Get $200 OFF your CI Markets subscription: https://completeintel.com/save200/.

Welcome to “The Week Ahead” with your host Tony Nash. In this episode, we discussed three crucial topics:

1. Housing: Time to pay attention: David Cervantes addresses the US housing market, noting its robustness during the pandemic due to backlogs but predicting a slowdown now that those backlogs have resolved. He stresses the significance of monitoring housing prices, especially rental prices, as indicators of inflation. Cervantes also discusses the frozen state of existing home sales, emphasizing the influence of wages on rents. He highlights the Federal Reserve’s focus on real estate and wage channels to manage aggregate demand. Additionally, he suggests potential investment prospects in the housing sector, including home builders and mortgage real estate investment trusts (REITs).

2. Fed & Bond Vigilantes: Gary Brode covers various topics in his discussion, including concerns about excessive government spending and monetization of debt. He highlights the impact on the bond market, expressing concern about inflation and the potential slowdown in the economy. Brode also discusses historical income taxes, property taxes in Texas, and challenges faced by the orange crop in Florida.

3. Soft commodities gone wild: Tracy Shuchart conversation covers a range of topics, from California’s potential as the top orange crop producer to student loan repayment’s possible impact on the housing market. Additionally, she touches on the conflict between monetary and fiscal policies, factors affecting soft commodities, and regional issues in the NatGas market. The discussion wraps up with speculation about the effect of snowfall on natural gas prices.

Join us for a clear and concise analysis of these important topics in plain language you can understand. Stay informed for the week ahead! Don’t forget to like, subscribe, and share for more valuable insights.

Key themes:

1. Housing: Time to pay attention

2. Fed & Bond Vigilantes

3. Soft commodities gone wild

Transcript

Gary Brode

The Republican financial plan is like being a waiter and coming to the table and saying, By the way, if you’d like, we’ve got a Republican plan for your dinner. I’m going to put enough poison in your dinner to kill you. The Democratic plan is we’ll offer you more poison than that. Either way, you’re dead.

Tracy Shuchart

Court is a really interesting case because it’s the largest orange juice or it’s the largest orange crop producer in the world. For the very first time this year, California is going to beat us.

David Cervantes

The existing home sales market is basically frozen shut.

Gary Brode

When he’s been screaming higher for longer and the whole market said, He doesn’t mean it. He’s going to pause. He’s going to pivot. We’ve heard all that. I’m like, No, no, no. The reason I believe this is because I think Powell is terrified of being the next Arthur Burns and he wants to be the next Volker.

David Cervantes

Rental prices will moderate and chip away at that sticky OER.

Tracy Shuchart

Their storage may be 90% full, but that 90% is only 25% of what they use during the whole winter.

Tony Nash

Hi, everyone, and welcome to the week ahead. My name is Tony Nash. Today, we’re joined by David Cervantes, Gary Brode, and Tracy Shuchart. Gosh, we’ve got a lot to cover this week. First is housing. And David is telling us that it’s time to pay attention to housing. When everyone was freaking out last year, David had a very cool head, and now he’s starting to pay a lot more attention to it. Gary is going to talk to us about the Fed and bond vigilantes, which I think will be a really interesting discussion. And then Tracy is going to talk to us about soft commodities. We may be able to get a little bit talk about the NatGas stuff that happened this week, but we’ll talk about soft commodities and why they’re rallying so hard.

Everyone, we’re having a quick promotion for our CI Market Platform. This is our platform that forecasts currencies, commodities, equity indices, individual stocks, and global economics. Right now, you can get 40% off of prepaid annual subscription. It’s a limited-time deal. That brings the price down from our normal $500 a year to $300 a year. Visit completeintel.com/save200. Use the promo code SAVE200 at checkout.

The deal is designed to help you better plan your portfolio and see the forecast of your investments and global markets. It’s our way of saying thank you for being a part of the Complete Intelligence Community. Again, visit completeintel.com/save200 and use the promo code, SAVE200, to check out.

Thank you. Guys, thanks so much for joining us. Gary, thanks for joining us for the first time this week. I really appreciate the time you guys take for this.

Gary Brode

Thanks, Tony. Great to be here.

Tony Nash

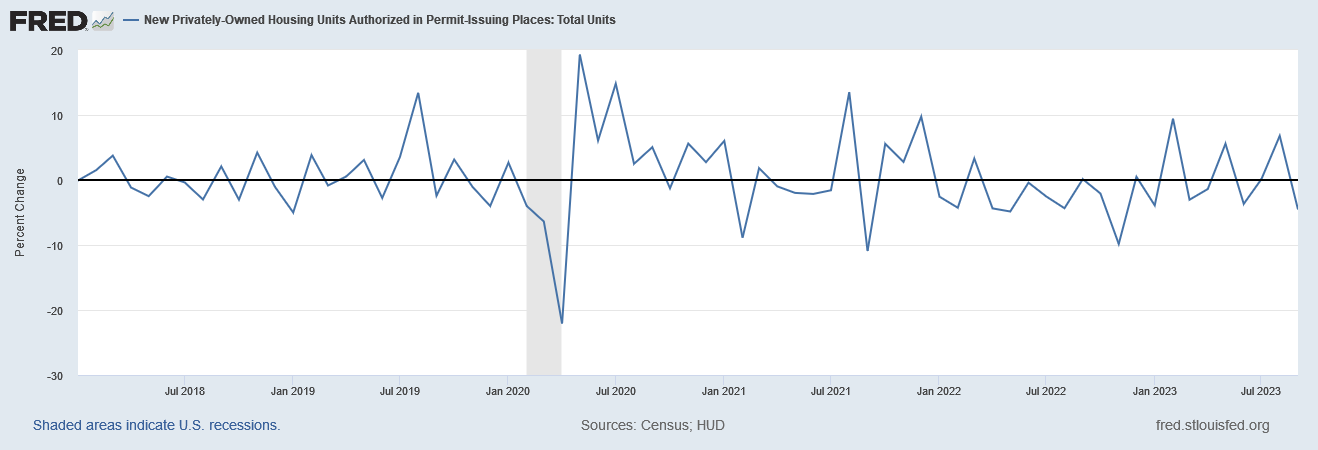

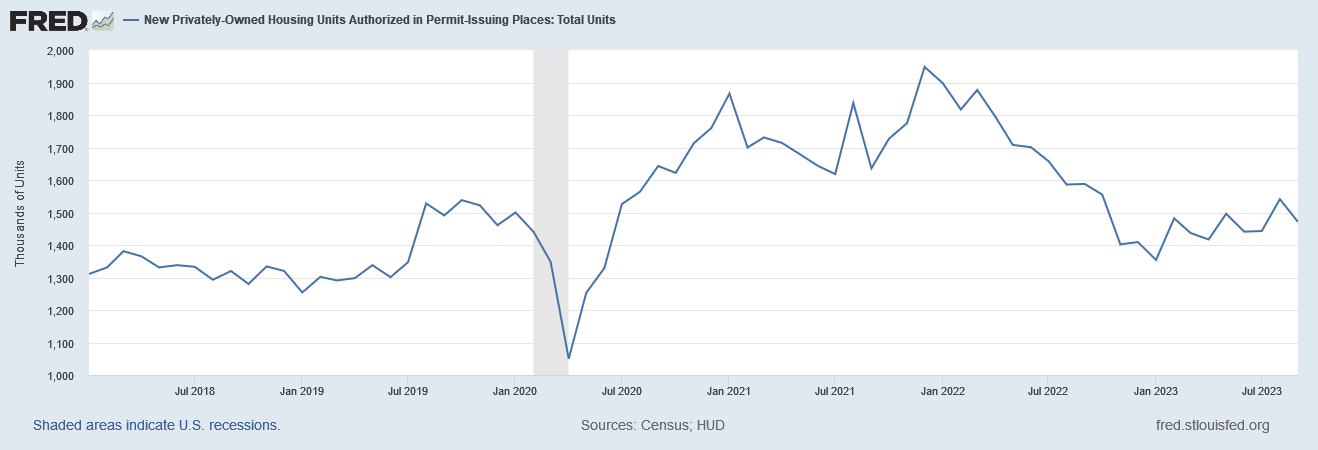

David, you remained fairly bullish on housing, or I would say not as bearish as many people last year when it got a lot of attention. You kept your head. You saw housing backlogs really as a key driver there. Lillie, you’ve really started to rethink that a bit. Part of this is based on the permits data, which we’ve got some of that on screen right now, both the % change and the total permits, which were down pretty hard in September. You say the backlogs are pretty played out. Can you walk us through what you’re looking at in housing now and what you think will play out in the near term?

David Cervantes

Yeah. First of all, thanks for having me. Glad to be here with everyone. Let’s just take a step back into the initial thesis and how that evolved. I think when the housing market started freezing up, mortgages rates started mooning and sales started collapsing, a lot of people conflated that for the impact or for actual economic activity. In reality, that’s just paper shifting. When people buy a house, there’s no new wealth created. I mean, maybe for somebody, but it’s zero sum. It’s a wealth transfer maybe, but there’s no new net wealth created. It’s like buying stocks. In any case, I was focused on actual economic activity that goes into national accounts for GDP accounting. What really matters for the cycle is construction spending and construction employment. Due to the backlogs, those were at all-time highs. Despite sales falling off the cliff and mortgage rates moonshotting, actual economic activity that made it into national GDP accounting remains strong. In addition, fixed residential investment was down, I believe, in Q3, 26% and Q4, 22 %. And I hypothesize, well, it doesn’t need to get necessarily better, it needs to get less bad. And I figured if it got less bad, we could get a growth impulse later in the year.

David Cervantes

And that’s exactly what happened. Fixed residential investment went from detracting from GDP to becoming mildly additive to GDP. We just got the GDP report yesterday. Q3 expectation was for it being 19 basis points additive to GDP came in line at additive 15 basis points to GDP. Now that’s all in the past. I think now with the backlog cleared out, we need to start paying attention to the data that we used to pay attention to, but that became noisy and muted due to the backlogs. So with the backlogs out of the way, I think that some of the signal in things like permits is going to start to matter more now because there are no backlogs to fill that gap anymore, or there’s less of them rather to fill that gap. So the expectation that I have is that with that impulse out of the way, we will see some deceleration not only in the sector, but also in the general economy. In fact, today, Atlanta Fed GDP, just a few minutes ago, I posted on Twitter, came out with a 2.3 expectation for the fourth quarter of this year. Yesterday came out saying 2.5 was my estimate.

David Cervantes

That was 20 basis points off. This is a fluid thing, but that’s where we’re starting from, is that we are already baking in a slowdown from the toward pace of growth we saw in the last quarter.

Tony Nash

Okay, so 2,3 is more in line with, say, a slightly above trend growth for the US, right? So 4,8 or whatever it was yesterday, obviously way ahead of where we should be where we are right now as an economy. I know you’ve been very bullish on economic growth all year, which is great, and you’ve called this excellently. With housing, so you’re saying even with the backlog is clear, do you expect housing, say, construction jobs to continue to decline? Is that what you’re saying?

David Cervantes

The answer is on the residential side, yes. Right now, it’s a huge market. There’s industrial construction, there’s manufacturing construction, and there’s a lot of IRA money that’s going to go into those sectors. But for purposes of tracking the economy, I really pay attention to the residential side. The reason is that’s the most volatile of the construction sectors, and that is what typically leads into and out of a recession. Seven out of 11 post-war recessions have started with a significant drop in fixed residential investment. That’s been the historical experience. I’m watching the residential side. That’s the answer.

Tony Nash

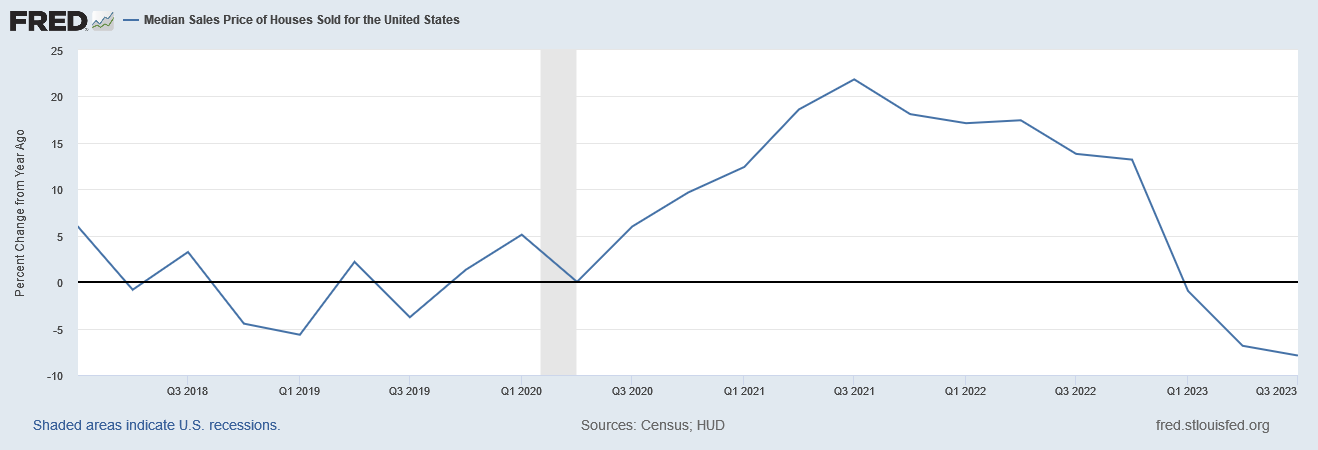

Can we talk a little bit about meeting house prices? If we look at meeting house prices, they started to fall in Q1 of this year. Of course, that’s local markets. San Francisco would be the same as Houston, Texas or whatever. Q2 and Q3, that decline accelerated. Can you talk us through what do you have expectations on, say, median house price to go in line with your housing thesis?

David Cervantes

The answer is not really, and here’s why. Again, house prices aren’t in and of themselves economic activity. But I still watch them for this reason. Rental prices lag, housing prices with the 12-18-month lag. As we know, the real sticky part of inflation has been OER. I forgot the. I’ve had a brain fart now on the acronym.

Tony Nash

Owners equivalent rent.

David Cervantes

Exactly. Thank you. Owners equivalent rent. That’s been sticky and still at a high single-digit level. I believe it’s 7.8, the last reading, but tomato, tomato, give or take, a few basis points. It’s still high historically. I think as long as house pressure prices have continued to moderate, either outright declines or at least increasing at a slower rate, I do think that rental prices will moderate and chip away at that sticky OER. For me, that’s really why I’m watching house prices. Not for any tells on the economy per se, but on the inflation front.

Tony Nash

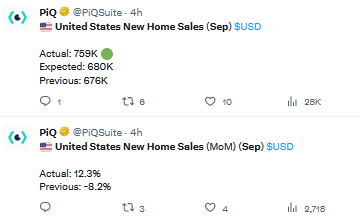

Okay, so I want to come back to that in a second, but I want to also talk about this information we have about home sales, which came out this week. Actual home sales in September in the US were 759,000. The expectation was 680,000. Year on year, it’s 12.3% growth where it was… Sorry, that’s month-on-month, 12.3% growth. The expectation was a negative 8% growth. With housing prices falling, are people going in with cash to buy those houses? Or why do we see this a little bit higher than expectations?

David Cervantes

Well, I think that’s a really good thing you bring up. Here, I think, is part of the issue. The number you referenced was for new home sales, not for existing home sales. The existing home sales market is frozen. There is no action. Whether it’s sellers that have a 3% mortgage and don’t want to leave it or they just can’t pull up the funds for a different, I don’t know, for whatever reason, the existing home sales market is basically frozen shut. And so we’re seeing a lot of that activity shift to new housing, especially with the larger home builders. They’re offering the rate buy downs. They’ve got the balance sheet, they’ve got the institutional wholesale funding to buy down these mortgage rates. Because of that dynamic, a lot of this is just shifting from existing to new.

Tony Nash

Okay. Let me open this up a little bit. If we go back to the rent discussion and we look at how price is declining, especially with rent, as rent starts to fall, does that have an impact on service industry inflation? Meaning, is the pressure on hourly wages, the upward pressure on hourly wages, is that alleviated a bit if rents start to fall?

David Cervantes

I think the answer is no. Wages come first and wages drive rents. What we’re seeing now, what we are seeing though, is a decline in the rate of growth of wages. I believe that the most recent one came out at 4.3. It was previously at 4.5. The Atlanta Fed does have a wage tracker. If you pull up a graph of that, you will see a precipitous decline in wages over the past few months. Okay. That’s actually what the Fed is. They have different economic linkages that they’re targeting. One of them is the real estate channel, the other one is the wage channel. They’re trying to address both of those so that they reduce aggregate demand. Ultimately, reducing aggregate demand is what they’re trying to do.

Tony Nash

Right. Gary, did you have something on that?

Gary Brode

Yeah, David, I want to ask you a question on one part of what you were talking about related to the residential market. I agree with you that people, if we’re going to say trapped with a 3% mortgage rate, they have an incentive not to sell. That’s kept inventory off the market. It’s kept housing prices very high in an 8% mortgage environment where affordability has plummeted. The question I’ve got for you is don’t you think one of the things that will help bring this in equilibrium, meaning more transactions at lower prices, is people will often sell houses for non-financial reasons. Like a death or a birth or somebody ages and they’re going to assisted living or change a job. This is one of those things where people might be able to hold off for a while, but at some point, life circumstances mean you have to dump the 3% mortgage and deal with whatever your current life situation is. Don’t you think that ends up bringing more inventory on the market and bringing prices more into equilibrium? By equilibrium, I mean more transactions at lower housing prices, particularly with 8% mortgages.

David Cervantes

The answer is yes, but that’s a slower moving… The answer is yes. It’s a question about what rate. And does that happen in time to unlock that market to make it economically beneficial? So all these things you mentioned are life things that you can probably kick the can on for a year or a year or two. Eventually, yes, you got to face reality. If you’re an empty nest or your kids are off to college and you just don’t need that 4,000-square-foot-Mid-Mansion or whatever it is you have. Yeah, at some point reality kicks in. But to make it cyclically important, I think we’re at a different bind right now for that to make a difference.

AI

Heads up for a short break.

Are you using the potential of AI in your portfolio management strategies? With an impressive 94.7% forecast accuracy on average, you can confidently integrate AI into your approach with CI Markets. Visualize the potential volatility of your portfolio over the next 12 months and gain insights into specific assets that might experience fluctuations. This empowers you to make informed decisions on when to buy, sell, or hold. CI Markets covers a wide range of over 1,600 assets, including stocks, commodities, forex, indices, and economic indicators. Imagine running limitless portfolio scenarios to optimize your gains. Curious about the outcome of removing or adding certain assets? Wondering how your portfolio might evolve in the next 3, 6, or 12 months? CI Markets equips you with answers to these crucial questions. Whether you seek a streamlined portfolio analysis, wish to explore diverse scenarios, or aspire to track your investments with precision, CI Markets is the ultimate tool for you. Ready to learn more? Visit us at completeintel.com/markets. Thank you and now back to the show.

Tony Nash

Can I ask you guys another probably weird question, but with the amount of money on credit cards in the US, could credit card debt push a segment of the population to sell their homes? Because that’s been rolling around in my head for a few months, and I’ve never really looked into the research on that. But could that be something that could move the housing market? Yes, somebody has a 3% loan or a segment of the population has a 3% loan, but they’ve had to put so much on credit cards over the last two or three years, and that’s bursting at the seams. Could that be something that pushes the housing market or is that just too on the edge that it’s really not going to impact that much?

David Cervantes

I would think as long as employment stays low or unemployment stays low, employment high, I think it’s a non-issue because as long as people can service their debt and hit their monthly or whatever, but look, a lot of houses are owned free and clear. I don’t know what the number is. I know it’s at a historical high where there’s a lot of equity. Granted that with rates aren’t where they are, that cost of equity is expensive, but it’s probably cheaper than your credit card debt. So I think at the macro aggregate level, there’s a ton of housing equity that can cover any shortfalls for a while as long as the employment picture stays okay, which right now it’s still a hot… By all definitions, it’s still a hot labor market.

Tony Nash

Okay, great. Go ahead. Go ahead, Tracy.

Tracy Shuchart

I had a question, Mario, on this. Do you foresee any problem right now with repayment of student loans and say, new first time home buyers and/or renters coming onto the market and having that cost some ripple in that market, in the housing market?

David Cervantes

I know. I think the student loan issue is overblown from a macro standpoint. Again, looking at the numbers sound big and scary, but my heuristic is take whatever macro doom problem you have divided by nominal GDP and you probably get a really small number. Typically it’s not big enough to really make a difference at the aggregate level. This is a $27 trillion nominal economy. It is huge. Last quarter, in one quarter alone, we grew the size of New Zealand’s GDP. Just to let that sink in for a moment, how big this economy is. When you take a problem like student loans, I don’t know exactly what the number is, a couple of hundred billion and you divide it by an auto GDP, you end up with a small number.

Gary Brode

David, I agree with you. One thing I’d add to that as well is for all the talk about our very high credit card debt, and granted, it has gone up a lot, but one of the things people don’t add to their evaluation of that is inflation. If we go from a certain level of credit card debt to a higher level, part of that, yeah, it’s more nominal dollars, but what does that actually represent as a percentage of household budgets? The issue that you’re talking about, how much does this matter in terms of GDP, that also plays out at the household level as well. How much does this play out in terms of our assets or our high income? Again, in nominal dollars.

David Cervantes

Right. It puts consumers in the privileged position of being a debtor in a higher than normal inflation regime, which means it deflates. Your debt is nominally fixed, but as long as inflation remains high, it gets deflated over time, especially if your wages rise. If your wages continue to rise, that real burden falls over time. It’s like what governments do all the time: deflate their debt.

Tony Nash

Okay, so great info on housing. What action can I take as a result of that? What are you watching as a result of where housing is right now and what’s happening in housing markets?

David Cervantes

I’m actually watching The Home Builders. I had a fantastic trade lap first half of last year. Killed it. Took off risk in middle of August. It was partially I got vibes and partially I was on vacation and I don’t like having a risk on when I’m on vacation. I got lucky, partly. But since late summer, housing stocks have been hit hard. But I think once we see some normalization in the yield curve, anything that any trade that involves borrowing low and lending high, a normalized yield curve is going to potentially do really well. Though, home builders being very leveraged to the economic cycle, home builders using their institutional buying power to buy down rates and deal with that. I think once we see some normalization of the curve, and we’re starting to see that, once we see some normalization of the curve, I think the home builders could be at play again. I’m looking at that. I’m also looking at Annaly Mortgage and REM, similar type of business that the Mortgage REITs. They’re basically just levered, borrow near, land-high operations. I think those trades could do really well.

Tony Nash

Perfect. That’s great. I love it when an extraordinarily smart person attributes their success to luck. It’s just it’s so humble. Thanks for that. I love it.

David Cervantes

I’ve burnt my hand on the stove enough times to know that I don’t know all the answers.

Tony Nash

Yeah. I’ll take luck over intelligence any day of the week. Let’s move on to the Fed and bonds. Gary, one of your recent tweets says that the Fed has lost control. I want to hear about that. Your tweet about this saying that Powell acknowledges that the bond vigilantes are in control. Can you talk about that? Why is that important and what near-term impacts do you expect?

Gary Brode

Sure. Thanks, Tony. The key thing is, at the last Fed meeting, the Fed kept interest rates flat. They basically paused three months ago. One of the things he acknowledged, which I think is accurate, as he said, the bond market is doing a lot of the Fed’s work for him. He’s right about that. If we go back three months to the last time the Fed raised rates, we had the yield curve where it was. In the three months since then, the short end of the curve, the Fed funds rate through the three-month treasury have all traded about flat. Well, the Fed funds rate has been completely flat. But the long end of the curve, the 10 year, the 20 year, the 30 year have all traded up about 100 basis points, and roughly half of that move has come in the last month, the last four weeks. What he’s recognizing is that the bond market is starting to price the long end of the curve at a much higher yield than it was despite the fact that the Fed hasn’t done anything. He’s saying, Wait a minute, the bond market is going to slow down the economy for me.

Gary Brode

We don’t need to do as much. I think he’s right about that. But to me, the key point is let’s take a look at why the bond market is reacting the way it is. We got this great question. I forget who it was, but somebody on Twitter asked this brilliant question, Wait a minute. We’ve got higher bond yields and gold and Bitcoin are going up. What in the world is going on here? My assertion is that all three of those markets and Powell are all watching Congress. We have a situation now where we had this budget deal back in June, July, where both sides pretended that there was this horrible, long, bitter, six-month fight. But we all knew the end result was going to be a solution that just guaranteed more and more and more spending. They agreed on a solution that would result in an excess of $4 trillion of spending in the roughly year and a half between then and the next election. It’s always amazing to me how they always finance it through the next election. Because, of course, we’re not concerned about our jobs. We’re not being selfish or self-interested where this is what we’re doing for the American people. Okay, great job.

Tony Nash

They’re all on the same side.

Gary Brode

I completely agree. I completely agree. We have one party. One of the things that I’ve said is the Republican financial plan is like being a waiter and coming to the table and saying, By the way, if you’d like, we’ve got a Republican plan for your dinner. I’m going to put enough poison in your dinner to kill you. The Democratic plan is we’ll offer you more poison than that. Either way, you’re dead. What’s the difference? If there’s anybody in Washington, the people that are serious are saying, We’ll give you your poison with dessert and acting like that’s a favor. What’s happened here is they’ve agreed to overspend by $4 trillion over less than two years. This is all happening with higher interest rates. Let’s just take that $4 trillion of spending, they’re going to monetize. It was just a fancy way of saying there’ll be more currency units created. If you assume a 5% rate on that, great. That’s another more than $200 billion over the next two years. That’s just the interest on the excess spending for the next two years. Add to that the fact that we’ve got 10-year securities rolling off with a rate of less than 1%.

Gary Brode

They’re replacing that with 5% paper. What we’re looking at is a situation where interest expense for the federal government was $400 billion a decade ago. It was $600 billion a couple of years ago. It’s now a trillion dollars heading for in the next couple of years, somewhere between 1.5 and $2 trillion. Let’s add that to the calculation. Basically, Congress is going to monetize another maybe $5 trillion over the next year and a half, and that’s assuming they’re on budget. Anybody wants to take the under on that, I will take that bet right now. What happens now is you have more currency units being created. In this case, it’s the dollar, the Fiat dollar, and it’s chasing the same amount of goods in the economy. All we’ve done is replace the meme that we’ve had over the last decade. We’ve all seen the meme of Powell and the Fed making the money printer go bur. Well, great. Now it’s Congress. What’s happening right now is the bond market, the Federal Reserve, the gold market, and the Bitcoin market are all watching Congress. Yeah, we’ll watch Powell’s press conferences and we’ll be interested in what they do next.

Gary Brode

But the truth is, at this point, it’s the bond market that has control, and they’re watching Congress. Tony, as you’ve pointed out, there is other than Rand Paul, there is no one in Congress even making noises about being fiscally responsible. There’s just going to be unlimited currency creation.

Tony Nash

Okay, so let me take a step back and ask a couple of questions, and David and Tracy jump in here. You started out talking about the Fed and the bond guys taking over, David talked about how the service wages are going down and other indicators that the Fed has managed are moving in the direction. The Fed has handed off some of their work to these bond vigilantes, whether they wanted to or not. Service wages are coming down as a result. From my perspective, although I don’t love to love these guys, it sounds like the Fed’s job is being done. Is that fair?

Gary Brode

I think what created the problem was more than a decade of zero or near zero rates.

Tony Nash

Of course. Yeah. I’m talking about.

Gary Brode

Their job- Right now. -let’s say.

Tony Nash

Over the past 2-3 years.

Tony Nash

Their job is being done. We don’t want to acknowledge that and we don’t want to say we like the Fed, but their job is being done. David, do you agree with that?

David Cervantes

I mean, beauty is in the eye of the beholder. It’s a question of what do you think their job is? If you take the- The inflation right now. Yeah. We’re experiencing a disinflationary impulse. There’s no argument there. The question is, what does the future look like based on what Gary said? I respect what he said. I’ll just take it as truth. Then maybe not. If they’re not doing their job. If you look at nominal… My favorite metric is nominal GDP. Right now, as of yesterday, 8.5%. It’s not in line with their target. Their target is around four, four and a half %. Five would be in the high side, but we can probably excuse that away. If you use a nominal GDP as a metric, the answer is no, they’re failing. That’s the answer. It really depends. What’s your metric?

Tony Nash

Okay, that’s great. That’s perfect.

Gary Brode

David, I would add one thing to what you’re saying, which is a huge part of nominal GDP right now is government spending. We have this really weird quirk in the way we calculate this where government spending is additive to GDP, nominal or adjusted, whether it creates value or not. We’ve all heard the constant example of you pay half the country to dig ditches, the other half to fill in ditches, and if the government pays for it, we’re adding that to GDP. I agree with you, Tony, that the Fed has done the right thing right now. The problem is everything the Fed is doing, Congress is undoing, and they have diffuse responses responsibility. My belief and one of the reasons why I have believed Powell over the last two years when he’s been screaming higher for longer and the whole market said, He doesn’t mean it. He’s going to pause. He’s going to pivot. We’ve heard all that. I’m like, No, the reason I believe this is because I think Powell is terrified to be the next Arthur Burns and he wants to be the next Volker. He does not want to have his last job in the public sphere being the next guy who failed on inflation.

Gary Brode

The issue he’s got is he’s now fighting Congress and they have to diffuse responsibility and they will blame everybody but themselves for the inflation that will inevitably come when they monetize the next two, three, five, six trillion dollars of currency units. They’ll blame Vladimir Putin, they’ll blame greedy corporations because corporations only became greedy in 2021. They didn’t want to make profits before that. I think they’ve done the right thing, but they’re like the Bank of Japan. I know you guys were talking about this in a recent episode. They’re stuck. There’s nothing they can do to go forward or backwards and whatever they do is being undone in Congress right now.

Tony Nash

Okay. Tracy, you keep nodding yes.

Tracy Shuchart

Yeah, I’ve been saying that, and I think this problem is going to get worse headed into an election year because this administration is going to do everything they can to avoid a recession. Obviously, nobody wants a recession. They want to get reelected. I know everybody says, Yeah, but we have the House that’s dominated by Republicans, but they’re wishy washy.

Tony Nash

They spend as much as everyone else.

Tracy Shuchart

Let’s call a spade to spade. I just think this problem is going to get worse and we’re going to still have monetary policy butting up against fiscal policy, in my opinion.

Tony Nash

Let me ask all of you. Guys this-

Tracy Shuchart

Maybe, Gary, we can expand on that.

Tony Nash

Yeah. David’s talked about nominal GDP, not overheating, but accelerating. We’ve got a disinflationary environment. Gary’s talking about the Congress doing trillions of dollars of additional spending, but unless we have a recession or an emergency, how are they going to justify a multi-trillion dollar spending plan?

Gary Brode

Well, they’ve already done that.

Tony Nash

Additional.

Gary Brode

That’s where we are now. We had a situation where we had GDP growth, insanely low unemployment, rising wages, an economy that was in really good shape and high levels of government spending. Remember, every time we’ve had a so-called emergency, we ramp up spending and then that’s the new baseline. We saw that in 2008. We took the baseline spending from the TARP plan and a trillion dollars of supposedly shovel-ready plan. All of that was the new baseline. Then we had COVID spending. That was a one-time emergency. That’s now the baseline. They’ve passed $2 trillion dollars of hilariously named inflation reduction as if the government pouring another $2 trillion of currency into the economy was going to lower prices for people. We’re already at insane levels of spending and nobody’s showing any signs of slowing down. Here’s the better question, Tony. Who in Congress is going to stop the next big spending bill?

Tony Nash

Well, okay. That’s a great question, but if this is going to happen anyway, why should we worry about it? I mean, I hate to be so fatalistic, but if we know this is going to happen anyway, why does it matter?

David Cervantes

I think it matters because if you have a situation with fiscal dominance, if we move to a regime of… We’re already in a regime of fiscal dominance. The question is, does monetary policy offset that and try to keep nominal and real GDP at a sustainable level? Or does the Fed have to do a monetary offset? I’m sorry, do they avoid monetary offset? And then policy goes off the rails. To Gary’s point, I don’t think that would happen because Powell is concerned about his legacy, and I think he cares about the institution as well. I think he’s trying his best as a public servant. I think if fiscal dominance does overreach, I think the Fed will deliver monetary offset. The way that will express itself will be in the yield curve. We’ll see even higher for longer.

AI

Heads up for a short break.

AI

In the fast-paced world of investments, staying informed is the key to success. Introducing CI Markets Free, your source for AI-powered forecasts. With our free version, you get access to powerful tools that help you make informed decisions. Join a community of savvy investors, analyze market trends, plan your investments strategically. Stay ahead with monthly forecasts, compare assets effortlessly and download data for your analysis. Don’t just take our word for it. Our users love the valuable insights CI markets provides. Get started today with CI Markets Free. No credit card required. CI Markets, your source for AI-powered forecasts.

Thank you and now back to the show.

Tony Nash

Higher or for longer? Okay, great.

David Cervantes

With lots of ERs at the end.

Tony Nash

Exactly. It’s like Abenomics from 2012 until whenever. It just became more and more intense. We could have something similar here. Gary, just back to your report that you sent me, inflation targeting is something that obviously is talked about, and one of your reports talks about that. Can you talk about how changing the inflation target would matter in an environment like this?

Gary Brode

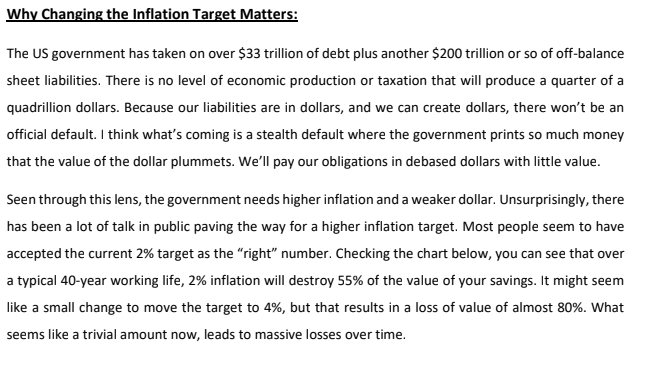

Yeah. So it’s a great question because what we’re seeing right now are a large number of people saying, Oh, well, we can fix the problem by changing the inflation target. Right? I mean, this is like you’re a marathoner and you get to the 24-mile mark and someone’s like, close enough, let’s just stop. Okay, great. But that’s not effective. Tony, you’ve been, in my opinion, correctly critical of the Federal Reserve. I’m 100% with you. Let’s talk for just one second about the danger of the existing discussion. Everybody accepts 2% as the correct reasonable, moral, fine inflation target. We all just… It’s and it’s only 2%. You pay a dollar for something one year and it’s a dollar two next year and who cares? It’s small. Okay, this is theft. Because over a 40-year working life, and most people have a 40-year working career, a 2% inflation rate, people forget about compounding, destroys 55% of the value of your money. That is value that is going from you to the government and the ability to do that is called senior. Just a fancy word for stealth stealing by the government. People say, Oh, well, you know what’s the big deal?

Gary Brode

We’ll just move the inflation rate to 3% or 4%. Okay, well, let’s talk about the implications of that. A 4% inflation rate over that same 40-year working life for people takes 79% of your money. Four out of every $5. There are people-

Tony Nash

What you’re saying is I get to keep 21% of it.

Gary Brode

Yeah, right. Congratulations. Fiat economics. It’s phenomenal for everybody. Part of the problem is they only steal a little bit at a time. By the way, that’s assuming you believe the CPI. I don’t. The CPI is hugely understated. OER, which you and David were talking about earlier, is a huge reason why that’s a big part of it. But because they’re stealing slowly and quietly and no one really knows who to blame and Congress can blame everybody, people, they let it go. But the real correct moral rate of inflation is zero. Two % is itself obscene, but going to 4 % and you’re losing, like you said, you get to keep 21 cents out of every dollar you make over your working career.

Tony Nash

Pre-taxes.

Gary Brode

Yeah, exactly. They’re stealing from you in a lot of ways, but at least taxes people know who to be angry about. Inflation is stealth stealing. What we’re seeing, one of the things that I think is really interesting is last week, one of the leading candidates in Argentina promised his people no taxes. This was not a President Bush, no new taxes. This was no taxes. He’s not offering to cut the massive size of the Argentinean government. Basically, what he’s saying is we will pay for 100% of our spending in inflation. The Congress, rather than viewing that at the US Congress, rather than viewing that as a warning, is saying, Oh, wait, that’s a great model. We can tax people an unlimited amount with this and we won’t get voted out of office. We can now be the Santa Claus of free stuff. We can be the Santa Claus of low taxes and we can blame inflation and everybody but ourselves. It doesn’t matter. It still ends in disaster either way. To anyone listening to this, I would strongly suggest that the next time you hear somebody talking about, Oh, just raise the inflation rate and that’ll solve the problem, push back on that.

Gary Brode

Help people understand that inflation is the way a government harnesses the currency to take money from you without you noticing, but it’s still theft.

Tony Nash

Yeah, but it’s just 4%, Gary.

Gary Brode

By the way, here’s the best one. We remember every time a taxing authority, whether it’s a state or the federal government in the United States, income taxes, it always starts at 1% and it’s temporary. That worked its way up to 90% tax rates at one point, and nothing is ever temporary. I promise you, if we don’t hold the line on this and we say, Okay, fine, we agree to 4%, does anyone here think it’ll stay at 4%, there’s no way in the world. Tracy, what’s next? 6, 8, 10?

Tracy Shuchart

Exactly.

David Cervantes

Sounds like my property taxes, I think they’ve doubled since we moved into the suburbs.

Tony Nash

I live in Texas, we have very high property taxes. No state income tax, but we make up for it in property tax. Okay, Gary, that’s all great. Thank you for all of that. Let’s move on to commodities. Tracy, we have seen a lot of upward pressure on soft commodities, really since the pandemic. Things like cocoa, orange juice, sugar, cattle. What’s happening with these soft commodities to push up those prices?

Tracy Shuchart

Well, I mean, I think you have to look at each one of these individually because they have their own unique set of problems you’re having. So for cocoa, for instance, we have most of those crops are located in West Africa. West Africa crop is doing poorly. Obviously, bean deliveries and ports on the Ivory Coast are about 16% behind this season. I won’t go into total details, but again, it’s a weather issue as well. El Niño is threatening dryness in West Africa, et cetera. That’s because so cocoa is really because the crop is really in one specific area. A lot of the crops are in one specific area. If we look at sugar, for example, we have a deficit that’s grown as a result of poor Indian Thai crops, which are huge. We also have issues in Latin America right now in Colombia and also in North America, in Mexico. We’re having issues there. If we look at cattle, I think cattle was on your thing, but it’s not a soft, so let’s move to OJ. If we look at… Florida is a really interesting case because it’s the largest orange juice or it’s the largest orange crop producer in the world.

Tracy Shuchart

For the very first time this year, California is going to beat us. Really, we have had our worst orange crop in the last 70 years. This is due to several problems that are really unique. Well, one, hurricanes, that’s not. We’ve had weather-related issues. We also have a deadly disease called citrus screening, which is an invasive Asian bug, essentially. But what is unique to Florida and really different is that what is happening is as people are moving into the state, those properties are actually being sold. Those crop properties are actually being sold to residential home construction. This is what is happening in particularly the Orange juice market in Florida.

David Cervantes

Hey, Tracy, I have some questions for you. You mentioned California. California has been a drought for a long time. Up until I believe it’s last year, they’ve gotten so much rain, they are no longer in drought conditions. In fact, some of the areas where I grew up in the Central Valley, some of the lakes that were drained and dikes and levees were put up for the irrigation system have returned. You’ve got these-

Tony Nash

Really?

David Cervantes

Yeah. Lake Tilare, I believe it’s called, was filled in the 1800s and it’s now refilled and yet farmers… This whole system was developed around farmer interests and looks like Mother Nature just took over instead. Too bad. But is the causality of California getting more involved in the secretion market due to the rehydration of the state or is that just some other factor? I’m just curious.

Tracy Shuchart

Yeah, I think it’s definitely helping. But we really haven’t seen the results of that yet. We really won’t know for a couple more seasons how that really pans out. Yes, their crop, their 23, 24 crop is much larger than it’s been, but I think we need to give it a couple more seasons to see how really those weather patterns filter into actual production.

Gary Brode

Tracy, any thoughts on fertilizer? Because you’re talking about these increases in prices. There have been fertilizer shortages. I know Russia has declined to export to certain parts of the world that we would care about in this case. Where do people get fertilizer now and how much is that impacting all of the issues that you’re talking about?

Tracy Shuchart

Yeah, well, I think right now, obviously, we saw that big run-up in 2021 to 2022 where we had a lot of shortages. We saw a big spike in prices. Everything’s come back down to normalized prices now because that might calm down a little bit. But I think what we really need to focus on right now is the drought situation in the Mississippi River, because what’s happening is that’s impacting not only what farmers, which farmers use that Mississippi River to send their goods to the Gulf Coast to be exported elsewhere, which is huge. With lower river levels, that means that you either can’t pass through and/or higher shipping costs because you need to split your product to make your vessel lighter. We’re also seeing problems with that in shipping fertilizer. Then again, in Florida, Florida is a huge fertilizer producer, has also been impacted over the last two seasons during hurricane season. We need to keep an eye on it. I’m not that worried about it right now, but it’s definitely worth keeping an eye on, especially if we start to see some rise in natural gas prices, which if you look at the weekly chart right now, we’re just about starting to break out.

Tracy Shuchart

We could have problems in Europe this winter. If we see a spike in natural gas prices again, you’ll probably see a spike and corresponding spike in fertilizer prices.

Tony Nash

As well. Okay, before we go on to NatGas because I do want to ask you some bonus questions on NatGas. But I do want to say that whenever I see AG prices spike, the first thing that I think of, you know what it is? Coffee prices.

Tracy Shuchart

You’re like, I could do it.

David Cervantes

I know why. I know why. I know why. I know why. I know why.

Tony Nash

Much to my relief, coffee prices are down 40% from the peak. We’re not seeing the run-up in coffee prices like we are with some of the other softs, which is such a relief. Tracy, can you talk us through some of the NatGas drama that’s happened this week? I know there’s been a lot of noise about it. I just want to help people understand what’s happening in those markets.

Tracy Shuchart

Well, we’ve had… Well, first of all, the obvious-obviously being the Israel-Hamas conflict, and they shut down the Tamar Field right off the Coast of Israel. However, I will say that’s relegated to being a regional issue more than a global issue, being that Jordan is the main importer of Israeli gas from that particular field. They’re more impacted than anything else. There is a pipeline to Egypt, so that means less exports out of Egypt. But again, I think the problem is mostly regional. I think we saw a kick-up in prices initially, obviously because of the region. We saw a kick-up in oil prices as well. Then we had the first cold snap in Europe, and I think that got the market a little bit jittery. I think that’s what the market is reacting to right now. But I do think Europe is not out of the problem. You have to realize their storage may be 90% full, but that 90% is only 25% of what they use during the whole winter. It’s not like their storage, We’re 95% full, so we’re good all winter long. No, it’s not really how it works. If we do have a colder winter, they’re still not out of the woods yet.

Tracy Shuchart

If manufacturing picks up for some reason, I don’t know what that would be, but if it does, then you’re also going to have a bigger problem. It’s definitely a market to watch right now. If we’re just looking at it from a technical standpoint, this market is very short. Any breakouts you could very easily see a short squeeze.

Tony Nash

Just for reference, NatGas is up over 10% today on Friday. The price right now at 350 is about half of what the price was a year ago at just over seven bucks.

Tracy Shuchart

Yeah, you have to… We just spent almost nine months flat.

Tony Nash

Exactly. We were-

Tracy Shuchart

In consolidation.

Tony Nash

-260 or something like that. This rise is really coming on fast. I don’t know, do you think we’ll get to the levels that we were at last year, or do you think we’re going to pass that?

Tracy Shuchart

Well, I’m not a weather expert, so I have to see it is a Linear year. Who knows what could happen? Who knows what could happen geopolitically. Those are all things that you need to watch. I think right now, if experts continue out of the Middle East because everybody wants to do business, as usual, even with BombSquad, we’ve seen that in the past. In Texas.

Tony Nash

They can always do business in Texas. That’s good.

Tracy Shuchart

They can always do businesses in Texas. But I could see a squeeze at $5, $6 easily. I don’t know about hitting the highs. But again, I don’t want to be a person that….

David Cervantes

Hey, Tracy. I’m an armchair weatherman only because I’m a snowboarder and I plan my snowboarding trips far in advance. I know it’s going to be a really good season. There’s already snow in Jackson Hole. There’s snow in Mountain hood, Washington. I don’t know if it’s the El Niño effect or some other effect, but it’s going to be an epic snowboarding season. I’m getting my stuff ready. I don’t know how that impacts natural gas prices, but I’m looking forward to the weather.

Tracy Shuchart

Okay, I’m with you.

David Cervantes

Snowboarder or skier?

Tracy Shuchart

I’m a skier, but I’ll tell you. Great.

Tony Nash

All right, guys. Hey, this has been fantastic. Thank you so much for all the stuff that you guys have talked about. This has really been really educational for me. I know you guys put time into it and a lot of thought, so I just want to thank you so much. Have a great weekend. Have a great week ahead. Thank you.

David Cervantes

Thank you all. Take care.

Tracy Shuchart

Thank you.

Gary Brode

Thanks. Bye.

AI

That’s it for this week’s episode of the week ahead. Please don’t forget to rate us and review on whatever platform you are watching or listening to this. Thank you.