Week of May 25, 2026 — CI Markets Weekly Outlook

Markets ended the week higher, but underlying volatility remains a focal point. Major indices touched fresh highs late in the week, driven largely by cautious optimism surrounding US-Iran negotiations. However, the lack of resolution regarding the Strait of Hormuz and nuclear capabilities continues to cast a long shadow over global supply chains. Beneath the surface, a clear bifurcation is emerging: energy and defensive sectors are demonstrating notable resilience, while certain pockets of technology are cooling. Risk appetite appears intact, but institutional capital is actively repositioning around two accelerating themes: persistent geopolitical supply risks and climbing Treasury yields.

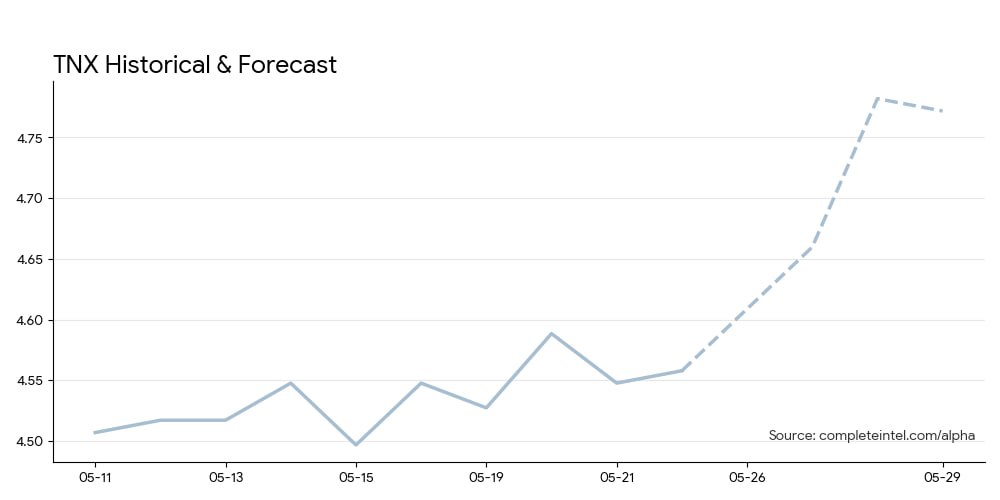

▲ The Rate Reality Check Forecast: 10-Year Treasury Yield (^TNX)

The 10-Year Treasury Yield (^TNX) is set to climb further over the coming week. Yields have steadily risen over the past two weeks, and this momentum is expected to persist as inflation expectations firm and traders anticipate less dovish policy signals from the Federal Reserve. While higher yields typically serve as a headwind for growth stocks, they also signal an underlying confidence in economic resilience. For investors, this dynamic favors sectors equipped to absorb a higher cost of capital. CI Markets is projecting continued upward pressure on rates throughout the week.

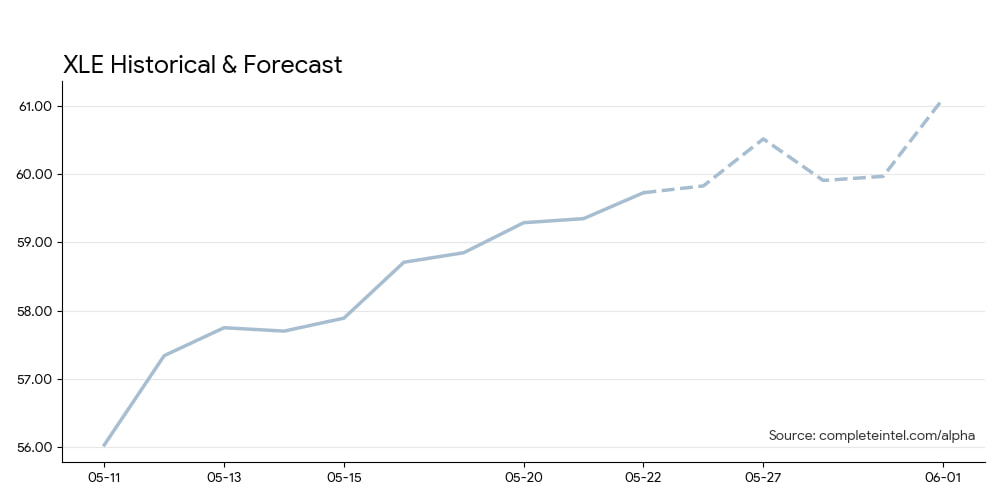

▲ The Supply Risk Premium Forecast: Energy Select Sector (XLE)

The Energy Select Sector (XLE) is positioned to extend its recent strength. The sector remains heavily supported by persistent supply concerns and the tense geopolitical backdrop involving Iran. Even as diplomatic headlines generate short-term optimism, unresolved risks concerning the Strait of Hormuz keep the geopolitical premium elevated. Furthermore, higher Treasury yields validate broader demand expectations, establishing a solid floor under the sector. XLE’s trajectory suggests continued outperformance relative to the broader market, particularly if Middle Eastern tensions escalate.

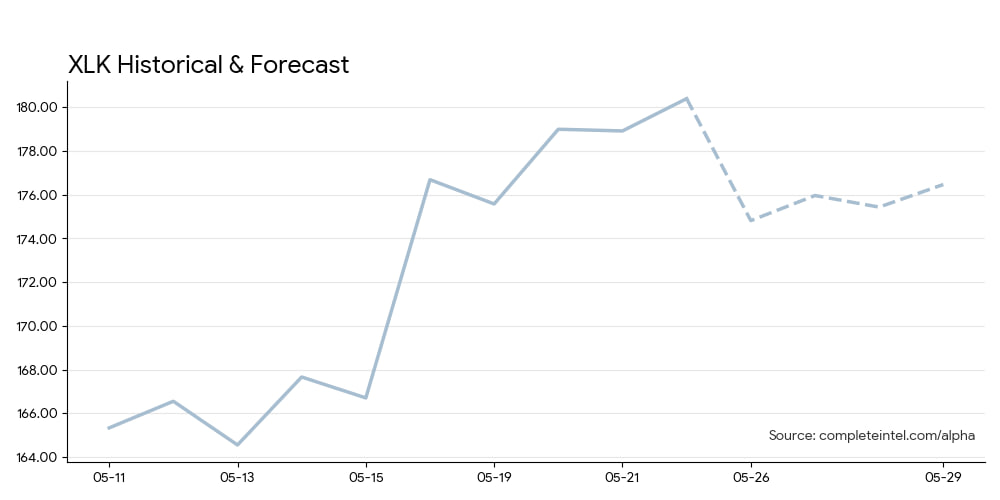

▲ The Valuation Headwind Forecast: Technology Select Sector SPDR Fund (XLK)

/ Sideways The Technology Select Sector (XLK) is forecasting a more challenging environment. While recent market gains have been impressive, surging Treasury yields are acting as a severe headwind for high-growth valuations. The forecast reflects an initial adjustment lower to open the week, followed by a period of choppy, sideways consolidation. Rather than sustaining its previous momentum, the tech sector is expected to struggle as the broader market digests a rising cost of capital. Expect intraday volatility as interest rate pressures and sector rotation vie for dominance. Wildcard Event: Any breakdown in US-Iran talks or physical escalation around the Strait of Hormuz would likely drive energy prices sharply higher and boost defensive sectors, while placing immediate, severe pressure on risk assets.

Conclusion

Subscribe to CI Markets PREMIUM — $24.95/mo

No contract. Cancel anytime.

The content presented in this note is for informational purposes only and should not be construed as investment, financial, or trading advice. This analysis is generated from the output of Complete Intelligence’s proprietary artificial intelligence platform and does not constitute a personal recommendation. You should not base any investment decision solely on this material. Please consult with a qualified financial professional before making any investment decisions. Complete Intelligence is not liable for any actions taken based on information provided herein.