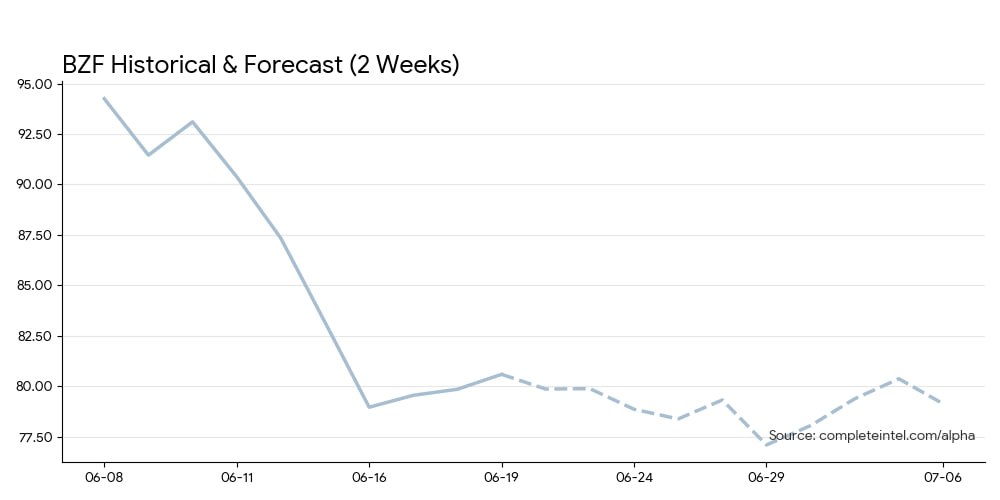

Brent Crude’s Continued Downward Drift 🔽

The energy market is undergoing a clear recalibration. Despite recent noise regarding events in the Strait of Hormuz over the weekend, the CI Markets forecast projects a continued drop in Brent Crude (BZ=F) to open the week, followed by ongoing downward pressure. The market is looking past localized skirmishes and pricing in two bearish realities. The successful advancement of Iran peace negotiations is actively lowering the geopolitical risk premium. Simultaneously, the rising US Dollar is suppressing global commodity demand.

Conclusion

The signal for the week of June 22 is Macroeconomic Reallocation. Investors must look beyond domestic equity rotations and focus on the power of the currency markets. An ascendant US Dollar will dictate commodity pricing, while a soft yen provides a structural advantage to Japanese equities.

The Wildcard: Keep a close watch on Chinese export data and trade rhetoric. As Japan’s export competitiveness rises on the back of a weak yen, Beijing may be forced to respond economically, potentially impacting regional currency stability.

The content presented in this note is for informational purposes only and should not be construed as investment, financial, or trading advice. This analysis is generated from the output of Complete Intelligence’s proprietary artificial intelligence platform and does not constitute a personal recommendation. You should not base any investment decision solely on this material. Please consult with a qualified financial professional before making any investment decisions. Complete Intelligence is not liable for any actions taken based on information provided herein.