Our CEO and founder, Tony Nash, joins the BBC Business Matters podcast to discuss mainly the anniversary of the US Capital riot — and why most Americans don’t really care anymore. Also discussed are the patent-free Covid vax and the CES 2022 and the coolest thing in the event.

FN: Let’s go to Tony and the view from Texas. And I’m just wondering, Tony, we talked about, you know, viewing this from outside the nation’s capital. What have people been talking about today?

TN: Fergus, I gotta be really honest. No, nobody cares. I talked to students. I talked to business people. I talked to people across the country, and this is a DC event, and it’s drama that DC has conjured up and nobody in the rest of the country really cares. It’s just not a big deal for people.

FN: Okay, I’ll tell you why. I find that interesting. One thing. People travel to DC, right? For this event, whether they attended the rally or whether they actually went to the capital and took part. They weren’t DC residents, all of them. And the second thing is it’s a political thing right now, surely, across the country, there are politicians running on this event as a mandate. No?

TN: I don’t think so. No, I don’t think there are politicians running on this. You may have some politicians who are trying to run on this, but honestly, I just spoke to a couple of College students an hour ago and asked them what they thought about it. They didn’t care. I spoke to business people today and they just didn’t care. And they shrug it off as just something that’s in DC, and they shrug it off as the administration trying to distract attention. That is in the middle of the country.

That is the view from Chicago down to Texas and across the middle of the country. Nobody cares. And even in the capital building. So if these guys really wanted to overthrow the government and harm Congress people, they would have gone to the administrative buildings. I mean, these aren’t stupid people, but nobody else cares.

KA: I’m sorry, that’s not accurate. They were in the capital building.

TN: It is. Absolutely. We were in the administrative building.

TN: There were Congress people who weren’t even close to the administrative building.

FN: So, demonstrators sitting in the Speaker’s chair. Right.

TN: The demonstrators were there. The Congress people weren’t there at the end of the day. Fergus, look at the end of the day here’s what we’re talking about. We’re talking about trespass and we’re talking about property crime. Okay. That’s why people don’t care.

FN: There were five fatalities.

TN: Yeah. The Capitol police shot a woman. Right.

FN: Tony, I want to pick up on your point about people in Chicago down to Houston, not caring. This is what you’re reflecting to us about. Hang on. Let me please ask. Does that mean that nobody from Houston up to Chicago, et cetera, in the middle of America believes the message that was behind this campaign because it strikes me that 48% of the Republican Party believe the message behind what happened a year ago.

TN: What message is that, Fergus?

FN: That the election was stolen. This is the message that President Trump continues. A former President Trump continues to put out and the message that those demonstrators sought to enact as they see it. When you say people don’t care, you’re suggesting that it’s done and dusted. And I’m suggesting to you that’s far from the case.

TN: I think it is done and dusted. And I think if you look at people like Ashley Babbitt, who was shot in the back as she was entering like she was unarmed and shot at the back, these were not people who were fighting for something. Right.

FN: All right. Tony, come in. You want to jump in there?

TN: Yeah. I think Rachel is absolutely right. With the Pelosi’s support of the storming of the entry into Ledgeco in 2019, I think the Apathy in the US is really just more exhaustion than anything. I think Americans are just tired of the partisan nonsense. They’re just exhausted by it. And I think people don’t care because they don’t see this coming to an end. And DC is a world unto itself. And most of America just doesn’t care anymore. Honestly.

FN: But at that point and Rachel’s point, I was just reflecting on some of Carrie Lam’s comments exactly a year ago. And this phrase double standards, she said foreign audience should set us. Do Americans recognize that as double standards?

TN: Oh, absolutely. Yes, absolutely. They do. Well, most do not all, of course. But I think most do. If you were to rewind to 2019 and show those tapes to many Americans, they would completely get it. We’re not the Cretans that everyone tries to make us out to be. We understand that.

FN: Tony Nash is with us from Houston, may well be familiar with many of the names we’ve been discussing in the last five, six minutes. Tony, let’s focus on the philanthropy first. Presumably, that’s something you recognize that when you don’t get federal funding, you don’t get the big sort of specific targeted funding that a lot of big Pharma got back at the beginning of the pandemic. You reach into donor sections.

TN: Sure. Yeah, absolutely. And I think the Baylor College of Medicine did fantastic work here with the resources they had, and everyone here is proud of them. Texas is a huge force in medical like in public health, in oncology in many areas of healthcare. And this is just a very public view, public way of doing it. I love what they’re doing. It’s hard not to love what they’re doing.

FN: In terms of the generic issue. We’ve heard a lot about big Pharma is, I guess, easy to demonize, because a lot of the companies are making some very big returns on vaccines, and these people seem to be ready to maybe not give up the whole game, but essentially go for the generic version so that it can be spread more quickly and more cheaply.

TN: Well, all of the private sector vaccine developers, I think they got $20 billion from the US government in 2020, so those medicines have been paid for. They should give them out for free. All their IP should be open source. There should be nothing secret. The American people paid for the ones that were developed in the US. And I think as a foreign policy, we should open source that and let every country develop it at whatever cost they can.

FN: It would be a fantastic kind of diplomatic soft power, too. Wouldn’t it be?

TN: Absolutely would.

FN: And, Tony, I’m not sure how much you heard. There a quick thought from you as we end the program on the survival of Tech despite the pandemic?

TN: I think tech has thrived in the pandemic. And I’m glad to see shows like CES happening where people can go in person or be remote. I think it’s great to be in person. So I’m really happy to see it. And the coolest thing I saw at CES was a car that could change color because of nanotechnology in the paint. That was the coolest thing I saw there.

FN: Yeah, I saw that one online as well. That’s the purple thing I was referring to. Kind of Sci-Fi is real, I guess. All right, Tony, thank you very much. Indeed. Glad we got you back. Briefly. Sorry we lost the line halfway through there.

Markets are tanking on concerns that rate hikes might occur sooner than expected, hence the possibility that heightened volatility and a flight to value havens could be in store for 2022, according to Tony Nash, CEO, Complete Intelligence.

KHC: Good morning. This is BFM 89 nine, five minutes past seven in the morning, 6 January 2022. I’m Khoo Hsu Chuang and I’m joined by Philip See. Okay, let’s also recap how global markets closer today, Phil.

PS: Yeah. Markets in the US really didn’t enjoy the fair minutes. So the Dow is down 1% SMP 500 down 1.9% Nasdaq also down 3.2% across over in Asia mixed the Nikkei was up zero 1% Hang Sing down 1.6% Shanghai Composite down 1% Singapore STI down 6%. But back home as FBMKLCI was up zero 4%.

KHC: Of course, markets are being rented all over the world because of the Fed minutes, which disclose that JPowell might introduce higher rates as early as March. So for some thoughts on what’s moving these markets, we now talk to Complete Intelligence Chief Executive Tony Nash. Tony, good morning. Now we are talking about how financial markets are being crushed everywhere, including in the US by the Fed minutes, which is just faster and higher rate hikes. Maybe as early as March. Do you share the same sentiment?

TN: Yeah. I think it’s a little bit weird. So it makes sense for the Fed to stop buying things. So they buy, like mortgage backed securities so that they can put money into the market. So those are things that go onto their balance sheet. So they’ve acquired trillions of dollars worth of assets in order to support markets and get money into the system. So it makes sense to taper off the things they buy. But it doesn’t make sense to raise interest rates because people are complaining about inflation.

Right. And so if people can’t afford stuff, the major issue is stop putting money into the market don’t necessarily raise the cost of money, which is what interest rates are. So the markets feel like Powell has things a little bit out of order and that he needs to just stop putting money in the market before he raises rates. It may be appropriate to raise rates later in the year, but not just yet. So people think this is a little bit preemptive. So I would expect to see statements to walk back this Fed meeting over the next couple of days or week.

KHC: Well, the thing, Mr. Tony, according to the Bloomberg and markets being the forward indicators, that they are the Bloomberg, that there’s going to be a 71% chance that there’s going to be a rate hike as early as the March 16 meeting for the FOMC. What do you make of that?

TN: I see that. But that’s a forecast by economists. So I’d love to see the error rates of the economists. So I think that the real expectation is around the market welcoming of that. So is it possible they raised by March? Yeah, it’s possible. I think they need to start the paper first to see how likely it is, because again, the major issue is inflation and raising interest rates is a very old school way of fighting inflation before we had the tools that we have right now brand QE QE and other things.

PS: So getting a perspective. Clearly, what we saw in the nest was 3% down. I think interest rate sensitive stocks like tech stocks, I think were biggest hit. Is it time to take some money off the table after a good run?

TN: Sure. Yeah. That’s definitely part of the calculation. Absolutely.

PS: And then the question is, do you rotate it into value?

TN: Well, I think what we’re expecting probably sooner rather than later. We saw some big moves today, but yeah, there is expected irritation out of tech. We’ve seen people load up on tech and durable goods over the past two years. They’re way overstretched. So we do expect tech to see some serious downside over the next quarter, two quarters. And we do expect a rotation more into traditional industries, what people would consider boring industry. So people who make stuff like actually make stuff, even things like tourism and those sorts of things.

So we expect to do some rotation there.

KHC: Yeah. Tony, the other spectre is obviously the covered variants. IHU and of course Florona as well. Assuming that you are right in the possibility of the Fed walking back comments about the March rate hike or the possibility of a March rate hike. Right. What would the smart money be doing now in terms of possibly buying to the dip and getting a nice bounce from a short term trading perspective?

TN: Well, I think you have to look at things like energy, which has gotten a lot of attention over the past week. I think you have to look at what opportunities will there be if the variant slows down and money remains cheap. Okay. So if we’re not going to see a dramatic rise in interest rates from the Fed, then you may have some legs on some things like real estate. I’m not sure. But you may I’d have to do some research there, but I think you really need to look at things like tourism and people getting out Airlines.

Those sorts of things really have to think about when people start to get out in force, what kind of difference can be made in markets?

KHC: I think you quite rightly pointed out that increasing interest rates is a very old fashioned way of dealing with inflation. What, in your opinion, are possibly alternative solutions to addressing higher costs, which is definitely a reality today.

TN: Look, a lot of the issue is on the supply side. So you raise interest rates when the issues are on the demand side and the demand side peaked in 2020 after the Fed just released a huge amount of money on to US citizens. So a lot of the issues are supply chain issues, and they’re on the supply side. So better to reduce or taper off the supply of money going into the system and focus on building out supply chain so if there were an infrastructure bill that came and said, we’re going to focus on these supply chains and make them more robust.

And we’re going to focus on near shoring manufacturing to reduce the length of the sophistication of those supply chains. I think that’s really all that they can do right now to focus on that supply side. So in short, interest rates aren’t going to help. There has to be a more medium and long term investment in Shoring up the supply side. Yeah. I agree with you.

PS: I think that’s a very medium long term outlook. And I just wondering how earnings will look like this year.

TN: Well, certainly not going to look like 20 or 21. A lot of the 21 interest earnings were up until, say Q3, there were effects based on expenses that were cut in 20. There was a lot of headcount reduction and real estate reduction in 20 because of work from home and staff reduction, those sorts of things. So 22 is going to be harder. It’s going to be a much more disciplined old school efficiency, automation and top line growth type of environment.

KHC: Well, Tony, given that we are only six years, six days into the new year, how should asset allocation strategies look like for the conservative investor in 2022?

TN: You know, you’ve got to really be careful of volatility and you’ve got to be careful of risk, even things like political risk, which is what’s happening in Kazakhstan today. We really have to be careful of political risk in market. So with the events in Kazakhstan, then I think you’ll start to see people really take another look at Em and try to figure out how much risk are in those investments. You may see people steer away from em because of that risk. So I think you’re going to see more consideration for developed markets.

You may even see more consideration for Europe. I think Europe may have a good year this year.

PS: And I wonder if there’s a consideration for traditional safe havens like gold, US dollar and treasury spend.

TN: Yeah. Well, that certainly supports the dollar, Treasuries and so on. Gold. I’m not so sure about gold may have some upside, but the focus on developed markets may will definitely support the US dollar and Treasuries.

KHC: All right, Tony, thank you so much for your time. And that was Tony Nash, the chief executive of Complete Intelligence, talking about the Fed minutes, which I have perturbed markets in a significant way.

PS: I think markets are factored in the tapering, but not the interest rate moving earlier.

KHC: Yeah.

PS: That’s why you saw the tech heavy Nasdaq really hit quite badly with 3.2% decline.

KHC: Yes. And of course, we saw the Bloomberg indicators surveying economists a 71% chance that there’s going to be a rate hike at the March 16 meeting.

PS: Incredible.

TN: Right.

PS: You know, you talk about just four or five months ago, we were talking about only two hikes at best, in June. And now we’re seeing things shift very fast.

The full episode was posted at https://www.channelnewsasia.com. It may be removed after a few weeks. This video segment is owned by CNA.

Show Notes

CNA: Welcome back to Asia First. Wall Street took a hit overnight amid concerns that a rise in Omicron cases would stall growth and add to inflationary pressures. Experts say supply chains and corporate profits could be dealt another blow as the possibility of increased restrictions is back on the table.

The Dow and the Nasdaq tumbled 1.2 percent. The S&P 500 closed 1.1 lower, with financials and materials among the biggest decliners. Also weighing on sentiment, Goldman Sachs has lowered its US growth forecast for next year. This after Senator Joe Manchin said over the weekend he would oppose President Biden’s 1.75 trillion dollar spending bill.

Let’s bring in Tony Nash. Now, he’s founder and CEO of Complete Intelligence, joining us from Houston, Texas. Lots to talk about today, Tony. So let’s start with Omicron. How much do you think potential measures are going to dent economic growth given the spread of the highly transmissible variant coinciding with the end of the era of cheap money?

TN: Yeah, it’s a good question. I think it really depends on where in the US you are. I’m in Texas and in in certain parts of the country you could barely tell that there’s a pandemic. There aren’t restrictions at all here, in Florida and other places. And also, we had our surge a couple months ago. So we’re on the downside of that surge now.

In the north, where you have kind of seasonal viruses, they’re on the up upward motion of the surge and so there’s a lot of sensitivity in northern states like New York, Boston, or Massachusetts, Washington DC, Michigan those sorts of places. So I think what you’re seeing is a kind of seasonal sensitivity because of Omicron and people getting nervous and so you know, again it really all depends where you are in the US.

For the upcoming Christmas break, flights are packed. Americans are traveling again. These sorts of things are happening. So, of course, there’s always a risk that people will do a hard lockdown like DC has put in some new measures today. But other places are seeing the virus as endemic and just kind of trying to move on with it. So, I think it could go either way but I don’t necessarily think we’ll have sustained negative impact. We could have short-term negative impact.

CNA: What about the risk from Fed moves and do you think the projected three rate hikes next year are going to be enough to contain inflation given the potential for Omicron to cause these price pressures to spike?

TN: Sure. You know, I do think that the Fed will pursue the tightening, meaning of its balance sheet pretty quickly. I think the rate hikes they’ll probably do one and wait and see and then they’ll proceed with the others later.

I think we can’t forget that 2022 is a midterm election year in the US and the Fed, you know, they they try to stay nonpartisan sometimes. But you know, there’s going to be a lot of pressure for them to make sure that the economy continues growing at an acceptable pace and kind of pushes down against inflation, So they’re in a tricky spot so they can’t just go out of the gate with three rises. They have to take one. See how the market digests it. Continue to build up expectations for the later rate rises then proceed based on how the expectations are set in.

CNA: What would that mean for the flows into markets given how Biden administrations Build Back Better Plan is also facing a setback? We could see a narrower bill than the 1.75 trillion on the social and climate front. What then do you think the market drivers are going to be if both the central bank and the government are curtailing that stimulus?

TN: Right. You know it is possible. Like I said earlier, kind of travel those sorts of things are coming back. I think Americans are just dying to get back to something that’s a little more regular, a little less constricted.

You know we do see things like food, entertainment, travel these sorts of things moving. Temporarily, we do see things like technology dialing back. But you know as we get into Q1 or Q2, we think that stuff will come back and be interesting again. So. But not necessarily as much of the work from home activities. People here are gradually getting back into the office.

So you know what we will see say for US equity markets is because tapering and interest rates we will likely see a stronger Dollar and that stronger Dollar will attract more money from the rest of the world as well. So both domestic growth, although it’ll be a bit tepid in ’22 will help to continue to push markets marginally.

We’re not going to see massive growth like we saw in ’21. But the the strengthening US dollar will draw up liquidity from other parts of the world, too.

CNA: Just very quickly if you can, Tony. What do you think the outlook for energy demand and oil prices is going to be like given how some countries are already reverting back to containment measures?

TN: Yeah. Oil is tricky. In the near term, I think oil is a little bit tricky for the next few months. I think the outlook is better as we get say to the end of Q1 and into Q2. But for now, we’re not expecting a dramatic upturn in crude prices like we’ve seen in gas prices in Europe and other places.

CNA: Okay, we’ll leave it there for today and keep an eye on those commodities. Thanks very much for sharing your insights with us. Tony Nash of Complete Intelligence.

BFM 89.9 asks Tony Nash from Complete Intelligence on how China’s PBOC adoption of looser monetary policy will affect the yuan and the broader Chinese economy.

SM: BFM 89 nine. Good morning. You’re listening to the morning run. I’m Shazana Mokhtar are together with Philip See. It is Christmas Eve, Friday, the 24 December 9:06 in the morning. But in the meantime, let’s take a look at the activity on Bursa Malaysia.

PS: It’s flat like Coke without any bubbles.

SM: Oh, no, that’s the worst kind of flat.

PS: Yes, the foot sabotage. Malaysia is flat slightly down .09% at 1515.

SM: So still above 1500.

PS: Still above 1500.

But it’s been yoyoing a bit green and red so far. But the rest of the markets across Asia are in green territory. The Straits time is up at 3100. Cosby also up 58% at 3015. Nikkei also up zero 6%, 28814. Now, just to bring your attention, looking at the crypto Bitcoin 5998.65 above the 50,000 mark. Theorem also uptrend 4114115.184. Now, if we shift over to the currencies, ring it to US dollar 4.11988. You’re seeing some strengthening there. But across the other two currencies pound and sing dollar, we’re seeing some weakness there.

Ring it to pound 5.62967. Ring it to Sing dollar 3.0922. Now, looking over to the value board. Really. Smattering of small caps actually driving it, but cost number one Ata IMS at .72 cent unchanged, followed by SM Track up 13% at .13, followed by Kajura Tran asphas flat at .26%.

SM: Okay, so that is the snapshot of Bursa Malaysia at 9:09 this morning. We’re taking a look now at how global markets closed yesterday.

So if we look at the US markets, they closed in the green. The Dow was up 0.6%. The S&P P 500 was up zero 6% as well. The Nasdaq was up zero 9%. So a lot of optimism going into the Christmas weekend. Joining us on the line for analysis on what’s moving markets. We have Tony Nash, CEO of Complete Intelligence. Tony, good morning. Thanks for joining us today. Now 2022 is just a week away. And given the triple headwinds of Fed tapering, Omicron and a China slowdown, will there be a difference in how developed and emerging markets in Asia are going to be impacted?

TN: I think with the tightening in the Fed and with what emerging markets are going to have to do, meaning in the near term, like China is going to have to loosen. So I think you’ll have a strengthening dollar and more of a rush for capital into the US, so that should at the margin, kind of help US markets stay strong across debt and equity. Other things. I think in emerging markets it could eventually China loosening. The PVC loosening could help demand in emerging markets, but it’s going to be hard to get around the hard slowdown that started in China around Omicron.

PS: I see.

And so when you contrast that to the Fed tightening, right. You said China PBOC is adopting a looser monetary policy. How will this affect the UN in relation to those Asian currencies in which there’s a lot of trade between these two countries?

TN: Yeah. CNY has been strong for a protracted period, and it’s made sense on one level, so China can import the energy and food, particularly and some raw materials that it needs in a time of uncertainty. So the PVC has kept it strong through this period. What we’ve expected for some time. And what we’ve shown is that after Lunar New Year, we expect the PPOC to begin to weaken the CNA. We don’t think it’s going to be dramatic, but we think it’s going to be obviously evident. Change of policy, Chinese exporters, although they’ve been producing at not capacity, but then producing pretty.

Okay. China is going to have to devalue the CNY to help those exporters regain their revenues that they’ve lost over the last two years. So we’re in a strange period globally of moving from kind of state support back to market support, whether it’s the US, Europe, Asia, we’ve really had state supportive industries, state supportive individuals as we move beyond covet. Hopefully we’re moving more into a market orientation globally, and there will be some volatility with that.

PS: Yeah, but I was wondering for China, especially, I’m interested to know what the state of the Chinese consumer will be in 2022 because the government is worried for slow down. Right. And wouldn’t they want to expedite and give a bit more ammunition to the Chinese consumer?

TN: They would. But the problem is with Chinese real estate values declining, a lot of consumer debt is secured against real estate. And so the ability of Chinese consumers to expand the debt load that they’re carrying. Is it’s pretty delicate? It’s a fine balance that they’re going to have to run. So either the economic authorities in China push real estate markets up to allow Chinese consumers to keep debt with their real estate portfolios, or they make other consumer debt type of rules that allow Chinese consumers to hold more debt.

Real estate is the part that’s really tricky in this whole equation in China, because if real estate values are falling, the perceived wealth of those consumers is falling pretty rapidly as well, and the desire to consume excessively, it’s just tempt out.

SM: And I suppose still sticking to our view of China looking at metal commodities, what metals have been affected by the slowdown of demand in China? And do you foresee a recovery for them in early 2022?

TN: Yeah. We’ve seen industrial metals like copper and steel, and those sorts of things really slow down dramatically compared to where they were earlier in 2021. We’re seeing reports of, say, copper shortages at the warehouse level at the official warehouses in China, but that’s not real. What we’re seeing and I speak to copper producers in Australia and other places. What they’re telling us is that those copper inventories are being shifted to unofficial warehouses to create a perception of shortage. So we may see a run. We may see an uptick in, say, industrial metals prices in early 22, but we don’t expect it to last long because the supply of constraint is not real.

So until demand picks up for manufacturing and goods consumption. And the other thing to remember is we’ve had a massive durable goods wave through covet. Everyone’s talked up on durable goods. Okay, so there is almost no pent up demand for durable goods. And this is the stuff that industrial metals go into on the demand side, there are some real problems on the supply side. There seems to be plenty of supply in many cases. So we don’t necessarily see the pressure upward, at least in Q1 of 2022 on industrial metals.

PS: And that’s why I’m quite interested where you say that this demand is, I think slowly going to dissipate because yesterday key US inflation gauge sharpest rise in nearly 40 years, right? Personal consumption expenditure surged 5.7% in November. How long do you think this elevator level will last?

TN: Well, US consumers are pretty tapped out. So I think inflation happens for a couple of different reasons. Some people say it’s only monetary. Not necessarily true. We’ve seen real supply constraints that contribute to inflation. We’ve seen demand pulls because of overstimulating economies, and those two things together have accelerated inflation. And so we have to remember at the same time in 2020, we saw prices. If things go down pretty dramatically around mid year, say a third of the way through the year to mid year to just after mid year.

Some of these inflationary effects have been a little bit base effects because prices fell so hard in 2020. But we have seen consumption ticking up because of government stimulus. And we have to remember if the Fed is tightening things like mortgage backed securities, their purchases of mortgage backed securities will slow. Okay, so if people can’t refinance their house or buy new houses again, those wealth effects dissipate if you have a home. If your home price is rising, whether it’s the US or China or elsewhere, the wealth perception is there and people have a propensity to spend.

But if the Fed is pulling back on mortgage backed securities, then you won’t necessarily have that wealth effect that will dissipate. So government spending will decline marginally because build back better didn’t pass. We won’t have that sugar rush of government spending flowing into the economy early in 2002, although we may see something later. I believe governments love to spend money. So I believe the US government will come with some massive package later in the year to bring government spending back up.

SM: Tony, thanks very much for speaking to us. And an early Merry Christmas to you. That was Tony Nash, CEO of Complete Intelligence, giving us a quick take on what he sees moving markets in the final year. In the final weeks of 2021. Looking ahead to 2022.

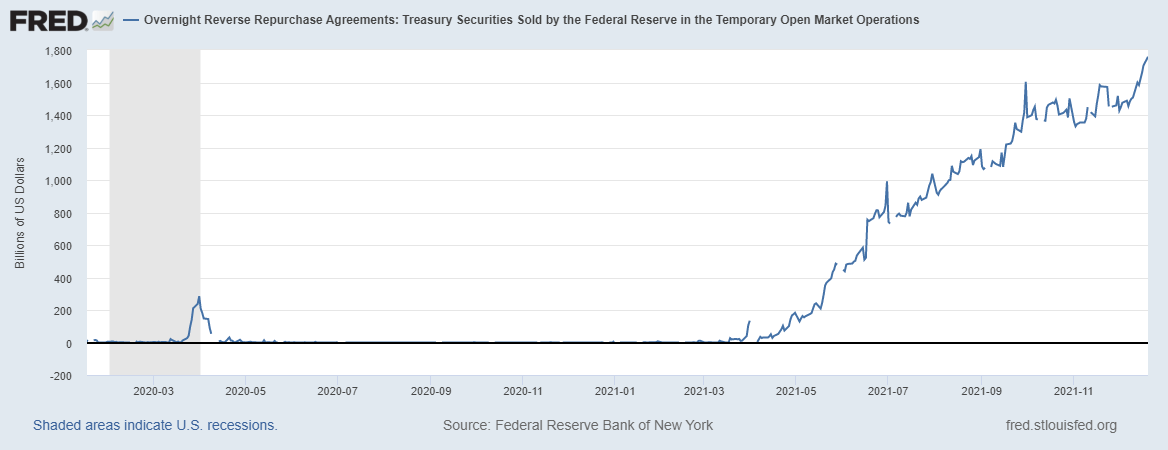

In the wake of the financial system’s cash glut and collateral shortage from the Fed’s quantitative easing program, the Secured Overnight Financing Rate drops to 0.04% from 0.05% on Monday, the first decline since October.

Even with asset purchase tapering underway, “it’s largely the same set of circumstances as in October,” TD Securities Strategist Gennadiy Goldberg told Bloomberg. “Lots of cash in the system and not a lot of collateral and that’s weighing down repo.”

Meanwhile, U.S. commercial banks park yet another record $1.75T at the Fed’s overnight repo facility, implying the banks are drowning in excess reserves, while searching for yield – which is scarce as most of the Treasury yield curve trades in net negative territory on an inflation-adjusted basis.

There’s an “incredibly large amount of cash sloshing the market,” said Complete Intelligence Founder Tony Nash via Twitter.

In August, the Fed’s overnight repo facility took up more than $1T.

Complete Intelligence – a fully automated and globally integrated AI platform for smarter cost and revenue planning.

Complete Intelligence provides actionable, accurate, and timely data to make better investment and procurement decisions.

The platform provides an integrated global model to ensure that actions in one market, country, or sector of the economy are reflected elsewhere in markets, industries, and the global economy. International trade, economic indicators, currencies, commodity prices, and equity indices are all factored in to create a proxy of the global economy. Over 1200 industries in more than 100 countries are covered!

Based on interviews with Tony Nash, founder, CEO, and Chief Data Scientist, this brief report introduces Complete Intelligence, one of a growing number of highly innovative companies supported by the Oracle for Startups program. The company, founded in 2019, is already significantly improving the forecasting and budget planning of a variety of large corporations through its advanced AI-driven intelligence platform. The theme for this month is around startups in the energy and utility sector and how they are innovating, changing the competitive landscape, and contributing to sustainability. CX-Create is an independent IT industry analyst and advisory firm, and this report is sponsored by the Oracle for Startups program team.

The business context for Complete Intelligence

Commodity price volatility and a post-pandemic surge in demand drive the need for more timely and accurate forecasting Businesses coming out of lockdown have increased demand for commodities, from energy supply to raw materials for their products. In Europe, benchmark prices for natural gas to power their factories and heat their buildings have risen from €16 megawatt-hour in January 2021 to €88 in October. This, in turn, has sent electricity prices soaring. (Source: Euronews). While some have locked in prices through forward-buying, others have been exposed and seen profit margins plummet, unable to pass on price hikes to their customers.

But it is not just energy prices that are volatile. Semiconductor chip shortages have impacted many industries that depend on them, from automotive to electronic household goods manufacturers, putting a brake on their post-pandemic recoveries despite strengthening demand.

The growing demand for clean and sustainable energy sources and precious metals, like copper and lithium that power batteries have also seen tremendous volatility. As major industrial companies digitally transform their organizations and business models seeking elusive growth, the importance of data and AI are increasingly recognized as fundamental to success.

Forecasting and budgeting needs data science, not spreadsheets The ability to sense change, respond quickly and adapt rapidly relies on a synthesis of massively increased volumes and varieties of data, both from operational and external sources. Data volumes are too complex for manual approaches and spreadsheets and require AI to extract insight and meaning from this complex array of external demand and supply signals. The old industrial-age planning approaches can’t cope. They are too slow, involve armies of accountants and analysts, and political wrestling between departmental heads, and are often based on opinion and inaccurate forecasts leading to erroneous budgeting decisions.

Complete Intelligence provides the accurate evidence base for budgeting and forecasting decisions

When markets are relatively calm and stable, the cycle of annual planning and budgeting makes sense. But amidst continual volatility and dramatic accelerated change, the planning cycle is too slow. It fails to mitigate the risks unfolding at such speed and is impacted by a confluence of so many variables, like extreme weather, scarcity of raw materials, pandemics, and weakened supply chains. An array of intelligent internal and external feedback loops is needed to mitigate risks and optimize resources in pursuit of the company’s goals. This is what Complete Intelligence provides with its integrated and modular intelligence platform.

Key observations

• Complete Intelligence provides the accurate evidence base for budgeting and forecasting decisions • The Complete Intelligence Platform consists of three modules – CI Futures, RevenueFlow and CostFlow • Forecast accuracy has rapidly improved, and error rates are now around 2%, which compares favorably with traditional methods and error rates of 35% or more

Complete Intelligence, the story so far

Tony Nash, founder, CEO, and Chief Data Scientist, is steeped in market intelligence. A former VP of market intelligence firm IHS (now IHS Markit), and The Economist Intelligence Unit, where he was Global Director Consulting and Custom Research. He observed that large international companies he had supported typically followed an annual budgeting cycle based on often inaccurate or opinion-based data. It was not unusual to find large teams of people, sometimes several hundred involved in the process and heavily reliant on gathering data from multiple departments in complicated spreadsheets. The process could last several months, and the variance between forecasts and actuals was often above 35%, which could erode profits or tie up resources unnecessarily.

Trial, error, and persistence As a data scientist familiar with cloud technologies, he developed algorithms to improve forecast accuracy and a complete process from data ingestion to forecasting and testing the results. He started developing the machine learning ML algorithms in 2017 while still consulting in Asia from his base in Singapore. His first iteration failed to produce a level of accuracy that would provide a sufficiently compelling proposition. He wanted to get down to an error rate of no more than 5%-7%. He adopted the ‘ensemble’ approach covering thousands of different scenarios layering external data on commodities such as the copper price with a customer’s actual costs, identified in their general ledger.

Ready for launch late 2019 In 2019, Nash returned from Singapore and set up his company in The Woodlands, near Houston, Texas. He continued his work on the algorithms and developed a commercial product ready to launch in early 2020. And then Covid-19 struck.

Through Covid-19, companies first tried to understand the changing environment, then remained risk-averse until public health, business environment, and supply chains became more stable. This has been a challenge for a cutting-edge machine learning firm like Complete Intelligence. It is only as the environment has begun to stabilize that enterprises have sought new solutions to legacy problems. With that has come a renewed interest in Complete Intelligence and deployment at a large scale.

Solution overview The Complete Intelligence Platform consists of three modules The Complete Intelligence Platform hosted on Oracle Cloud Infrastructure (OCI) consists of three forecasting modules:

•CI Futures – to forecast market trends. Covering over 1,400 industries in more than 100 countries and a database of over 16 billion data points from proprietary and publicly available data. Millions of learning algorithms are used, which factor in the most recent global events.

• RevenueFlow – provides accurate results for demand and forecast sales and revenue projections.

• CostFlow – to enhance product line profitability and improve supply chain and procurement outcomes.

Figure 1. provides a diagram of the Complete Intelligence Platform

Figure 1: Complete Intelligence Platform by Complete Intelligence.

Market data is ingested from multiple trusted data sources like national statistical agencies, multilateral banks, multilateral government bodies, commodities exchanges, bilateral trade bodies and combined with the client’s data from their general ledger. A multi-layer testing and validation process used to ensure the accuracy of the data to be used in any forecast. Third-party data is gathered via internet spiders and APIs.

The platform provides an integrated global model to ensure that actions in one market, country, or sector of the economy are reflected elsewhere in markets, industries, and the global economy. International trade, economic indicators, currencies, commodity prices, and equity indices are all factored in to create a proxy of the global economy.

A comprehensive list of futures, currencies, and market indices is covered and accessed through a highly graphical and easy-to-use interface. Almost 1,000 assets, with historical data from 2010 and forecasts over a one-year horizon, are provided. More assets are being added all the time.

The platform is designed around three attributes: • A globally integrated model • A data-driven process without human intervention in the output • A simple means of interfacing with the platform.

The platform can be connected to existing ERP systems and automatically upload pricing data from the general ledger at a very granular level for each item.

The Complete Intelligence Platform supports a variety of use cases: • Supply Chain & Purchasing Optimization – help lower costs, anticipate risks, and provide input to sourcing strategies. • Sales and market entry strategies – by identifying higher growth markets and optimizing resources • Strategic Financial Planning – identifying growth markets and fine-tuning resource allocations in each market to minimize exposure to currency fluctuations. • Mergers and acquisitions – provide a snapshot of cost structures and projections of future costs and profitability of target acquisitions.

Forecast accuracy has rapidly improved, and error rates are now around 2% Nash’s persistence has resulted in significant levels of forecasting accuracy. A twelve-month forecast now sees error rates around 2%, which gives users considerable confidence compared with traditional methods, where the error rates are often above 35%.

As well as dramatically improving forecast accuracy on markets, revenues, and costs, the onboarding process to going live is a matter of a few weeks. After that, forecasting takes hours, not months.

Current position

Successes to date

While still a relatively new company, Complete Intelligence has already proved its value to several large companies.

• A major petrochemical company wanted to improve its predictive intelligence capability for feedstocks and refined products. They asked Complete Intelligence to examine nine categories across crude oil, gasoline, diesel, natural gas, and gas-to-liquid (GTL) products. Monthly forecast averages are provided by category with extremely low differences from actual results on the order of 3% or less.

• A global furniture company wanted a more explicit link between their sales and revenue planning and their sales teams in China. Complete Intelligence built a sales forecasting model that more clearly identified and utilized market demand drivers and connected these directly to their business. An analytics-based approach to identify the drivers of sales by city and industry. Complete Intelligence built a city and industry-level forecasting tool that determined the company’s growth trajectory and provided recommendations to support the direction and transition of their sales teams. • A global chemicals company needed a better understanding of the trends for costs in their supply chain and a more precise way to manage margin expansion and contraction at the bill of material level. Complete Intelligence was commissioned to forecast factor inputs and currencies for the key categories. The forecasts were calibrated based on the component make-up of the bill of materials. This enabled the client to identify the direction of the materials pricing and the impact on their BOM. Through the process, the client learned how to anticipate cost movements and protect margins.

Current go-to-market model

Complete Intelligence sells directly to large organizations, mainly targeting CFOs and COOs with a broad view of their companies and strategic decisions.

The company also has strategic partnerships with Microsoft and is listed on the Azure Marketplace and with Oracle as part of the Oracle for Startups program and hosted on OCI.

Other partnerships with Bloomberg and Refinitiv allow for exchanging financial and market data and connection to their platforms.

More transparent accuracy reporting so customers can view accuracy/error for every line item

More robust and flexible data visualization for clients to utilize Complete Intelligence forecasts within their visual narratives

More sophisticated data science to account for detailed sentiment and other qualitative factors

Do-it-yourself forecasts for customers to do ad hoc forecasts for any data at any time. This will enable teams within a company to do their own sophisticated, reliable forecasts without waiting on their in-house market analysis or forecasting team with complicated macros and massive spreadsheet workbooks

Embedding Complete Intelligence forecast APIs into ERP and accounting software.

Oracle Cloud Infrastructure and the Oracle for Startups program prove their value to Complete Intelligence When asked what he felt about the relationship with Oracle and the Oracle for Startups program, Nash said, “Oracle Cloud Infrastructure is very flexible and secure. The Oracle for Startups team has been great. Oracle has been the most responsive and helpful of all our partnerships, connecting us to the right people to help with marketing, sales, or technical questions. I really feel that they want us to succeed. I’m a huge advocate of the Oracle for Startups program.’’

CX-Create’s viewpoint The Complete Intelligence Platform addresses a fundamental business need

Providing a global proxy model on markets, commodities, currency fluctuations, and many other aspects and making this easily accessible for business people will significantly improve strategic investment and procurement decisions. The emphasis on accurate and timely data supported by ML models will make it easier for business people to make informed decisions, stripped of personal bias. Digital transformation should lead to a more agile and responsive organization. The more progressive organizations will want highly attuned external signals that are constantly updated, enabling them to de-risk investment decisions and optimize resources for growth. Complete Intelligence provides for that.

Our CEO, Tony Nash, talks about inflation’s and Omicron’s role in US shares sinking, as fears spread over their non-transitory nature. And how will Asia react to the ‘non-transitory’ nature of inflation and the new Covid variant? Is Gold a good asset to use to hedge against inflation?

Discover how Complete Intelligence can help your company be more profitable with AI and ML technologies. Book a demo here.

Show Notes

PS: Markets in the US were down across the board. The Dow is down 1.3%. S&P 500 down 1.2% Nasdaq down 1.8%. Now over across in Asia, everyone was up. Nikkei was up .4% Hang Seng up .8% Shanghai Composite also up .4% and STI Singapore up 1.9%. And as I was saying early on, FBM KLCI was down 1.1%.

TN: Yeah. Thanks for having me, guys. I think the biggest consideration really is Powell’s comments on inflation, saying it’s kind of no longer transitory. So people should expect inflation to stay. What that means generally is we’ve hit a new pricing level is his expectation. So meaning prices are not in his mind, in many cases, going to go back to the levels that we saw before this inflationary stairstep. And what we’ve seen, particularly in the US, is consumers have accepted this and consumers accepted it, thinking that it was a temporary rise in prices.

But what he delivered today is some bad news that it’s likely a permanent prize in the level of prices. And the kind of short term cost rises that people thought they were going to endure are more permanent.

KSC: Yeah. So, Tony, try and give us a bit of a perspective here, because obviously the last twelve years and the last accelerated two years of monetary easing have induced this inflation. How does it all end? And does it stop the weak economic growth we’ve been seeing in the US the last few months.

TN: Yeah. So US economic growth, we don’t see a rapid acceleration of US economic growth. And so we have the US, China, Japan, and the EU, all at very subdued growth rates. And that’s bad. Those are the four largest economies with elevated price rises. Earnings are growing in some areas. I’m sorry, wages are growing in some areas, but they’re not necessarily growing across the economy. And part of that, particularly in the US, is a shortage of staff. So people have opted out of the workforce. We’ve lost, like 6 million workers in the US since Covid.

And so there are fewer workers. And so we have wages rising in certain areas. But it’s not necessarily across the board. So people are really going to have to start taking a look at their disposable income to understand what of these ongoing price rises that they can continue to accept. And I think we’re at a point where, since it’s no longer viewed as temporary, people and companies are going to have to start making trade offs. This is really the bad news is when people have to, when it’s no longer temporary, companies and people have to start making trade offs of what to do with their resources.

And that’s where the real problem is. So it’s not ongoing expansionary spending. And even I think it was Biden who said today we don’t expect a stimulus package for the current variant. Again, people are having to look at trade offs, and this is the real problem. When companies have to look at trade offs, they’re looking at their operating costs, they’re looking at their capital expenditure, they’re looking at their investments, they’re looking at other things. So down to Earth type of environment where we’re starting to enter Realville, we’re starting to exit the kind of fantasy environment we’ve been in the monetary induced sugar coma that we’ve been in for the past year and a half.

PS: So that’s a very interesting point, because I’ve always felt like in 2021, we saw this huge divergence in recovery right between the developed world led by the US and emerging markets, which are still really struggling to contain the virus and such. So when we talk about Asia, how do you think markets will react to this tightening of monetary policy by the Fed?

TN: Yeah. We think that Southeast Asia generally will stay pretty muted. We don’t expect early breakout at least over the next quarter or two. We don’t expect really breakout moves in Southeast Asia. We expect China to have a fair bit of volatility, but we do expect China to be generally positive over the next quarter to quarter horizon. We do expect Japan to continue to rise pretty well in India as well. Japan largely on the back of monetary policy automation, other things. So Asia is not one market, of course.

So we do expect different parts of Asia to react differently. Korea will be a mix between China and Japan like it always is. So we’ll see some volatility there reflecting China, but we’ll see some, I guess, acceleration and equities like we would see in Japan to make some both.

KSC: Well, Tony, in truth, inflation has been with us for some weeks now. But what hasn’t been with us for some weeks has been on the Omicron that’s the other big roadblock posing an obstacle to markets. How does Asia behave? How does Asia react, especially since we’re going to be opening in a few hours time?

TN: Yeah, I think Asia generally. You guys know I lived in Asia for most of my life, and Asia generally takes these things in stride with more vaccines available with the typical kind of weathering, the storm kind of approach that people have, particularly in Southeast Asia. I think people will generally take it in stride. This is really the first pandemic. Let’s say in the west that people have had for probably 50 years where they’ve really been kind of freaked out and worried in Asia, we’ve seen these types of pandemics for 2030 years.

It’s a bit different. People are more conservative, people are more used to these types of volatile, say, public health and market and other type of environments in Asia. So of course, we’ll see things shake up, but we won’t necessarily see the dire kind of messages that we’ve seen, say in the west. I don’t think we will. We’ve seen dire messages come out of, say, Germany and Italy and Austria, particularly over the past week with full lockdowns with 100% vaccine mandates, with really dire messaging. I don’t necessarily think we’re going to see super negative messaging in Asia like we’ve seen there.

PS: We won’t freak out as much as what you’re saying then essentially.

TN: No. Come on, man. It’s Asia, right? People are used to volatility in Asia and the developed markets. Developed markets are highly calibrated. Right? 0.2% change. Either way is people see as dramatic in Asia a small they’re not as calibrated. So people are accustomed to more ups and downs, and people just generally take it in stride.

PS: And I said that generally it’s quite calming. Is gold with inflation basically consigned away from this trend trade term? What’s your view in terms of gold? That’s a hit against inflation then? Because if I look at the data, the method is down 6% year to date.

TN: Right. And a lot of the inflationary rise has already happened. A lot of the stuff happens in stairstep fashion, and a lot of the mitigation efforts are already under way. So while we’ll continue to see inflation and we’ll continue to stay at an inflated level, I don’t necessarily. Or we’re not seeing dramatic price rises going forward. Okay. You’ll see it in pockets where there are, say, supply issues or something like that. But gold is more effective when everything is well, gold is a barometer for finding value.

I’ll say that much. It’s a tangible metal and people see it as worth something. And so what used to happen is gold and say the dollar as the dollar do value the gold would appreciate. But now we have crypto and people treat crypto kind of in the same way they used to treat gold. The gold market is really trying to find itself. So I think we’re going to have to see some fallout in crypto if it is to happen. We’ll have to see some fallout in crypto before we start to see gold being the safe haven again or being the preeminent safe haven.

So until Bitcoin and the other crypto assets really deteriorate in value and people go flocking back to gold, which I think will happen eventually. I don’t think it’ll happen overnight, but until we see a lack of faith in crypto, I don’t think we’ll necessarily see dramatic price pressure on gold.

KSC: Tony, you talked about Asia, right? And now China is moving to banners via structure, which is the loophole that allows its companies to list in New York and other foreign exchanges. What does this mean in terms of China’s overall strategy to go its own way to quote Fleetwood Mac?

TN: Sure. Yeah. So I think, of course, it hurts Western banks, and it hurts the Western banks that are in Asia because they don’t necessarily have those fees to take things public in the west. But I think the bigger problem is this those companies going public don’t have US dollar denominated resources to access, and so they have to get CNY or Hong Kong dollar or Japanese yen or other Sing dollar other denominated assets. Okay. But the US dollar is 87% of global transactions. So it helps those companies to have US dollar reserves, especially as they’re newly public.

Because why do you go public? Because you want to buy another company, you want to use that cash for a big investment or something, you want to expand in a big way. So if you don’t have the US dollar assets that come from going public, say, in New York or somewhere in the US or whatever, it’s really hard to have a big source of cash to do a massive international expansion or undertake a big international project or do a big international buy that’s I guess the biggest downside I would see from the decline of that type of structure in China.

KSC: All right, Tony, thank you so much for your time, Tony Nash there chief executive of Complete Intelligence. And just to hang on this last point, Phil, if you don’t list in the US, you don’t get US dollars necessarily. But that doesn’t matter if you are China, and you believe that the real market is domestically or within ASEAN, where you’ve got to combine, I don’t know, 2.1 trillion people or 2.1 billion people. That’s quite a fair few heads. Yes.

PS: Correct. I think it’s a question of whether you see a convergence between where you list versus where you operate.

KSC: Absolutely.

PS: And I think in the past we thought, okay, you could tap financial markets globally to serve your local markets. But I think China is kind of proving the point. No. I think it’ll be closer together.

KSC: Yeah. And what he was talking about in response to your question on gold, Phil, how gold hasn’t responded to all this uncertainty, which has been traditionally the case. And Bitcoin is somewhere hovering around in the mid 50s, which is a bit weird because you would expect some kind of flight to what was seen as safe havens, right.

PS: Ironic is considered Bitcoin a flight to safe havens.

KSC: Well, because it’s finite in nature. So it’s a bit like gold, right. It seems interesting, because in the last few weeks, we’ve seen a move among corporates like Mark Zuckerberg of Facebook and now Jack Dorsey, formerly of Twitter, who has left his job at Twitter. Still, at the same time was CEO of Square fintech platform financial platform. He’s moving to turn Square into a company called Block, and it’s a bit like it would make Mr. Miyagi proud because martial arts moves from square to block, but he’s going all in.

PS: But this is a very interesting thing because he’s going all in on crypto. And I think you’re referring to Blockchain blockchain reference to Blockchain, which is the distributed platform for data used by Crypto.

But it’s interesting, right? This whole name shift.

I think Jack Dorsey, I think, is trying to evolve away from just being a pure payments provider to offering solutions that are anchored on blockchain as a solution.

Tony Nash gave the BFM 89.9: The Morning Run his thoughts on how the sooner-than-expected Fed rate hikes could affect global markets. Will inflation derail hastening of the tapering talk? How does crude oil look like in the next few months? As the Christmas season is coming, how much of a concern supply chains will be for the consumers and the economy? When the Fed begins normalizing rates, which currencies will be vulnerable if or when this happens?

❗️ Discover how Complete Intelligence can help your company be more profitable with AI and ML technologies. Book a demo here.

Show Notes

SM: BFM 89.9 good morning. You are listening to the Morning Run. I’m Shazana Mokhtar together with Khoo Hsu Chuang and Philip See. It’s 9:07 in the morning. Thursday, the 25 November. If we look at how the US markets closed yesterday, the Dow was down marginally by 0.3%. The S&P 500 was up 0.2%. Nasdaq was also up 0.4%. So for some thoughts on where international markets are headed, we have with us on the line Tony Nash, CEO of Complete Intelligence. Good morning, Tony. So the Fed minutes revealed that the pace of tapering may be hastened, while macro data points from personal spending to job data suggest that the US economy is in quite the sweet spot, but will inflation derail this?

TN: Yeah. There was a statement from one of the Fed governors today talking about that inflation is not transitory in their mind or could potentially not be transitory in their mind. That’s a real danger to people who are thinking that we’re really in a sweet spot right now because it could mean Fed intervention, meaning tightening sooner than many people had counted on. So I think people had counted on some sort of intervention, maybe in Q2, but it may be happening sooner. That would have a real impact on the dollar. The dollar would strengthen, and that would have a real impact on emerging markets all around Asia, all around Africa. People would feel it in a big way where there is US dollar debt.

KHC: We are seeing that strengthening US dollar in our currency now. But I just want to get your perspective on crude oil because various countries from the US to China are now tapping into their strategic crude reserves to alleviate the present energy crisis. But if you look at crude now, it’s not really being responsive, right to these actions?

TN: Right? That’s right. So what the US agreed to release is about two and a half days of consumption. Not much. The releases agreed in the UK and India, for example, were really token releases. They weren’t really major portions of their consumption. So these countries are kind of giving a nod to the Biden administration, but they’re not really alleviating the supply concerns that are spiking prices. So it really has been a dud for the White House. It’s been kind of an embarrassment because crude prices haven’t fallen, really. They fell initially, but they really came back after the release announcement was absorbed.

PS: Yeah. Tony, that trickling in oil supply releases from the US government hasn’t done much to alleviate the supply concerns. Gas prices in America have been on a massive uptrend as well, just in terms of inflation and not being as transitory as people expected, as we enter Christmas season, how much of a concern is it for consumers as well as the economy?

TN: It’s a real concern. I have to tell you, I’ve driven halfway across the US for our Thanksgiving holiday, which is tomorrow morning. It’s Thursday here, and we’ve seen a lot of trucks with cargoes on US roads, and I make this drive pretty regularly. So it seems like a lot more on roads than I normally see. So that’s good in terms of the domestic supply chain.

I think it’s the international supply chain that is really concerning, and we still have those backups in the Port of Long Beach. That is the real main constraint for supply chains in the US. So I don’t think we’re going to see major disruptions outside of other ports. But through Long Beach, we definitely see issues.

The semiconductor supply chain is the main impact for, say, electronics and automobiles in the US. We did see semi manufacturers start to produce more auto related semiconductors, say mid-Q3 and into Q4. We should start to see those automotive supply chains, the semiconductor dependent issues and automotive supply chains alleviate, probably in Q1. So that will help.

But for the Christmas season, I’m not sure that there’s a whole lot that’s going to help with electronics and say automobiles.

PS: Yeah, Tony with JPowell still back and still in the fair chair in terms of his reappointment. And he does hike rates earlier than expected to address inflationary concerns. How much of a dangerous is to slowing down the economy in America and as the rest of the world.

TN: Sure, it is a risk in America. I think it’s really hard to hire people in the US right now. There’s a lot of job switching happening and people haven’t come back into the workforce. We lost about 5 million people in the workforce in the US through the Covid period. So that’s a real issue. Anything that raises the cost of doing business is problematic for the US and will inhibit growth. The main problem in the US is that the environment right now, it continues to crush small companies. It’s very difficult for small companies. And while it may seem that small companies don’t matter that much, they are the main employer in the US and the main growth engine in the US. And the Biden administration hasn’t helped this with a lot of their policies. Their policies have been very favorable toward big companies. If the Fed pushes inflation, it will make borrowing a little bit harder. I’m sorry if the Fed pushes the interest rate, it’ll make borrowing a little bit harder. But the collapsing, say, the tapering of the Fed balance sheet will have a bigger impact on liquidity in the US.

SM: And if I could just touch on large US dollar debt and what happens to emerging markets when the Fed begins normalizing rates, which currencies do you see as going to be particularly vulnerable if or when this happens?

TN: Well, I think one that I’m really keeping an eye on is the Chinese Yuan because it’s a highly appreciated currency right now. And the Chinese government has kept the CNY strong so they can continue to import commodities and energy for the winter. And they’ll likely keep it strong through Chinese New Year. We expect CNY to really start to weaken, say, after Chinese New Year to help Chinese exporters. So winter we mostly pass. They want to help kind of push a Chinese export, so they’ll start to really devalue, seeing why probably end of Q1 early Q2.

We do see pressure, the Euro, as you’ve seen over the last three weeks, there’s been real pressure on the Euro as well. Other Asian currencies. We do think that there will be pressure on other Asian currencies. Sing Dollar will likely continue to stay pretty consistent. But we’ll see some pressure on other Asian currencies simply because of the US dollar pressure. The US dollar is something like 88% of transnational transactions. So the US dollar as a share of transnational transactions actually come up over the past two to three years. So there’s much more pressure with an appreciated dollar and it’s coming.

KHC: Just like the one. Tony, India Indian equities record high. Have you reached to speak considering PTM’s IPO failure?

TN: Yeah. I think there’s been a lot of excitement there, and I think it’s at least for now. I think it has I don’t think you can ever really claim that an equity market has hit its peak, but I think for now, a lot of the excitement is dissipated. It may come back in a month, it may come back in six months. But I think that momentum is really important. And as you see, failed IPOs, I think it’s really hard for equity investors to kind of get their mojo back.

SM: Tony, thank you so much as always for speaking to us and happy Thanksgiving to you and your family. That was Tony Nash, CEO of Complete Intelligence, giving us his thoughts on how the sooner-than-expected Fed rate hikes could affect global markets.

This is the most recent guesting of our CEO and founder Tony Nash in CNA’s Asia First, where he shares his expertise on inflation and the US economy. Will consumers continue to spend to help the economy? What’s his view on Biden’s call to boost oil supply to ease prices? Where does he think the US dollar is headed and how will that impact Asian currencies?

The full episode was posted at https://www.channelnewsasia.com. It may be removed after a few weeks. This video segment is owned by CNA.

Show Notes

CNA: What’s still ahead here in Asia First. We’ll check if US companies continue to charm investors with some big earnings in focus. Plus, to give us a stake on markets inflation and the US economy, we’ll be joined by Tony Nash from Complete Intelligence.

US stocks closed in the red overnight as lingering inflation concerns continue to dog investors. The Dow ended lower by six tenths of one percent, dragged down by a four point seven percent. Drop in visa the S&O 500 slipped 0.2 percent. And the NASDAQ fell by 0.3 percent.

Now after the bell, we also had some US tech earnings. NVIDIA shares rose after it beats on the top and bottom lines. The ship maker saw its revenue jump 50 percent on year on strong gaming and data center sales. Cisco shares tumbled and extended trade after missing on revenue expectations before the quarter. The computer networking company also issued a weaker than expected guidance.

For more on the broader markets and economy. We’re joined by Tony Nash is founder and CEO of Complete Intelligence speaking to us from Houston, Texas. So Tony as we heard their inflation fears seem to be back despite better expected earnings but CEO’s are starting to warn of more pain when it comes to supply chains. And that could put a damper on in that could lift inflation. Do you think the US consumers will continue to spend despite all this and will that help the recovery of the US in the next year?

TN: Yeah, I think the real issue here is that inflation is rising faster than wages. And what we’re seeing with oil prices. These oil prices are not terrible given kind of historical prices but it’s oil prices within the context of everything else. Obviously, the supply constraints really are pushing up prices of food and other activities as well as say goods that are imported for say the holiday purchases that Americans will make.

So Americans have absorbed a lot of those price rises to date. They’ll continue to absorb some but I think they’re almost at their limit in terms of what they can tolerate without getting upset.

CNA: Yeah, Do you think there’s a disconnect here when it comes to energy because Biden administration is hoping to boost supply to ease that oil price pressure but OPEC and its allies expect surplus into the next year. So, do you think they’re looking at it differently? And who has it right here and where oil prices headed?

TN: Yeah, I think part of the issue in the US with crude oil is the Biden administration restrictions on pipelines and on the supply side in the US. So, Joe Biden is asking other countries Russia, Saudi Arabia, other OPEC members to supply more oil yet he’s restricting the supply domestic supply in the US. So, I think what’s happening with those other suppliers they have customers who are buying their crude oil. They don’t necessarily want to have to produce more because they want slightly higher prices. They don’t want things too high but they want slightly higher prices and so they’re pushing back on on Joe Biden and saying look you really need to look at your own domestic supply. You really need to look at at those issues yourself before we start to open up our own market.

So you know, the current administration is trying to have it both ways. They’re trying to restrict supply within the US. They’re trying to bring in more supply from overseas. Americans see this and they understand kind of the incongruent nature of that argument from the administration.

CNA: I want to get your thoughts on the US dollar, Tony. Because that hit a 16-month high amid his expectations of more aggressive policy from the Federal Reserve. Where do you think the US dollar is headed and how will that impact us here in Asia, especially Asian currencies?

TN: Sure, it’s a great question. We saw a lot of action with the US dollar yesterday. The dollar index as you said reached highs for in the last say 18 months, two years. And that is on Fed action but one thing to consider is we’re looking at potentially changing the Fed chairman later this year.

So, if the current Fed chairman is exited. There is an expectation of a more dovish Fed chair coming in that’s one possibility. I think people are really trying to… While there is upward pressure on the dollar. People are trying not to get too far too much behind it because there could be a more double dovish Fed chair coming in. So, we think the dollar is overshot just a little bit in the short term.

We don’t expect it to continue rallying at its current pace. We expect say the Euro has fallen quite a bit and depreciated quite a bit in the last say three weeks. It’s going to appreciate just a bit a couple cents over the next month or so. Asian currencies, we think the CNY will stay strong. We think CNY will remain strong through say March, April as they start a devaluation cycle to help exporters. We think the Singapore dollar is going to stay in the same range that it’s in about now. We don’t see much policy change in Singapore and we think with a stable dollar at these levels. We think the same dollar will stay at about the same exchange rate of Scott now.

CNA: All right. We’ll keep our eyes on those currency exchanges and who becomes the next Federal Reserve Chairman. Tony Nash thanks for joining us. Tony Nash there founder and CEO of Complete Intelligence joining us from Houston, Texas.

Tony Nash, CEO and founder of Complete Intelligence, joins the BFM 89.9 The Morning Run show to give insights on the US Market, specially now that the CPI hits 6.2%. What does this mean for the Fed Fund?

SM: BFM 89.9 Good morning. You are listening to The Morning Run. I’m Shazana Mokhtar there together with Wong Shou Ning. But for some thoughts on what’s moving global markets we have on the line with us. Tony Nash, CEO of Complete Intelligence. Good morning, Tony. Always good to have you. Can we get some of your thoughts on, I guess this red equity markets outlook? One of the stocks that reported after hours was Disney and they reported results that underwhelmed with only about 2 million new streaming subscribers added this quarter the stock is down and after market hours trading. Do you see this as a buying opportunity, or do you think that there are still headwinds when it comes to the sectors that Disney operates in?

TN: Yeah. I think Disney has some real headwinds. Their park attendance is down on COVID concerns and regulations. Their streaming service just doesn’t really have the content throughput meaning the new content that people would expect from, say a Netflix or a Hulu or other types of streaming services. So part of what Disney needs to do is really have much more throughput on their content on Disney+.

WSN: What about CPI numbers, Tony? Are you really concerned about that? They came in at 6.2%, which was higher than street expectations of 5.9%. I think from now onwards, it’s going to be very hard for the Fed to say that inflation is just transitory, right?

TN: Oh, very much. So the Fed targets 2%, and this was just a little bit above that to the point where it’s really turning heads now and it’s really got people afraid. So part of this is base effects on last year, but not much it really is the supply and demand are weird. In some places, you have real supply chain shocks. You also have demand issues, say winter is coming, things like natural gas, oil, these sorts of things. They’re really being impacted. Food is being impacted. So people are seeing price rises that they haven’t seen for a long, long time.

WSN: Does this change your investment strategy, Tony? Or maybe a change in terms of your asset allocation? Are you going to go long equities or short fixed income? What’s your plan for 2022 or even in the next three months?

TN: Well, we’ve been saying for a while that this really isn’t a broad market environment. This is individual equity or say individual commodity type of market. Because if you are investing broad, yes, you’ll get incremental gains depending on where you are in the world in which market you’re in. But it really is a stock pickers market. You really have to understand the company. You have to understand how a trade you have to understand where the value is and how that is relative to the rest of the market in the economy.

And you also have to understand, actually, at least in the US, you have to understand what the Fed is doing. In your own country, you have to understand what your central bank is doing and what I mean by that is how easy are the monetary conditions? How does that impact individual countries and markets? How does that impact demand and, say commodity prices? So it’s not an easy question to answer, but it is a more specific and expert-driven market than it has been for the last two years.

SM: All right. Sounds like you’re giving our listeners a good reason to stay tuned to our chats every morning, Tony. Turning our attention to some recent developments in the US Biden’s 1 trillion infrastructure bill has just been passed. How much of a windfall will this be for US transport infra and telecommunication companies?

TN: Well, it’ll be a windfall, but it’ll happen over an extended period. This really won’t be spent for probably five to eight years. It will drip out over that time. So, yes, it is a lot of money, but it’s not happening in one tranche. And by passing this bill, it’s effectively saying this is it for infrastructure for the next almost decade. Okay.

So those companies who can successfully lobby and or successfully bid are going to get paid well over that period, those who don’t have the infrastructure in place to do that are going to have a tougher time. So. It’s a massive number. But it’s happening over an extended period.

WSN: What about oil and gas? Do you see them benefiting from this push into infrastructure?

TN: I don’t see an immediate positive impact for oil and gas. There are other reasons I’m positive on oil and gas, but on infrastructure, because this will come out over such an extended period of time. You see, infrastructure spending is really meant to be the foundation for future growth. Right. So you create the infrastructure that, say productivity gains and other things can leverage off of in the future. If we were doing a lot of infrastructure over, say, the next three years, you would expect a lot of oil and gas to be used to manufacture that, to power that and so on and so forth. But because it’s an extended period and because it’s distributed all around the US, there really isn’t a concentration of, say, the activity and it’s happening over a long period. I know I’ve said that several times, but that’s my biggest takeaway from this bill is the slow drip that it comes out on.

WSN: But you did say that you are a bit of a oil and gas bull at this juncture. What are your reasons for it, though?

TN: Well, we have regional, say, shortages or regional supply chain issues, say in Europe and parts of Asia for oil and gas, particularly gas, right now, as winter is coming on. Gas has performed well over the last, say six to nine months, maybe a year, and we expect it to continue to do well for the next few months. Crude oil? It looks like we’ll see some interesting upside in crude oil as well, partly on those regional supply issues as well.

WSN: But historically, by this time, right. Wouldn’t the shale producers be pumping away, too? And kind of adding supply? But it doesn’t seem to be the case this time, right. Because Brent crude this morning is still $83 a barrel.

TN: Right. Well, the shale is a different story because there are so many restrictions and regulations put in place by the US government under the current administration that it’s taking more for them to get started. So without the, I would say, aggressive kind of enforcement and new impediments to domestic shale production in the US, Yes, I believe we would have more rigs moving by now. But because of the impediments that the administration has put in place, the US administration is asking the Middle East, and they’re asking Russia to produce more.They’re not necessarily leaning on US producers. They’re trying to minimize the production here in the US. And part of that is the Green New Deal and other things to kind of regulate green energy into existence in the US.