In this Week Ahead, Tony Nash is joined by Deer Point Macro, Fabian Wintersberger, and Albert Marko. The discussion focuses on US banks and the credit crunch, ECB & Europe’s banks, and the debt ceiling.

Deer talks about the recent market cap decline in US regional banks and highlights how the slow movement of bank deposit rates are causing depositors to push money into mutual funds. He also shares insights on how banks are provisioning for losses and discusses the potential impact on credit availability.

Fabian provides insights into the ECB’s decision to raise by 25bps and Madame Lagarde’s cautious stance. He also talks about the recent drama in the US over regional banks and expresses concern about the possibility of more wreckage with European banks.

Albert delves into the topic of the debt ceiling, which has recently been making headlines. He talks about whether most Americans care about it, whether US government employees go without pay, and the “full faith and credit of the US government” concept. He also explains why markets care about the debt ceiling and discusses how he expects the situation to play out.

Overall, the Week Ahead offers a thought-provoking discussion on some of the most pressing topics of the week. Tune in to get expert insights from our panelists.

Key themes:

1. US Banks. Credit crunch?

2. ECB & Europe’s banks

3. Debt ceiling

This is the 64th episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

Deer: https://twitter.com/deerpointmacro

Albert: https://twitter.com/amlivemon

Fabian: https://twitter.com/f_wintersberger

Transcript

AI: With CI Futures, you can access AI-powered market forecasting for as low as $20 a month. Get 94.7% market forecast accuracy for over 1,000 assets across commodities, currencies, equity indices, economics, and stocks. With weekly updates, one-month and three-month error rates, and top ten and bottom correlations, you can rely on CI Futures to help you make informed decisions. Join a growing number of satisfied users who have already transformed the way they invest with CI Futures. Don’t wait. Start forecasting with confidence today for as low as $20 a month.

Tony: Hi, and welcome to The Week Ahead. I’m Tony Nash. Today, we’re joined by Deer Point Macro, Fabian Wintersberger, and eventually, we’ll be joined by Albert Marko.

Tony: So, this week has not been a boring week. There’s been quite a lot going on this week, and we really haven’t had a boring week for quite a while. So the first thing we’re going to talk about with Deer is US banks. Is there a looming credit crunch coming? We’re next going to talk about the ECB and Europe’s banks with Fabian. Finally, we’ll wrap up with Albert talking about the debt ceiling, both the politics around it and the reality of it. Will we ever not have a year where there’s a dramatic debt ceiling crisis?

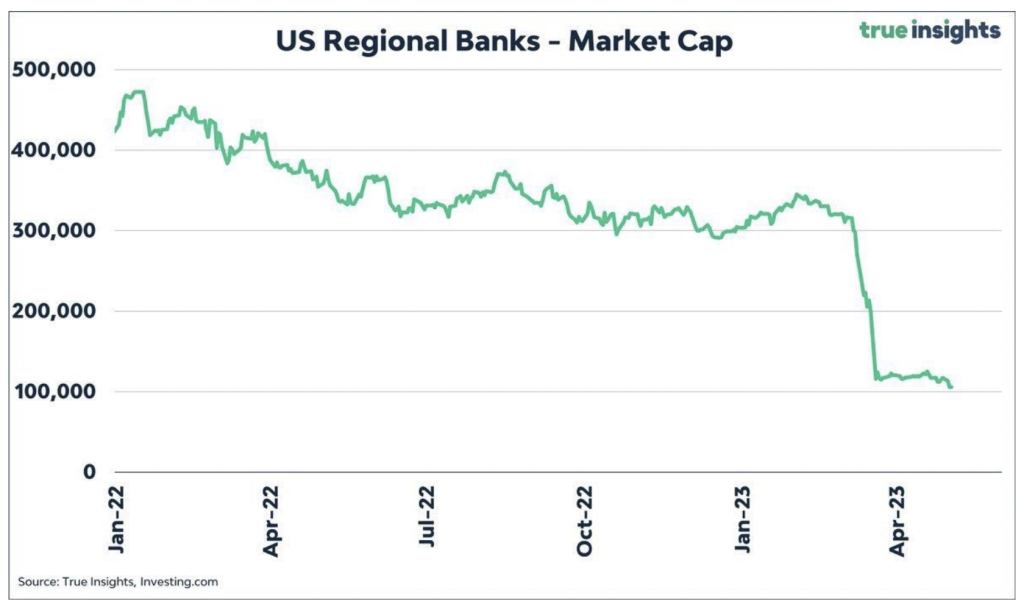

Tony: So, Deer, let’s get started with you this week. Obviously, we can’t avoid it. We’ve seen a lot around US regional banks, right? This chart on the market cap of US regional banks was published earlier this week, and we’re looking at the value of regional banks being about a fifth of what they were in January, which I think is pretty shocking when we see it in one place.

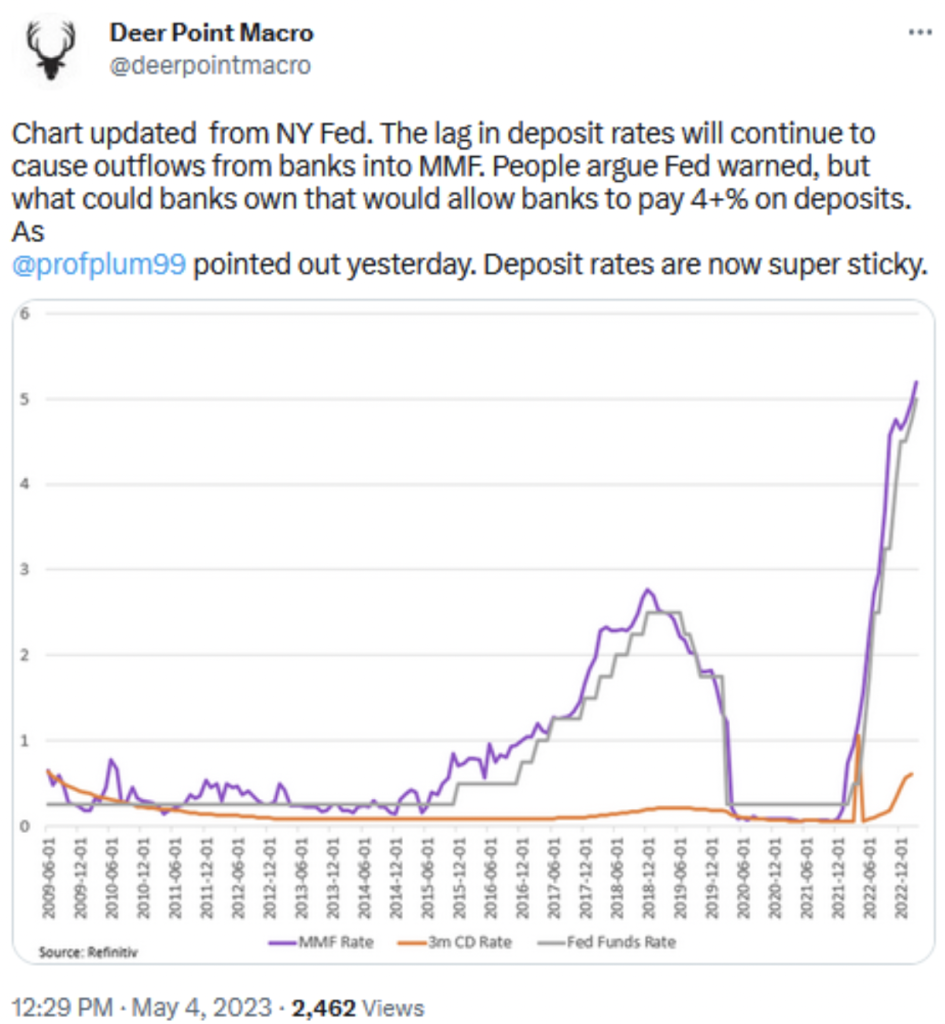

Tony: You put out a great tweet this week showing that deposit rates are pushing depositors out of banks and into money market funds.

The reasons are pretty obvious. When we look at the rates that they’re getting in money market funds, I guess the real question is how do depositors catch up?

Deer: That’s the real question. And I think if we look at what’s happened over the last 14 years, Mike Green actually touched on this a couple of days ago, and I quoted him in that tweet. What could banks have really owned to be able to pay 4-5% on deposits? The answer really is nothing, right? Because if you look at the only thing that has really yielded 4% over the last 14 years or so, it’s been in the high-yield market. And then obviously, you have all the credit risk that’s associated with that. What’s also now been exacerbated is the stickiness of those deposits. I touched on something last night as well on another post where I was kind of looking at some data that the New York Fed posted. Essentially what they found is that if you look at a 1% change in the effective Federal funds rate, the actual beta for deposits is about 26 basis points, and for money market funds, it’s about 88. So the elasticity of money market funds is much easier for them to fluctuate along with the change in the effective Federal funds rate.

But like I’ve said, over the last 14 years, deposits have just become so sticky. I think that’s broadly a function of the fact that there hasn’t been anything in investment-grade paper or otherwise that would have allowed them to actually be able to pay 4% on deposits. And I’ll end that here as well. Even, I know some people say, well, they have the ability through excess reserves and the Fed’s rate.

But as I have said, over the last 14 years, deposits have become increasingly sticky. I believe this is due to the fact that there hasn’t been anything in investment-grade paper or otherwise that would have allowed banks to pay 4% on deposits. I will end my point here. Some people argue that banks have the ability to pay 4% on deposits through excess reserves and the Fed’s rate. They can receive the Fed rate plus 15 basis points and pay deposit holders a rate below this to ensure net interest margins are suitable. However, even with the current federal funds rate at 525 basis points plus the 15 that they receive, banks would not have had enough to pay out 4% on deposits over the last two years. Therefore, I think this has been the problem for banks.

Tony: I was on the board of a microfinance bank in Cambodia for several years. So the precision with which US banks are managed fascinates me because they can watch every move closely. One interesting thing about this flock to money market funds is that back in 2008, we saw money market funds break the buck. Although it appears to be a risk-free approach, there are downsides to both money market funds and traditional banking vehicles.

You shared a great chart that shows how banks are provisioning for losses. Could you explain what this means? While we are not seeing losses as severe as those in 2007-2009 or 2020, what does this indicate?

Deer: I think banks are engaging in practical cyclical risk management by increasing provisions for credit losses above gross impaired loans. Everyone has been predicting a recession for the past two years, and banks are preparing for a possible credit cycle. We don’t know how deep this cycle will be, but by positively provisioning, banks are building a buffer in the ratio between provisions for credit losses and gross impaired loans. This allows banks to be comfortable in case of risk. This strategy may reduce earnings, but many US banks can make up for this through capital markets rather than retail banking. Therefore, I think the current market conditions allow banks to make up for any losses resulting from positive provisioning on the capital market side.

But obviously, if we have an overall slowdown, I just think that banks are being very, let’s say, tactful in the way that they’re actually going about preparing for any sort of credit cycle.

Tony: Okay, that’s good, that’s respectable. So if there is tighter credit, who gets hit first?

Deer: That’s a good question. I would say it’s probably going to end up being middle America, and then I would actually say that it probably flows through into Europe in kind of the offshore dollar funding markets. I mean, obviously, that gets a little into shadow banking. But what happens then is that, once this credit starts to contract, a lot of those European banks, actually the money market funds they have, outflows, and so, therefore, they’re not going to be there purchasing commercial paper, they’re not going to be there purchasing certificate deposits. And then obviously, that leads to funding issues on the dollar side for a lot of European banks. So I think that tightening of credit is actually probably going to have the biggest flow through into offshore dollar funding markets. And you can look at that kind of by dollar funding cost, which is the implied rate minus three-month libor, or I guess you could use SOFR now. Or you could look at that through cross-currency basis swaps as well, and that’s kind of a gauge of dollar shortage of dollars against other currency pairs.

Tony: Okay, so we see the most dramatic contraction in the Euro dollar market first, right? So it seizes up overseas first. So that’s going to hit EM, then it’s going to hit other markets, then it’s going to come back to the US. Is that what you’re saying?

Deer: That’s what I would believe would actually happen, and I would argue kind of what we saw in the beginning of COVID you saw a really seizure in dollar funding markets, and you saw the basis widen. If you were looking at cross-currency basis swaps, you saw dollar funding costs overall increase dramatically. And obviously, that puts a lot of strain on the global capital markets, but especially Europeans, just as a function of the fact that they don’t have access to US dollar retail deposits, but they use a massive amount of dollar-denominated, let’s say, assets to fund long-term portfolios and other kind of funding needs that the Europeans have. So, I would believe it would kind of flow through in Europe and then come back around. But we’ll probably see credit contraction, at least in middle America. But if you’re Apple, I don’t think even in a credit cycle you’re going to have a problem getting access to debt markets.

Tony: Okay, but looking at those US markets is the first person that same.

Albert: Same game plan as 2012, Tony.

Tony: Same game plan as 2012. So then the guys who get hit.

Albert: Over here.

Tony: Okay, so domestically, is it mostly small businesses who will get hit?

Deer: I would say yes.

Tony: Okay.

Deer: And even the NFIB, you can see that if you look at the NFIB, like, what is the credit availability next three months that’s contracted quite drastically.

Tony: Okay, and so is this why the Russell is lagging other markets, and why it’s been so hurt over the last several weeks as well? Because small company credit conditions and small companies are tight?

Deer: I would say yes.

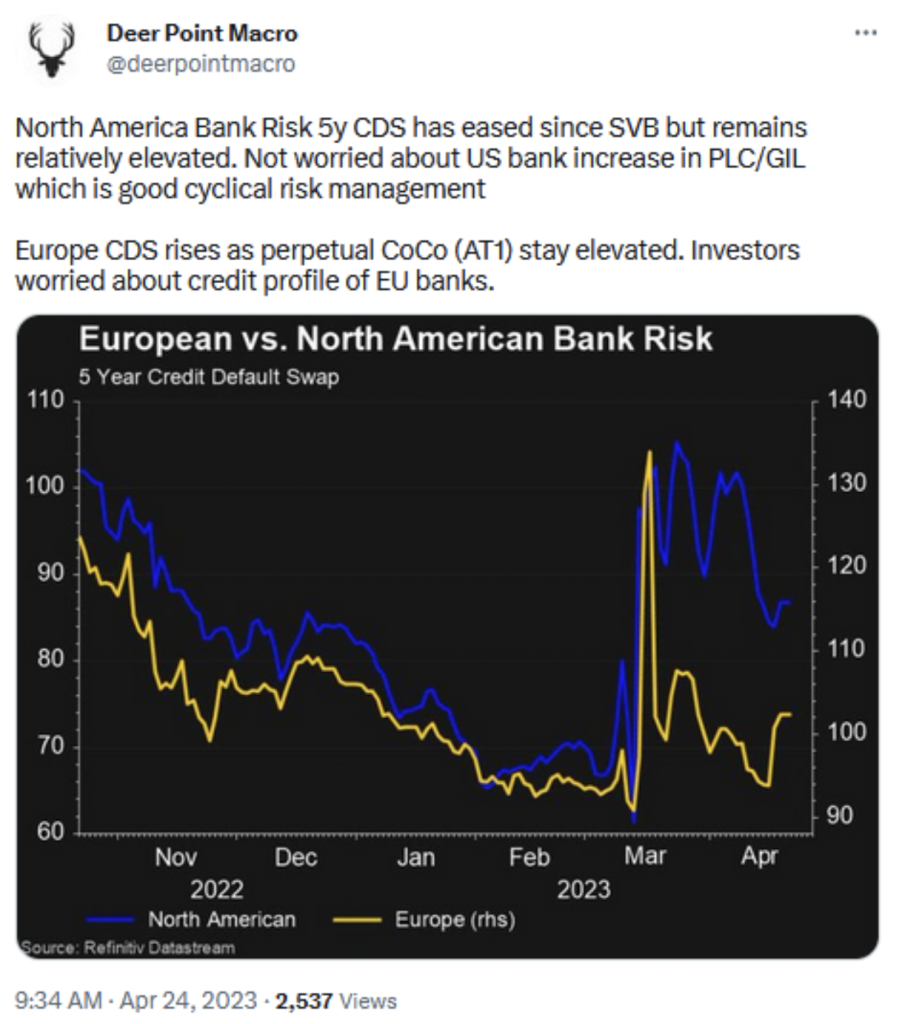

Tony: Okay, very good. Let me ask you another question about one of your tweets about credit default swaps. A couple of weeks ago, you put out a chart comparing five-year credit default swaps for US and European banks.

What does this tell us about the risk in each of those banking areas compared to the US?

Deer: If we look at credit default swaps, they are still elevated, at least in the US. However, they are not as bad as they were in the beginning of November 2022. There is still risk in the US, but I do think that people are relatively assured that the Fed will do whatever it takes. On the other hand, European credit default swaps lag what are called cocoa bonds or tier one capital bonds. We have seen a massive change in the underperformance of perpetual cocoa bonds, which are much more susceptible to changes and fluctuate. They are a leading indicator of what will happen with credit default swaps. Therefore, credit default swaps in Europe are just starting to catch up with where those tier one capital bonds were trading at.

Tony: So is this what happened with Credit Suisse? All those AT1 investors thought it was secured and discounted, but the Swiss National Bank came in and blew them out? Is this why things are a little more difficult in Europe?

Deer: Yes, that’s correct. It’s not a huge market, about $260 billion, but a lot of banks and pension funds hold these because they have outperformed holding European banking stocks. However, perpetuals perform extremely well when there are no bad macroeconomic data or problems in the financial sector. But now that we’re seeing that, a lot of these investors will be on the hook.

Tony: Okay, great. Albert, Deer mentioned that the Fed will come to the rescue. I know you have said some things about this over the past few days. Thanks for joining us. Do you think the Fed will come to the rescue for these regional banks?

Albert: It depends on the regional bank. Bigger banks that have small business exposure, specifically the SBA loans and whatnot, I think they’re going to come to the rescue of those banks. They sent out warnings maybe a week or two ago, where they said the coastal banks are doing their part and tightening lending and whatnot, and then called out the Midwestern and southern banks, not by name, but alluded to it. That signified to me that they want to press the banks to stop lending. That’s their way of tightening at the moment. They can’t tighten because there’s not too much liquidity in the market for the Fed to take. So what do they do next? They use the banks to do it. Credit is drying up, and that’s part of their game plan at the moment.

Tony: Well, this is the traditional monetary transmission mechanism. This is how it was designed in the beginning, with the Fed providing liquidity and banks transmitting that liquidity out to borrowers. Then if the Fed wants to sop up capital, the banks are the primary means for that happening. It seems like the immediacy of this is with the smaller banks, more so than with the larger banks. Is that fair?

Albert: The larger banks are going to play ball. The smaller banks need to chase profits and deal with margins and shareholders. They need money, and they kept lending. You can see that in the housing market, which saw a 10% increase in sales because people kept getting credit. They need to stop that lending.

Tony: With some of these coastal banks that are in trouble, is it their portfolio? To me, I could be wrong, and Deer, jump in here. Is it their deposits that are leaving, or is it their lending portfolio, meaning commercial real estate and other things? That is the bigger concern for investors?

Albert: That’s a little bit over my pay grade, but from my perception, it’s not really so much the deposits, but the risky lending that they’ve practiced over the past few years. I mean, SVB was using G5 jets as collateral for clients buying G5 jets. That all comes into question. And how they manage their risk, which they really didn’t. That’s the problem in my view.

Tony: Okay, do you want to come in here? Is that relevant and accurate? It’s more their loan portfolio than it is the deposit run, which seems to largely be over.

Deer: It’s actually very interesting. I’ll be posting something on this today because I just finished it up yesterday, but I was looking at the proportion of loans to deposits. If we look at the US banking sector in aggregate, deposits are roughly about $16 trillion. Loans are roughly $10 trillion. So there’s a massive base between current deposits to loans. And then if we break it down between large and small banks, the large US banks are about 63% in their ratio to loans as a percentage of deposits. What is actually very interesting is that the small banks are actually far higher. So current loans account for over 80% of deposits. If we look at loans to deposits, it’s actually, in fact, weighted much more to large commercial banks than small banks. I actually think that a lot of these deposit flights we’re seeing is the fault of the media.

It’s much like “It’s a Wonderful Life,” the movie where there was a bank run. If you get on Twitter every day, people are like, “OPAC West is screwed. This bank is screwed. It’s screwed.” So if you’re just an everyday Joe who sees these accounts with 200,000 followers saying, “Take your money from Pac West,” what are you going to do? I think this is actually really the fault of regulatory oversight. I know in Europe and Canada, you can’t come on TV and say, “X bank is screwed,” without tremendous evidence to back that up. We saw that with SVB when they came on, and they were like, “Oh, SVB is screwed.” After a couple of hours after that aired, everybody was freaking out that SVB was over. You can’t do that in a lot of countries. So this fact that we have people who can kind of come on and fearmonger, obviously, if you don’t know any better and you’re just somebody who sees this headline flash across your newsfeed or on your cell phone, you’re going to freak out. If that’s a bank that you bank at, it’s going to cause you to pull your deposits. I do think that a lot of these banks are relatively healthy, and I think that they’re actually extremely important.

Deer: I think it’s also a function of just bad regulatory oversight that somewhat we’re allowed to do this.

Tony: I spent most of my life in Asia, as most people know. If that stuff happened in Asia, people would be in jail for manipulating markets in just about any market there, I think. It’s strange how social media commentary is allowed in the US to manipulate markets, and it’s not prosecuted by the SEC. This goes from, go ahead, Albert.

Albert: You have all those crypto and gold bulls out there saying the dollar’s dying, banks are ending, and to buy this and buy that. It’s shameful. I mean, the SEC needs to really step up on that sort of stuff. I’ve seen very popular financial guys out there on Twitter saying the same thing just to pump their retail services. It’s absurd.

Tony: We see that all the time. Fabian, did you want to jump in?

Fabian: As we talk about the credit crunch, isn’t this exactly what the Fed wanted to have? I mean, they raised interest rates. They want credit to tighten. And I think the main problem is that they kept interest rates for so long that all those banks have a lot of assets that yield basically nothing, and so they can’t raise the deposit rates.

Tony: Yes. Let me ask that to you, Deer, but before we get to that, I want to say that with all this information on social media and other things, your average depositor, even your well-educated depositor, generally doesn’t understand the banking system, right? I mean, you just heard Albert say, and he’s a very educated guy in financial markets say, “Well, that’s kind of above my pay grade,” and I observe financial markets. Fabian observes financial markets every day. I don’t consider myself a banking expert. So your average person saying, “Pull your money from First Republic or whatever,” it’s kind of terrifying. So if there is a regulatory issue, I think part of it is that some of these people really need to be at least investigated to see if they violated applicable laws, maybe not prosecuted, but at least investigated.

Deer, I think Fabian raises a great point about the credit crunch. So, are we going to see a significant credit crunch as a result of the Fed’s actions and some of these higher visibility on some of these regional banks?

Deer: I think that the credit crunch is coming, but I broadly adhere to Milton Friedman’s philosophy of the interest rate fallacy. He said, “We actually saw that when interest rates were increasing recently, you saw increases on a year-over-year basis of volumes of credit issuance.” So if you look at loans and leases at all commercial banks, while interest rates were increasing, banks were also extending more credit. I think what happens is when we talk about the low-interest-rate environment, we think of that through a present value kind of calculation. If I’m a consumer and I’m doing a present value calculation and interest rates are on a mortgage, what was the low? I think people were getting them at almost 300 basis points, so things become very attractive. But on the supply side of that equation, if you’re the bank who has to decide whom to lend to at what price, you’re going to actually tighten credit. It’s a bit against conventional wisdom, but what Friedman pointed out is that essentially when rates are low, it’s because credit has been too tight, and when rates are high, it’s because credit has been too loose. We actually see that because once the rates start to rise, it becomes more profitable for banks to lend. So what do you do? You have banks come in, and you have the supply curve shift to the right, where they’re now going to start to supply the market with more credit. It’s a very interesting thing where it actually seems that consumers are really overall agnostic to what rate they take credit at. Obviously, you see that because if loans and leases are increasing, that means somebody has to be asking for loans for banks to be extending credit. So I think that now that credit is contracting in the face of higher rates, this is really going to pose a bit of an issue for the Fed as well. Because now if there’s no access to credit markets, or if interbank liquidity becomes super inelastic, you have massive funding issues in capital markets.

Tony: The impact of Fed policy is more direct when money is tighter, so each time they raise the money supply, it contracts, and the impacts are more immediate for the market. I think all of this makes a lot of sense, but we all need to relearn this every cycle.

Tony: CI Futures is our subscription platform for global markets and economics. We forecast hundreds of assets across currencies, commodities, equity indices, and economics. We have new forecasts for currencies, commodities, and equity indices every Monday morning. We do new economic forecasts for 50 countries once a month within CI Futures, we show you our error rates. So every forecast every month, we give you the one and three-month error rates for our previous forecast. We also show you the top correlations and allow you to download charts and date. You can find out more or get a demo on completeintel.com. Thank you.

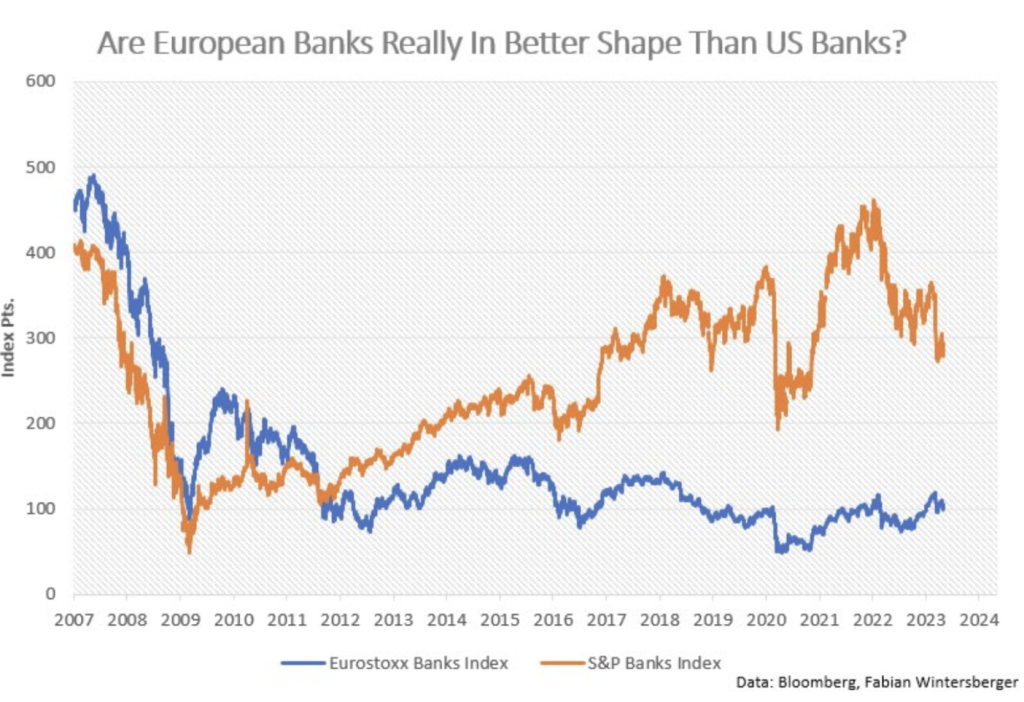

Tony: Let’s move on to Europe. And Fabian, Deer had a chart about five-year CDs in the US versus Europe, and you sent me a chart asking, “Are European banks really in better shape than US banks?” So can you talk us through that? And are you worried about more wreckage or distress in European banks?

Fabian: Not immediately. I think European supervision has been much better than in the US, and we didn’t deregulate financial markets as much. That doesn’t mean that some banks might have mismanaged interest rate risk. But I think the problem started, as we can see in the chart, during the GFC. European and US banks went down, but Europe’s banks never recovered. And that’s, in my opinion, because the ECB never raised interest rates. So banks had – and the bread and butter of banks is to lend money – and rates were so low, spread, and that’s exactly what you said. If interest rates are too low, then the banks think about real economic investments. They say, “Well, why should I lend money for two and a half percent if I just can put it into Treasuries and get one and a half or so, right?”

Tony: Or with negative interest rates, they’re punished for holding money. Right? It makes sense to me. And their profitability was razor-thin, so that makes a lot of sense. So can you help us? What is the ECB doing in terms of the banking crisis? We saw Madame Lagarde speak earlier this week. We saw a 25 basis point rise, and do you think that’s the right pace? And where do you think they’ll head next?

Fabian: Well, I was hoping for a 50 basis point increase because I thought it was justifiable, but I think she referred to the bank lending survey on why the ECB just raised by 25 basis points. And in the lending survey, you can see that drop in lending growth across the board. I think demand for corporate loans in the first quarter had the biggest drop since 2009. But, on the other hand, you have growing net income for the banks, and they had extremely good numbers in earnings, so I’m not quite sure if they took the correct path. Yields have dropped prior to the meeting, and so I thought they have the room to go for 50, and maybe then they could think about what to do next because now we just know for sure that there’s another 25 basis point hike coming, and I don’t know. I think the ECB is praying that inflation will drop similar to the US because otherwise, they are in a very tough spot. And I’m not so sure about that because if you think about why inflation is that high in the euro area, it’s because on the one hand, the ECB is tightening, and on the other hand, governments are handing out fiscal stimulus, fiscal stimulus, fiscal stimulus. You get price caps for energy, for consumers. Now, I think German Economic Minister Harbeck talks about price caps for German industries and who’s going to pay the bill? The government pays the bill. And if the government pays the bill, it’s you paying the bill.

Tony: I mean, if anybody has the budget, Germany has a budget for it, right?

Albert: This is exactly what we talked about a couple of weeks ago, where politicians have a short-term view of their political careers rather than sound economic policies.

Tony: Let’s be honest, it’s central banks and fiscal spending that got us here, right? And if you pay people to stay at home for two years, you have to turn around at some point. So, for all the slack time people had in their jobs and for all the slack that we had in the economy and in the fiscal environment for two years, the other side is extremely painful. Some people have been saying that for a while, but nobody really wanted to believe them. So, it’s a tough spot. Fabian, in Europe, are the local banks as stressed as some of the regional banks here in the US? Or is there a pretty uniform view of banks across Europe?

Fabian: It’s hard to say. I think currently the regional banks are in a good situation because the regulation works better than in the US. We have another positive thing, which is positive for the banks, of course, because I think you had it in the US, too. You had credit guarantees by the government. In Europe, they’re still in place in many countries, so they never lifted it. They’re handing out credit and the bank lends because they know they get the money anyway. If the data falls out, you get the money from the government. I think that may be helpful, that the banks will continue to lend. And basically, it’s exactly what Russell Naper talks about, I think, since 2020, that’s the way how to keep credit flowing and to keep inflation a bit higher so you can bring the debt to GDP ratio down.

Tony: We may have to do that in the US for a short period. I mean, I don’t know that there’s any other way around it without having some pretty hard lessons learned. So, I could be wrong, but it seems like we’re headed there at least for a temporary period. Okay, thanks for that, Fabian.

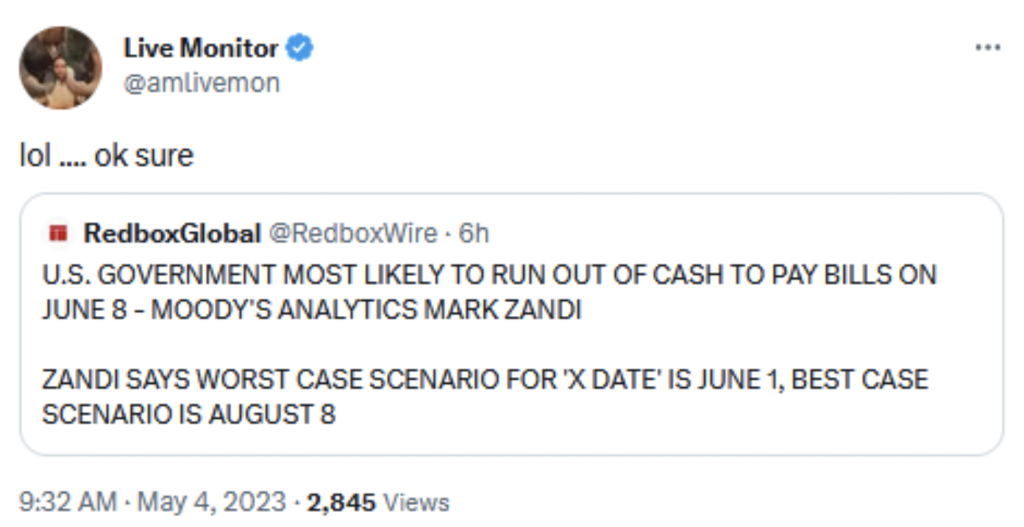

Let’s talk about the debt ceiling now. Everyone’s favorite topic, I guess, aside from banks. Albert, I know you’re all over this, and I know that you talk to folks on the Hill on a regular basis. You sent out this great tweet earlier this week. Mark Zandi, who’s at Moody, said the US is going to run out of cash on June 8th. And you said, ‘Lol. Okay, sure. Lol, okay, sure.’

So, the debt panic story started a couple of weeks ago, maybe a month ago. To be honest, to me, it feels like the same fake drama that we see every year. I think a lot of Americans are just cynical about the debt ceiling discussion. So now that it’s May, we keep hearing that the US government is going to run out of money by a certain date. From your perspective, do most Americans really care about that? We kind of have an antagonistic relationship with our government, right? So, on some level, most Americans just kind of shrug shoulders. What’s the thought, the popular opinion there?

Albert: Well, from the public’s point of view, they don’t care if the government shuts down. They want them to shut down and stop spending money. But for the markets, which is what we really care about, the debt ceiling is a bit of an issue. It’s an issue only because of the narratives that it provides for market movers. That’s the only issue because we’re not going to run out of money. It’s just not going to happen. Yellen is going to prioritize what she needs to, and the United States will be fine. The problem is pretty much in DC at the moment because the Republicans and Democrats are so far apart that I don’t see any kind of resolution happening before June 1, which is the theoretical deadline they have set. If McCarthy caves, he could be ousted as a GOP leader, which would cause a bigger problem because people don’t realize that if he’s ousted, there’s no process to get bills done until they find a new leader, which could take weeks or months.

Biden and the Democrats want a clean bill with infinite spending and zero restrictions, which is just outrageous, and it doesn’t even have a chance to get to that point in the Senate with Sinema and Mansion coming out against it just today. They don’t have 60 votes for that. I don’t think any Republicans would even go for a clean bill on the debt ceiling. So it’s something that we’re going to have to deal with because it’s going to be a scapegoat for the market, and we have to keep an eye on it at the moment just because of the narrative.

Tony: Right. For people who aren’t in the US, the House of Representatives has the power of the purse. So a lot of this budget stuff has to be approved by them. Kevin McCarthy has a delicate coalition in the Republican Party to stay in power, and if he doesn’t keep some of these budget hawks on his side, he will lose his seat. Someone will call a vote. He’ll get a vote of confidence. There will be no majority leader with the Republicans, and no legislation will come to the floor.

Albert: That’s right.

Tony: Then the legislative branch is deadlocked until somebody else comes, and it’ll be a very difficult fight to get something done. I think it’s important, Albert, to explain to people, especially outside of the US, the view of the debt ceiling from the people who are exasperated by DC versus the view of the debt ceiling from the markets, who deep down know this is going to be resolved, but play to the narrative just to get it done as quickly as possible. Will the US government actually run out of money? And I guess this is kind of a technical thing, but will US government employees go without pay? This is something that always comes up with a debt ceiling. Will the poor bureaucrats of the US government go without money?

Albert: Some will, for a short amount of time. It’s more of a political question because it depends on which workers go without pay. That’ll maximize the pain for the opposition. It could be teachers or someone in the government with vacation time coming up, but they’re not getting paid, technically. But no, the US government is not going to run out of money until about September anyway, so this whole June 1 thing is a bit silly.

Tony: So, the executive branch always cuts the most visible jobs, right? It’s the people that work at national parks during the tourist season, showing people around, so they have to close national parks and disrupt people’s vacations. It’s the people that work at the VA, so they can pull on heartstrings around healthcare. It’s those sorts of jobs that are being cut. But make no mistake, those people always receive their back pay even though they’re not working. They will always be compensated for the time that they were off. So nobody is going without money. It may be delayed, but nobody is going without money, health care or benefits. Right? So, these people are literally just taking time off.

Albert: Okay. Pretty much. So when we hear statements that say “the full faith and credit of the US government”, what does that mean?

Tony: Does that mean anything?

Albert: Not to me it doesn’t. I don’t know what they’re talking about. I mean it’s just PR jargon for them to push out agendas and narratives. That’s all it is to me.

Tony: Right. These are sympathetic words that people use to get emotions on their side. And so again, I think most people who hear this, for some reason it touches their heartstrings, but it really doesn’t mean a lot because everyone knows that the US government is going to pay their bills.

Albert: Of course.

Tony: How do you expect this to play out, first of all? And second of all, will anything change this time next year?

Albert: No. I mean the most likely scenario is they get a one-year funding deal with some spending cuts and probably leftover COVID money out there, which the Republicans have been trying to get rid of anyways. I mean, realistically, Biden is going to have to negotiate at some point. It’s just when, and I think it’ll probably be towards the end of May or early June, and you could have a little bit of drama for a week or two. But something will get done. It always gets done.

Tony: It always gets done, right. And my guess is it’ll go into the second or third week of June just to make it really painful for all of us. So we don’t want to reach anywhere.

Albert: Of course. And this is political season now because the primaries are starting to gear up, campaigning and whatnot. So Biden and the Democrats, and same thing with the Republicans, want to scapegoat things. If the market drops, they need a scapegoat. So that’s ceiling it is. Let’s see what party takes the brunt of it.

Tony: So, let’s look at the next week. We’ve seen a lot of banking-related events happen over the last week, and we saw Apple report its earnings which started out good, but then it wasn’t so good. What do you guys expect to happen in the markets in the US and Europe next week? Is it going to be more of the same, or are we on a downward trend? Will we see a change in sentiment when new data, such as today’s NFP, is released and if it’s higher than expected? Albert, why don’t you get us started?

Albert: Regarding the week ahead, for me, it’s all about what the market will price in for a pause versus a rate hike. Today’s numbers definitely show that another rate hike is likely coming. Aside from that, it’s the regional banks and how much pain they will go through over the next week and what the narratives will be around that. I don’t see a solution for that until Congress agrees to increase the FDIC limits from 500,000, which the GOP has no appetite for. So, I think the next few weeks will be challenging for regional banks, and we may see some ups and downs. You would expect a bit of a sell-off because this market is way overvalued, but with these tech earnings beating, who knows?

Tony: What are you seeing for the next week, Fabian?

Fabian: Especially in Europe, I see more of the same, probably with yields hedging lower a bit, because I think it started on Wednesday with Powell’s speech this week. I don’t think the market believes any of the ‘higher for longer’ talk. If you look at Fed history, it’s probably justified, especially in a high inflation environment. I read that in environments with high inflation, the Fed typically cuts the next month after they reach the peak, and in a low-interest-rate environment, it is usually four months. I actually wrote about this in my report today. I don’t think Powell is done yet. I checked the Fed watch tool, and I think the probability of a pause was around 99%. But that will likely go down over the next month, as I think Powell was really hawkish during the press conference. He talked about excessive demand and wages, and what I liked was that he said wages do not cause inflation. I think that is correct, and you usually see wage gains at the end of the expansion as profit margins drop, and workers get a higher share until businesses say, ‘we can’t afford it, you buy it.’ It’s interesting, and that is where we are heading, but it will take time.

I wrote about that in my submission today, that I don’t think Powell is done yet. Right, I checked the Fed watch tool, and I think the probability of a pause was around 99%.

Tony: That probability will go down over the next month.

Fabian: I think so too because I listened to the press conference, and he was really hawkish. I didn’t expect him to be that hawkish. He always talked about excessive demand, excessive demand wages. What I liked about it is that he said that wages do not cause inflation because I think that is correct. You see wage gains at the end of the expansion as profit margins drop and workers get a higher share until businesses say, ‘We can’t afford it. You buy it.’ Interesting. That is where we are heading. But it will take time.

Tony: It always takes time for markets to observe that. And Deer, what do you expect in markets over the next week? Do you expect the banking situation to continue to worsen, or do you think that things will stabilize after a couple of days?

Deer: I’m hoping that things stabilize. I’m not sure if you saw Hugh Henry’s interview with Bloomberg, but I actually think that he posed a very important question, and it’s the only way to stop deposit outflows. Does the federal government come in and do like what they do with hedge funds, where they essentially lock in money and say, ‘You can’t withdraw your money,’ or if you want to withdraw your money, you have to wait three months or six months, or kind of we’ll call you back. So I actually think that’s a very interesting question because at least with AIG, there was something that the government could do. They could come in and backstop the MBS market. What do you do to stop deposit flight? I think the real question, and I think the only way to do that, is by putting some sort of cap on the ability to pull deposits. But then at that point…I wouldn’t say nationalizing the banking industry, but at that point, you’re putting massive oversight if you’re telling people you can’t withdraw your money, right?

Tony: Look, it’s a temporary backstop, and that’s what the Fed was designed to do, right? I mean, the Fed was designed to be a backstop for monetary policy and banks. I mean, I could be wrong, but that’s my general understanding.

Deer: Well, that’s the thing, and I’m relatively optimistic. I watched your interview with Bob, and I know that they were talking about some banks in South Carolina. Obviously, that’s my home state, and there’s one bank there that’s extremely well run. I mean, quarter over quarter, I think deposit growth has been about 10%. They are extremely conservative in terms of lending practices and it’s been kind of unnecessarily targeted because of everything that’s happening. So I look at the regional banking sector and I remain somewhat optimistic. But I do think in the next couple of weeks there could still kind of continue to be some pain, and I think some banks are going to continue to kind of be in the crosshairs of people within financial markets.

Tony: And going back to Hughes’ interview, I did watch it. He had me until he said that crypto is really the only way out of this. Tell me what you think about that. Is crypto the solution to this? Sorry, I know people are going to hate me.

Deer: No, for me, absolutely not. But I don’t want to say I’m a Fiat maxi, but I think the Fiat system works relatively well. But at least with what we have, there’s no way that we go back to a gold standard. And I think that there’s even less of a chance that we get to a crypto standard. But…

Fabian: That’s clear because governments can’t load up on debt, but they want to load up on debt. They want to spend money, they want to buy votes. That’s right, because that’s how politics works. You buy votes. Therefore, I think it’s in the nature of a fractional reserve banking that if there’s panic, then it doesn’t matter how good the banks capitalize because there’s not enough around. I think now the problem is way too big, and if something happens on a huge scale, then you got no other chance than to bail out the banks, bail out all of them, and just flush them with money. You may unleash an extreme wave of inflation then, but that’s the only thing to do. Because the system, if it had been about 60, 70 years ago, and you said, if you do bad management, then we let you fail, probably banks wouldn’t have lent out so much compared to their assets. But they did, and they learned that they will get bailed out anytime something happens.

Tony: And we set some bad precedent in 2008 and nine. Right, it’s very hard to unlearn those. And at this point, should people today be punished for the bad precedent that was set in 2008? I actually don’t know the answer to that. Right, it’s really hard. In general, is it fair to say, and I know Albert had to go, and I appreciate him coming on, but in general, do you guys believe there will be some intervention by the Fed and the Treasury to stabilize the regional banking environment, even if it takes an act of Congress to do so? Dear, what do you think about that?

Deer: Sorry, I missed that. My Internet got kind of glitchy. Just repeat it.

Tony: So in general, just in terms of the weeks ahead, maybe not the week ahead, is it fair to say you believe that there will be some sort of intervention in this regional banking issue to stabilize a regional banking environment, even if it takes an act of Congress, which is actually what would be required to reenact the 2008-2009 solution we had to backstop the banks?

Deer: I think at some point they have to. It’s kind of ironic because Powell came out last week and said the banking sector is fine, and then fast forward to this week, everything’s in chaos. I think that if you’re the Fed, you have to start. I’ve used this example a lot because people are like, “SVB isn’t that big, or FRC isn’t that big.” But we’re looking at that in the American context. There are six large banks in Canada. If you took the three largest or like the three smallest of the banks, Regions, which is based in Birmingham, Alabama, is larger than all of them. What we consider a regional bank for many nations is like large banks. So what I worry about is if they don’t backstop this and this continues to happen, what does the United States do where roughly 70% of GDP is foreign direct investment inflows? Foreign direct investment inflows as a percent of GDP are about 70%, where if you look back almost a decade, it was like maybe 20 or 30. I don’t have the data, but it’s gotten drastically larger.

And so how do we protect that foreign direct investment when people look towards us and say, “This is a nation that has relatively good rules and regulations in place to protect investor money,” and now you look at the Fed who’s just kind of saying, “We’re just going to let this dumpster fire run wild”? What does that mean for the United States from an outflow perspective as well? If they don’t do something, this obviously has spillover effects. It can no longer stay contained in the United States. So I think that’s where they do have to, where Congress has to come together. What always makes me laugh about that whole thing is even if you went back to the Trump administration, the Democrats were saying, “No, we need 2 trillion,” and the Republicans were saying, “We need 1 trillion.” But when you’re talking about the difference between 1 trillion and 2 trillion, is it really all that important? We’re still talking about tremendous amounts of money, right? 2 trillion for one party, 1 trillion for the other.

It’s just like, I think that’s where they’re just getting into gridlock to get in gridlock. But I think now if we look at what we have to do, making sure that we support these banks that provide funding to the backbone of America is extremely important. And I’ll kind of land it here. If we talk about productive capacity and real economic investments, that’s what a lot of these regional banks do. If you’re a farmer in Nebraska, you can’t go to JPMorgan because if you send off a loan application and it goes to some guy at JPMorgan, he’s going to be like, “A farmer in Nebraska? Who cares?” But that’s where a lot of those regional banks provide that extremely important funding to that backbone. That actually increases total factor productivity. I know total factor productivity from the economic standpoint is a bit nuanced. Some people don’t like it as a measure.

But that’s where a lot of those regional banks provide that extremely important funding to that backbone. That actually is what I would say. Increases total factor productivity. Increases. And I know total factor productivity from the economic standpoint is a bit nuanced. Some people don’t like it as a measure.

Fabian: It’s the same thing in Germany and Austria. We have a lot of regional banks, and I think there are studies that show this is a main cause that we have. I think the US has many hidden champions who, because they get funding from the regional banks and get treated like stars.

Tony: This incremental loan or business opportunity is big for them. It wouldn’t be for a globally systemic bank. This is great. Thank you so much for this. Let me end this on this. I’m old enough to remember when the $780,000,000,000 Tarp program was the largest program ever put out. Now we’re throwing around a trillion here, a trillion there, right. It’s just really strange to see where 15 years go and what happens over that time. This has been hugely valuable. You guys have heard a lot of my thoughts about banks and a lot of my questions. Thanks so much for your time. I really, really appreciate it. Have a great weekend and a great week ahead. Thank you.

Fabian: Thank you. You too.