Week of June 15, 2026 – CI Markets Weekly Outlook

The market is undergoing a profound transition, signaling a structural shift beyond the initial AI hype cycle. Last week, the broader technology sector faced a severe reality check, heavily pressured by rising AI skepticism and a disappointing earnings report from Broadcom. However, this dynamic does not represent a wholesale abandonment of equities. Rather, it marks a rapid rotation away from speculative growth and toward tangible value and industrial quality. Adding a layer of complex regulatory overhang, President Trump has summoned top AI executives to the White House next week. This impending summit introduces significant policy uncertainty into the tech space, further accelerating the flight toward legacy incumbents and traditional industrial sectors. Meanwhile, the highly anticipated SpaceX IPO continues to draw capital and attention, highlighting the market’s appetite for tangible, frontier hardware over unproven software concepts. Simultaneously, weekend geopolitical developments surrounding Iran peace negotiations are forcing a rapid repricing in energy markets. CI Markets signals a week of intense strategic repositioning, where investors prioritize foundational industrials, legacy tech quality, and recalibrated commodity risk.

No contract. Cancel anytime.

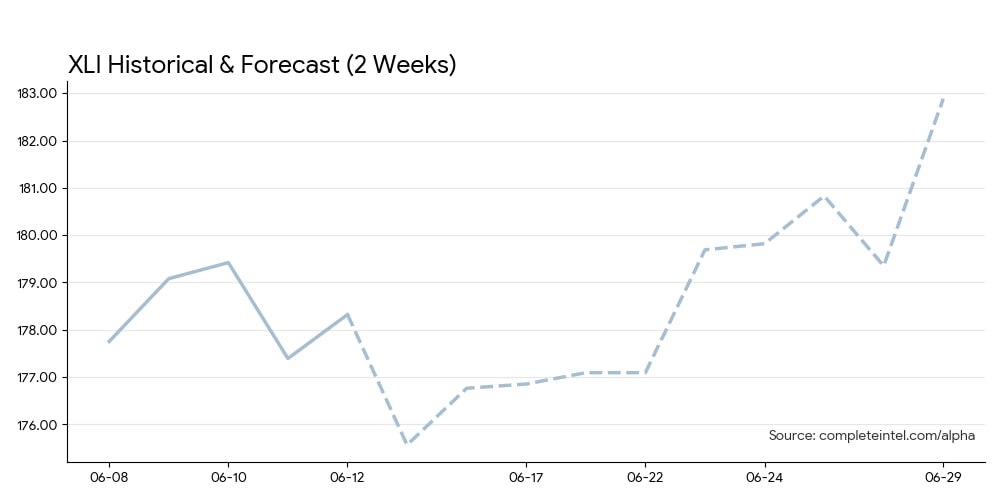

▲ The Industrial Rotation Takes Hold: Industrial Select Sector SPDR Fund (XLI)

As capital rotates out of high-flying tech names, it is actively searching for grounded value, and the Industrial sector is catching the bid. After a brief recalibration to open the week, CI Markets forecasts the Industrial Select Sector (XLI) to build steady, day-over-day upward momentum, actively breaking higher as the rotation matures. This indicates that institutional capital is not just fleeing speculative growth, but is structurally reallocating into foundational, “real economy” sectors. Investors should view this upward trajectory as a signal that the rotation toward quality is finding solid footing.

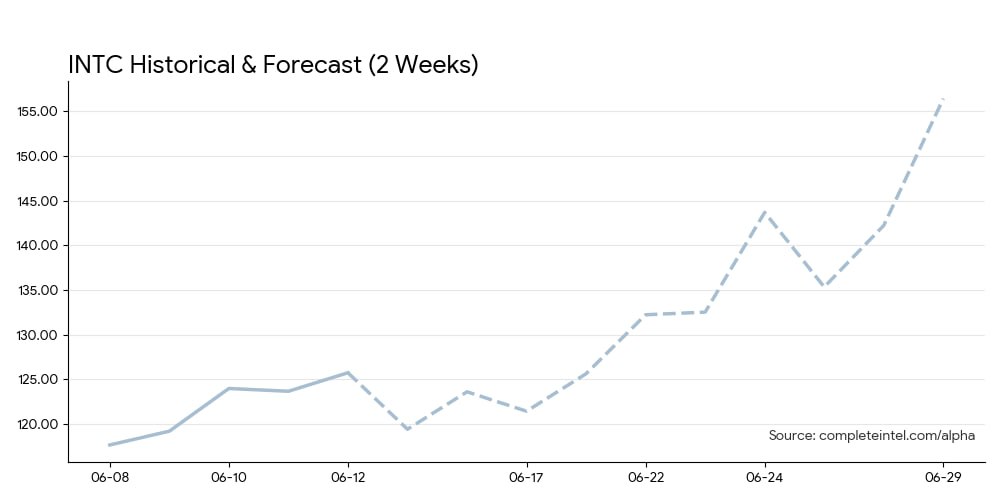

▲ The Legacy Tech Resurgence: Intel Corporation (INTC)

Amidst the broader tech sector turbulence and mounting regulatory fears, legacy incumbents are catching a significant bid. CI Markets forecasts Intel (INTC) to experience a sharp downward adjustment on Monday, followed immediately by a powerful, sustained upward rally throughout the week. As institutional capital abandons highly speculative, unproven AI plays, it is actively seeking the safety of established blue chips with proven manufacturing capabilities and deep structural moats. INTC’s forecasted strength highlights a clear “flight to quality” within the semiconductor space itself.

▼ The Geopolitical Repricing: Crude Oil (CL=F)

Over the weekend, headlines regarding renewed Iran peace negotiations introduced the possibility of an easing geopolitical risk premium. CI Markets forecast data for Crude Oil (CL=F) perfectly captures this breaking narrative. The model shows an immediate, steep downward adjustment early in the week—reflecting the market aggressively stripping out the geopolitical premium—before finding a lower floor and establishing choppy consolidation. This provides a clear, data-driven signal that energy markets are rapidly recalibrating to the weekend’s diplomatic developments.

Conclusion

The signal for the week of June 15 is a Structural Repositioning. The market is actively punishing speculative tech while rewarding legacy incumbents (INTC) and industrial quality (XLI), while adjusting to shifting geopolitical realities (CL=F). The Wildcard: Keep a close watch on the headlines emerging from the White House AI summit. Any indication of broadening, stringent regulatory frameworks or additional export controls could severely amplify the tech sector’s bifurcation, heavily favoring established hardware manufacturers over software and service challengers.

No contract. Cancel anytime.

The content presented in this note is for informational purposes only and should not be construed as investment, financial, or trading advice. This analysis is generated from the output of Complete Intelligence’s proprietary artificial intelligence platform and does not constitute a personal recommendation. You should not base any investment decision solely on this material. Please consult with a qualified financial professional before making any investment decisions. Complete Intelligence is not liable for any actions taken based on information provided herein.