Access AI-powered markets forecasts for free with CI Markets Free. Sign up here: https://completeintel.com/markets

Welcome to “The Week Ahead” with your host Tony Nash.

1. Bullish economic resilience. Jonny Matthews talks over the resilience of the consumer in the US due to low mortgage rates, potential concerns about a secondary wave of inflation, the impact of rates on corporate debt, and the market’s expectations of rate cuts. Additionally, he highlights the challenges in achieving the Fed’s 2% inflation target and the complexities involved in making adjustments to the target.

2. Fed and inflation targeting. Albert Marko examines the Federal Reserve’s handling of inflation and interest rates, expressing concern about a potential second wave of inflation and skepticism about the market’s expectations of rate cuts. He also touches on the challenges of hitting the 2% inflation target and potential changes in the Fed’s inflation target.

3. Oil (OPEC) and Silver (ready for liftoff?). Tracy Shuchart explores the recent OPEC meeting, and an exploration of the silver market, including supply-demand imbalances, industrial uses of silver, and potential investment opportunities in the sector.

Transcript

Tony Nash

Hi. Everyone. Welcome to the week ahead. I’m Tony Nash. Today, we’re joined by Johnny Matthews. You’d know him on Twitter as super_macro. Also, Albert Marko and Tracy Shuchart. Today, we’re talking about bullish economic resilience. Johnny has got some great charts for us to talk through. We’re also talking about the Fed and inflation targeting. There’s been a little bit happening over the past week on that and Albert will go deep with us there. Then we just had an OPEC meeting, so we’re going to cover OPEC in a little bit of detail. But we’re also going to cover Silver, both of those with Tracy, so we can understand what’s happening in both of those.

Tony Nash

Hi, I’d like to make sure you know that you can access our AI-driven market forecasting tool called CI Markets for free. No strings attached, and it does not require any credit card information. Go to completeintel.com/markets to subscribe. CI Markets is the perfect addition to your analysis toolbox. This free account includes Nikkei stocks, major currency pairs, and global economics. Of course, we have much more in our paid account, but this lets you experience CI Markets before making a financial commitment. CI Markets uses the power of AI to help you make better trading investment decisions. It’s absolutely free. Again, go to completeintel.com/markets to subscribe to CI Markets Free.

Tony Nash

Guys, thanks so much for joining. I really, really appreciate the time you guys take and the thought and work you put into this. It means a lot to everyone watching the show.

Tony Nash

Johnny, thanks for joining us for the first time.

Johnny Matthews

Thank you for inviting me.

Tony Nash

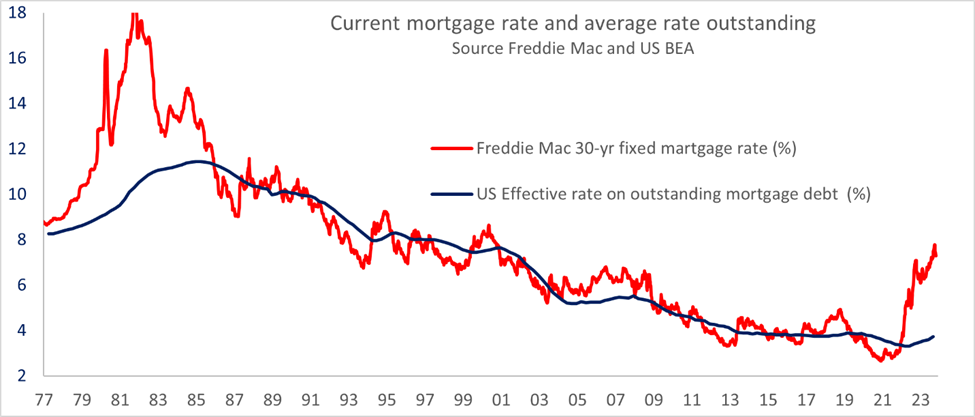

Yes, sir. You have sent across some great charts, and I’m looking forward to digging into them. The first is the 30-year fixed mortgage rate on current mortgage debt outstanding. I hear a lot of people talking about this, and the reasoning seems to be that the Fed rates don’t really matter that much for existing homeowners. The difficulties arise when people buy a new home, whether they’re moving or buying a first home. Can you walk us through this chart and help us what it means, not just for mortgage holders, but the health of the consumer in the US?

Johnny Matthews

Yes. The blue line is the current average rate on the outstanding stock of 30-year mortgages. That is just 3.6%. Although the current mortgage rate for someone that wants to buy a house is something close to seven and a half. It’s come off its highs. People are just not paying that. They’re staying put, they’re not moving house, and they’re paying on average 3.6 % rate. They’re unaffected by these steep increases in interest rates that we’ve had.

Johnny Matthews

In fact, I haven’t got the chart in the pack, but if you look at actual debt servicing obligations of the household sector as a percentage of income, it’s as low as it’s been since the early ’80s outside of the pandemic. I mean, households are really not exposed to these higher interest rates. As far as the consumer is concerned, the consumer is quite well immunized from what the Fed has done. I’m hopeful that that will provide a great deal of resilience for the consumer going forward.

Tony Nash

There seems to be a growing group of people who believe that. We’ve had some guests who started talking about this 9, 10 months ago about the bullish case that you’re talking about. I think, Albert, you’re not quite so convinced. I don’t want to put words in your mouth, but you’re worried about it as a second wave of inflation and additional tightening. Do you still have worries there?

Albert Marko

Yeah, I do. I absolutely do have a worry about the secondary wave of inflation coming just because the Fed is notorious for making mistakes. It’s like I don’t believe any of the CPI data that comes out. One wrong move and we’re back into the four, maybe even fives in the inflation target again. It’s problematic. Obviously, it’s not… I don’t might not happen. They might keep us in the threes for however long in 2024, but it certainly should be a worry.

Tony Nash

Yeah- Go ahead. Sorry, Johnny.

Johnny Matthews

I was going to say I don’t wholly disagree with Albert. Maybe it doesn’t go that high, but I just don’t think the Fed is going to get inflation down to the two % target with what they’ve done so far and with how well immunized the consumer is from these rate hikes. So we’re still…

Johnny Matthews

If you look at the total employment, I know the unemployment rate has gone up, but that’s because more people have entered the workforce. If anything, it’s not like we’re shedding jobs at the moment. You’ve had this tremendous pace of income growth certainly in the first half of the year, tremendous pace of job growth and an enormous pile of wealth that the consumers are sitting on and they are spending it.

Johnny Matthews

We’re seeing the Fed has conquered the easy part of inflation. Energy prices have been falling, used car prices, they’ve been in freefall for almost a year, so durable goods prices, that inflation is down to virtually zero. We’re seeing big, steep declines in headline inflation. But if you look at core and you look at services inflation, I think that’s where the Fed is going to have difficulty in getting it back down to two %. That’s going to provide quite a solid base for inflation going forward.

Johnny Matthews

My concern along the lines of what Albert was saying is that the Fed is going to think that they’ve scored a victory and start easing. Well, certainly that’s what the market thinks at the moment. And if they do start easing too quickly, inflation will get a second wind.

Albert Marko

Imagine them cutting rates early 2024, what the housing market would do. People that were sitting on the sidelines because the rates are too high or start piling back in the real estate.

Johnny Matthews

Well, I think we’ve seen mortgage rates… Sorry, Tony, I was because we’ve seen the mortgage rate drop almost 50 basis points from its peak already, and it’s probably going to come down even further with these declines in treasury yields.

Tony Nash

I know mortgage brokers are really suffering. We’re in Texas, so the real estate market is relatively robust here still, as it is in Florida, of course.

Tracy Shuchart

Just in general, if you look at the recent housing listings, we literally hit the lowest amount of listings on the market in two decades. Even more so then after the financial crisis, when everybody-.

Albert Marko

Yeah, but how much is that due to people just not wanting to leave their 2 or 3% mortgages for seven.

Tony Nash

Yeah, and that’s a supply issue, right? Absolutely. That’ll likely keep prices up because it’s a supply issue.

Tracy Shuchart

Well, you have a supply issue and then you also have a raising mortgage rate issue, in my opinion. Even though we came down to the basis points, you’re still looking at seven % compared to three % or two % whenever you locked your rate in, if you were lucky enough to.

Tony Nash

Yeah, my first house in 2003, I think, or 2002 was seven %. I felt like things were good. I feel old telling those stories, but 7%. I think we could live with it if we had it for a little bit longer. Although the magnitude feels dramatic, but I think it’s doable. We’ve done it in the past.

Tony Nash

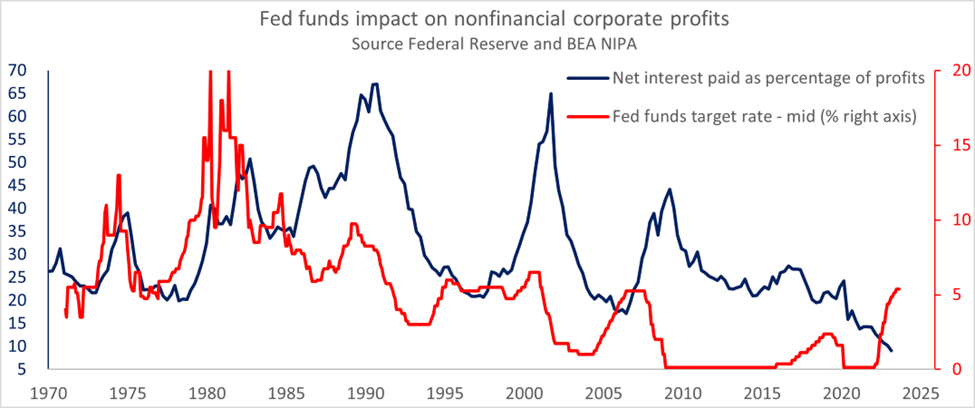

Let’s move from consumer to corporate. Johnny, you said this great chart. It looks like businesses are in good shape as they pay off debt. You’re showing the blue line here is the net interest paid as a percentage of profits, and the red line is the Fed Fund’s target rate. With this, what’s the average maturity of corporate debt? How big of a risk is it to see debt roll over for companies to have to get higher risk? Is this generally long-term debt or is this a combination of long and short-term debt?

Johnny Matthews

Yeah, I think first of all, let me just explain that this is from the NEPA accounts. This is not just S&P companies. We’re talking about the whole economy, basically, all corporates.

Johnny Matthews

You can see in that period during the ’70s and early ’80s when the Fed hiked rates, companies were paying a much higher percentage of interest as a % of profits whenever the Fed pushed rates higher. But then once we had the financial crisis, I think what happened was we had rates that the yield curve was flat as a pancake, rates were on the floor, and companies turned out their debts.

Johnny Matthews

Now, we’re not seeing the distribution here. Obviously, the biggest company with access to capital markets were able to issue bonds and lock in really low rates for very long periods of time like Apple did. They issue 40-year bonds. For the larger companies that have done that, they’re in great shape and they’re the ones that generate most of the profit, which is why you’re seeing this effect here.

Johnny Matthews

We’re seeing net interest as a % of profits is the lowest it’s been in decades. And so the impact of the Fed’s rate hikes on the corporate sector is nowhere near as painful as they used to be. Now. I wasn’t able to get the distribution of maturities of debt. This data covers just all companies of all sizes, and so we don’t have that data available. Some of the investment banks have done a reasonable job of estimating the debt distribution of the S&P companies, but for the most part, the larger companies, this is just not a problem.

Johnny Matthews

Obviously, for the smaller companies and in the high yield sector, they’re really going to have a problem. But we spent a decade listening to people moaning about zombie companies being kept alive by ultra-low rates. Well, now is the time to clear them out. Let’s have a bit of that creative destruction that everybody was missing over the previous decade.

Tony Nash

But you’re right. I mean, interest rates caused this stuff. I think you’re right also that I suspect all the large companies refinanced and issued new debt at zero or whatever for long periods of time. Anybody who didn’t, the CFO should probably be gone. But it is the smaller companies that really don’t have that term luxury who are probably suffering with this?

Johnny Matthews

Yes, I would think so, which is perhaps a little unfair. It does give the biggest companies an advantage and they’re able to grab more market share. But that’s just the way evolution goes in the corporate sector.

Tony Nash

Yeah, the risk of being with the small company is coming back. That’s what your interest rates, there really hasn’t been a cost to risk for a long time because interest rates have been zero or negative, and we’re seeing the cost of risk come back pretty strong.

Tony Nash

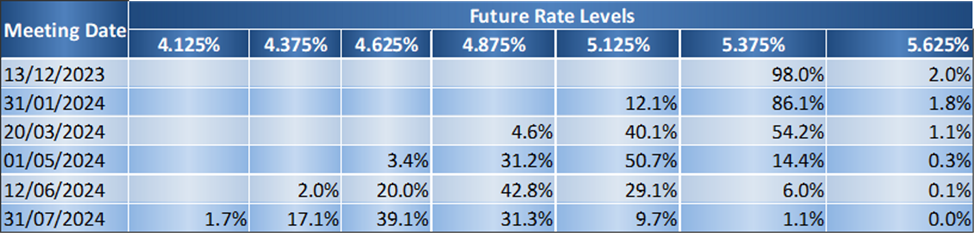

Finally, let’s take a look at rate expectations. This will flow into Albert’s section really well. It seems like there’s an expectation to see rate cut in Q2 of ’24. Of course, that’d be great for some people, but what brings that on? What do you think is in these rate assumptions to bring on these rate cuts?

Albert Marko

Hope and dreams of getting their portfolios up. I mean, a lot of the people that are demanding, not demanding, but vocal about cuts or the guys heavy into the tech sector that love to see us go back to like one %, you know what I mean? Or even zero rates. I mean, Ludacris to talk about. I’ve actually heard some people say that 5% is going to be 1% within by September or whatnot. I think it’s just crazy at this moment. I can’t see the Fed making such an obvious mistake when most of the Fed speakers come out and say, We’re not even talking about it. We’re even thinking about cuts. Why is the market talking about this right now?

Albert Marko

The market has been wrong. That’s what Palo said today, Friday, right? He basically said that. Yeah. Even somebody else that came out there said the same thing. I don’t understand why this Pivot Talk comes up every two months or Pivot and pause right now. Okay, we have a somewhat of a pause. But I still think that we’re probably going to get another rate hike or two. Especially. If core and supercore inflation goes up, starts ticking up, they’re going to have to do it.

Tony Nash

Okay. Jonny-

Johnny Matthews

I think at the moment, these are market implied rates. At the moment, the market is just selectively latching onto every sign of weakness in all the data, like, for example, the manufacturing PMI that we had today from ISM. The new orders were at the second-highest level that it’s been in over a year. That’s a forward-looking indicator of where this ISM index is going. But the market just looked at the low level of the headline index and just pushed, I think, the two-year yields have made a new low for the week. At the moment, the market’s got the bit between its teeth as far as rate cuts are concerned.

Johnny Matthews

Just looking at this chart of rate cut probabilities, by May, the market is saying that there’s only a 15 % chance that rates will be unchanged. And the market is now pricing in over 100 basis points of rate cuts next year, which I think is ambitious. I just don’t think it’s going to happen. Like Albert says, my concern is that we’ve cracked the… We’ve done the easy part of getting inflation down, and this hard part is going to be much more challenging. We may well see a bounce in some of these factors that we’re heading south very, very fast.

Johnny Matthews

Base effects in energy, we’re looking at year-over-year price changes that are… That’s going to change directions soon. As we go into the early months of next year, we’re going to find that energy prices are probably higher than they were a year previously. These effects will start to have an upward impact on inflation, and you’ve still got that high base from services inflation, which hasn’t… I think it was 4% at the last inflation print. Hopes of over 100 basis points of rate cuts next year, I think the market is dreaming.

Tony Nash

Yeah. I mean, with the charts you have the consumer is strong, business is strong. I’m just not like… I’m a little bit puzzled why we’re seeing rates expected to be below five by June. That’s very-.

Tracy Shuchart

The Fed hasn’t changed their mantra. Powell has been very adamant, hired for longer, hasn’t changed, but the market keeps trying to second-guess them. This is not the first time. We had rate cuts actually priced in this year, earlier this year, which were priced out in the market. But if you listen to the Fed, they’re telling you hire for longer. And the markets are thinking they get really excited over any dip in economic data, so to speak.

Albert Marko

But it’s like a double edged sword. I mean, dip in economic data lowers demand. Labor market is going to be affected going forward into an election year. The Fed has been mindful and very vocal about a soft landing. Well, maybe we’ve already had a soft landing. And maybe we’re in the second half of the game here, going into the 2024. It’s like, do we have another soft landing, or do we have a little bit of a harder landing? It’s a debate that I’m starting to have with myself going forward six months down the line. I mean, the rate cut idea is just absolutely mind-boggling to me. I can’t see it until Supercore or Core starts going under two % CPI prints. I don’t want to even talk about cuts.

Tony Nash

Well, I guess the thing that I have started to see over the past month is people saying, Maybe this time is different. And when I start seeing that, that’s when I start to worry, when people start saying, Maybe this time is different. I don’t know, maybe it is, but it hasn’t been before.

Johnny Matthews

I think it is-

Albert Marko

Go. Ahead. Johnny.

Johnny Matthews

I was going to say it is very different from what people have experienced. We had the financial crisis that… And at the time, we all read this Reinhardt and Rogoff book, “Eight Centuries of Financial Folly.” In the book, they said, “Right, you’re going to have a decade of sluggish growth and low rates. You’re doomed to that.” They were right, and that’s what we had. People’s expectations now are that rates are going to go back to that super-low level.

Johnny Matthews

Then we had a pandemic where we shed 20 million workers in a space of a month and then tried to hire them all back as quick as we could. It just wasn’t possible. We had all these supply chain snares and excess labor demand. The interesting thing after the pandemic, from my perspective, is that in the same way as the US, there was a much greater demand for labor than the available supply. The vacancies were running at twice as many unemployed workers, a much higher ratio than you’d ever seen before. It was the same in something like 20 of the top OECD advanced economies. The same thing happened. We had it in the UK, where vacancies as a ratio to unemployed people were higher than they’d ever been.

Johnny Matthews

And it was the same. There was this global shortage of labor. It is different in a sense that we had a decade of doom, gloom, just unable to really get the economy motoring. Then we had the pandemic, and then everything was shaken up. And people have these biases that are influenced by their experience over the prior sluggish decade and think that rates are going back down there, but they’re not. This is a whole new world we’ve entered.

Tony Nash

I would recommend anybody… This was recommended to me by someone on Twitter. It’s a book called The Price of Time by Chancellor. If you have not read it, it’s an absolutely interesting read on interest rates. Every time we have a period of low interest rates, when interest rates rise again, there is this period of delusion where people think higher interest rates really is going to impact us like it did last time, and then something happens. Is that something going to happen? I don’t know, but it’s happened every other time. I’m not a doomer like I hope it doesn’t happen, but I’m always a little bit wary of that. Albert, go ahead.

Albert Marko

Yeah. I mean, if you go back throughout history, humans do the same thing over and over again, just repurpose and regurgitate policies and rhetoric from the previous, from the predecessors. I fully expect the Fed to do the same thing that was done in the ’60s and ’70s in terms of errors, just the way humans are. They’re looking for some rally, and I think that they’ll probably make a mistake leading up to it. Inflation is such a problem, Tony, that Barkin and a few other people are starting to come out saying, Well, maybe we should talk about moving the inflation target up a couple of notches or making it fluid.

Tony Nash

Let’s hold off on that. Let’s hold off on that for just a second, okay? Let’s close out. Tracy, do you want to… In terms of this time is different or something like that, what are your thoughts on that? Because we’re seeing crude at relatively, I would say, average to low prices. But it’s not whatpeople, I guess, what people would expect given the level of demand that we’re seeing. Do you expect those prices to kick up? We’ll talk about OPEC in a couple of segments, but just generally, just where we are economically, what’s your view on… Johnny mentioned that oil prices may kick up next year. Is that your general view?

Tracy Shuchart

Yeah. I have to just push back on what you just said just a little bit because I think, first of all, at $76, oil is still higher. You know what I’m saying? Than the historical north. So what we are seeing-

Tony Nash

I’m buying the narrative that we’re at cheap oil, sadly.

Tracy Shuchart

Yes, we have seen oil prices come down, but oil prices above $100 are not really sustainable. You would bring down virtual markets. It’s terrible for everybody. Still, sustained higher oil prices at $76—everybody thinks this is, “Oh, yeah, we saw 120 after the Ukraine invasion, and then we saw another kick-up to 95 after the conflict in Israel.” But literally, if you back out to your five-minute chart for a minute, we’re in this range where we’re at $72 to say, for WTI, a $72 to $85 range, a bit higher for Brent. That is still historically higher than we’ve seen.

Tracy Shuchart

Yes, we are seeing that really hit us right now in the US, but we are definitely seeing that hit in Europe, particularly in Germany right now, where you have a lot of companies leaving because energy prices are just higher there. I understand that has to do with a lot of the policies they have, but still, natural gas prices have come down, things of that nature. Energy prices, in general, are still rather elevated compared to what they have been in comparison to historical norms.

Tracy Shuchart

I think that absolutely the risk is higher energy prices next year. I think that’s a complete possibility. I think all eyes are on the US right now for a multitude of reasons.

Tony Nash

Great. Okay, let’s wrap that up and let’s move on to Fed speak.

Tony Nash

Hey, I’d like to make sure you know that you can access our AI-driven market forecasting tool called CI markets for free. No strings attached and it does not require any credit card information. Go to completeintel.com/markets to subscribe. CI markets is the perfect addition to your analysis toolbox. This free account includes Nikkei stocks, major currency pairs, and global economics. Of course, we offer much more in our paid account, but this lets you experience CI Markets before making a financial commitment. CI Markets uses the power of AI to help you make better trading investment decisions. It’s absolutely free. Again, go to completeintel.com/markets to subscribe to CI markets free.

Tony Nash

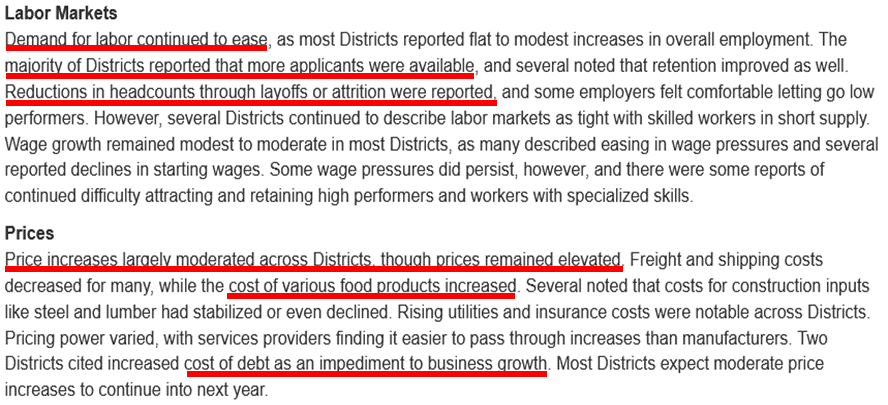

Albert, there were a number of Fed speakers and the Beige book was released this week. I think it’s easy to dismiss the Beige book, but there are some pretty clear statements in it regarding slowdown in inflation and easing of job market.

Tony Nash

I’ve got on the screen a screenshot of the takeaways from the Beige book. It has phrases like, Demand for labor continued to ease. Phrases like, Reduction in headcount through layoffs or attrition were reported. Things like price increases, largely moderated. Those are the things at the top of the takeaway sections.

Tony Nash

But lower the takeaway sections, there are things like cost of various food products increased. Anybody who goes to the market understands that. Increased cost of debt as an impediment to business growth, which we mentioned with Johnny earlier on small companies. That seems to show some continued headwinds. What are your thoughts on that? I mean, it’s a mixed message.

Albert Marko

Well, yeah, depending on which Fed speaker is talking and which way they lean politically. I mean, some of them want to show that the market is resilient and the economy is resilient for political purposes. Others have better intentions of actually trying to get the economy on a stable footing at the moment.

Albert Marko

Labor layoffs are not coming fast enough for the Fed. I mean, I hate to be the guy saying such a thing because of the personal aspect of people losing their jobs and whatnot. But in terms of how the Fed’s policies working, the layoffs are just not coming fast enough. Honestly, it’s because no company wants to be that first one that lays off a significant number of employees because of the political ramifications that come with it in this atmosphere. We’ve talked about that.

Tony Nash

They’re trying to employ more people, so having higher interest rates makes it harder for those small companies. You’ll see more small companies and mid-sized companies close. I think that’s where a lot of your layoffs will be found.

Albert Marko

eah, but they can do a lot of stuff to help that to alleviate that. The SBA loans that a lot of these small companies took up to $2-5 million can easily be forgiven. If they really wanted to sit there and help small and medium-sized companies, they can do stuff like that instead of letting layoffs gain steam or closures and whatnot.

Albert Marko

Like I was saying previously, food prices are still on the verge of going higher. A lot of it’s due to the energy issues of natural gas and oil going forward. There’s a lot of derivatives in that, specifically fertilizers and stuff like that. Those become problematic. Again, we like to harp on inflation in this channel, but that’s just it’s sticky. Supercore is sticky. It’s problematic. Barkin is out there now saying CPI target should be or inflation target should be fluid or a little bit above 2%, which was absolutely dismissed. I was laughed at when I said that this is probably going to end up happening about a year ago.

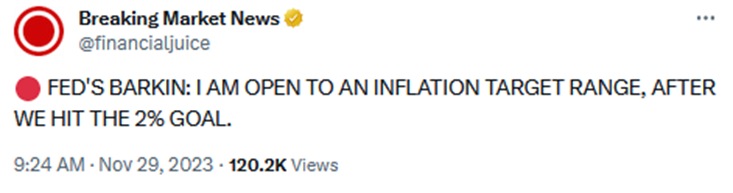

Tony Nash

Let’s go to that. Okay, so Barkin was out this week saying, and I’ve got this on the screen, I am open to an inflation target range after we hit the 2% goal. He’s saying that now. In August, just a few months ago, he said a new inflation target would risk Fed credibility. What’s happening and what’s changed since August for him to change his view?

Albert Marko

It’s sticky. It’s hard. Like Johnny was saying earlier, they did the easy work. They got it down to 3. Whatever fake number they want to throw out there. But now to get this to an actual 2% target, they’re going to have to do a lot of hard things. I don’t think they can really do it. I mean, you know what? They could probably say, Oh, look at this healthcare data is minus 68 %, and shelter is minus 14. Oh, we hit two %. Now let’s change it. They could do something silly like that, but I don’t think the market and everybody else is just going to laugh at them. They’re going to lose credibility, like Barkin was saying a year ago.

Tony Nah

Johnny, what’s your thought on that?

Johnny Matthews

Yeah, I really don’t think they would dare change the target. But by the same token, I don’t think they’re going to hit it. I mean, if they do continue tightening or they hold rates at the current level for long enough and they start to see some deterioration, some further deterioration in the labor market and unemployment continues to creep higher and higher and higher, with inflation at three or slightly lower, that would be good enough for them to cut rates. They’re just not going to get it down to. The two % target.

Tony Nash

They’ll talk about lags or something and. Say-

Johnny Matthews

Yeah, exactly. They’ll put it in their forecast, in the Philips curve framework, with unemployment going higher, wage growth will continue to slow down, and that means services inflation will continue to decline. They can do pretty much whatever they like to come up with reasons for cutting rates, and that’s what they’ll do. If getting down to the two % target and sacrificing the economy and sacrificing a whole load of jobs and pushing unemployment up to six %, they’re just not going to do it. They’re going to stop at a little bit below 3%, that’ll be good enough for them. And I think actually, for most people, they would think, Okay, well, it’s not so bad if inflation was three %. So –

Tony Nash

Don’t help us if someone like Austin Goulds, if he ever becomes Fed share, because we’ll have inflation targeting at like six % or something. I mean, it’s people love to be critical of Powell. But the guy is being, I would say, relatively disciplined in keeping prices at a reasonable rate. I mean, he can’t help supply chain issues, but he’s really staying very focused on this 2% target. I think he should get some credit for that.\

Johnny Matthews

Oh, absolutely. I think he’s to the past few decades I’ve had to listen to speeches from the likes of Janet Yellen and Ben Bernanke, which was so boring. My ears were bleeding, honestly. It was just unbearable. At least Powell, when you ask him a question, he answers the question. He doesn’t just waffle on and on and try to skirt around it. He answers the question. He was asked recently where do you think the neutral rate is? And he basically said, I don’t know. I just don’t know. Who the hell does know?

Tony Nash

It’s theoretical anyway, right?

Johnny Matthews

Yeah, who the hell does know? I really welcome that in the Fed Chairman. He’s very clear and down to earth. I really do like that. But just getting back to the labor market and what the Fed will do, one thing that we haven’t discussed that is a bit of a concern to me is that when I look at the cyclical or non-cyclical components of job growth, what I call the non-cyclical government, education, and health care, that’s showing now reasonably strong growth, stronger growth than the cyclical components, which surged after the pandemic, and now they’re coming down and down and down.

Johnny Matthews

In the last payroll print, it was something like 150,000 payrolls, 50,000 were with government. I don’t know what the breakdown was between education and health care, but you can see what I mean. More of the jobs were in non-cyclical sectors, and that is really quite a concern to me. I think the Fed will start to focus more on the labor market if this trend continues. Getting back to your earlier point, Albert, and what we were discussing earlier, with inflation down where it is currently, if the labor market really does begin to crack, the Fed, they will start cutting.

Tony Nash

Yeah, they’ll say dual mandate, right? And they’ll start cutting and say, I don’t care where the inflation rate is. We need to start cutting for jobs.

Albert Marko

Yeah, which will be a mistake, like usual. It’ll be a mistake.

Tony Nash

That’s true. Can we just have a moratorium on government jobs for a while in the US?

Albert Marko

Yeah, they should do a skeleton crew of just basic one-tenth of what they have out there and cut their salaries too until they get things right.

Tracy Shuchart

I love it. I mean, where do I load on that?

Tony Nash

Just in terms of –

Tracy Shuchart

Can we. Put that on the ballot?

Tony Nash

Just in terms of inflation target, are there other central banks, say, in Europe or England or whatever, that are doing inflation targeting right now?

Johnny Matthews

Oh, yeah, all of them. This whole inflation targeting thing, this two % target was just plucked out of the air by some, I think it was a treasurer of the New Zealand Central Bank, just came up with two %. Yeah, that sounds like a. Good number.

Albert Marko

Sort of like COVID social distancing.

Johnny Matthews

And it stuck. One central bank after another adopted a two % inflation target. So we have it in the UK, they have it in Europe, they have it in Australia, New Zealand. It’s become a universal thing. But it was just a spurious number that they picked. There’s no real science behind it.

Tony Nash

It’s like I’m old enough to remember when 6% was the assumed natural rate of unemployment.

Albert Marko

You know, if they wanted to have-

Tony Nash

This was in the ’90s. 6% employment was normal.

Albert Marko

Yeah. I mean, if they want to have an actual discussion on what an inflation target should be, I welcome that. But the fact of the matter is they’ve stuck to this 2% threshold and if they deviate from it, it’ll have repercussions.

Tony Nash

Huge repercussions.

Johnny Matthews

Absolutely. I mean, we’ve already seen inflation expectations in the Michigan survey creeping higher. The longer term inflation expectations are the highest they’ve been in I don’t know how long. And it’s strange to have one year inflation expectations going higher when gas prices are heading south. So that is the big danger, isn’t it?

Albert Marko

How much. Of it, though? Sorry to interrupt you, but how much of that is due to wage growth that just keeps on creeping up? It doesn’t stop, really.

Johnny Matthews

I think the two things feed each other, don’t they? High inflation feeds higher wage demands, and then wage growth feeds into services inflation. That has always been the big fear of central banks that you have this wage price spiral, and that’s how it… That’s how it rolls along.

Tony Nash

Yeah, but that doesn’t exist, Johnny. We’ve been told for the last three. Years that the wage-

Johnny Matthews

Yeah, true.

Albert Marko

We talked about that, Tony, I think even like a year ago in the doom loop of wage inflation, energy inflation and interest rates and so on and so forth. And here we are. Here we are. Experiencing this.

Tony Nash

Yeah. Same discussions, not a lot’s changing aside from the interest rates. I think I like your rosy charts, Johnny. I’m not quite sure from that first segment. I’m just not quite sure how it all sticks in, say, the 3-6-month time frame. Again, I don’t want to be a downer. I’m just seeing some of those correlations, especially on that business chart, really break down over the last 12 months. There are a lot of things around unconventional Fed policy, discussions about new inflation targets, other things where expectations in the marketplace, people don’t know what to expect. They don’t know if their food is going to rise another 15% next year. They don’t know if cars are going to be cheap or expensive.

Tony Nash

I think we do have a lot of this slack in terms of what consumers have on the sidelines. But I think on some level, they’re keeping dry powder because they have no idea what’s going to happen. We’re hearing about this new virus in China that’s supposed to go out. Nobody knows what’s going to happen, and they don’t know the unpredictable factor. Going back to the government employment that you talked about, nobody knows what governments are going to impose on people if this thing really is a new thing. I think that uncertainty is probably hurting some government spending or some company spending, some personal spending and other things. I could be very wrong here. But I think a lot of those expectations have broken down because there’s a lot of uncertainty really around prices, especially. At the household level.

Albert Marko

Yeah. But, Tony, the thing is looking at Johnny’s rosy charts, well, he’s probably going to be 90% right.

Tony Nash

Of course. I think so too.

Albert Marko

Over the next. Six months, five months of it is going to be absolutely what is Johnny is talking about.

Tony Nash

I think you’re right. The part that worries me is the question mark.

Johnny Matthews

Well, I put those charts together. I did another talk recently. I said that I’ve been a recession denier for the almost two years now. When the Yield Curve first inverted and people were screaming about the oncoming recession, I just couldn’t see it with what was going on. But I’ve got to be honest, some of the data more recently do suggest that, well, clearly the economy’s lost momentum. I mean, it was never going to carry on growing up north of five % like it did in Q3.

Johnny Matthews

But consumption growth that we were seeing that we saw in October wasn’t bad, that was okay, and Q4 consumption growth could still be on track for two %. The wheels haven’t fallen off. I’m hopeful that now that headline inflation has come down a long way, primarily driven by lower energy prices and cheaper gas, people have more discretionary income and they’re going to spend it. They’re going to carry on spending it. And it’s these services that are really benefiting, sporting events, concerts, whether it’s Beyonce, Taylor Swift, people pay top dollar to get a ticket and they’re lucky if they can.

Tony Nash

That’s right.

Albert Marko

$1300 a ticket for the Michigan-Ohio State game. $1300. Those were Super Bowl-

Tony Nash

What score was that? Is that Rest Night or something?

Albert Marko

Well, the real football. Listen, I’m a big soccer. I’m a huge soccer fan, so. I got to throw that dig into the British guys.

Johnny Matthews

That’s all right. We used to it.

Tony Nash

Tracy, you were raising your hand about services. Was there something you wanted to add there?

Tracy Shuchart

No, I wasn’t. I’m sorry. That was an accident. I was. That was a. Total accident.

Tony Nash

Okay, great. Let’s just keep talking, though. Since we’re talking about things coming back next year and a little bit of uncertainty, there was an OPEC meeting this week. Can you talk us through what happened, why is it important, and what are the expectations for next year?

Tracy Shuchart

Yeah, absolutely. I think the major problem is we saw that big drop after the OPEC meeting, even though we had additional cuts. I think the market was expecting OPEC to have a solid plan and not to announce that additional voluntary cuts would be announced by each producer individually. But how it all shuffled out at the end of the day. We saw market kick up a little bit afterwards and again today. But the long and short of that, the whole situation was what we have is we have 1.5 million barrels and cuts and voluntary cuts carried over from this year between Saudi Arabia and Russia. Then we have an additional 684,000 barrels per day cuts between several nations.

Tony Nash

Okay. If they agreed that today, how long before that’s implemented?

Tracy Shuchart

That’s implemented starting Q1. It’ll start January first because the current… There’s two parts of this. The current agreement that was supposed to end December 31st, 2023, on the quotas, the depressed quotas that they came up with last summer are going to carry over again for another quarter. Then on top of that, we had additional voluntary quotas. Again, it’s the same numbers, except for heading into Q1 for the group as a total, we’ll have the long and short of it is we’ll have an extra 684,000 barrel per day cuts from today’s levels, from Q4 levels.

Tony Nash

Okay, so you said something interesting. You said voluntary. The 684,000, are these all-voluntary cuts?

Tracy Shuchart

These are all voluntary cuts. You have the nations that were voluntary were Algeria, UAE, Oman, Kuwait, Kazakhstan, and Iraq.

Tony Nash

Okay. How voluntary is voluntary? I mean-.

Tracy Shuchart

Well, voluntary.

Albert Marko

And how much of it is maintenance baked into the voluntary cuts?

Tony Nash

Great question.

Tracy Shuchart

Well, this is where you get… This is where it gets sketchy, but these are voluntary cuts. I do expect, I think, Iraq. Iraq sounds like to me they’re counting on Kurdish oil not coming back soon. That sounds like they’re voluntary cuts to me, to be honest with you.

Tracy Shuchart

I think the rest honestly would make those. I was not surprised UAE or Kuwait or Oman would curb less… I think, who is the largest UAE at 163K BPD? It’s nothing for them. The rest didn’t really surprise me. They’re very small cuts. Obviously, you come into springtime and there’s a meat season for all these players, and so partially that factors in, but generally not for January or February.

Tracy Shuchart

But in those cases too, part of that also could be they don’t have to produce as much because they don’t have summer demand anymore, domestically speaking. There’s a lot of ways you can look at this situation, but the market was really expecting a broader base cut between the group and it to be on the final communique and to say, We’re going to do this plus another million barrels per day. That’s what the market was expecting because of all the nonsense headlines that were leading up to that.

Tony Nash

Okay. The market took it pretty much in stride, didn’t see it as a big deal. Yes, it’s more supply offline, but….

Tracy Shuchart

Yeah, we saw a significant drop. We saw a volatile drop from $80 to $76 in WTI. We’re bouncing a little bit back after that after the market’s been seems okay with the fact that there still will be additional funds.

Tony Nash

Okay, great. Albert, what do you think on that?

Albert Marko

I mean, it’s just the open game of we’re going to do cuts, and then all of a sudden, ship-to-ship transfers without transbinders are moving everywhere in the Persian Gulf. It’s like, yeah, whatever. You know what I mean?

Tony Nash

Johnny, we’re skeptics here on the weekend, just so you know.

Johnny Matthews

Oh, well, yeah. I mean, it sounds nuts to me. A bunch of these guys get together and say, agree. Well, we’ve got to cut two and a bit million barrels a day of oil production. I volunteered to do a couple of hundred thousand a day and they will share it out, but it’s voluntary. Well, none of them are going to do it, are they? They’re going to say, Well, okay, they’re doing it. I’m not going to bother. I’ll just pump it out while the price is still where it is.

Tony Nash

Right. They said it was voluntary, right? So…

Johnny Matthews

Yeah, exactly. It was voluntary. It’s voluntary. It’s like anything else, voluntary. You don’t have to do that.

Albert Marko

And that data doesn’t until the end of 2024 again, so whatever.

Tracy Shuchart

I will. Say in OPEC’s defense, after the 2020 April debacle when oil prices went negative and in March when they had the blowout and everything crumbled between Saudi Arabia and Russia, we have seen a little bit more cohesive of a group and that has helped keep oil prices elevated. I think it’s also interesting to note that Brazil has just joined the plus part of OPEC. I think that’s generally politically motivated, but that’ll start in January first, 2024.

Tony Nash

Interesting. Okay. Maybe we’ll see some Middle Eastern sovereign wealth investments in Brazil as a part of that or something?

Tracy Shuchart

I would not be surprised.

Tony Nash

Interesting. Okay. All right, let’s move on to silver. I think, Tracy, there’s some really interesting things happening in the silver market. Silver has been pretty strong lately. Now, we saw a huge run-up in silver in 2011. Part of my reason for wanting to cover this is I’m wondering if we’re going to head there again soon.

Tony Nash

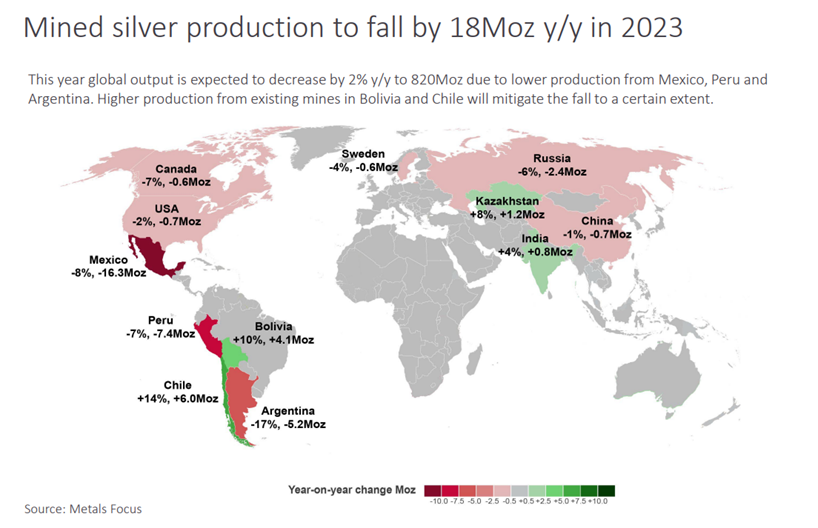

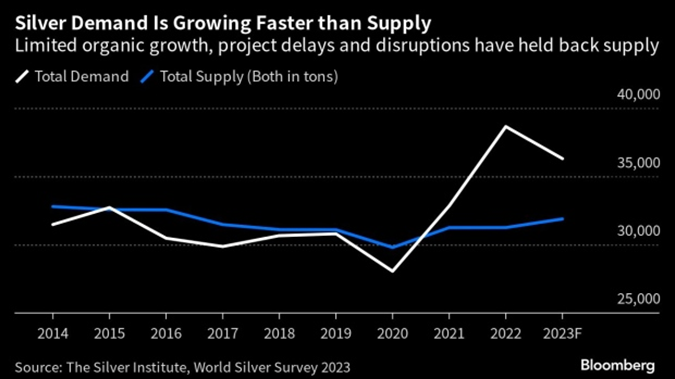

I guess the most fundamental question in a precious metal market like silver is supply-demand. Silver production has been expected to fall about 18 million ounces in 2022, with the largest cuts in places like Mexico, Brazil, sorry, Peru and Argentina. At the same time, we’re seeing a huge upswing in demand over the last two years. This is the second chart where the white line is total demand and the blue line is total supply.

Tony Nash

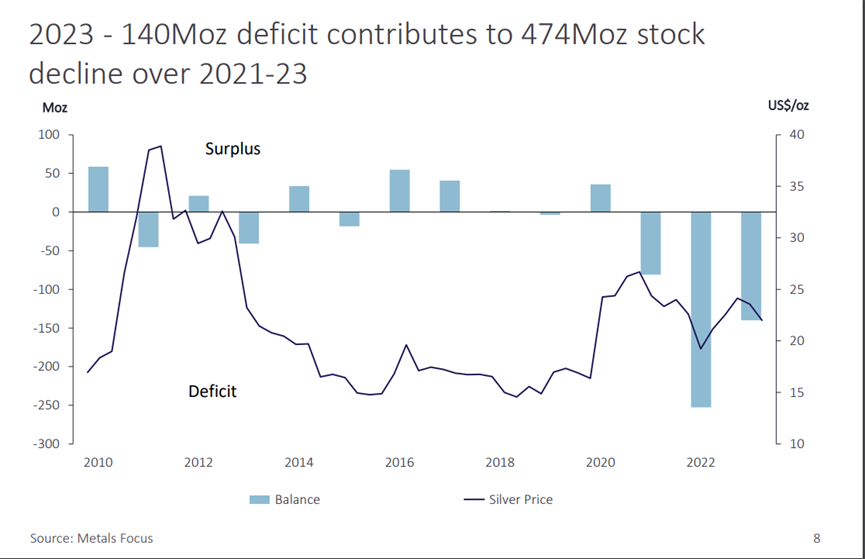

We’ve seen silver supply fall, but we’ve also seen the price not necessarily keep up with that. Can you help us understand what’s happening in silver markets? This third chart is showing a decline in silver prices as the balance is in deficit. What industries do you see driving demand and what would bring supply back online?

Tracy Shuchart

Yeah, I think when you’re talking about silver, most people think of it as in jewelry and/or physical investment such as gold. But you have to think about the industrial properties and the industrial uses for silver, and that’s really 45% of the market. Really 27% is investment, and you’re talking even lower percentages when you’re talking jewelry or anything like that.

Tracy Shuchart

When we’re talking about industrial properties, especially with transition, green energy, this big push that we’re having, we’re talking solar panels and EVs in particular, but you also have healthcare demand too, that is also growing. That demand has been there for a while, but if you want to look at where the demand is exponentially growing right now, we have to look at, say, things like solar panels, which have found that silver is much better for use in solar panels than anything else right now. It’s long and short without getting too technical about it.

Tracy Shuchart

Then if you look at vehicles, for example, all the soldering and everything, we all use a silver. Then when you start talking about EVs and hybrids and EVs, you’re talking about more electric components than ICE vehicles already currently have. There’s a lot of demand coming particularly from that industry.

Tony Nash

Okay. So do you expect strengths, like real strength, $30, $40 an ounce strength to return to silver markets as a result of this demand at some point?

Tracy Shuchart

At some point. I won’t say tomorrow. The silver market is very finicky. Most people, it’s very volatile. You had the Hunt Brothers, right? Yeah. The silver market. And so in a lot of it’s paper, too. You have to understand a lot of these things are paper. And so if I were looking to invest in the silver markets, I would look for something that was backed by actual silver, just say, rather than paper markets, but that’s just a side note. This is not investment advice.

Tracy Shuchart

I think that possibly we could return to those levels as soon as people realize what the deficit is really going to look like. It’s particularly, we’re not in a nerve world anymore. If you have all these mining projects, they take a lot of money to find. A lot of money to finance. With rising interest rates, these make a lot of these projects unaffordable or harder to get off the ground because they cost so much more money. I actually posted a chart today which basically says that my production is not expected to get to the highs that we were like any time soon. Again, in this current rate environment. That’s also something to factor in. I keep trying to stress that these projects take a lot of money and a lot of money to borrow from the banks, and it’s just not that affordable. It’s just not as affordable anymore. Plus, you have that permitting issues, you’ve got all sorts of problems that are already conducive to the mining industry trying to get a project off the ground. Interest rates certainly are not helping that.

Tony Nash

But Tracy, if we couldn’t get people to invest in things like silver mines and upstream oil and gas and all these things at zero interest rates, what’s going to be the thing to drive them to invest with higher interest rates?

Tracy Shuchart

Well, that’s exactly. If you were to invest in the market, you would be investing on the supply-demand imbalance, not necessarily. Or you would be looking at either current mining companies that are already producing and/or mining companies that have already borrowed, already permitted, and maybe haven’t started yet. You want companies that are halfway there, so to speak.

Tony Nash

Yeah. No, that’s really interesting. The miners are-

Johnny Matthews

I thought the question was-

Tony Nash

Sorry, go. Ahead, Johnny.

Johnny Matthews

Yeah, yeah. Because this third chart of yours that shows quite a deep deficit of production compared to demand. Yet the price hasn’t really responded up to now. The price is going higher, has gone higher in the last few weeks, alongside gold because the dollar has been sinking.

Johnny Matthews

Question one is, how do you explain the fact that it doesn’t seem to respond to demand or the supply deficit? The question two is just a general question because I was quite bullish of silver a few years ago when inflation just started to pick up. I bought a silver miner on the expectation that some of the factors that you were talking about before were there are very high costs to running a silver mine. When the price goes up, the profit in the mines goes up a long way. It’s a bit like owning almost like a cool option on silver, in theory, if you are in the mines, you should get that payoff. Except that maybe it’s just the mine that I owned, but seems to me like these silver mines underperform what you’d expect when the silver price goes up.

Johnny Matthews

So my second question really is, are you not just better off to buy an ETF or something?

Tracy Shuchart

Yeah, I would suggest that unless you really know your stuff on silver miners, they’re very difficult to trade. You also have to think for the last 11 years, we almost had not a lot of supply, but supply on the market. We’ve had the last 11 years, it’s been a terrible market to invest in. We’ve had more supply than demand. It hasn’t really gone anywhere. You’ve had no reason to really… If you were looking at you’re an investor and you want to invest in precious metals, so to speak, that hasn’t been really the big trade either. I mean, gold’s gone sideways, silver’s gone sideways. It really hasn’t been… Really hasn’t been a really attractive market, so to speak, for investors, unless you’re a very long-term investor.

Tracy Shuchart

But I think that’s changing because if you look at that chart and you look at the last three years of deficits, that’s more than the last 11 years of supply upside at all. And we’re only talking… Nobody’s getting rid of the screen push. Everybody’s still gung ho for this. The EV push is still there. And so in my opinion, I just don’t see supply catching up with demand anytime soon, and I don’t see any real new greenfield projects coming online right now.

Albert Marko

I hate silver.

Tracy Shuchart

Everybody hates silver. It’s been a terrible trade. I mean, it’s been a terrible trade. I think for the first time we’re seeing opportunity, particularly because we’re seeing this demand in transition materials. We’re also seeing higher demand in the healthcare industry, which that demand has always already been there. But again, it’s not a market for everybody. I mean, it’s not an easy market to start at home.

Tony Nash

Yeah, be careful.

Albertt Marko

That and net gas are widow makers for me. Yeah. Notorial.

Tony Nash

Yeah, this is fantastic. Thank you, guys. Thank you so much for all the thought you put into this. Thank you so much for sharing your insight. Really appreciate it. Have a great weekend and have a great weekend. Thank you.

Trcay Shuchart

Thank you.

Albert Marko

Thank you so much.

Johnny Matthews

Thank you.

AI

That’s it for this week’s episode of the week ahead. Please don’t forget to rate us and review on whatever platform you are watching or listening to this. Thank you.