The full episode was posted at https://www.channelnewsasia.com. It may be removed after a few weeks. This video segment is owned by CNA.

Show Notes

CNA: Welcome back to Asia First. Wall Street took a hit overnight amid concerns that a rise in Omicron cases would stall growth and add to inflationary pressures. Experts say supply chains and corporate profits could be dealt another blow as the possibility of increased restrictions is back on the table.

The Dow and the Nasdaq tumbled 1.2 percent. The S&P 500 closed 1.1 lower, with financials and materials among the biggest decliners. Also weighing on sentiment, Goldman Sachs has lowered its US growth forecast for next year. This after Senator Joe Manchin said over the weekend he would oppose President Biden’s 1.75 trillion dollar spending bill.

Let’s bring in Tony Nash. Now, he’s founder and CEO of Complete Intelligence, joining us from Houston, Texas. Lots to talk about today, Tony. So let’s start with Omicron. How much do you think potential measures are going to dent economic growth given the spread of the highly transmissible variant coinciding with the end of the era of cheap money?

TN: Yeah, it’s a good question. I think it really depends on where in the US you are. I’m in Texas and in in certain parts of the country you could barely tell that there’s a pandemic. There aren’t restrictions at all here, in Florida and other places. And also, we had our surge a couple months ago. So we’re on the downside of that surge now.

In the north, where you have kind of seasonal viruses, they’re on the up upward motion of the surge and so there’s a lot of sensitivity in northern states like New York, Boston, or Massachusetts, Washington DC, Michigan those sorts of places. So I think what you’re seeing is a kind of seasonal sensitivity because of Omicron and people getting nervous and so you know, again it really all depends where you are in the US.

For the upcoming Christmas break, flights are packed. Americans are traveling again. These sorts of things are happening. So, of course, there’s always a risk that people will do a hard lockdown like DC has put in some new measures today. But other places are seeing the virus as endemic and just kind of trying to move on with it. So, I think it could go either way but I don’t necessarily think we’ll have sustained negative impact. We could have short-term negative impact.

CNA: What about the risk from Fed moves and do you think the projected three rate hikes next year are going to be enough to contain inflation given the potential for Omicron to cause these price pressures to spike?

TN: Sure. You know, I do think that the Fed will pursue the tightening, meaning of its balance sheet pretty quickly. I think the rate hikes they’ll probably do one and wait and see and then they’ll proceed with the others later.

I think we can’t forget that 2022 is a midterm election year in the US and the Fed, you know, they they try to stay nonpartisan sometimes. But you know, there’s going to be a lot of pressure for them to make sure that the economy continues growing at an acceptable pace and kind of pushes down against inflation, So they’re in a tricky spot so they can’t just go out of the gate with three rises. They have to take one. See how the market digests it. Continue to build up expectations for the later rate rises then proceed based on how the expectations are set in.

CNA: What would that mean for the flows into markets given how Biden administrations Build Back Better Plan is also facing a setback? We could see a narrower bill than the 1.75 trillion on the social and climate front. What then do you think the market drivers are going to be if both the central bank and the government are curtailing that stimulus?

TN: Right. You know it is possible. Like I said earlier, kind of travel those sorts of things are coming back. I think Americans are just dying to get back to something that’s a little more regular, a little less constricted.

You know we do see things like food, entertainment, travel these sorts of things moving. Temporarily, we do see things like technology dialing back. But you know as we get into Q1 or Q2, we think that stuff will come back and be interesting again. So. But not necessarily as much of the work from home activities. People here are gradually getting back into the office.

So you know what we will see say for US equity markets is because tapering and interest rates we will likely see a stronger Dollar and that stronger Dollar will attract more money from the rest of the world as well. So both domestic growth, although it’ll be a bit tepid in ’22 will help to continue to push markets marginally.

We’re not going to see massive growth like we saw in ’21. But the the strengthening US dollar will draw up liquidity from other parts of the world, too.

CNA: Just very quickly if you can, Tony. What do you think the outlook for energy demand and oil prices is going to be like given how some countries are already reverting back to containment measures?

TN: Yeah. Oil is tricky. In the near term, I think oil is a little bit tricky for the next few months. I think the outlook is better as we get say to the end of Q1 and into Q2. But for now, we’re not expecting a dramatic upturn in crude prices like we’ve seen in gas prices in Europe and other places.

CNA: Okay, we’ll leave it there for today and keep an eye on those commodities. Thanks very much for sharing your insights with us. Tony Nash of Complete Intelligence.

Patrick Perret-Green of PPG Macro joins us for a QuickHit episode to reflect what 2022 brings. Patrick got not only the Covid call, but a lot of inflation calls right through the pandemic. As we wrap up 2021, what does he think about right now and how does that set the stage for his view on 2022?

PPG started in 1997 in research where he learned how bank balance sheets work. He also run the strategy for Citi for rates and effects in Asia and at one point worked out in Sydney. And in the past five years now, he’s been focused on the global macro environment.

📊 Forward-looking companies become more profitable with Complete Intelligence. The only fully automated and globally integrated AI platform for smarter cost and revenue planning. Book a demo here.

This QuickHit episode was recorded on December 16, 2021.

The views and opinions expressed in this The year ahead: What have we learned from 2021? (Part 1) Quickhit episode are those of the guest and do not necessarily reflect the official policy or position of Complete Intelligence. Any contents provided by our guest are of their opinion and are not intended to malign any political party, religion, ethnic group, club, organization, company, individual or anyone or anything.

Show Notes

TN: So, Patrick, you’ve got not only the Covid call, you’ve gotten a lot of inflation calls right through the pandemic. And as we wrap up 2021, I guess what I’d really like is, what are you thinking about right now and then how does that set the stage for your view on 2022?

PPG: Well, there’s a whole lot of multiple issues. So I was rewatching Powell’s Q&A this morning. And clearly there is the energy side of things. There is the good side of things, the demand for goods, and they are responsible for big chunks. And I was quite surprised by the ECB’s massive upward revision for inflation for 2022 in the press conference earlier on today. But base effects are very powerful. So we always knew we were going to get peak base effects. We’re going to come in around October, November time. Oil average WTI average below about 39 to $40 last October, November. And by January are up to, or early February, we were early 60s. That base effect will tumble out quite dramatically.

I also think that the durable goods effect is also going to tumble out dramatically. We’ve had record purchases, but I remember talking joking with people last year. It was about the middle of last year, and I was saying I was just as an experiment going on ebay and seeing what I could pick a Peloton up for. So everyone got their Peloton or they bought a flat screen TV. They did the house, they did the kitchen because everyone was at home.

And I think when you look at durable goods purchases in the US and this is chart I’ve posted many times on Twitter. They are off the charts and they’re off the charts relative to disposable income as well, which is now falling. Okay, due to inflation as well. But in the US, we’ve also got this remarkable thing that it’s very different to other countries.

So you look at the UK. We had the employees taken out the other day. We’ve now got more people on payrolls than we had prepandemic. Non-farm payrolls are still down 3.9%. And in Europe employment has been much better. So the great retirement, the great resignation seems to be a US phenomenon.

But I think next year the risks are that everyone that goods purchases collapse and pricing power similarly collapses with that. And even things like autos as well will pass. So we know for well that the auto manufacturers have got lots full of 95% completed cars, and the chip shortage is actually a thing. It’s not that the world has run out of chips. There’s some papers recently looking at chip supply.

So the supply chain disruptions are being true. Yes, there’s still log jams with ports in the US, but in Asia, around Singapore, they’ve largely cleared into chain. Yeah, we’ve still got subjects very pandemic risks of problems with changing over ship crews and things like that. But overall, I think that side of things will ease down.

Okay. The pandemic is of pain, but we all know that. And there’s a lot of we’ve got Omicron now, but there is some cause for hope. It’s incredibly infectious. But all the people I know have got it. I don’t know anybody who’s had it really bad. Whereas I know people who even had Delta and they were really late. I don’t know anybody hospitalized, really. But could this be, like a bit of a bushfire?

It goes through very quickly. But actually, then we have the benefit because it’s so infectious. So many people get it. That herd in unity becomes higher. And actually, by February we’re back and everyone not giving a damn.

TN: Which is what I love. I love it. I love it. Let it be. So I hope it happens.

PPG: But let us go. But let’s not forget the underlying reality. People seem to stare in sort of my a rose tinted glasses and look back and think like, oh, wasn’t it wonderful prepondemic? No, it wasn’t. The world central banks weren’t cutting rates in 2019 because we were in good shape and there wasn’t a load of excess capacity. My concern is now that actually we talk about capacity being built. So records for containerships is less.

However, the volume of global trade actually is not particularly higher. It’s more because of disruptions. An empty container has been trapped in places. So people are building more containers and they’re building more factory space. But once the supply chain disruptions come down, then you’re going to be left with even more excess capacity.

TN: Right. Well, it’s the other side of letting all those old containerships and book carriers retire in kind of 2011 to 15. Right?

PPG: I’m still left with an image of a world that, compared to 2019, has more debt, it’s older and the capacity hasn’t gone away. And then we’ve also got the geopolitics and the politics and all that sort of stuff as well.

Watching Powell last night, I was struck by how amazingly sort of confidently was about the outlook for the US economy. Two, how he seemed to have lost all recollection of the effect of the last tightening cycle on what was a much healthier economy. So here we’re talking about, we got a 150 basis points of tightening by the end of 2023.

Okay, tapers. We all knew that’s going to end quickly. It’s going to be done by middle of March, in 10 weeks time.

TN: Just words, Patrick. It’s just words.

PPG: And then they do Redux. And he admitted at the end towards the end that they had their first discussion about the balance sheet. So I think they’ll start balance sheet reduction much sooner. But the problem is if we go back to last time when debt was so much lower, the Fed overtightened.

My reckoning, was they should have only really gone to one of the records. They completely underestimated the impact of balance sheet reduction on liquidity. I did quite a lot of work on the plumbing, and the irony is that the Fed is in charge of a mandatory systems. They’re not a very good plumber. They seem to actually understand how their own system works properly. So you end up being like the repo crisis. No, it’s not QE. We’re just buying bills and then we’re buying coupons. But it’s not QE it’s just liquidity management.

All these various issues and the other aspects I think about inflation is, there’s a lot of similarities with what happened with China in 2008, 2009. China had this. It was only a $7 trillion economy. A trillion dollars of stimulus. M1 was up 40%, M2 was up 30%. And rather than normal lags of six to eight, nine months, M2 growth peaked at the end of 2009 or late 2009. But inflation didn’t peak until the end of 2010, early 2011. So such was the volume of stimulus that came through. It just reverberated along. You dropped a Boulder in a pond?

TN: Sure.

PPG: So the ripples effect just last for much longer. And I think that’s one of the things we’re seeing, but obviously, what we also are seeing is global money growth as a whole has slowed very dramatically. And even when I look at things like excess reserves or where we are now or currency and circulation within the US, the sort of three to six month annualized rates are backed down to rates that they were at pre crisis.

So the year on year base effects are all fading out. And ultimately, unfortunately, most central bankers aren’t monetarists. They seem to have banned monetary economics. Greens bank scrapped M3 in the US. He’s a great scenery as far as I’m concerned.

TN: So when do you see this stuff really taking hold? Is it kind of mid 22 or?

PPG: The second quarter it really picks it. And we got the other side of it. So we got a US that’s doing okay or brilliantly, as far as pounds and the Feds… Europe, that actually is doing all right as well I mean, everyone’s got perpetual downer in Europe. But I think Europe could be the surprise next year.

And we got China, which is everyone still gets on this sugar high. They’re doing stimulus. And I keep on trying to explain to people, it’s not stimulus. This is dialysis.

TN: That’s a great statement.

PPG: I had a long term view on China, and it really goes back to sort of 2014. Once Xi really took control, got rid of all the rivals, started centralizing the power.

And there’s a long term rationale behind that. So, yes, in terms of the Chinese are great at some long term thinking. In other ways, I describe them to people as like, yeah, China is like a linebacker. He’s like 250 pounds. He’s six foot six tall, but unfortunately, he’s got the brain of an 18-year-old.

TN: I think the latter is more accurate, actually. With that in mind, as we move from inflation to say another obvious kind of what’s ahead for 22? What do you see for China in 22? Do you see ongoing stimulus? Do you see a roaring Chinese economy? What does China look like for you in 2022?

PPG: Well, the interesting one is that we look at everything that’s come out of the recent Central Economic Forum, all the going. The whole emphasis is on stability. None of this grandiose stuff about we’re going to be strong. It’s about stability.

Think tank South China Morning Post, which is owned by Alibaba, which is effectively controlled by the state nowadays. So there’s the G 40 Economic Council, whatever they are think tank. But it’s next PVoC governor or deputy governor on it as well. A big article. Nothing is said without less it’s approved.

So they were talking about monetary and fiscal stimulus next year and by that moderately lower interest rates. Central government stimulus because it can’t come from local governments because they’re bankrupt and they’re not getting the land sales revenue and they won’t because the collapse of the real estate.

TN: That’s an important point, though, if you don’t mind holding on the SCMP article for a second. I see people on social media say all the time, well, local governments will always come in with stimulus. But from where? I don’t understand this fallacy, that local governments can always come in with stimulus.

PPG: Well, no, they can’t, because I think even Goldman come out and say that local governments have got hidden debt of about 40 trillion CNY. And all their various financing vehicles. They’re screwed.

They don’t have the money. But over time over the past few years, we’ve probably seen this greater and greater central control. Come on them anyway. They’re more and more dependent on central government forward expenditure. And the rationale comes to this because I think the regime has always recognized that the debt or we’ll keep playing the game of Jenga is unsustainable.

TN: Right.

PPG: And therefore you have to get to a point where we’re going to take some pain. So if you look back at what Xi’s been talking about over the past few years, it’s all about struggle, the Long March. I mean, this is like really going in. That is the story of China. He conveniently forgets to mention, the Long March was actually really a long retreat and basically hardly anybody who started it survived. But that’s completely ignored.

But there is this centralization of power because they know that things have to be dealt with and there will be there’s a potential for trouble. So you become a super authoritarian super, you know, look at all the moves about data.

It’s all about the Chinese government having much more control, much more visibility, a greater ability to snuff out any sort of signs of opposition at the very earliest time.

TN: But my worry there is that China, actually, I think, is becoming fairly brittle. Meaning the Chinese government is becoming fairly brittle.

Under previous regimes, you had a fair bit of flexibility where you had the different levels, not with a lot of autonomy, but with a fair bit of autonomy. Now you have a huge amount of centralization and that creates a fairly brittle government, both economically and politically.

I’m not saying it’s necessarily going to break, but I do worry about what they’re creating.

PPG: Well, I agree with you. I’ve made sneak it past my then investment bank employees. When I came out 2014, I wrote about the stylinization of Chairman Xi.

So you have the centralization of power in one man. But then you also get that fear of slightly Tsar Russia. Nobody wants to be the bearer of bad news. So you had African swine fever. Everyone covered it up. Which was one of my concerns about Covid, because, like you saw in Wuhan, local police shut up the doctors on the 1 January.

And similarly, so you have this culture of paralysis, even pre crisis, Xi comes out and says, oh, we need to reduce coal fire stations. So good party figures, party Chiefs, local party Chiefs. We shut it, shut it down. And then they realize, actually, we haven’t got anything to heat the homes or schools.

Oh, by the way, then we have to divide the energy from the gas from the aluminium shelters to actually do that. You got this sort of, whereas, if you look back to China and Zheng and other leaders, China sort of thrived on its basically Brown envelope culture. We just get it done. Ignore central government. Okay, but at the same time, we are putting loads of cadmium into the ground and killing ourselves. But so be it.

TN: When you look at what’s happening in China domestically, with the economy and with the political structure. I’m also curious about their outward political projection. And I do worry about Northeast Asia, not just China, but Japan, Korea, Taiwan.

And I’m curious, since you have such a historical background, I’m curious what you think about China in terms of political projection, say for 2022. Are you worried that they are going to become aggressive in ’22?

BFM 89.9 asks Tony Nash from Complete Intelligence on how China’s PBOC adoption of looser monetary policy will affect the yuan and the broader Chinese economy.

SM: BFM 89 nine. Good morning. You’re listening to the morning run. I’m Shazana Mokhtar are together with Philip See. It is Christmas Eve, Friday, the 24 December 9:06 in the morning. But in the meantime, let’s take a look at the activity on Bursa Malaysia.

PS: It’s flat like Coke without any bubbles.

SM: Oh, no, that’s the worst kind of flat.

PS: Yes, the foot sabotage. Malaysia is flat slightly down .09% at 1515.

SM: So still above 1500.

PS: Still above 1500.

But it’s been yoyoing a bit green and red so far. But the rest of the markets across Asia are in green territory. The Straits time is up at 3100. Cosby also up 58% at 3015. Nikkei also up zero 6%, 28814. Now, just to bring your attention, looking at the crypto Bitcoin 5998.65 above the 50,000 mark. Theorem also uptrend 4114115.184. Now, if we shift over to the currencies, ring it to US dollar 4.11988. You’re seeing some strengthening there. But across the other two currencies pound and sing dollar, we’re seeing some weakness there.

Ring it to pound 5.62967. Ring it to Sing dollar 3.0922. Now, looking over to the value board. Really. Smattering of small caps actually driving it, but cost number one Ata IMS at .72 cent unchanged, followed by SM Track up 13% at .13, followed by Kajura Tran asphas flat at .26%.

SM: Okay, so that is the snapshot of Bursa Malaysia at 9:09 this morning. We’re taking a look now at how global markets closed yesterday.

So if we look at the US markets, they closed in the green. The Dow was up 0.6%. The S&P P 500 was up zero 6% as well. The Nasdaq was up zero 9%. So a lot of optimism going into the Christmas weekend. Joining us on the line for analysis on what’s moving markets. We have Tony Nash, CEO of Complete Intelligence. Tony, good morning. Thanks for joining us today. Now 2022 is just a week away. And given the triple headwinds of Fed tapering, Omicron and a China slowdown, will there be a difference in how developed and emerging markets in Asia are going to be impacted?

TN: I think with the tightening in the Fed and with what emerging markets are going to have to do, meaning in the near term, like China is going to have to loosen. So I think you’ll have a strengthening dollar and more of a rush for capital into the US, so that should at the margin, kind of help US markets stay strong across debt and equity. Other things. I think in emerging markets it could eventually China loosening. The PVC loosening could help demand in emerging markets, but it’s going to be hard to get around the hard slowdown that started in China around Omicron.

PS: I see.

And so when you contrast that to the Fed tightening, right. You said China PBOC is adopting a looser monetary policy. How will this affect the UN in relation to those Asian currencies in which there’s a lot of trade between these two countries?

TN: Yeah. CNY has been strong for a protracted period, and it’s made sense on one level, so China can import the energy and food, particularly and some raw materials that it needs in a time of uncertainty. So the PVC has kept it strong through this period. What we’ve expected for some time. And what we’ve shown is that after Lunar New Year, we expect the PPOC to begin to weaken the CNA. We don’t think it’s going to be dramatic, but we think it’s going to be obviously evident. Change of policy, Chinese exporters, although they’ve been producing at not capacity, but then producing pretty.

Okay. China is going to have to devalue the CNY to help those exporters regain their revenues that they’ve lost over the last two years. So we’re in a strange period globally of moving from kind of state support back to market support, whether it’s the US, Europe, Asia, we’ve really had state supportive industries, state supportive individuals as we move beyond covet. Hopefully we’re moving more into a market orientation globally, and there will be some volatility with that.

PS: Yeah, but I was wondering for China, especially, I’m interested to know what the state of the Chinese consumer will be in 2022 because the government is worried for slow down. Right. And wouldn’t they want to expedite and give a bit more ammunition to the Chinese consumer?

TN: They would. But the problem is with Chinese real estate values declining, a lot of consumer debt is secured against real estate. And so the ability of Chinese consumers to expand the debt load that they’re carrying. Is it’s pretty delicate? It’s a fine balance that they’re going to have to run. So either the economic authorities in China push real estate markets up to allow Chinese consumers to keep debt with their real estate portfolios, or they make other consumer debt type of rules that allow Chinese consumers to hold more debt.

Real estate is the part that’s really tricky in this whole equation in China, because if real estate values are falling, the perceived wealth of those consumers is falling pretty rapidly as well, and the desire to consume excessively, it’s just tempt out.

SM: And I suppose still sticking to our view of China looking at metal commodities, what metals have been affected by the slowdown of demand in China? And do you foresee a recovery for them in early 2022?

TN: Yeah. We’ve seen industrial metals like copper and steel, and those sorts of things really slow down dramatically compared to where they were earlier in 2021. We’re seeing reports of, say, copper shortages at the warehouse level at the official warehouses in China, but that’s not real. What we’re seeing and I speak to copper producers in Australia and other places. What they’re telling us is that those copper inventories are being shifted to unofficial warehouses to create a perception of shortage. So we may see a run. We may see an uptick in, say, industrial metals prices in early 22, but we don’t expect it to last long because the supply of constraint is not real.

So until demand picks up for manufacturing and goods consumption. And the other thing to remember is we’ve had a massive durable goods wave through covet. Everyone’s talked up on durable goods. Okay, so there is almost no pent up demand for durable goods. And this is the stuff that industrial metals go into on the demand side, there are some real problems on the supply side. There seems to be plenty of supply in many cases. So we don’t necessarily see the pressure upward, at least in Q1 of 2022 on industrial metals.

PS: And that’s why I’m quite interested where you say that this demand is, I think slowly going to dissipate because yesterday key US inflation gauge sharpest rise in nearly 40 years, right? Personal consumption expenditure surged 5.7% in November. How long do you think this elevator level will last?

TN: Well, US consumers are pretty tapped out. So I think inflation happens for a couple of different reasons. Some people say it’s only monetary. Not necessarily true. We’ve seen real supply constraints that contribute to inflation. We’ve seen demand pulls because of overstimulating economies, and those two things together have accelerated inflation. And so we have to remember at the same time in 2020, we saw prices. If things go down pretty dramatically around mid year, say a third of the way through the year to mid year to just after mid year.

Some of these inflationary effects have been a little bit base effects because prices fell so hard in 2020. But we have seen consumption ticking up because of government stimulus. And we have to remember if the Fed is tightening things like mortgage backed securities, their purchases of mortgage backed securities will slow. Okay, so if people can’t refinance their house or buy new houses again, those wealth effects dissipate if you have a home. If your home price is rising, whether it’s the US or China or elsewhere, the wealth perception is there and people have a propensity to spend.

But if the Fed is pulling back on mortgage backed securities, then you won’t necessarily have that wealth effect that will dissipate. So government spending will decline marginally because build back better didn’t pass. We won’t have that sugar rush of government spending flowing into the economy early in 2002, although we may see something later. I believe governments love to spend money. So I believe the US government will come with some massive package later in the year to bring government spending back up.

SM: Tony, thanks very much for speaking to us. And an early Merry Christmas to you. That was Tony Nash, CEO of Complete Intelligence, giving us a quick take on what he sees moving markets in the final year. In the final weeks of 2021. Looking ahead to 2022.

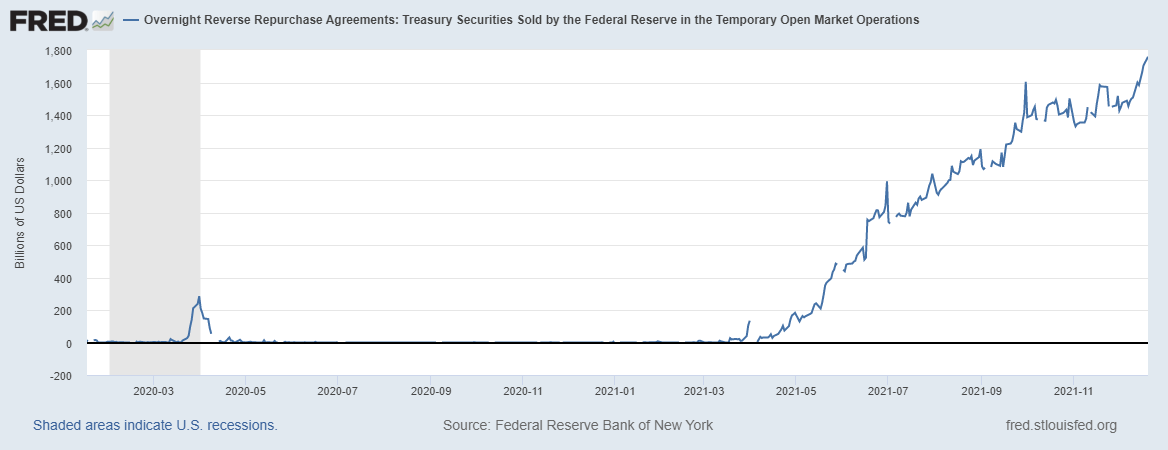

In the wake of the financial system’s cash glut and collateral shortage from the Fed’s quantitative easing program, the Secured Overnight Financing Rate drops to 0.04% from 0.05% on Monday, the first decline since October.

Even with asset purchase tapering underway, “it’s largely the same set of circumstances as in October,” TD Securities Strategist Gennadiy Goldberg told Bloomberg. “Lots of cash in the system and not a lot of collateral and that’s weighing down repo.”

Meanwhile, U.S. commercial banks park yet another record $1.75T at the Fed’s overnight repo facility, implying the banks are drowning in excess reserves, while searching for yield – which is scarce as most of the Treasury yield curve trades in net negative territory on an inflation-adjusted basis.

There’s an “incredibly large amount of cash sloshing the market,” said Complete Intelligence Founder Tony Nash via Twitter.

In August, the Fed’s overnight repo facility took up more than $1T.

Complete Intelligence – a fully automated and globally integrated AI platform for smarter cost and revenue planning.

Complete Intelligence provides actionable, accurate, and timely data to make better investment and procurement decisions.

The platform provides an integrated global model to ensure that actions in one market, country, or sector of the economy are reflected elsewhere in markets, industries, and the global economy. International trade, economic indicators, currencies, commodity prices, and equity indices are all factored in to create a proxy of the global economy. Over 1200 industries in more than 100 countries are covered!

Based on interviews with Tony Nash, founder, CEO, and Chief Data Scientist, this brief report introduces Complete Intelligence, one of a growing number of highly innovative companies supported by the Oracle for Startups program. The company, founded in 2019, is already significantly improving the forecasting and budget planning of a variety of large corporations through its advanced AI-driven intelligence platform. The theme for this month is around startups in the energy and utility sector and how they are innovating, changing the competitive landscape, and contributing to sustainability. CX-Create is an independent IT industry analyst and advisory firm, and this report is sponsored by the Oracle for Startups program team.

The business context for Complete Intelligence

Commodity price volatility and a post-pandemic surge in demand drive the need for more timely and accurate forecasting Businesses coming out of lockdown have increased demand for commodities, from energy supply to raw materials for their products. In Europe, benchmark prices for natural gas to power their factories and heat their buildings have risen from €16 megawatt-hour in January 2021 to €88 in October. This, in turn, has sent electricity prices soaring. (Source: Euronews). While some have locked in prices through forward-buying, others have been exposed and seen profit margins plummet, unable to pass on price hikes to their customers.

But it is not just energy prices that are volatile. Semiconductor chip shortages have impacted many industries that depend on them, from automotive to electronic household goods manufacturers, putting a brake on their post-pandemic recoveries despite strengthening demand.

The growing demand for clean and sustainable energy sources and precious metals, like copper and lithium that power batteries have also seen tremendous volatility. As major industrial companies digitally transform their organizations and business models seeking elusive growth, the importance of data and AI are increasingly recognized as fundamental to success.

Forecasting and budgeting needs data science, not spreadsheets The ability to sense change, respond quickly and adapt rapidly relies on a synthesis of massively increased volumes and varieties of data, both from operational and external sources. Data volumes are too complex for manual approaches and spreadsheets and require AI to extract insight and meaning from this complex array of external demand and supply signals. The old industrial-age planning approaches can’t cope. They are too slow, involve armies of accountants and analysts, and political wrestling between departmental heads, and are often based on opinion and inaccurate forecasts leading to erroneous budgeting decisions.

Complete Intelligence provides the accurate evidence base for budgeting and forecasting decisions

When markets are relatively calm and stable, the cycle of annual planning and budgeting makes sense. But amidst continual volatility and dramatic accelerated change, the planning cycle is too slow. It fails to mitigate the risks unfolding at such speed and is impacted by a confluence of so many variables, like extreme weather, scarcity of raw materials, pandemics, and weakened supply chains. An array of intelligent internal and external feedback loops is needed to mitigate risks and optimize resources in pursuit of the company’s goals. This is what Complete Intelligence provides with its integrated and modular intelligence platform.

Key observations

• Complete Intelligence provides the accurate evidence base for budgeting and forecasting decisions • The Complete Intelligence Platform consists of three modules – CI Futures, RevenueFlow and CostFlow • Forecast accuracy has rapidly improved, and error rates are now around 2%, which compares favorably with traditional methods and error rates of 35% or more

Complete Intelligence, the story so far

Tony Nash, founder, CEO, and Chief Data Scientist, is steeped in market intelligence. A former VP of market intelligence firm IHS (now IHS Markit), and The Economist Intelligence Unit, where he was Global Director Consulting and Custom Research. He observed that large international companies he had supported typically followed an annual budgeting cycle based on often inaccurate or opinion-based data. It was not unusual to find large teams of people, sometimes several hundred involved in the process and heavily reliant on gathering data from multiple departments in complicated spreadsheets. The process could last several months, and the variance between forecasts and actuals was often above 35%, which could erode profits or tie up resources unnecessarily.

Trial, error, and persistence As a data scientist familiar with cloud technologies, he developed algorithms to improve forecast accuracy and a complete process from data ingestion to forecasting and testing the results. He started developing the machine learning ML algorithms in 2017 while still consulting in Asia from his base in Singapore. His first iteration failed to produce a level of accuracy that would provide a sufficiently compelling proposition. He wanted to get down to an error rate of no more than 5%-7%. He adopted the ‘ensemble’ approach covering thousands of different scenarios layering external data on commodities such as the copper price with a customer’s actual costs, identified in their general ledger.

Ready for launch late 2019 In 2019, Nash returned from Singapore and set up his company in The Woodlands, near Houston, Texas. He continued his work on the algorithms and developed a commercial product ready to launch in early 2020. And then Covid-19 struck.

Through Covid-19, companies first tried to understand the changing environment, then remained risk-averse until public health, business environment, and supply chains became more stable. This has been a challenge for a cutting-edge machine learning firm like Complete Intelligence. It is only as the environment has begun to stabilize that enterprises have sought new solutions to legacy problems. With that has come a renewed interest in Complete Intelligence and deployment at a large scale.

Solution overview The Complete Intelligence Platform consists of three modules The Complete Intelligence Platform hosted on Oracle Cloud Infrastructure (OCI) consists of three forecasting modules:

•CI Futures – to forecast market trends. Covering over 1,400 industries in more than 100 countries and a database of over 16 billion data points from proprietary and publicly available data. Millions of learning algorithms are used, which factor in the most recent global events.

• RevenueFlow – provides accurate results for demand and forecast sales and revenue projections.

• CostFlow – to enhance product line profitability and improve supply chain and procurement outcomes.

Figure 1. provides a diagram of the Complete Intelligence Platform

Figure 1: Complete Intelligence Platform by Complete Intelligence.

Market data is ingested from multiple trusted data sources like national statistical agencies, multilateral banks, multilateral government bodies, commodities exchanges, bilateral trade bodies and combined with the client’s data from their general ledger. A multi-layer testing and validation process used to ensure the accuracy of the data to be used in any forecast. Third-party data is gathered via internet spiders and APIs.

The platform provides an integrated global model to ensure that actions in one market, country, or sector of the economy are reflected elsewhere in markets, industries, and the global economy. International trade, economic indicators, currencies, commodity prices, and equity indices are all factored in to create a proxy of the global economy.

A comprehensive list of futures, currencies, and market indices is covered and accessed through a highly graphical and easy-to-use interface. Almost 1,000 assets, with historical data from 2010 and forecasts over a one-year horizon, are provided. More assets are being added all the time.

The platform is designed around three attributes: • A globally integrated model • A data-driven process without human intervention in the output • A simple means of interfacing with the platform.

The platform can be connected to existing ERP systems and automatically upload pricing data from the general ledger at a very granular level for each item.

The Complete Intelligence Platform supports a variety of use cases: • Supply Chain & Purchasing Optimization – help lower costs, anticipate risks, and provide input to sourcing strategies. • Sales and market entry strategies – by identifying higher growth markets and optimizing resources • Strategic Financial Planning – identifying growth markets and fine-tuning resource allocations in each market to minimize exposure to currency fluctuations. • Mergers and acquisitions – provide a snapshot of cost structures and projections of future costs and profitability of target acquisitions.

Forecast accuracy has rapidly improved, and error rates are now around 2% Nash’s persistence has resulted in significant levels of forecasting accuracy. A twelve-month forecast now sees error rates around 2%, which gives users considerable confidence compared with traditional methods, where the error rates are often above 35%.

As well as dramatically improving forecast accuracy on markets, revenues, and costs, the onboarding process to going live is a matter of a few weeks. After that, forecasting takes hours, not months.

Current position

Successes to date

While still a relatively new company, Complete Intelligence has already proved its value to several large companies.

• A major petrochemical company wanted to improve its predictive intelligence capability for feedstocks and refined products. They asked Complete Intelligence to examine nine categories across crude oil, gasoline, diesel, natural gas, and gas-to-liquid (GTL) products. Monthly forecast averages are provided by category with extremely low differences from actual results on the order of 3% or less.

• A global furniture company wanted a more explicit link between their sales and revenue planning and their sales teams in China. Complete Intelligence built a sales forecasting model that more clearly identified and utilized market demand drivers and connected these directly to their business. An analytics-based approach to identify the drivers of sales by city and industry. Complete Intelligence built a city and industry-level forecasting tool that determined the company’s growth trajectory and provided recommendations to support the direction and transition of their sales teams. • A global chemicals company needed a better understanding of the trends for costs in their supply chain and a more precise way to manage margin expansion and contraction at the bill of material level. Complete Intelligence was commissioned to forecast factor inputs and currencies for the key categories. The forecasts were calibrated based on the component make-up of the bill of materials. This enabled the client to identify the direction of the materials pricing and the impact on their BOM. Through the process, the client learned how to anticipate cost movements and protect margins.

Current go-to-market model

Complete Intelligence sells directly to large organizations, mainly targeting CFOs and COOs with a broad view of their companies and strategic decisions.

The company also has strategic partnerships with Microsoft and is listed on the Azure Marketplace and with Oracle as part of the Oracle for Startups program and hosted on OCI.

Other partnerships with Bloomberg and Refinitiv allow for exchanging financial and market data and connection to their platforms.

More transparent accuracy reporting so customers can view accuracy/error for every line item

More robust and flexible data visualization for clients to utilize Complete Intelligence forecasts within their visual narratives

More sophisticated data science to account for detailed sentiment and other qualitative factors

Do-it-yourself forecasts for customers to do ad hoc forecasts for any data at any time. This will enable teams within a company to do their own sophisticated, reliable forecasts without waiting on their in-house market analysis or forecasting team with complicated macros and massive spreadsheet workbooks

Embedding Complete Intelligence forecast APIs into ERP and accounting software.

Oracle Cloud Infrastructure and the Oracle for Startups program prove their value to Complete Intelligence When asked what he felt about the relationship with Oracle and the Oracle for Startups program, Nash said, “Oracle Cloud Infrastructure is very flexible and secure. The Oracle for Startups team has been great. Oracle has been the most responsive and helpful of all our partnerships, connecting us to the right people to help with marketing, sales, or technical questions. I really feel that they want us to succeed. I’m a huge advocate of the Oracle for Startups program.’’

CX-Create’s viewpoint The Complete Intelligence Platform addresses a fundamental business need

Providing a global proxy model on markets, commodities, currency fluctuations, and many other aspects and making this easily accessible for business people will significantly improve strategic investment and procurement decisions. The emphasis on accurate and timely data supported by ML models will make it easier for business people to make informed decisions, stripped of personal bias. Digital transformation should lead to a more agile and responsive organization. The more progressive organizations will want highly attuned external signals that are constantly updated, enabling them to de-risk investment decisions and optimize resources for growth. Complete Intelligence provides for that.

Get 94.7% accuracy on your markets forecasts with CI Futures. Subscribe for only $50/mo for a limited-time only: http://completeintel.com/2022Promo

In this second part, Mike Green explains what will happen to Europe if China invades Taiwan. Will the region be a mere audience? Will it be affected or not, and if so, how? How about the Euro — will it rise or fall with the invasion? Also, what will happen to China’s labor in that case, and will Chinese companies continue to go public in the West?

📊 Forward-looking companies become more profitable with Complete Intelligence. The only fully automated and globally integrated AI platform for smarter cost and revenue planning. Book a demo here.

This QuickHit episode was recorded on December 2, 2021.

The views and opinions expressed in this What happens to markets if China invades Taiwan? Part 2 Quickhit episode are those of the guest and do not necessarily reflect the official policy or position of Complete Intelligence. Any contents provided by our guest are of their opinion and are not intended to malign any political party, religion, ethnic group, club, organization, company, individual or anyone or anything.

Show Notes

TN: So we have a lot of risk in, say, Northeast Asian markets. We have a lot of risk to the electronics supply chain. I know that this may seem like a secondary consideration. Maybe it’s not.

What about Europe? Does Europe just kind of stand by and watch this happen, or are they any less, say, risky than any place else? Are they insulated? Somehow?

I want to thank everyone for joining us. And please, when you have a minute, please follow us on YouTube. We need those follows so that we can get to the right number to reach more people.

MG: No, Europe exists, I would argue, as basically two separate components. You have a massive export engine in the form of Germany, whose core business is dealing with China and to a lesser extent, the rest of the world. And then you have the rest of Europe, which effectively runs a massive trade deficit with Germany. I’m sorry. Germany is uniquely vulnerable in the same way that the corporate sector is vulnerable in the United States. That supply chain disruption basically means things go away.

They are also very vulnerable because of the Russian dynamic, as we discussed. In many ways, if I look at what’s happened to Germany over the past decade, their actions on climate change and moving away from nuclear, away from coal into solar, et cetera, has left them extraordinarily dependent upon Russian natural gas supplies. It’s shocking to me that they’ve allowed themselves to get into that place. Right.

So my guess is that their reaction is largely going to be determined by what happens with Russia rather than what happens with China. Right. In the same way that Jamie Diamond can’t say bad things about China. Germany very much understands that they can’t say bad things about China.

Europe, to me, is exceptionally vulnerable, potentially as vulnerable as it has ever been in its history. I agree. It has extraordinary… Terrible way to say it. I don’t know any other way to say it, but Europe basically has unresolved civil wars from 1810, the Napoleonic dynamics all the way through to today, right. And everybody keeps intervening, and it keeps getting shoved back down into a false equilibrium in which everyone pretends to get along, even as you don’t have the migratory patterns across language and physical geographic barriers that would actually lead to the type of integration that you have with the United States, right.

Now ironically, the United States are starting to see those dynamics dramatically reduce geographic mobility, particularly within the center of the country. People are becoming more and more set in their physical geographies, et cetera. Similar to the dynamics that you see in Europe, which has literally 100,000 more years worth of Western settlement and physical location, than does the United States. But they’ve never resolved these wars. Right.

And so the integration of Europe has happened at a political level, but not at a cultural level in any way, shape or form. That leaves them very vulnerable. Their demographics leaves them extraordinarily vulnerable, the rapid aging of the populations, the extraordinarily high cost of having children, even though they don’t bear the same characteristics of the United States, but effectively the lack of land space, et cetera, that has raised housing costs on an ownership basis, et cetera. Makes it very difficult for the Europeans, and they have nowhere else to go now. Right. So the great thing that Europe had was effectively an escape valve to the United States, to a lesser extent, Canada, Australia, et cetera, for give or take 200 or 300 years, and that’s largely going away. Right.

We are becoming so culturally distinct and so culturally unacceptable to many Europeans that with the exception of the cosmopolitan environments of New York City and potentially Los Angeles, nobody wants to move here anymore. Certainly not from a place like Europe. I think they’re extraordinarily vulnerable.

I also think, though, that they’ve lost sight of that because they’re so deeply enjoying the schadenfreude of seeing the unquestioned hegemony of the United States being challenged. Right. It’s fun to watch your overbearing neighbor be brought down a notch. Right. You tend not to focus on how that’s actually adversely affecting your property values in the process.

TN: Sure. Absolutely. So just staying on Europe, what does that do to the importance of the Euro as an international currency? Does the status of the Euro because of Germany’s trade status stay relatively consistent, or do we see the CNY chip away at the Euros, say, second place status?

MG: Well, I would broadly argue that the irony is that the Euro has already peaked and fallen. Right. So if I go back to 2005 2006, you could make a coherent argument that there was a legitimate challenge to the dollar right.

Over the past 15 years, you’ve seen continual degradation of the Euro’s role in international commerce, if I were to correctly calculate it, treating Europe as effectively these United States in the same manner that we have with the US, there’s really no international demand for the Euro. It’s all settlement between Germany, France, Italy, et cetera.

If I go a step further and say the same thing about the Chinese Yuan or the Hong Kong dollar, right. They really don’t exist in international transactions. To any meaningful degree. The dollar has resumed its historical gains on that front. Now that actually does open up a Contra trade.

And I would suggest that in just the past couple of days, we’ve seen an example of this where weirdly, if the status quo is maintained, the dollar is showing elements of becoming a risk on currency as the rest of the world basically says some aspect of we’re much less concerned about the liquidity components of the dollar, and we’re much more interested in the opportunity to invest in a place that at least pretends to have growth left. Right. Because Europe does not have it. Japan does not have it. China, I would argue, does not have it. And the rest of the world, as Erdogan and others are beginning to show us, is becoming increasingly dysfunctional as a destination for capital. Right.

Brazil, perennially the story for the next 20 years and always will be right. Africa, almost no question anymore that it is not going to become a bastion for economic development going forward. And we’re broadly seeing emerging markets around the world begin to deteriorate sharply because the conflict between the United States and China creates conditions under which bad actors can be rewarded. Right.

If I sell out my people, we just saw this in the Congo, for example, if I sell out my people for political influence, I can suddenly put tons of money into a bank account somewhere. Right. China writing a check for $20 million. It’s an awful lot of money if I’m using it in Africa.

TN: For that specific example, and for many other things, the interesting part is China is writing a check for $20 million. Yeah, they’re writing a check for €20 million. They’re not writing a check for 20 million CNY. It’s $20 million. All the Belt and Road Initiative activities are nominated in dollars.

So I think there’s a very strange situation with China’s attempt to rise, although they have economic influence, they don’t have a currency that can match that influence. And I’m not aware, and you’re such a great historian. I’m not aware of an economic power that’s come up that hasn’t really had its own currency on an international basis. I’m sure there are. I just can’t think of many.

MG: Well, no. I mean, the quick answer is no. You cannot project power internationally unless effectively the tax receipts of your local population are accepted around the world. Right? Broadly speaking, I would just highlight that the way I think of currency is effectively the equity in a country right now. It’s not a perfect analog, but it’s a reasonable analog. And so, what you’re actually saying is the US remains a safe haven. It remains a place where people want to invest. It remains a place where people believe that the rule of law is largely in place. And as a result, anyone who trades with the United States is willing in one form or another to say, okay, you know what? I can actually exchange this with somebody who really needs it at some point in the future.

I think one of the reasons that we tend to think about the dollar as having fallen relative to the Euro or the CNY is we have a very false impression of what the dollar used to be. Right. So we tend to think about the dollar was the world’s reserve currency following World War Two and everything happened in dollars. Right.

People forget that half the world, certainly by population, never had access to dollars, never saw dollars. There was a dollar block. And then because of their refusal to participate in Bretton Woods, there was a Soviet ruble block and then ultimately far less impactful things like a Chinese Yuan, et cetera. But the Soviets, for a period of time, had that type of influence. They could actually offer raw materials. They could actually offer technology. They could offer things that had the equivalent of monetary value to places like Cuba, to places like Africa, to places like South America, et cetera. China right.\

That characterized the world from 1945 until 1990. Right. I mean, the real change that occurred and really in 1980 was that Russia basically ran out of things to sell to the rest of the world, particularly in the relative commodity abundance that emerged in the 1980s after the 70s, their influence around the globe collapsed.

And I think the interesting question for me is China setting up for something very similar. Right. It feels like we’re looking at a last gasp like Brisbanev going into Afghanistan, right. And oh, my gosh, they’re moving out and they’re taking over. Well, that was the end. They make a move on Taiwan. And I think a lot of people correctly point to this. It’s probably the end of China, not the beginning of China.

I just don’t know that China knows that it has an alternative because it’s probably the end of China, regardless.

TN: Sitting in Beijing, if you bring up any analogues to the Soviet Union to China in current history, they’ll do everything to avoid that conversation. They don’t want to be compared. Is Xi Jinping, Brezhnev or Andropov or. That’s a very interesting conversation to have outside of Beijing. But I think what you bring up is really interesting. And what does China bring to the world? Well, they bring labor, right. They’re a labor arbitrage vehicle. And so where the Soviet Union brought natural resources, China’s brought labor.

So with things like automation and other, say, technologies and resources that are coming to market, can that main resource that China supplied the world with for the last 30 years continue to be the base of their economic power? I don’t know. I don’t know how quickly that stuff will come to market. I have some ideas, but I think what you’re saying is if they do make a play for Taiwan, it will force people to question what China brings to the world. And with an abundance of or, let’s say, a growing influence of things like automation technologies, robotics, that sort of thing, it may force the growth of those things. Potentially. Is that fair to say?

MG: I think it’s totally fair. And I would use the tired adage from commodities. Right. The cure for high prices is high prices. If China withdraws its labor or is forced to withdraw its labor from the rest of the world, there’s two separate impacts to it.

One is that China’s role as the largest consumer of many goods and services in things like raw materials, et cetera. That has largely passed. Right. And so as we look at things like electrification, sure, you can create a bid for copper. But at the same time, you’re not seeing any building of the Three Gorges again. Right. You’re not seeing a reelectrification of China. You may see components of it in India. And I would look to areas like India as potential beneficiaries of this type of dynamic. But we’re a long way away from a world that looks like the 20th century. And you’ve heard me draw this analogy. Right. So people think about inflation.

The 20th century was somewhat uniquely inflationary in world history. The reason I think that happened is because of a massive explosion of global population. Right. So we started the 20th century with give or take a billion people in the global population. We finished the 20th century with give or take 7 billion people. So roughly seven X in terms of the total population. The labor force rose by about five and a half X.

If I look at the next 100 years, we’re actually approaching peak population very quickly. And if I use revised demographic numbers following the COVID dynamics, we could hit peak global population in the 2030s 2040s. Right. That’s an astonishing event that we haven’t seen basically since the 14th century, a decline in global population. And it tends to be hugely deflationary for things like raw materials. Right. People who aren’t there don’t need copper, people who aren’t there don’t need houses, people who aren’t there don’t need air conditioners, et cetera.

I think the scale of what’s transpiring in China continues to elude people. I would just highlight that we’ve all seen examples of this. Right. So go to any Nebraska town where the local farming community has been eviscerated with corporatization of farms, and the population has fallen from 3000 people to 1000 people. What’s happened to local home prices? What’s happened to the local schooling system? What’s happened to deaths of despair, et cetera. Right. They’ve exploded. China’s facing the exact same thing, except on a scale that people generally can’t imagine. The graduating high school classes are now down 50% versus where they were 25 years ago. That’s so mind blowing in terms of the impact of it.

TN: That’s pretty incredible. Hey, Mike, one of the things that I want to cover is from kind of the Chinese perspective. Okay. So we’ve had for the last 20-25 years, we’ve had Chinese companies going public on, say, Western exchanges and US exchanges. Okay. So if something happens with Taiwan, if China invades Taiwan, do you believe Chinese companies will still have access to, say, going public in the US? And if they don’t, how do they get the money to expand as companies?

Meaning, if they can’t go public in the west, they can’t raise a huge tranche of dollar resources to invest globally. So first of all, do you think it’s feasible that Chinese companies can continue to go public in the west?

MG: Yeah. Broadly speaking, I think that’s already over. Right. So the number of IPOs has collapsed, the number of shell company takeovers has collapsed. So the direct listing dynamics. I just had an exchange on Twitter with a mutual friend of ours, Brent Johnson, on this. Ironically, that would actually probably help us equities for the very simple reason that the domestic indices like the S&P 500 and the Russell 2000 do not include those companies. Right.

So if those companies fail to attract additional capital or those companies are delisted, it effectively reduces competition for the dollars to invest in US companies and US indices. Where those companies are listed and are natively traded, at least are in places like Hong Kong, China, et cetera, those are incorporated in emerging market indices. And I would anticipate, although it certainly has not happened yet. That on that type of action, you would see a very aggressive move from the US federal government to force divestiture and prohibit investment in countries like China.

I think that would very negatively affect their ability to raise dollars. Again, and I mean, no disrespect when I say this. I want to emphasize this, but we tend to think of Xi Jinping as this extraordinarily brilliant, super thoughtful, intelligent guy. The reality is he’s kind of Tony Soprano, right? I mean, it’s incredibly street smart, incredibly savvy, survived a system that would have taken you and I down in a heartbeat. Right. You and I would have been sitting there. Wow. Theoretically, someone would have shot. Congratulations. Welcome to the real world, right. He survived that system. But that leaves him in a position where I do not think that he’s actually playing third dimensional chess and projecting moves 17 moves off into the future. I think he very much is behaving in the “Ohh, that can only looks good.”

I think it’s really important for people to kind of take a step back and look at that in the same way that Japan wasn’t actually forecasting out the next 100 years. The Chinese are not doing that. It’s a wonderful psychological operation. One of the best things that people can do is go back and relisten to the descriptions of IBM’s Big Blue computer or Deep Blue. I’m sorry beating Gary Kasparov. Right. So one of the things that they programmed into that computer was random pauses. So the computer processed things and computed things at the exact same speed. But by giving Kasparov the illusion that he forced the machine to think, he started to second guess himself.

Well, what did I do there that made it think, right. He didn’t do anything. It was doing its own thing and designed to elicit a reaction from you. I think China’s done probably a pretty good job of getting a lot of people in the west and elsewhere. And I think Putin is even better at this, of second guessing our capabilities and genuinely believing that we’re second rate now.

It’s fascinating. There was just a piece that came out from the US Space Force where they’re talking about the rising capabilities of China. And if you read the public Press’s interpretation of this, China is moving ahead in leaps and bounds. And what actually he’s saying is, no, we’re way ahead. But they are catching up at an alarming rate.

TN: That’s what happens. Right.

MG: Of course, it is always easier to imitate than it is to innovate.

TN: Right. When I hear you say that it’s easier to imitate than innovate. I know you don’t mean it this way, but I think people hear it this way that the Chinese say IP creators are incapable of creating intellectual property. I don’t think that’s the case. I don’t think you mean that to be the case. They are very innovative. It’s just a matter of baselining yourself against existing technology. So it does take time to catch up. Right. And that takes years. Your TFP and all the other factors within your economy have to catch up. And it takes time. It takes time for anybody to do that.

MG: Well… And I think also it’s important to recognize that things like TFP, total factor productivity, tends to be overstated because we don’t do a great job of actually correctly defining it.

TN: It’s residual. I can tell you.

MG: Exactly right. And just to emphasize what that means, it means it’s the part that we can’t explain with the variables we’ve currently declared. Right.

TN: Right.

MG: And so when I look at TFP in the United States, I actually think TFP is quite a bit lower than the data sets would suggest, because I think that we are failing to consider the fact that we’ve introduced women into the labor force. We’ve introduced minorities into the labor force. Right. So the job matching characteristics or the average skill level of people has risen.

People live longer, so they get to work in different industries and careers for a longer period of time. The center of the distribution is now starting to shift too old, and that’s showing up as a negative impact. But we failed to consider that on the other side. And the last part is just again, remember going back to the start of the 20th century, the average American had three years worth of education at that point. Third grade education, where a year was defined as three months, basically during the non harvest season. Right.

TN: It’s the stock of productivity. Correct. We’re adding to that stock of productivity, and the incremental add is large compared.

MG: But small compared to the stock. Absolutely correct. Right.

TN: Okay. Just to sum up, since we wanted to talk about the impact on markets, I want to sum up a couple of things that you’ve said just to make sure that I have a correct understanding.

If China is to invade Taiwan, we would have in Northeast Asia a period of volatility and uncertainty. That would go across equity markets, across currencies, across cross border investments and so on and so forth. Okay. So we would have that in Northeast Asia.

MG: And I would just emphasize very quickly. So we’ve seen this rolling pattern of spikes in volatility. Right. So we saw it in 2018 in the equity markets. We saw it in late 2018 in the credit markets and commodity markets. We’ve now seen it in interest rate markets. What’s referred to as the Move index. The implied volatility around interest rates has reached relatively high levels of uncertainty.

The one kind of residual area where we just have seen no impact whatsoever has been in FX. That has been remarkably stable, remarkably managed. That’s kind of my pick for the breakout space.

TN: Okay. Great. Europe also appeared of volatility because of their exposure to both China and Russia. Since both China and Russia have a degree of kind of wiliness, especially Russia, I think almost a second derivative. Europe is volatile because of both of those factors. Is that fair to say? And that has to do with the Euro that has to do with their supply chains? That has to do with a number of factors.

MG: I would broadly argue that’s a reasonable way to think about it. I mean, almost think about it. Flip the image and imagine that the continents are ponds and the oceans are land. Right. What we’re describing is a scenario where a rock gets dropped into Asia or a rock gets dropped into Europe. You will see the waves spread across. There’s potential for sloshing over, and it’ll absolutely impact the United States. But in that scenario, we literally have two giant barriers in the form of the Pacific and the Atlantic Ocean that separate us.

And while our supply chains are integrated currently, in a weird way, COVID has been a bit of a blessing in starting to fracture those supply chains. We’ve diversified them significantly in the last couple of years.

TN: Okay. And then from what I understand from what you said about the US is supply chains will definitely be a major factor. Corporates will likely keep their investments in China until they can’t. They won’t necessarily come up with, say, dual supply chains or redundant supply chains.

US equity markets could actually be helped by the delisting of Chinese companies. Or we’ll say, US listed equities, meaning US companies listed could be helped by the delisting of Chinese equities, potentially.

MG: Certainly on a relative basis. I might not go so far as to say in an absolute simply again, because you do have people and strategies that run levered exposures. And so anytime asset values in one area of the world falls, you run the risk that the collateral has become impaired, and therefore there’s a deleveraging impact.

TN: Yes. Understood. And then the dollar continues to be kind of the preeminent currency just on a relative basis because there really isn’t in that volatile environment, there aren’t many other options. Is that fair to say?

MG: Well, again, I think there’s an element of complication. I would prefer to argue volatility. I think it is hard to argue that the dollar wouldn’t appreciate, but I also think it’s important, and this is why I go back and say we can’t actually stop Russia from taking Ukraine. We can’t stop China from taking Taiwan.

If they were to actually do that, then there is kind of the secondary loss of phase dynamic associated with it that may you could see and you’ve already seen Myanmar. You could see Thailand. You could see Vietnam. Say, you know what? We got to switch. I’m skeptical, but I’m open to that possibility.

TN: Interesting. Okay. Very good. Mike, thank you so much for your time. I really appreciate how generous you’ve been with what you’ve shared. I’d love to spend another couple of hours going into this deeper, but you’ve been really generous with us.

I want to thank everyone for joining us. And please, when you have a minute, please follow us on YouTube. We need those follow so that we’ve we can get to the right number to reach more people.

So thanks again for watching. And Mike Green, thanks so much for your thoughts on China’s invasion of Taiwan.

Get 94.7% accuracy on your markets forecasts with CI Futures. Subscribe for only $50/mo for a limited-time only: http://completeintel.com/2022Promo

In this QuickHit episode, we’re joined by Mike Green to talk about what will happen if China invades Taiwan? We’re not saying that China is going to invade Taiwan, but what if it is to happen? What will be the impact to markets?

Mike Green is the chief strategist and portfolio manager for an ETF firm called Simplify Asset Management. They specialize in derivative overlays and derivative structures that modify the traditional market exposures. Their flagship products are things like US equities with downside protection.

His background prior to Simplify, has been in hedge funds for about 15 years and have built an expertise or a degree of renowned for the work that he does in primarily the derivatives and volatility space and have managed traditionally in what’s referred to as a discretionary global macro style. The assets that he purchases or that he monitors exist around the world, including places like China, Taiwan, et cetera.

A lot of the discussions Tony and Mike have had around Taiwan are tied to some geopolitical observations and some dynamics that exist in which Mike played a role less under the Biden administration. But in the prior administration had an advisory capacity to some components of the Department of State and Department of Defense.

📊 Forward-looking companies become more profitable with Complete Intelligence. The only fully automated and globally integrated AI platform for smarter cost and revenue planning. Book a demo here.

This QuickHit episode was recorded on December 2, 2021.

The views and opinions expressed in this What happens to markets if China invades Taiwan? Quickhit episode are those of the guest and do not necessarily reflect the official policy or position of Complete Intelligence. Any contents provided by our guest are of their opinion and are not intended to malign any political party, religion, ethnic group, club, organization, company, individual or anyone or anything.

Show Notes

TN: So today we hear or any day, pick a day. We hear that China is invading Taiwan. What are the first things that come to your mind as the news crosses the wires?

MG: Well, I think there’s a couple of things that are really important about the question of is China invading Taiwan, right. And so what we have seen very clearly, and this is fact, not speculation, is a dramatic escalation of China’s incursion on what would traditionally be thought of as Taiwan sovereignty or independence. Right.

We’ve seen a dramatic increase in boats transitioning across the international marine borders. We have seen a dramatic increase in incursion of both fighter jets and bombers into Taiwanese airspace. And in general, the strategy that you see China engaged in is what is typically thought of as a precursor to an invasion. They’re effectively forcing Taiwan to maintain alertness and readiness, which slowly degrades the quality of defenses.

If you have to constantly scramble jets, there’s only so many hours that you can actually have them in the air. There’s only so many hours you can have pilots operating before their capability deteriorates. That is very clearly what is in play here.

Now, it’s an unknown question whether they go to the next step, whether they take what is currently a largely psychological and relative resource advantage to degrade Taiwan’s capabilities, whether they turn that kinetic as compared to hoping for a psychological collapse where Taiwan effectively decides to sue for the best possible deal they can get is unclear.

And I think that’s really what we’re all debating. I mean, China has come out very clearly. Others have made this observation, and it’s not dissimilar to my former employer, Peter Thiel’s observation about Donald Trump, right. That everyone takes him literally, but not seriously. I would flip that on its head. And everyone say everyone takes Xi seriously, but not literally when he says we will reunify with Taiwan in one form or another within the next five years.

And that’s the core of the question. Are they going to do this in a peaceful fashion? Are they going to do it in a kinetic military fashion? What are the ramifications of each of those two strategies and what’s the state of gameplay that is in place right now, as each side including the allies of Taiwan in the form of Japan, the United States, et cetera, evaluates how they want to respond to it.

TN: Right. What is that? What are those initial responses that you think happen, setting aside battle plans, of course. Honestly, I don’t believe that Min Def or DoD know 100% of whether this will happen or not. I think everything is a potential.

What do you think those reactions are initially in terms of, say, markets, investments, even things like trade? Those are like, what do you think happens right away?

MG: Well, I think there’s a couple of things that are worth hitting on. Right. So the first is why does China want Taiwan or why does it matter? Right. So one component is just the psychological final victory over the Republic, the Taiwanese Republic, what is known as the Republic of China outside of the area.

When you think about that dynamic, this is a final victory that would allow Xi to place himself permanently on par with the founders of the Chinese Communist state. Right. The Mao’s, et cetera, of the world. So this is a huge accomplishment.

I think there’s a huge misunderstanding that the objective is to obtain the semiconductor resources, right. To me that feels, one, extremely unlikely to expect that they could do that successfully, and two, I’m not sure it’s actually entirely relevant. Right. But that does then speak to the indications that the game is being taken much more seriously.

And so one of the things that I would point to people is the dramatic expansion of capabilities and investment that Taiwan is making in Arizona, where they’ve effectively doubled on a nameplate capacity and potentially up to 5x the capacity of TSMC in Taiwan. Now, that’s a huge implication.

If we were to put ourselves back into the 17th century, it would be the akin of a European sovereign entity, a small Principality, taking the Crown jewels and shipping them for safekeeping somewhere further away when they were faced with a threat, taking the error apparent and shipping them abroad so that there’s a base of operations. If you think about TSMC’s investment in Arizona, that can be very easily thought of as a base of operations and a source of income for a government in exile. Right. So I don’t think Taiwan is planning on going away.

It also opens up kind of the interesting angle of how effective is China’s strategy, because I think that China broadly looks at it and says, we can wear them down and I would point to it and say, yeah, your best opportunity was actually probably a year ago to use the element of surprise. Now you’ve pretty well telegraphed it. Taiwan has made significant advances. The US Department of Defense, in particular, I would argue, would have been caught very much off guard a year to a year and a half ago. Today they’re pretty much on top of this, right.

The Pacific Theater has been opened pretty widely. You’re actively hearing expressions of support from South Korea, Japan, et cetera. So to me, it feels like the element of surprise has been lost, and now it just becomes a question of, is this ultimately going to happen? It seems extremely unlikely to me that it will be a long term successful component.

Then you have to ask yourself the last question, which is, why does China care beyond simply the moral victory or the desire for that? And that’s where you and I have been through these maps. And I don’t know if we’re doing this in a visual format, but I could share it if you wanted to.