Register for a CI Markets account for FREE! No credit card required: https://completeintel.com/markets.

Welcome to “The Week Ahead” with your host, Tony Nash! In this episode, we engage in thought-provoking discussions on a range of critical topics:

1. Price Disinflation Recession: Our expert panel, featuring Seth Golden, challenges conventional wisdom by analyzing the rise in manufacturing volumes and its implications for the economy. Are we on the cusp of a period where valuation multiples could expand once again?

Also, discover differing perspectives on inflation and disinflation as our panelists share their views on the deceleration of inflation rates and concerns about wage inflation and political policies. Explore the impact of interest rates on the housing market and the potential for lower prices due to disinflation. We also shed light on the critical role of diesel prices in the economy.

2. Crude Tumbling: This discussion, led by Tracy Shuchart, dissects the secondary impacts of rising gas prices and the global dynamics affecting fuel prices. Stability in oil prices becomes a focal point as we examine the intricate interplay of factors like global demand and export policies. Comparisons are drawn between OPEC’s influence on energy markets and the Federal Reserve’s impact on equities.

3. DC Drama & Markets: Albert Marko led this discussion and he doesn’t shy away from discussing the lack of unity within political parties and the need for stable economic and fiscal policies. The panel raises concerns about wealth accumulation among politicians and calls for a reevaluation of the system.

The discussion also touches on the significance of the Speaker of the House in US politics and potential candidates for the role. Learn why an efficient speaker is vital for the productivity of the legislative body as we wrap up our discussions.

Transcript

Tony Nash

First is the Price Disinflation Recession, Crude Tumbling, which has… It dovetails with Price Disinflation, DC drama, and the relevance to markets. So… Hi, welcome, everybody. Welcome to the week ahead. I’m Tony Nash. This week, we are joined by Seth Golden, Tracy Shuchart, and Albert Marko. We’ve got some key themes this week. First is the Price Disinflation Recession, which is a really interesting concept that Seth’s been talking about. I just want to talk about crude tumbling, which dovetails with Price Disinflation. And then we’re going to talk with Albert about DC drama and the relevance to markets.

Tony Nash

So before we get started, I want to let you know about a new free tier we have within CI Markets, our global market forecasting platform. We want to share the power of CI Markets with everyone. So we’ve made a few things free. First, economics. We share all of our global economics forecast for the top 50 economies. We also share our major currency forecasts as well as Nikkei 100 stocks. So you can get a look at what do our stock forecast look like. There is no credit card required. You can just sign up on our website and get started right away. So check it out. CI Markets free. Look at the link below and get started ASAP. Thank you.

Tony Nash

Seth, thanks for coming on. First time, really appreciate it. It’s great to have you. I’ve been following you for a long time, and I love your Twitter presence. I saw your tweet about the NOPE index and rising PMIs. Your expectation is for a price disinflation recession, which is at odds with what Albert’s baseline hypothesis, I think, but not a volume-based recession, price deflation-based. Can you walk us through that? I’ve got that tweet up on the screen now. If you can walk us through your NOPE index tweet.

Seth Golden

Yeah. The NOPE index was actually developed by the Leuthold Groups, Jim Paulsen, who retired recently. But it essentially tries to strip out the sentiment factor within these soft data. The ISM is a survey-based report. And I think what becomes a greater magnitude in these survey data is what’s happening at the most basic level in price. So what the NOPE index does is it takes the new orders, that’s the NOV part, and then the price, which is the P part, and it basically takes the new orders and subtracts it from the price. Because when you look at the questions within the survey, the ISM, whether it’s the manufacturing survey or the services survey, there’s never any good price. There’s always this underlying bias within the ISM that is lower bound as opposed to above 50 or expansionary. Jim Paulsen created the NOPE index, which just says, hey, focus on this. It’s already soft data. But let’s see what’s really going on in the economy. So if you take the actual new orders and you subtract them from the price, whatever the reading is, if it’s above zero, you actually typically have a better manufacturing situation, then maybe the overall index is implying, the ISM manufacturing index is implying.

Seth Golden

The threshold or line of demarcation, if you will, in the NOPE index is zero. So a reading above zero is typically expansionary, and typically that is good for the S&P 500. The forward S&P 500 returns on an annualized basis when the NOPE index is above zero is about 13%, I believe. It’s a good gage, not only of what’s going on in the economy, but what could possibly foreshadow market performance going forward. I know that we’ve had this seemingly recession in the manufacturing sector, but there’s various data that says not even close. If we look at just the ISM, if we look at the S&P also, their measure of manufacturing, they’re both under 50, which technically is a recession in those particular industries within the economy. But the reality is if you look at, let’s say, the St. Louis Fed, the total manufacturing output in the United States has been booming. We’re out the from 2022 and through this calendar year. But we’re not getting the manufacturing inputs that we usually do get, which are driving this manufacturing expansion. Usually it’s the refining capacity, and usually there’s some various variables of goods production that is taking place, textiles or otherwise that are driving the ISM and S&P manufacturing data.

Seth Golden

But we have this dynamic since ’22 where it’s actually construction manufacturing, as well as electronics manufacturing that is driving this boom in the total manufacturing here stateside. So I’m not necessarily looking for a recession based on this NOPE index or what have you, I’m just trying to define what is actually going on through the NOPE index. Is it a real recession in manufacturing and or services, or is there underlying strength that just isn’t being realized by the ISM or the S&P manufacturing indices?

Tony Nash

Okay, so you’re saying that the manufacturing volumes are continuing to rise?

Seth Golden

Correct. That’s the most important thing about this. The NOPE index is that it strips out the price sentiment, basically. It gives you what’s actually taking place in new orders. Because if you subtract the price and you’re above zero in the NOPE index, you still have an expansion situation in manufacturing. You don’t really have a recession.

Tony Nash

Okay, so let’s take a look at that.

Seth Golden

Let’s take a look at the actual price that is influencing how respondents are actually answering the questions in the survey.

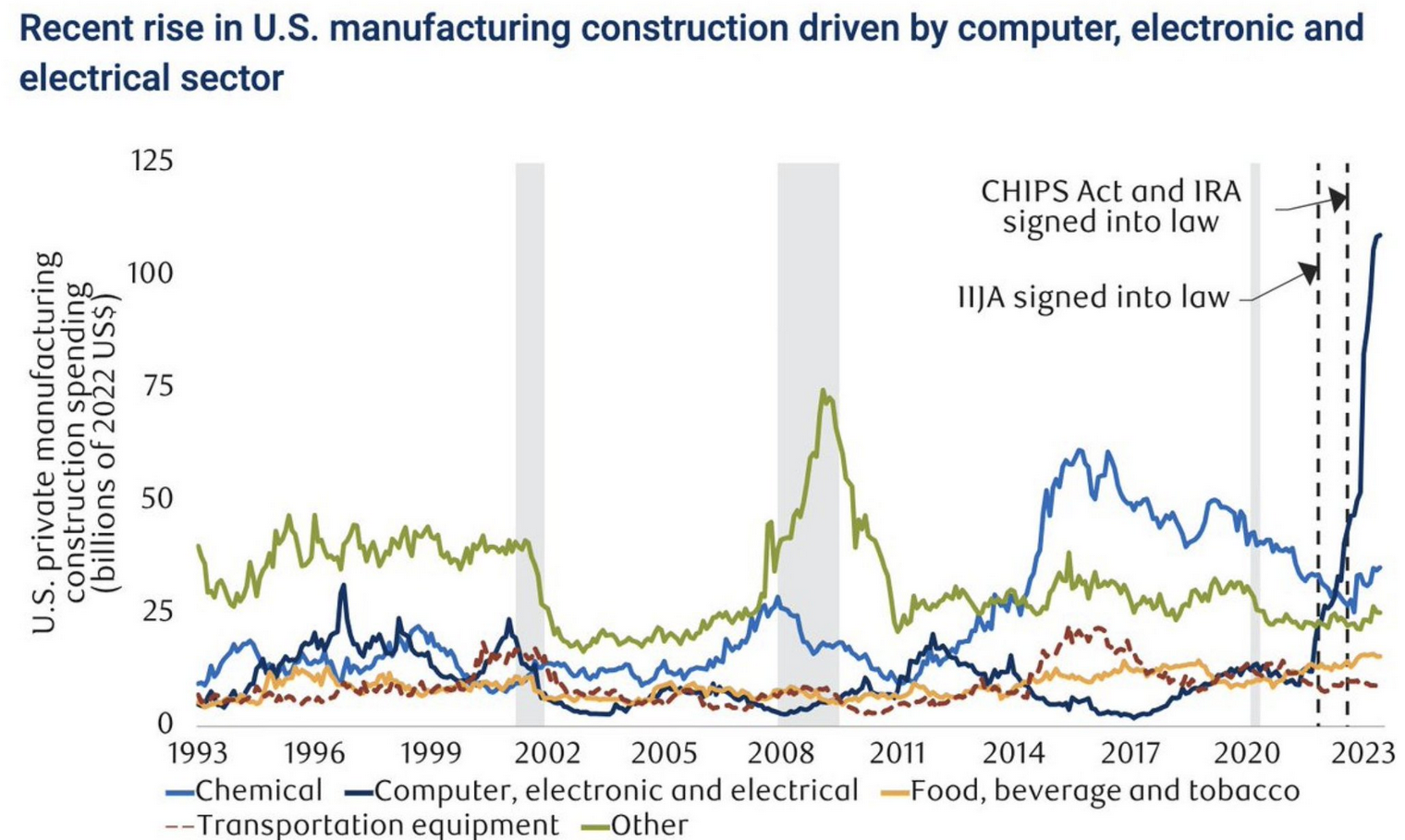

Tony Nash

Okay, so let’s look at this second chart you sent me, and I want to talk about that. I also want to put the price layer on that because I want to make sure that that’s not missed. You sent me this chart, recent rise in US manufacturing construction driven by computer, electronic, and electrical sector. Since these two acts were signed, the CHIPS Act and the IRA signed, we’ve had a spike in computer, electronic, and electrical manufacturing, right? That’s good, right? That’s good for US manufacturing.

Seth Golden

Right. Yeah, you’re getting a lot of transactional volume through that fiscal policy initiative, getting a lot and minimal. I mean, there is some price appreciation in there, but it’s nowhere on the scale of, let’s say, what we see in refining prices through that manufacturing capacity.

Tony Nash

Okay. Where do you pick up the construction or manufacturing?

Seth Golden

Yeah, you’re getting materials. That’s another way that you can validate that this is… Those aspects or industries where we are seeing electronics and computing and construction, we know construction materials and whatnot have actually been disinflating for more than a year now. Whether it’s lumber, sheetrock, concrete, all of those necessary construction inputs are actually disinflating for more than a year, but the transactional volume is basically superseding the price disinflation. Hence, you’re still getting this boom in manufacturing overall.

Tony Nash

Okay. Based on your thesis, so in ’22 and the first half of ’23, we saw manufacturers and services firms able to grow their margins because of the inflationary tailwinds. They could add margin, they had their top line growing, they had their bottom line growing. And they didn’t really care about the volume of transactions in many companies because they were still hitting top and bottom line numbers that were better year on year. Now you’re saying that because of disinflation, that margin is collapsing and those volume of transactions matter as much or more than the price itself.

Seth Golden

Right. Yeah, that’s a great way to summarize it because when you have this volume, you get this a reading in the total manufacturing layout. But it’s in sharp contrast to what we’ve seen in ISE because there’s no price situation that is ever really good for the respondents. Take, for example, we had an inflation boom. We got the ISM up to 60. It was there for what? One month before it collapsed? Because the respondents know this can’t last forever. I can’t push my cost onto the end producer and then the consumer. I’m going to start responding negatively because I know there’s an inevitability in this inflationary boom. Well, okay. Then the reading starts coming down. There wasn’t even in inflation times, that’s only going to live for so long. Then you get into disinflationary situation. Again, will prices keep coming down? Now, my profit margins, as you are alluding to, are also coming down. I’ve got to rely on volume, but how do I increase demand? The number one problem for a CEO, every single morning he’s always thinking about, I wake up every morning, I’ve got to figure out how to increase demand. So these ISM readings, they’re so sentimental and it’s always focused on price.

Seth Golden

One way or the other, price is bad always. So the note model does a great job of distinguishing the true strength and what the trend is in manufacturing, overall.

Tony Nash

Okay. Albert, I want to bring you in here in just a minute, but I have just a couple more things with Seth that I want to put on through. Okay, so we’ve gone from a very low interest rate to a significant interest rate rise over the past year. We’ve gone from very nice margins on marginally lower transaction volume to thinner margins on transaction volumes that may or may not be increasing. When we take those two worlds and we look at the valuations that companies have had, we had really nice valuations in a low interest rate environment with high margins. Now we’re in a higher interest in the environment, and I assume a higher for longer environment where we have lower margins and the transactions may or may not be increasing. What happens to valuations under your hypothesis, what happens to equity valuations in general? Without talking about specific sectors, but what happens in general?

Seth Golden

All right, yeah, if we just use the benchmark S&P 500, the consensus is that valuation should compress level. So far as the margins are concerned, there’s a bit more nuance there because while the actual margins per sale may indeed decline, the total profitability may not follow suit or the earnings per share may not follow suit because we have this dynamic of higher rates where part cash, be it households or corporations, is earning millions upon millions and billions every single month. So you have this free cash flow that also has to work itself way into the valuation model. Again, the consensus belief is that higher rates, higher for longer, should compress the earnings multiple. When in reality, that has been the exact opposite. If we go back to, let’s say, 1960s, 1970s, all the way up to the early 1990s, the S&P 500’s multiple was actually higher over a good 23-year span. I think it was 17.7 times from the late ’70s to the 1990s in that higher rate environment than even where we are today after the Federal Reserves program here. And now we’re at 17.4. But of course, we won’t know where we’ll be going forward.

Seth Golden

But there’s not hard and fast data suggesting that the multiple should compress because we’re not even where we were back in the ’70s or ’80s when it comes to the federal funds rate, let alone, let’s say, the benchmark 10-year Treasury yield. I don’t fall into the camp that aligns with a compressed multiple. If you look at the PE multiple, if you look at the CAPE ratio, they do nothing but expand over time. That’s the history of multiples. They expand over time, mostly because for every dollar that goes toward wages or whatnot, we get that much more productivity, so we have that much more cash flow. With that being said, the common pushback is no multiples don’t look at the peak. We still haven’t made it back to the peak of the dot com period. Okay, so fine, X dot com, that hyperbolic event or parabolic event, multiples indeed expand over time. So who’s to say that we are not in that new period, this post-pandemic period, where we once again jump the shark? Because there’s always this jump the shark moment when it comes to PE expansion. In real time, we shun it, we belittle it, we berate the multiple expansion.

Seth Golden

It’s only in hindsight that we realize, Oh, we just took a leap.

Seth Golden

That’s how I look at it secondarily, I say, if you look at the long term history of yields, they go lower over time. We might be in this vacuum moment where we’re becoming prisoners of the moment given the monetary policy initiatives. But in hindsight, again, we look back and we say, well, of course, the 10-year yield is lower over time. It’s just a matter of when it finds that new lower, low bound territory. So I’m comfortable with saying… And if, in fact, we finish at a 20-time multiple here this calendar year over the trailing five-year period, the S&P 500 forward PE multiple will have averaged 20 times for the first time in history, hence the jump the shark moment.

Tony Nash

Very interesting. All very sophisticated. Thank you so much for this. Albert, I know you are not well. I suspect you were not in line with the disinflationary underpinning of Seth’s hypothesis. Can you walk us through that?

Albert Marko

Yeah, Nope.

Seth Golden

I’ve been wrong twice before. No, I’m on you.

Albert Marko

I don’t even want to discuss this inflation until wage inflation is under control, and that is nowhere near getting control at the moment. On top of that, inflation in the last year and a half has only shown that companies can earn more. Put earnings through the roof. Until I see wage inflation actually coming down, I don’t want to talk about this inflation, to be honest with you. I can’t see it. Even the CPI prints have been completely nonsensical. Goods are just still 17%-20% higher than they were pre-COVID. Energy, as much as they want to push it down, energy is just bursting at the seams to go back to 100 on the Brent. I can’t see a pathway for disinflation. But of course, I’m only talking for the next 6-12 months after that. That’s just a different era, in my opinion.

AI

Heads up for a short break.

AI

Are you using the potential of AI in your portfolio management strategies? With an impressive 94.7and 10.7% forecast accuracy on average, you can confidently integrate AI into your approach with CI Markets. Visualize the potential volatility of your portfolio over the next 12 months and gain insights into specific assets that might experience fluctuations. This empowers you to make informed decisions on when to buy, sell, or hold. CI Markets covers a wide range of over 1,600 assets, including stocks, commodities, forex, indices, and economic indicators. Imagine running limitless portfolio scenarios to optimize your gains. Curious about the outcome of removing or adding certain assets? Wondering how your portfolio might evolve in the next 3, 6, or 12 months? CI Markets equips you with answers to these crucial questions. Whether you seek a streamlined portfolio analysis, wish to explore diverse scenarios, or aspire to track your investments with precision, CI Markets is the ultimate tool for you. Ready to learn more? Visit us at completeintel.com/markets.

AI

Thank you and now back to the show.

Tony Nash

Seth, do you have a timeline on yours? Are you thinking ’24? What are your thoughts on the timeline?

Seth Golden

So far as getting to the Fed’s target?

Tony Nash

No, getting to this disinflationary environment that you’re talking about.

Seth Golden

Philosophically, obviously, Albert and I disagree. I understand where… He’s absolutely right. We have absolute inflation. That’s all we actually ever have. But in terms of what’s being measured by CPI, PCE and PPI, consumer price index and producer price index, they measure rate of change. So it’s the month of the month or year over year. So philosophically, I think we agree on the fact that there’s always inflation, but it’s a matter of what’s being measured is the rate of change of that inflation. So do I see that deceleration continuing? Yeah, I would suggest I see that disinflation or deceleration in the inflation rate continuing through the end of this year and at least for the better part of 2024. And so far as the wage inflation is concerned, we are starting to see an increase in the labor participation rate, which will facilitate some of that, at least to some degree, that deceleration in wages. This morning’s report may be a prime example, or the last two monthly reports, in fact, might be a prime example of an increase in the labor participation rate, working in favor of reducing that overall wage inflation.

Tony Nash

Right.

Albert Marko

Yeah, I just don’t take those numbers at face value. I’m just over the fact that CPI is at whatever, 3.3%. They’ve changed the weighting of it. They use the BLS deflators to manipulate the numbers on unemployment. The revisions come in every 3-6 months later that shows that it was actually worse than they were reporting. Like I said, until wage inflation, in my opinion, gets sorted out and they actually have political policies to address the oil and gas and energy markets, I don’t want to even discuss this inflation in my opinion.

Tony Nash

Interesting. Seth, I do think that your thoughts about the volume of manufacturing will be very interesting. I’m really intrigued by the disinflationary underpinning of it and how that could drive things. I think that’s very, very interesting. Definitely not a consensus view right now.

Albert Marko

If you get disinflation, like he’s saying, six months later, we’re just going to have another inflationary event because people are going to go out and buy everything. I mean, houses, goods.

Seth Golden

Yeah, I agree. One of the caveats or antithesis that I put into my models does center on the resilience of the consumer, the strengthening the labor market being what it is. And just the monthly, and I think it gets just way overlooked in terms of people that have been calling for a session since last year. The Fed is actually stimulating while it’s trying to ease the economic situation by tightening. We’re not as rate-sensitive as we used to be. Probably the least rate-sensitive economy as a whole, households and corporations in history. You have all these people that have fixed rate mortgages at three and four %, so the Fed raises to 550 basis points. What do they care? It’s not really affecting them to any monthly bill payment degree. Now they take that, their savings and they put it into a money market fund for 5 and 6% of monthly income coming. The Fed is tightening while these people are actually seeing the benefits of the tightening cycle. Unless you say, Well, the service industry, that’s where the real inflation is. I would totally agree. You go to any restaurant. You go to even some of the lesser Darden Restaurants like an olive garden, you can’t get a chicken parmigiana for less than $25.

Seth Golden

Your boy likes chicken parmigiana. I’m trying to feed a family of four out at the olive garden for dinner, and you get a bill for 150 bucks and you’re like, Whoa. I’m the consumer spending.

Tracy Shuchart

You also can’t forget what the government is doing, right? Fiscal policy is doing. I mean, the IRA act, which is very inflationary, for me. It’s butting heads. I just don’t see disinflation either at any point soon, except for maybe what the Fed is looking at in their core. But it’s hard for me to get on board with this disinflation theory.

Albert Marko

For me, it’s like a double-edged. Everything that Seth says is most likely correct. But the flip side is there’s double-edged swords everywhere. If you have disinflation, let’s say housing starts coming down or they have rate hikes coming down, mortgage is coming down.

Albert Marko

You have such low inventory of homes in certain states that they get snapped up like this because people are just cash rich at the moment. They sold whatever they did or their stock market. They’ve had calls on NVIDIA, made them 10 million bucks, and they come back and they start buying things cash. So you’re right. They don’t care about rates at all. They don’t care about it.

Tony Nash

I was talking to Morgan’s broker earlier this week, and I said, How is your business doing? Has it slowed down? And they said, Oh, yeah, a lot. It’s slowed down a lot. But they said, Most of the buyers that we’re seeing are cash buyers. So what you’re saying, Albert, is right, is people are not taking out a mortgage. They’re using their cash to buy a home. Has the volume declined? Yeah, it has. But I think that what the Fed has done with interest rates is working because you have these guys with two and three and four Airbnb’s who are not seeing the occupancy that they saw a year or two years ago. Because of the higher mortgage rates, those houses are eventually going to have to come on the market because it can’t service those mortgages. Those will come on at a lower rate. Will they get stopped up for cash? Maybe they will. Maybe they’ll stay on the market for a while longer. But I do think that the game that the Fed is playing is a medium term game, and it’s slow to get to where it’s going. So I don’t want Seth to feel like he’s being hanged up on it. I’m actually –

Seth Golden

Oh, no. No, no. I always do. I’m fine with the constraint.

Albert Marko

It’s good to test your theories on the other side. It’s not important to have that.

Tony Nash

I think one day in ’24, we could wake up, and the disinflationary part of our hypothesis could be very true. It could be or Feb, sorry, April, May, something like that. We got the the boob in this this disinflationary and people are just like, Wow, we’ve got high rates, but we’ve got my olive garden dinner is now 15 bucks instead of 25 bucks. Maybe that happens, right?

Albert Marko

I think that Seth is right. I just don’t know about the timing. I don’t buy it for the next six months for sure. On the next 12 months, 50-50. 18-24 months, absolutely. That’s-

Tony Nash

50-50, so that’s a win. Take the win.

Albert Marko

Because it’s an election year, right? It’s an election year, and political policies always want to be… They’re always inflationary. Food, corn, energy, all that stuff, and then mixing them up.

Seth Golden

No president has been reelected when there’s been a recession.

Tracy Shuchart

A recession, exactly.

Albert Marko

Yeah.

Tracy Shuchart

So they gonna do everything they can to halt that recession.

Tony Nash

Interesting. Tracy, I want to bring you on on this… While on some of this first topic. You had a great tweet about US manufacturing, rebound stretching diesel supplies and pushing up diesel prices. With Cess Hypothesis about the manufacturing volume coming back, which is great, how much of an impact do you think diesel prices will have on overall inflation readings? Is that a big driver of inflation in the US?

Tracy Shuchart

Well, I think that diesel runs the economy, period, end of story. It has everything to do with manufacturing, transportation, with agriculture. It is at the heart of what makes the economy go around, essentially. If you want to move anything anywhere, if you want to produce anything, you’re going to need diesel. Of course, that’s going to make a big impact on inflation. That said, that energy is not part of what the Fed looks at conveniently. That may not figure into their metric when they’re looking at for inflation, so to speak. But does that impact the consumer? Absolutely, that impacts the consumer because those costs are obviously passed on to the consumer.

Tony Nash

Yeah, there are secondary tertiary impacts, of course, that are passed on to consumers or that service industry people need higher wages, gas prices are higher and so on. Last night here in Houston, I noticed our gas prices were under $3 for the first time in a long time.

Seth Golden

Here in Florida, well, north where we are as of last week, $2.99, at one of the local stations.

Tony Nash

Yeah. If you’re on the Coast, I’m sorry, guys, but…

Tracy Shuchart

I’m like, Sir, our gas is not there yet, but it has come down, obviously. But we’re not really having a gasoline issue so much as a distillate issue, and people have to seem to separate those two because it’s it’s not doesn’t run the economy, Distillates.

Tony Nash

You’re right.

AI

Heads up for a short break.

AI

The fast-paced world of investments, staying informed is the key to success. Introducing CI Markets Free, your source for AI-powered forecasts. With our free version, you get access to powerful tools that help you make informed decisions. Join a community of savvy investors. Analyze market trends. Your investments strategically, stay ahead with monthly forecasts, compare assets effortlessly, and download data for your analysis. Don’t just take our word for it. Our users love the valuable insights CI Markets provides. Get started today with CI Markets. No credit card required. CI markets, your source for AI-powered forecasts.

AI

Thank you. And back to the show.

Tony Nash

Let’s look at those fuel stocks. You sent me a chart from Morgan Stanley and the EIA looking at fuel stocks in the US. They look to be at definitely lows within a a five-year range for ’23. That’s the dark blue line on the chart. Can you talk us through, since we do have low stocks, if we see this rise in the volume of manufacturing in the US, would it be almost this bullwhip-y rise in diesel prices because of that surge in demand?

Tracy Shuchart

Absolutely. Obviously, you’re going to see knock-on effects of that. Even though we’ve seen prices come come back, just had Russia this morning decide they’re going to allow diesel pipeline exports. That’s not all of their diesel prices. Remember, on the 21st, they said that we are stopping all gasoline and diesel exports, which really affects Europe more than anything. But they did come out this morning and say they are going to allow pipeline diesel exports, but still no gasoline gasoline That did alleviate some of the pressure across global markets. You saw some of those fuel prices come down, those diesel fuel prices come down globally. But that said, there’s still a global crunch. If we look at countries that are reporting, reporting, so OPEC countries, for example, because because they’re The US reporting is the best, but they’re next. If we’re looking at what they’re selling, their light sweet barrels will take Nigeria, for example. Their light sweet barrels are not really selling. There’s a lot of pressure on on light right now because all you can make from that is gasoline, essentially. But if you look at their heavier barrels right now in countries that produce crude oil that can be cracked into diesel fuel, those are selling for $8 or $9 above Brett prices right now.

Tony Nash

Russian are the selling you $9 above Brett.

Tracy Shuchart

No, not Russian. Other countries, because Russia obviously has a price cap, et cetera, but they are selling for it about $85 for their heavier crude distillates. But Russia is a totally different story because of the price caps and things of that nature, because they’ve had a very large discount to Brett. But I’m talking about other OPEC countries that are selling. In fact, we just had Saudi Arabia come out this week and they’re selling OSP, which is their official selling price is above above brand. Selling that across Europe and Asia and to the US.

Tony Nash

Yes. That is a perfect segue into our next subject, which is tumbling crude prices. As you were just talking about, as we’ve talked about for several weeks, our most visible discussion about this was crude not hitting $100. That was about a month ago. We’ve seen seen crude fall ten this week, I’ve got the light, sweet futures on the screen. In addition to what you were just saying, can you tell us what’s happening and how far do you expect it to go?

Tracy Shuchart

Well, I think it’s because we had such an initial… Every reaction creates an equal and opposite reaction. We had that that kick to almost $100 on Brent, $95 on WTI. That was just a major… That was a major chase push-up, CTA following people got on the trade, etc, etc, and then it’s a momentum. It’s a Mo-mo trade, right? When you have CTA traders, they tend to jump on any momentum no matter what product that is. That pushed prices to what levels that were where they really probably shouldn’t have have been? I mean, don’t need to be that high. High. That’s terrible. When we saw prices push up to $95, that is terrible for refiners. We saw margins collapse. You knew immediately these prices were too high and that we would have to see oil prices come down again because it was just awful for the industry in general. It’s horrible on emerging markets, especially with the dollar pushing up and you have dollar-denominated debt and then you have the pressure of oil prices being high. It’s a terrible scenario. It’s not surprising that we have seen a pullback. Has this pullback been more exaggerated than it likely should have been?

Tracy Shuchart

Probably. But I think what we really need is stability in oil prices because what happens is when you have this volatility in oil prices, this does not encourage producers to go out and spend money on new wells and new production, etc, where they’re all going to hold up. In the end, then this is going to hurt us in the long term because they’re going to be like, Oil prices are too volatile. We’re not going to invest. We’re not going to invest in new production right now. We just can’t. We don’t know what our oil prices will be tomorrow. In the long run, this adds to the theory that there’s higher oil prices for later because we’re going to see demand increase regardless if we see demand decrease in the we’re still seeing demand increasing in, in, again, emerging markets, Asia in particular. I think right right what we really need is some stability in oil prices. That encourages producers to at least start producing a little more to keep up with with so it’s not becomes crushing later on.

Tony Nash

Okay. How do we go and what is that stability oil price? Because I don’t think those two numbers are the same.

Tracy Shuchart

Well, I think $80, $90 range for right now is great. I think OPEC would be thrilled with that.

Seth Golden

That’s what I’ve been saying, OPEC, I think that’s-.

Tracy Shuchart

Would be thrilled with that. How low does it go right now? I don’t know how long. We’ve seen this drastic sell-off reside over the last couple of days. We’ve seen oil prices here stabilizing a bit today and yesterday, even though we had a little bit more of a a I don’t know. I think if you’re looking at $79, I would be a long-term buyer there for swing higher.

Tony Nash

Higher. I thought it was drilling.

Tracy Shuchart

I’m not saying that it can’t. Here is not a bad level either. I think the way… The oil markets are telling you that because the oil markets have stabilized again over the last couple of days. Yeah, we’re moving sideways over the last couple of days, but that drastic sell-off is over. I think people are done.

Tony Nash

So, OPEC’s happy where we we are mid 80’s. Low to mid 80’s. Dollar is happy where we are, 106. Is the world happy with where the dollar is? No.

Albert Marko

No.

Seth Golden

I mean

Tracy Shuchart

I’ll leave the dollar up to Albert.

Albert Marko

I would love to see oil go back down to 75-77.

Seth Golden

That’s my call. I think if I were a step aside long enough to get it down there.

Albert Marko

Yeah. I just don’t buy into these… I mean, last week we were talking to a couple of guys, and everyone last week was like, 120 coming, 150 coming. I don’t buy into these extreme moves, especially when you have OPEC and the Fed playing all these games. They’re not stupid. Saudis don’t want it over 100. The US doesn’t want it under 65. So you pick a range 75-90, 95. We’ve been talking about that for how long, Tracy? A month. A year almost. That’s such a nice sweet spot for everybody. They can do whatever they want with their CPI prints of crushing it down to 75. They’ll make the Saudis happy at 90, ping-pong back and forth. I just see sitting there for quite a long time, to be honest with you.

Tony Nash

That’s good. We need that. We need some stability, right? Some –

Tracy Shuchart

Absolutely.

Albert Marko

It’s crazy, though, because you look at these 6% drops the other day.

Tracy Shuchart

It’s ridiculous.

Albert Marko

What is that? Bitcoin? Is that what we are now? Oil is the Bitcoin market? Yeah, 6, 7% drop is insane.

Tracy Shuchart

You need stability in the oil market. I think think if you’re looking at oil equities in particular, if you’re trading those, that’s what you need to see. You don’t need to see this this volatility, does not help investors and it does not help producers.

Albert Marko

It doesn’t even help the shipping. By the time you ship something two months later, you can have a drastic swing of like $15. That’s way over my head, but I’ve heard complaints where traders had to hedge because they have ships out to sea.

Tracy Shuchart

Oh, absolutely.

Tony Nash

Yup.

Seth Golden

Think of OPEC just like the Fed. OPEC with these announcements that made more frequently this year than I can recall in the more recent past. It’s helped to create, I should say, volatility in the energy market in the same way that the Fed. With their ongoing, every day of every week post an FOMC meeting, we just get these wild swings in the equity markets. It’s realized volatility in the equity markets, not so much in the VIX, which is implied. But that’s how we’ve had these 6% positive swings include in in and then you get the adverse effect as well, mean reversion. But both of these entities with their press conferences and their press releases here and there and interviews with Saudi members and what have you, it’s helping to sustain the volatility that really does not need to be there and is not productive.

Tony Nash

And not helpful for for consumers, Right. People freak out about oil for a few few or gasoline prices, petrol prices for a few weeks, and then they’re relieved. And then they freak out and then they’re relieved. And it’s just uncertainty at the consumer level. Okay, so good. Thanks, guys. So let’s change the topic to a completely ridiculous one, which is a clown show that we call Washington, D. C. We’re going to talk about DC drama and markets. We’ve seen a lot of drama drama in this week. Us politics just doesn’t seem to make sense to foreigners, really. But Americans are in the middle of this. Government closures, House leadership contests, all this stuff. We care, but we don’t care. I could be wrong on on that, I think with every day, we’re just washed over with this news. I don’t know that it really makes that much emotional sense to us anymore. Can you tell us why the Speaker of the House is such an important role in Congress. Let’s dig into that a little bit. Also, where is the American mind on this? Because we have some people from overseas who watch watch and they’re hearing that this this the first speaker of the House that was let go outside of an election in 150 years or something.

Tony Nash

I don’t know. But I don’t know that most Americans really care all that much because of the drama that’s coming out of DC every day.

Albert Marko

Yeah. I mean, McCarthy was hated from both sides. It took him like two dozen votes to get elected to the speaker the first time around. It was a deal between seven or eight GOP members with McCarthy saying, do this, otherwise we’re going to vacate you. And McCarthy thought, and actually a lot of the congressional members that I talked to thought that he was going to be able to survive this. And last week, I’m a senator for shutdown because I didn’t think think would be that dumb to work with the Democrats and face vacation. And so all his famous tweet, bring it on, they brought it and he’s gone and not going to run again. And this is is worse than a shutdown, in my opinion, because now we have a contentious speakership of between three individuals, Scalise, which is basically McCarthy 2.0, Tom Emer, I’m not a big fan of him and his ridiculous Bitcoin antics. I don’t even know who else would be.

Seth Golden

Jordan.

Albert Marko

Jordan is not going to make it. He’s not going to make it. I would probably say Scalise or Emer are the top two guys.

Tony Nash

You know who is? I pay attention to this stuff.

Albert Marko

Yeah. I would say it’s problematic because the speaker is used as the mechanism to bring floor votes to whip up the majority, find the the and pass bills. We have eight appropriate… Well, seven Appropriations bills that need to get get passed. One has to be reworked all before 40 days comes up and a new shutdown deadline looms. The house is not even in session for another week. Take 10 days of that out of the way. You have 30 days to somehow get get bill that funds the government through. Like I said, this is so much worse than a shutdown at the moment. I would rather have a week’s shutdown and some compromise has been found and then get back to the the table get back to work, rather than now we have a speakership race between three monkeys that really shouldn’t even be there in the speakership saying ridiculous things and throwing out Trump’s name left and right. This is just an absurd clown show that we’re having at the moment.

Tony Nash

Is it feasible that Trump becomes a speaker? Yes or no?

Albert Marko

Absolutely not. I don’t want to even hear that stupid.

Tracy Shuchart

I wanted to add that, Tony.

Tony Nash

Tony. Sorry, sorry.

Seth Golden

I think you are potting, Albert,

Tracy Shuchart

The Twitter for the last two days have been like…

Albert Marko

You guys are just trying to give me a heart attack. That’s the color of that.

Tony Nash

I have a question about it.

Albert Marko

Trump has no chance to be a speaker nor should he even be a speaker. He doesn’t know anything about the mechanism about being a speaker. It would be nothing more than a campaign ad for the next seven months.

Albert Marko

This is a stupid idea put on by stupid griifters that we were trying to get into Trump’s favor for the 2024 election. That’s all it is.

Tony Nash

I was just talking about this yesterday with somebody in Asia. Americans see someone like Dianne Feinstein who made made salary for whatever, 35 years in the Senate, but passed away with $110 million estate. That is, I think, a perfect example of how Americans view people in Congress, House or Senate, and how they go to Congress as relatively normal people and then emerge these multi-multi-millionaires. So the frustration —

Seth Golden

It looks extortionist.

Tony Nash

Exactly.

Albert Marko

Don’t vote him in.

Seth Golden

They’re extortionists. Well, any time —.

Albert Marko

If you have a problem about your congressional member making $10 million every five years, don’t vote vote in. I don’t understand what the people are talking.

Tony Nash

My congressional member is Dan Crenshaw.

Seth Golden

What are we going to do about MTVs rock to vote then?

Tony Nash

Right. My congressional member —.

Albert Marko

Dan Crenshaw is a moron.

Tony Nash

I complain about that.

Albert Marko

Dan Crenshaw is nothing more than a corporate chill. He’s a corporate chill.

Tony Nash

That’s right. I can’t get used to it.

Albert Marko

Don’t vote him in.

Tracy Shuchart

But why do people keep voting these people in? This is what what it all mentions, Nancy.

Tony Nash

Because every election they vote.

Tony Nash

We were doing our civic duty.

Tony Nash

Every election that he says maybe —.

Seth Golden

Every time we get to the conversation of politics, I always go back to the same thing. When was the last two-party system that has succeeded in perpetuity for its population might drop? Because it should be be after that. We get to a certain tipping point, if you will, where the structure of the system just doesn’t work to the benefit of the average person. The other aspect of, and why, in my opinion, it’s become so contentious in the turn of the century is I think if you go back to the great financial financial crisis, were already in the deficit, but that compounded the deficit. And then you get the pandemic. And there’s no win here for politicians. When you have a deficit that is entrenched, what can you really do? You’re really just just a that guy who appeases that guy. It’s all a chain of appeasement at this point because we’re not paying our bills one way or the other at the end of the the day. Come out of this to what? $31, $32, $33 trillion. So it’s who can I appease best and can I amass a certain population of people where I can get elected?

Seth Golden

But then it’s just still about appeasement. And at some point, it just becomes unsatisfactory to the general population. And we’re at the point where there’s no such thing as as on a real continuum. It just doesn’t work.

Albert Marko

Bipartisanship is dead. It’s dead.

Tony Nash

Okay, Albert, given what Seth said, does whoever the speaker is even matter?

Albert Marko

Not really. Not in this day and age. It’s more about groups within each party that are controlling something. I mean, the democrats-

Seth Golden

It’s It’s too much within the parties.

Albert Marko

Yeah. I mean, the Democrats are more unified than the GOP at the moment because it’s the Trump GOP versus the rest of the GOP. They’re simply not unified, nor are they going to be unified.

Tony Nash

But I’ll argue you even have have I don’t believe we have a two-party system. I believe we have parties within parties. He’s going to be able have the party and all that stuff. You even have people like Marjorie Taylor Greene who are at odds with Matt Gaetz or at odds withand and these are all Trump people. So not necessarily two parties. There are are Bolsheviks Menshevik within each party. Sorry for that.

Seth Golden

You get stalemates. You get Mexican standoffs and and in perpetuity, year after year after year.

Albert Marko

I would gladly take stalemates with this clown Congress. Gladly. Because honestly, if you’re a corporation and you’re trying to do a five-year to 10-year outlook, I would rather have stable stalemates than extreme policies on the left and the right every time a new Congress gets elected in.

Seth Golden

You could just take line items out of the budget. You could just take line like they did with the Department of Weight and Measures. When was the last time you saw the Department of Weight and Measures in the congressional budget line items? It just hasn’t existed since 2014. Why hasn’t it existed since 2014? Because Amazon literally pays fines to equate to their entire budget. Just find other companies that will satisfy that as well.

Tony Nash

I had no idea about that, Seth. That’s amazing.

Tracy Shuchart

Me neither. That’s insane.

Tony Nash

Okay, so Albert, What happens? So is this intractable environment, one that actually creates some stability for, say, the private sector?

Albert Marko

No.

Tony Nash

No.

Albert Marko

No. Only because we don’t have normal, logical, economic, fiscal policies in act right now. We have insane things going on at the Fed and the Treasury and out of the White House. So we don’t have anything normal happening. So why would we… We have no chance to fix it. That’s the problem that I’m seeing going forward. We have dumb EPA rules, we have dumb immigration rules, we have dumb foreign policy, we have dumb economic policy. So until we actually have a decent congressional opposition to the White House, nothing’s going to get fixed, nothing’s going to get resolved.

Tony Nash

Does this change before, say, 2030? Is this a generational thing where we’re waiting for baby boomers to-

Seth Golden

I think we have to lower our expectations.

Albert Marko

No, baby boomers are checked out. They’re checked out. They’re cashing out of this market.

Seth Golden

We’re just still going to –

Tracy Shuchart

We need GenX to step up people.

Albert Marko

Boomers are using these market rallies. Boomers are using these market rallies for exit liquidity on the backs of millennials and Gen Z, where the GenX are going to have to step up and run the show for whatever’s left until the Marxist progressives are coming out of college and run things. That’s just the way it is. It’s a cyclical thing. I’m not even complaining about it. It’s It’s a thing. It happens in every society, every government. You have extreme right, extreme left, and then it falls back in the center a decade or two later.

Tony Nash

Okay, so there will be a speaker, right? It will not be done with someone, but we will have a a speaker.

Albert Marko

For sure. Sure. Two weeks.

Tony Nash

That will happen happen –

Albert Marko

Two weeks.

Tony Nash

-two or something, right?

Albert Marko

Yeah.

Tony Nash

Okay. Okay. And person is just really a tool to serve as a traffic light for things to work in the house. That’s all they do.

Albert Marko

That’s right.

Tony Nash

Okay. So once that is in, we have… I like a legislature that can’t do that much. Much. So does that mean when this person is in? Are they full scheme ahead, making legislation that we all can’t stand? Or is it a minimalist legislative body where there’s so much disagreement that very little gets through?

Albert Marko

It depends on who’s running the show. If it’s Jim Jordan, nothing’s going to happen at all whatsoever. If it’s Scalise, it’ll be status quo for what McCarthy was doing. Yeah, we’ll get some stuff done here and there. If it’s Tom Emer, yeah, I think it’s probably a little bit more efficient from the GOP side.

Tony Nash

Okay. Not who do you want to win, but who do you think would be the best to win for the functioning of that legislative body? Is it Tom Emer?

Albert Marko

No, I think it’d be Scalise. As much as I don’t like it, it’s Scalise.

Tony Nash

Okay.

Seth Golden

It’s status quo.

Tony Nash

It’s status quo. Okay.

Tracy Shuchart

Better the devil you know than the devil you don’t know.

Albert Marko

Well, the thing. That’s always the case. With Russia and Putin, the DOD guys say, Oh, we can get rid of him. Well, who’s coming next? You have no idea. I know what Scalise is going to do. I don’t know what Jim Jordan is going to do. God knows what he’s going to do. Do. So just the reality of it.

Tony Nash

Interesting. Such as American politics. Guys, thank you so much for this week. This is great. I appreciate your thoughts. Have a great weekend. Have a great weekend. Thanks, guys.

Albert Marko

Thanks, guys.

Seth Golden

Take care.

AI

That’s it for this week’s episode of The Week Ahead. Please don’t forget to rate us and review on whatever platform you are watching or listening to this. Thank you.