Beyond the Static Spreadsheet: Why Modern Corporate Finance Demands Advanced AI Forecasting Software for Business

Key Takeaways

- Traditional, spreadsheet-based financial modeling cannot keep pace with modern market volatility and non-linear cost structures.

- Implementing specialized AI forecasting software for business transforms financial planning from a reactive monthly cycle into a continuous intelligence layer.

- High-fidelity forecasting requires clean, real-time data inputs, making continuous audit automation a prerequisite for accurate predictive modeling.

- Deploying predictive tools through a parallel path strategy allows corporate finance teams to validate algorithmic accuracy without disrupting ongoing operations.

Introduction

For the modern corporate finance executive, the pressure to deliver accurate, forward-looking guidance has never been more intense. Organizations operate in an environment defined by rapid macroeconomic shifts, complex supply chains, and unprecedented data volumes. Despite these structural changes, many finance departments continue to rely on the same planning mechanisms that were designed decades ago. The reliance on manual data entry, historic averages, and isolated spreadsheets introduces material risk into the capital allocation process.

To bridge this operational gap, leadership teams are increasingly evaluating specialized AI forecasting software for business to establish objective, data-driven baselines. At Complete Intelligence, we have AI tools designed to modernize these legacy workflows and replace guesswork with mathematical precision. However, adopting predictive technology involves more than simply installing a new software layer. It requires a fundamental rethinking of how corporate finance balances foresight with data integrity. This comprehensive analysis explores the strategic transition from static reporting to continuous intelligence, detailing how modern enterprises use advanced software to reclaim analytical focus.

Why the Problem Matters

The failure of traditional forecasting is not merely an administrative inconvenience. It is a core systemic risk that directly impacts corporate profitability, cash flow stability, and market valuation. When a business relies on inaccurate financial projections, the downstream effects damage every department across the enterprise.

In a volatile economic climate, cost structures are rarely linear. Variable expenses, shifting vendor agreements, fluctuating raw material prices, and evolving regulatory frameworks mean that past performance is no longer an accurate indicator of future outlays. When corporate forecasting fails to capture these non-linear shifts, organizations face unexpected margin compression. By the time a variance is identified during the standard month-end close review, the financial quarter is often already compromised.

Furthermore, capital allocation decisions depend entirely on the reliability of the corporate forecast. If a treasury or FP&A team overestimates revenue or underestimates capital expenditure due to a flawed model, the company may misallocate funds, delay critical infrastructure investments, or find itself facing unexpected liquidity constraints. In high-stakes corporate environments, a variance of even a few percentage points can mean the difference between a successful fiscal year and a missed earnings target.

Finally, the problem extends to internal accountability. When forecasts are consistently inaccurate, business unit leaders lose faith in the corporate baseline. This leads to fragmented planning, where individual departments build their own informal shadow models in Excel. The organization loses its single source of truth, creating a siloed environment where leaders spend more time debating the validity of the data than executing strategic corporate objectives.

How Finance Teams Currently Operate

To understand why advanced forecasting tools are necessary, it is useful to critique the current state of financial planning and analysis. In the vast majority of mid-market and enterprise organizations, the annual budget process begins months before the fiscal year starts. This exercise requires a massive coordination of human effort, where department managers submit their projected expenses and revenue targets into centralized templates.

This legacy workflow suffers from three primary structural defects:

1. Dependence on Univariate Extrapolation

Most legacy software and spreadsheet models rely on simple algorithms such as moving averages or basic linear trends. These are univariate methodologies, meaning they look at the historical performance of a single budget line in isolation. For example, a model might look at historical logistics costs over the past three years and project a forward trend based on that data alone. This method is blind to the external economic factors, leads, lags, and indirect relationships that actually dictate logistics expenses, such as fuel price indices or regional labor constraints.

2. The Trap of the “Gamed” Budget

Because manual budgets are built on human inputs, they are naturally exposed to corporate politics and behavioral bias. Department heads frequently engage in sandbagging – deliberately overestimating costs or underestimating revenue targets – to ensure they easily meet their annual performance incentives. Conversely, over-optimistic projections may be submitted to secure project funding from executive leadership. These human interventions alter the data, rendering the final corporate budget an exercise in political negotiation rather than an accurate economic forecast.

3. The Delinked Close and Forecast

In typical finance operations, the accounting close and the forecasting cycle run on completely separate tracks. The accounting team spends the first two weeks of the month reconciling the General Ledger and checking for errors. Once the month is closed, the historical data is passed to the FP&A team, who manually upload the actuals into their planning models to calculate variances. This means that by the time the forecast is updated with real-world information, the data is already several weeks old. The finance team is permanently forced to look in the rearview mirror, reacting to past disruptions rather than preparing for future challenges.

How AI Is Changing the Process

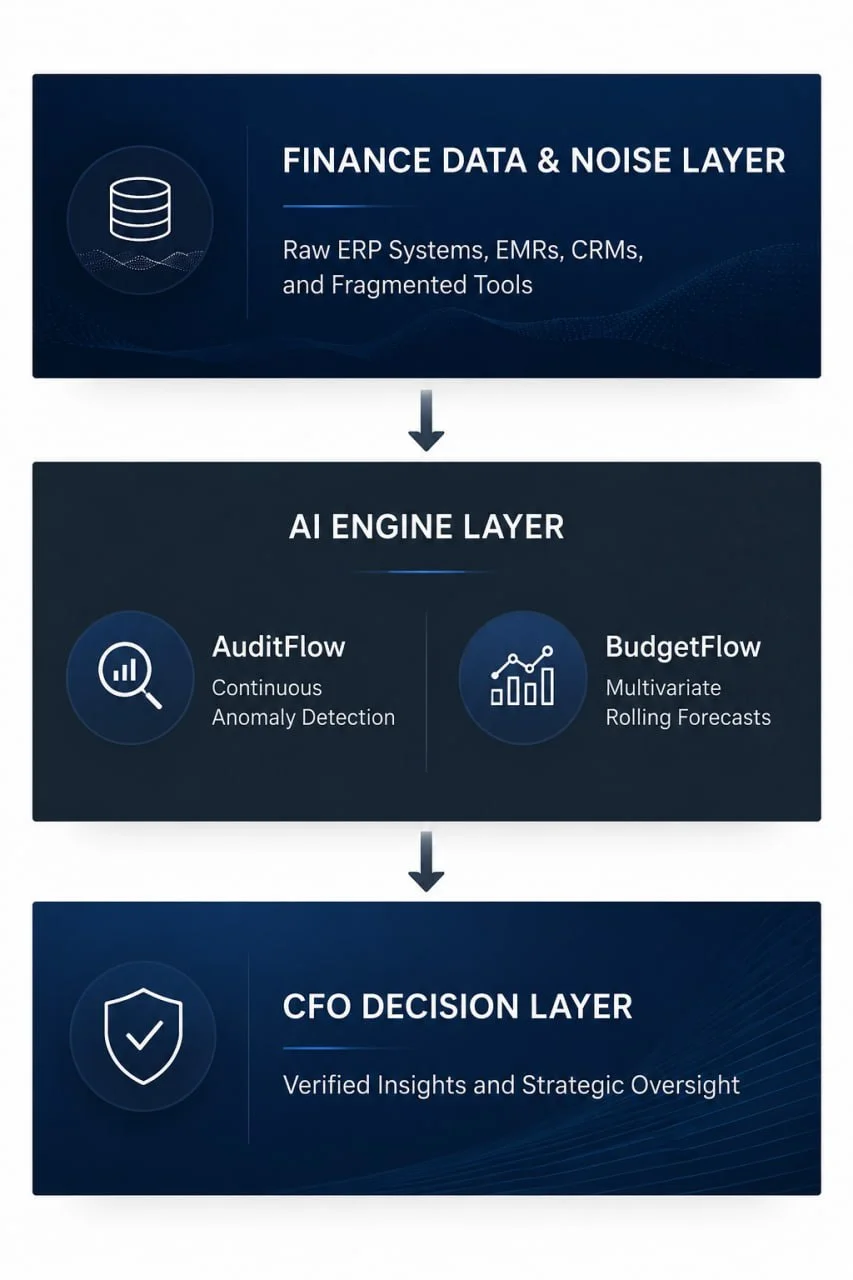

The integration of machine learning and specialized AI engines changes the architectural framework of corporate finance. Instead of forcing teams to manually manipulate linear models, sophisticated AI forecasting software for business introduces automated, multivariate analysis that responds continuously to real-world variables.

This technological evolution occurs across two primary vectors: predictive foresight and automated data governance.

Multivariate Predictive Foresight

Advanced forecasting software removes the constraints of univariate modeling. Instead of looking at a budget line in isolation, machine learning models analyze hundreds of internal and external datasets simultaneously. These systems identify the direct and indirect relationships, leads, lags, and macro correlations that govern corporate financial performance.

For example, when projecting corporate revenues or material outlays, the software integrates internal ERP data with external market signals, currency fluctuations, and consumer demand indices. This creates a highly calibrated, automated baseline that adapts as soon as an underlying leading indicator shifts. Forecasting tools like BudgetFlow utilize these multivariate inputs to replace static planning cycles with dynamic, rolling financial forecasts. This allows the corporate finance team to run complex scenario modeling in minutes rather than weeks, giving executive leadership a clear view of how shifting market conditions will impact future corporate margins.

Continuous Data Governance

A predictive model is only as reliable as the financial data feeding it. If an enterprise feeds inaccurate, misclassified, or incomplete General Ledger data into a machine learning algorithm, the system will generate an equally flawed projection.

To solve this data quality challenge, advanced corporate architecture incorporates automated risk discovery directly into the transactional pipeline. Organizations using AI tools such as AuditFlow can transition from periodic manual sampling to continuous financial anomaly detection. The software scans 100% of financial transactions and ledger relationships in real time, automatically flagging unusual account behavior, missing entries, or potential revenue manipulation. This ensures that the corporate dataset is continuously scrubbed and verified, providing an uncompromised foundation for the predictive forecasting models, a critical capability for continuous intelligence.

What Finance Leaders Should Do Next

Transitioning to an AI-driven financial architecture can seem daunting for finance directors and vice presidents who are responsible for maintaining operational continuity. To deploy these capabilities successfully without risking systemic disruption, leadership teams should adopt a practical, phased approach.

1. Implement a Parallel Path Methodology

Finance leaders should never approach an AI deployment as a risky rip-and-replace operation. The most effective strategy is to run the AI forecasting software for business on a parallel path alongside existing Excel-based workflows. During this phase, the machine learning models generate objective forecasts using historical data, while the traditional team continues their manual inputs. This allows executive leadership to compare the two outputs side by side over a multi-month period. It provides empirical proof of the AI’s accuracy and allows the team to build trust in the algorithmic baselines before making any changes to the primary operational workflow.

2. Establish a Single Source of Truth

To eliminate gamed budgets and internal friction, corporate leadership must establish the AI-generated model as the objective baseline for the entire enterprise. Business unit leaders should no longer submit arbitrary targets. Instead, the software creates the data-driven foundation, and the human managers are tasked with explaining why their operational realities might diverge from that baseline. This flips the budgeting paradigm, shifting the conversation from political negotiation to empirical variance analysis.

3. Transition the Team to Data Quality Engineering

Deploying automated tools requires a conscious shift in human resource allocation. Finance leaders must retrain their analysts to move away from low-value data entry, manual cross-checks, and spreadsheet consolidation. Because the software handles the automated forecasting and transaction scanning, finance professionals must be elevated to data quality engineers and strategic advisors. Their primary role becomes verifying flagged anomalies, calibrating model assumptions against long-term strategy, and providing the executive suite with actionable insights to preserve operating margins.

Ready to Transform Your Financial Forecasting?

Discover how BudgetFlow can help your finance team eliminate manual spreadsheet drag and achieve market-aware predictive accuracy.

Strategic Implications

The deployment of continuous intelligence layers has profound strategic implications for corporate governance, audit readiness, and executive decision-making.

For the Chief Financial Officer and the internal audit team, the combination of predictive modeling and automated testing creates an ironclad corporate governance structure. Traditional compliance frameworks rely on historical look-backs that occur months after an event. By incorporating automated systems, the governance layer becomes an active, preventive shield. When tools like AuditFlow flag an unusual relationship or a transactional deviation, the system generates an audit-ready trail that documents the team’s validation and resolution in real time. This ensures total transparency for external auditors and audit committees, significantly reducing compliance costs and remediation expenses.

From a strategic planning perspective, the use of tools like BudgetFlow alters how companies manage capital cycles. In a standard corporate structure, capital allocation is fixed during the annual budget event. If a market disruption occurs in Q2, the organization is often too slow to reallocate funds because they are locked into static divisional budgets.

Advanced forecasting tools remove this rigid constraint. Because the software provides a continuous, rolling projection responsive to economic indicators, the executive team can adjust capital deployment dynamically. If a leading indicator signals an impending slowdown in a specific business unit, funds can be systematically rerouted to high-growth divisions before the resource is wasted. This structural agility transforms the finance department from a defensive cost center into a primary driver of enterprise value.

Conclusion

The corporate finance workday is becoming denser and more complex, rendering legacy spreadsheets and simple moving averages, as highlighted in our analysis of the productivity paradox obsolete. Relying on linear extrapolations and politically motivated targets leaves organizations highly exposed to margin erosion and operational surprise.

The adoption of specialized AI forecasting software for business provides a path forward, allowing leadership teams to establish a reliable, unbiased baseline for their entire financial operation. By deploying these capabilities as a parallel path, corporate finance leaders can safely transition from periodic, reactive reporting to continuous, intelligent foresight. When sophisticated cost forecasting is paired with continuous anomaly detection, the enterprise eliminates dangerous data blind spots. This dual approach ensures that executive decisions are permanently anchored in financial truth, providing the clarity and agility needed to navigate a volatile global market.

Learn more about Complete Intelligence’s AI-powered finance platform:

- AuditFlow: Continuous Audit for Financial Governance — Automated anomaly detection that accelerates monthly close by up to 7 days and cuts remediation time by 85%

- BudgetFlow: Dynamic Planning with Real-Time Forecasts — AI-powered financial planning and budget allocation with multivariate rolling forecasts

- AI in Corporate Finance: Complete Intelligence Series — In-depth analyses of how AI is transforming financial operations, auditing, and corporate governance

FAQ

How does AI forecasting software for business differ from a standard Excel moving average model?

A standard Excel model typically uses univariate extrapolation, looking only at the historical performance of a single budget line in isolation and assuming a linear progression. Advanced AI software uses multivariate machine learning algorithms, analyzing hundreds of internal and external data points simultaneously to identify complex direct relationships, indirect relationships, leads, lags, and economic correlations.

Why is continuous monitoring necessary for accurate financial forecasting?

A predictive forecasting model is entirely dependent on the quality of its inputs. Continuous monitoring acts as a data governance filter, scanning 100% of transactions in real time to eliminate misclassifications, missing values, and anomalies. This ensures the forecasting engine always builds its projections on a clean, verified financial foundation.

How can our finance team trust the AI model if it operates as a black box?

Trust is built through a parallel path implementation. By running the AI software alongside your existing manual forecasting models for several consecutive periods, leadership can directly compare the accuracy of both outputs against actual results. This empirical validation proves the reliability of the algorithmic baseline before any legacy workflows are altered.

Does adopting advanced forecasting tools mean we have to replace our existing ERP system?

No. Specialized AI engines do not replace your core transactional architecture. Instead, they sit directly on top of your existing data stack, acting as an intelligent bridge that integrates data from your current ERP, CRM, and general ledger subledgers into a unified decision layer.