Explore your CI Futures options: https://completeintel.com/futures

This Week Ahead is joined by Bob Elliott, CIO at Unlimited Funds, Sam Rines from Corbu, and Josh Young from Bison Interests. In this episode, we delve into three crucial themes – Higher for Longer (H4L), Earnings, and Refining Margins – with a focus on stocks like $FRB, $META, $MSFT, $AMZN, $KMB, $XOM, $NOV, and $VLO.

Bob Elliott kicks off the discussion on H4L, sharing his insights on the current stocks versus bonds situation under this environment. Despite little progress from the Fed, he notes that equities signal a different outcome from bonds, which indicates an impending recession.

The panel then engages in a deep dive, discussing the possibility of the Fed relenting on inflation, the duration of the H4L phenomenon, and the role of the labor market in shaping its trajectory.

Sam Rines then shifts the focus to Earnings, highlighting key trends in the First Republic and Kimberly Clark stocks, including a decline in Price Over Volume. The panel also touches on the tech industry, analyzing its current position and outlook.

Finally, Josh Young explores the intriguing topic of Refining Margins, with a particular focus on the US and China dynamics that have contributed to Valero’s strong earnings report. Josh examines the significant drop in refining margins in recent months, assessing how the trend fits into the historical context of this industry.

Key themes:

1. Higher for Longer (H4L)

2. Earnings

3. Refining margins down, but strong demand

This is the 63rd episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

Bob: https://twitter.com/BobEUnlimited

Sam: https://twitter.com/SamuelRines

Josh: https://twitter.com/Josh_Young_1

Transcript

Tony

Hi, everyone, and welcome to the Week Ahead. I’m Tony Nash. Today we’re joined by Bob Elliott from Unlimited Funds. We’ve also got Sam Rines from Corbu and Josh Young from Bison Interest.

Tony

We’ve seen a lot of activity in markets this week and it’s been honestly, some of it really surprising. So we’re going to talk through some key themes. The first one is higher for longer. Bob’s talked about this quite a bit, and in light of some of this week’s events, I think there’s really a lot to talk about there. With Sam, we’re going to talk through earnings. He’s done some great discussion of earnings in his newsletter. So I want to talk through some earnings with Sam and then we’ll talk about energy with Josh. And so part of it is refining margins, but part of it also is what are some of those energy earnings look like? So, guys, thanks so much. I know it’s Friday. I know it’s been a busy week, so I really appreciate the time that you’ve taken for this.

Tony

So, Bob, this week you put out a tweet about kind of stocks being kind of greater than bonds in a higher for longer environment.

And so I’d like to talk through that a little bit. You’ve also said several times that the Fed hasn’t made much progress in light of some of the recent data. And we also saw Japan overnight with some of their inflation data, which really surprised to the upside, and that puts the BOJ in a difficult position as well. So can you talk us through some of your thoughts around higher for longer and the position that some of these central banks are in right now?

Bob

Yeah, I think it’s been an important week in getting incremental information and understanding how the economy, the US economy in particular, is playing out. I think the GDP report there were already signs in this direction. But we basically had a confirmation that if you look at nominal final sales, which really describes the underlying nominal demand in the economy that was growing at seven and a half percent annualized rate in the first quarter in acceleration from the downtick that we saw in the fourth quarter of last year. And that, to be frank, seven and a half percent nominal growth is where the US economy has been roughly for the last two years. And so I think what this is speaking to is the fact that there is a lot of nominal spending and nominal growth momentum in the economy, in the US economy that really has not the Fed has obviously started to take steps and has tightened significantly. But if you think about how much progress have they actually made, given the fact that nominal growth continues to persist in the way that it is, they haven’t made a whole heck of a lot of progress.

Bob

And I think it’s important to connect that to the underlying capacity of the economy. Many people if we look at the last cycles that we were familiar with, overall capacity growth in the economy was more like two or 3%, right? Because you had labor force expansion and you had higher rates of productivity. Today capacity growth is something like 1.5%. And so if you take seven and a half percent nominal growth at 1.5% capacity growth, the difference between those two things either has to be inflation or has to be a tightening of capacity. And we’re already running at very tight capacity across much of the economy, particularly the services sector. And so that’s just translating to higher prices that continue to persist above the Fed’s target. And then there’s some details under the hood on that, but I think that’s the basic picture. And so if you compare that, for instance, to what’s priced into the short rate market, the short rate market is pricing a return to 300 basis points over the course of the next 18 months. Like, okay, given the short rate market is basically saying we’re going to have an almost instantaneous significant recession based upon what’s happened, and that’s really possible, maybe we get a total banking meltdown, maybe we get something else that occurs as a shock to the economy.

Bob

But certainly it wouldn’t be my median case that we’re going to see an economic slowdown over the course of the next 15 or 18 months that’s aligned with moving the given where we are today, given the momentum, we’re seeing. Given that set of circumstances, we’re not probably going to see it’s a low probability that it would be appropriate for the Fed to bring interest rates down to 3% over that time frame.

Sam

And I can’t agree with this more. And sorry, I’m going to jump in and please, I saw you about to talk, Tony, so sorry, but I’m going to jump in because I don’t think this can be emphasized enough. And to Bob’s point on the slowdown, I mean, think about what the airlines are telling us. Think about what the cruise lines are telling us. Restaurants, when you have Pepsi and Coca Cola raising prices like they’re raising prices, the consumer is not dead in any way. I mean, middle America is going on carnival cruises like they’re going out of style. And these aren’t bookings for the last quarter. These are forward looking. I mean, Hilton’s booked up. So to the point on, we can kind of differentiate between do we have enough capacity and goods. I think we have enough capacity there. But on the services front, you don’t have enough capacity on labor, you don’t have enough capacity to handle the vacations people want to go on, never mind last summer. This summer. And so this is a persistent thing that we have seen.

Sam

Remember we were having a similar discussion last summer about possible recession in the fall of last year, and we were going to fall off cliff. Fed was going to pause. Fed was going to cut. We argued about that on here and I was pretty adamant that that was not happening and the Fed was going higher. But it’s very difficult to see where this economic slowdown is going to happen when people have basically pre spent away a recession. I can’t agree enough on that one.

Tony

Yeah, go ahead, Josh. And I know that talk of no recession has you salivating on crude prices.

Josh

Yeah, I guess it sounds good. And there are certain aspects of what Bob saying and Sam saying that resonate. But there are other data points and there’s other perspectives. So Capital One, I think it was this morning, they came out with a sort of negative guide and indicating that they’re seeing more charge offs with a view of even more charge offs coming soon. Or I guess it’s delinquencies that are leading that they expect to lead to significant charge offs. And historically Capital One has been sort of a leading indicator. They come in well ahead of Amex or some of the other credit providers just because they’re sort of in the lower to mid end of the market. And then when you look at oil and oil products consumption, it’s pretty soft. And contrary to the EIA report this past week, when you look at the Gas Buddy stats or some of the other sort of more real time, more accurate stuff than the government reports, it’s not. There’s a different I know the services aspect of the economy is strong and the goods aspect is weak. But there’s some and you look at things like lumber prices which are indicative of sort of housing construction activity being very weak.

Josh

And so there’s these sort of, I think, chinks in the armor of this narrative around the economy being strong that maybe they’re too forward looking, but I just don’t honestly, I would like to be more bullish because it would be better for oil. I think oil goes up anyway. But I’m very curious about your guys take specifically on this Capital One report.

Ad

With CI Futures, you can access AI-powered market forecasting for as low as $20 a month. Get 94.7% market forecast accuracy for over 1000 assets across commodities, currencies, equity indices, economics and stocks. With weekly updates, one-month and three-month error rates, and top ten and bottom correlations, you can rely on CI futures to help you make informed decisions. Join a growing number of satisfied users who have already transformed the way they invest with CI futures. Don’t wait. Start forecasting with confidence today for as low as $20 a month.

Tony

I think. Josh, on the housing, it’s interesting the housing stuff is slowing, but housing wages and construction wages have been pretty strong. And so I think we’re getting some mixed messages there. And this goes into Sam’s discussion about kind of a gracklish Fed or a lot of kind of contracting discussions about the economy. Right. We don’t necessarily have consensus on where things are going and that’s what I find so interesting about right now because honestly, by now I thought we would start to see a slowdown, a significant slowdown in inflation, a significant slowdown. This quarter was supposed to be a pretty negative quarter for earnings and we’re down two something percent or something off of really great earnings last year. So Sam, go ahead. I’m sorry, I just wanted to interject that.

Sam

No, my only comment there would be mostly centered around the fact that we are in a freight recession because nobody’s buying goods because we bought them all while we were sitting on our couch during COVID, right. We’re in the call it the down cycle of an inventory cycle across the board. Right. You hear that from JB Hunt. You hear from all the majors. That’s a pretty energy, particularly oil and gas, gasoline, diesel, that’s very intensive on that front. So when you have a slowdown there, you’re naturally going to have a slowdown in the consumption numbers.

Sam

But I would also point out that where you’re really seeing the upticks are in aviation fuel. Right? You’re not seeing any weakness in demand for aviation fuel. You’re not seeing any weakness, particularly in the US. And parts of Europe. You’re not seeing any weakness on that front. So it’s really kind of pick your poison if you want to look at what’s going on with gasoline. Nobody’s on spring break right now. We’re all waiting for our kids to get out of school before we go on summer vacations. Right. I would be very tentative on looking at the weakness in certain aspects of the energy space right now and look at where we know the demand is if aviation fuel began to fall off a cliff, I would be very concerned. Right. But it’s more than likely going to be because Southwest had to cancel a bunch of flights again. So again, it’s probably going to be noise in the system.

Tony

Yeah, that’s fair. So, Bob, go ahead.

Bob

Yeah, I think in a typical macro cycle, there’s always indications of leading aspects that point to recession in the future. And to be clear, there will be a recession. It’ll probably be worse than most people think. But the question is when and if it happens. I mean, for instance, the median consensus coming into the first quarter of the year was that we were going to have zero growth, essentially a shift towards recession. That was the median consensus expectation. And instead we had essentially the strongest nominal growth that we’ve had over the course of several years. And so I think the question is basically, yes, there are some indications. There are always those indications, but how fast, how indicative are they of us getting to a point where the macro cycle is meaningfully turning over?

Bob

As an example, simple example, like the typical lead time between the slowing, the shift from construction employment growth going negative to aggregate employment growth going negative is 18 months. Okay. Well, 18 months in the life of a person who’s trading markets on a weeks or months time frame is an eternity. Right? And so I think when you look at the market and you look at what people are saying, there’s lots of people who are making first order simple points about this leads, this leads that. Totally right. And the challenge is it’s like, hard to disagree with that.

Bob

It’s absolutely true that the yield curve leads to leads recessions. Totally true. But it can be between yield curve inversion leads to recessions, but that can happen with a lead time of nine months or 28 months. Okay, well, that’s a big difference. And it’s particularly important in this environment where that difference in time emphasizes the race that the Fed is in. The Fed is in a race to slow down the economy fast enough before inflation becomes entrenched. That’s the race. Right? And so if it takes that 28 months for the Fed to finally slow down the economy and inflation is persistent through that period, then we have a risk of entrenchment. And that’s actually when I put out just before we got on the phone here.

Bob

When I look at the underlying indications of what’s going on with the inflationary picture, there are real signs of entrenchment in this economy across the sort of stickiest parts. Not just housing, which of course, is like elevated and overstated and lagging. But I’m talking about like core services, ex housing. Those prices are rising meaningfully faster than they were pre COVID and are not showing any signs of slowing. That sort of sticky entrenchment is a very concerning aspect for the Fed.

Sam

Kind of jumping in on that. It’s one point data point. But when you look at what Cracker Barrel was saying about what they were going to do this year, and it’s my favorite example because it’s middle America, you don’t get more middle America than Cracker Barrel when it comes to a restaurant. They were saying wages are going to rise five to 6% and we’re going to raise our prices, I believe it was six to percent, seven just above that. And that’s for the year. So it’s not as though companies are anticipating that they’re going to get some sort of break on inflation and wage pressures. And that services. If you want to go have your sausage and biscuits, it’s going to be more expensive. And frankly, middle America is going to feel good because they’re getting a pay raise.

Sam

And on top of that, a lot of Middle America got a 9% pay raise on Social Security. So they’re feeling really good about themselves. And that is very high powered money going into the system. Social Security doesn’t get saved, it gets spent. So it is going to be a really interesting dynamic because the demand for services is not declining and the labor pool is not increasing anywhere near fast enough. And those wages are either going to have to continue to creep higher to pull more people in, or you’re going to have to creep prices higher to destroy some of that incremental demand. And that’s where I think it gets really intriguing, where you could have a significant amount of stickiness simply because businesses themselves are trying to be able to adjust a weaker labor outlook with very strong services demand.

Tony

So guys, I keep hearing kind of economists say that the data the Fed is looking at is lagged, and so they’re looking at data that isn’t relevant to today and so on and so forth, and that the Fed has gone too fast and all this other stuff. So I hear that, and I’m the first guy on every government data point to say, wait for the revision, right? So of course it’s lagged. Of course these are all preliminary data that we’re seeing released. But when you hear somebody say the data the Fed is looking at is lagged and they’ve really done too much too quickly, what’s your response to that in terms of, okay, it’s lagged? We just need to accept that. But the Fed has always made decisions on lagged data. So is there anything else to that statement?

Bob

Well, I think the Fed I like to call the fact that the Fed looks at lagged information as both a feature and a bug. Right? It’s a bug because inevitably their behaviors will exacerbate or be overreaching on being too tight at the top of cycles and overreaching on being too easy on the bottom of cycles because they’re looking at backward looking data. I think it’s important to recognize, though, that that reaction function has, if anything, gotten tighter to looking at backward looking data rather than forward looking data as a result of their experience over the last three years. Because Fed made a bet. Fed made a big, terrible bet on the fact that inflation would be transitory. And that was a forward looking bet driven by what the staff believed at the time. The governors, following the staff’s advice, bet on transitory inflation. They were painfully wrong. And the reason why they’re in this circumstance is as a result of making that bet. So if anything, what that does is that brings their attention back to they should be focused on looking at the data that they actually see and responding to the data that they actually see.

Bob

And so whether or not you like it, whether or not you think it’s the perfect way to manage monetary policy, it doesn’t matter. How you think they should manage monetary policy is of no relevance to trading financial markets. How they actually manage monetary policy is perfectly relevant. And when you look at that, that’s why I keep going back to the data. The Fed has woken up today, has opened their book and said, nominal real final sale 7.5% annualized. Holy shit. Unemployment 3.5%. Holy shit. Okay, when they look at that services, X housing, PCE services, X Housing 5% and rising in recent quarters. They don’t have a choice in terms of what their decisions are. They have to continue the path forward.

Sam

To this point, and I think this is extraordinarily relevant in the face of a banking crisis that was heavily blamed on them raising interest rates so quickly. When they released the minutes, it was obvious they did not care. It wasn’t even a debate, really, as to whether or not they were going to go 25 and be pretty hawkish about the future. It was mostly like, yeah, we’ll do that. Even though the staff. The staff had this strange, like, we’re going to go into a recession, blah, blah, blah, and it was all over the place. On the staff front, the actual voting participants did not care. They were like, whatever. Banking. Yeah, we solved that with BTFP. Moving on.

Bob

My favorite thing about the minutes the minutes were seven pages and the word inflation appeared 100 times. Imagine writing a seven-page document where one word exists 100 times over 100 times. So if you want to know what is the Fed worried about, it’s the thing that they’ve mentioned an obscenely frequent number of times over the course of their papers.

Sam

If I had an editor and I had put inflation 100 times in seven pages, they would just absolutely destroy me. Just to be clear. At least I would say “prices increasing,” or you’d have to come up with at least some other way of saying it. Yes.

Tony

CI Futures is our subscription platform for global markets and economics. We forecast hundreds of assets across currencies, commodities, equity indices and economics. We have new forecasts for currencies, commodities and equity indices every Monday morning. We do new economics forecasts for 50 countries once a month. Within CI Futures, we show you our error rates. So every forecast every month, we give you the one- and three-month error rates for our previous forecast. We also show you the top correlations and allow you to download charts and data. You can find out more or get a demo on completeintel.com. Thank you.

Tony

I actually heard Mohamed Al-Arian say this morning that the Fed is overly data-dependent, which just sounded a little weird to me, but he actually said that. I think we’re at a point where certain people are advocating for a looser Fed, even though nominal is very high, and it’s just we’re in this very strange place where people just aren’t sure about this. Josh, were you going to jump in?

Josh

So I think one of the things that sort of the bridge between sort of expectations and sort of where this conversation has been so far is that there are things that we know that have happened in between the backward-looking data that the Fed is obviously heavily reliant on. And what we’re seeing sort of today and sort of what we know is happening over the next few months. So, for example, the giant wave of multifamily housing that’s crashing onto the market as rents are starting to roll, especially in major metropolitan areas, I mean, you sort of know that the owner’s equivalent rent is about to roll hard, and so it’s not unknown. And the Fed, they’ll indicate that they’re sort of watching these things, even though I agree with Bob, I think ultimately, and Mohamed Al-Arian and others, that they’re just really looking at the actual data that they’re getting. But you sort of know over the next few months, I think even that you’re going to start to see pretty negative moves which could offset some of the wage inflation and other issues. And so, I don’t know, I feel like I was sort of in the inflation is not transitory camp.

Josh

And it does look like we’re really I mean, I think we could see a situation with higher oil prices we can talk about later and lower inflation as this progresses, especially knowing the nature of the labor market and how important these jobs are for finishing up the 50 or 100 giant multifamily complexes here in Houston and every other major city. So you sort of know where it’s going. And it’s just a question of, like, how do they rearrange the chairs before they drop rates by like, 300 basis points over a four or five-month period when they realize how things have gotten.

Sam

So what’s interesting is, in that case, all of a sudden you have ripping real earnings, like real wages go through the roof if you have negative month-over-month headline inflation prints. All of a sudden the story is going to be real wages are going through the roof. Everybody’s going out and spending those real wages on things like services. And so it almost reinforces the decline in all the other stuff, almost reinforces the services argument going forward.

Josh

Everyone who has jobs still is going out and spending it a lot. And the problem is there’s also this role from high-paying jobs to low-paying jobs. The losses are on the high-paying side, the gains are on the low paying side. So it’s wonderful, right? Like the Chipotle worker is getting $20 an hour instead of 15, I think is actually very the Fed is very worried about it. I’m very excited about it. And there was one term that I think is worth mentioning that I read, I think it was yesterday, food as a service, since you were mentioning Cracker Barrel where they need to fast. It’s sort of the new outperformers of the restaurants, the Chipotle’s and the Cracker Barrels.

Sam

Exactly. No, it’s a good one.

Tony

Burrito company valued at $65 billion. So they’ve got to find some new term to justify that. One last thing on this topic, Bob, is you mentioned this very briefly, and I just want to circle back to this just to make it clear to viewers. We have bonds pricing in a recession. We have equities saying kind of the opposite, at least in certain segments. So what is happening? And Josh has brought up some kind of recession tailwinds or something into the conversation as well. So why are we seeing bonds tell us one story and equities tell us another story? What do bonds kind of know or think they know that equities don’t?

Bob

Well, I’m not sure one market knows anything more than the other markets. The price…

Tony

There’s an assumption always that bonds are smarter or not always. I mean, like a lot of people.

Bob

How bonds done this in the past 15 months, right? The bond traders have been, frankly the worst traders in the world. So if you look at what’s transpired relative to expectations, or at least the long bond traders is maybe the right way to say that. So I wouldn’t just assume that the bond traders have any idea what’s going on, if anything. I see, and it reminds me very much of 2011. And in 2011 we were coming out of the bottom of the financial crisis. At the time, in my seat at Bridgewater, I was talking a lot about how the economy was experiencing not a typical rebound because of the deleverage, the banking problems and the overall deleveraging in both the household and the corporate sector. Yet what was being priced into the bond market was a normal cyclical recovery, hundreds of basis points of tightening on relatively short order in 2011. And the bond market was totally wrong. In fact, it was arguably one of the best trades in the last 15 years was that bond trade, just fading what the bond market was thinking. And what they were doing was they were based on the pricing, was based upon the experience prior to the financial crisis and how cycles were.

Bob

And what we’re seeing today is a lot. What’s being priced in the bond market is based upon the experience of bond traders expecting the Fed to be highly responsive to a growth slowdown. When inflation is 5% persistently, and across the economy, the Fed’s reaction function is totally different than when inflation is one and a half percent in the economy. That’s all there is to it. And you have to recognize that. And I think what’s happening is the bond market is just not recognizing that. And the flip side, the equity market probably is too positive about how this is all going to play out as well. And so it’s certainly possible that both could be wrong, that the equity market could be a little too positive and the bond market could be too bearish. Last thing I’d say is probably about of all those things, probably the one with the best skew is what’s going on in the commodities markets for a variety of reasons. Skew in terms of upside skew and the risk return profile of going long commodities given the set of macro circumstances. But I’ll leave the particulars of that to Josh because he knows a lot more about it than I.

Tony

Okay, I think, Bob, we’re going to put that in quotes where you say, bond traders are the worst traders in the world.

Sam

Don’t do that.

Bob

I get it. They’ll be on my Twitter with pitchforks.

Tony

Yeah, they will.

Bob

They’ve been the worst traders in the world over the last 15 months. That’s it.

Tony

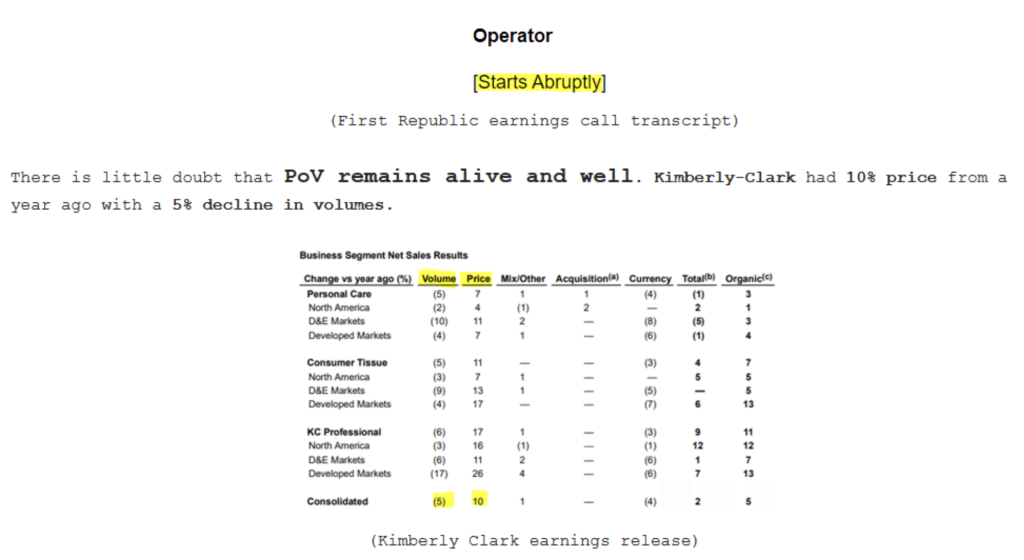

Perfect. So let’s move on to earnings. Sam, obviously a lot of earnings stuff over the past week. Really interesting. And from your newsletter, I thought it was hilarious when you talked about the First Republic earnings call, and the only thing you said was the quote from the transcript that says, starts abruptly.

So can you talk to us a little bit about First Republic? And it just seems like a case of a lot of really bad communication. What’s the big takeaway there.

Sam

It’s really bad communication tied with a horribly run bank, tied with rising interest rates. I mean, it’s that simple. It was horribly run. I don’t even know how to describe how poorly that was run. I mean, maybe Silicon Valley Bank was worse, but this one after this latest call, is just nuts. You read through that thing and it’s just crazy. The transcript goes starts abruptly, and then at the end it’s just no Q and A. What is going on here? Like, you at least have to have some Q and A if you want to survive as a penny stock bank. It’s that simple.

Tony

It’s easy to be in a management team when times are good. This is where we see where management teams earn their stripes. And you’ve talked about earnings from some regional banks in California and South Carolina and other places who seem to have come through this much better.

Sam

Yes, there are lots of banks that actually came through this with better deposits than people were anticipating. Don’t have a lot of CRE and office on the books. A lot of banks are getting beaten up here that are probably worth picking through at this point. It’s probably too early to really do it because it’s still top of mind, but there should be some shopping lists out there for when you begin to have some capitulation in the narrative around banking stress, et cetera. Because there’s some great banks that simply don’t have the problems and won’t have the problems that Silicon Valley, SI, Signature Bank, that First Republic does. So I think it’s very much time to build the shopping list, not necessarily time to go grocery shopping, but when it comes to the other earnings, you look at the staples companies revenue lines, and they’re absolutely stunning. You start with Procter and Gamble, Kimberly Clark raising price, don’t care about volume. The elasticities are perfectly fine. Going back a little bit further is ConAgra Hunt’s Ketchup absolutely crushing it price over volume. Kraft Heinz, obviously the other ketchup that we use, absolutely crushing on pricing over volume.

Tony

And then you go to McDonald’s and you have to really dig through their report to figure it out. But they put up a 12.6% same store sales number in the US. Which granted, on a year over year basis, helped a little bit by Omicron. But when you dig through it, it was 8.4%, give or take, price. They broke it down one third, two thirds, which is annoying on the call, but they kind of slipped up on that one. They never give you that breakdown. But it was eight plus percent pricing at McDonald’s.

Tony

So these revenue lines are pretty spectacular across the consumer facing companies. Hilton with very, very good RevPAR numbers. RevPAR is simply Occupancy and the average daily rate, in other words, how much you pay for the hotel room multiplied together. I mean, absolutely stunning there across the entirety of their portfolio. So it’s really interesting when you dig into the consumer facing revenue lines, right? Margins are still a little call it squeezed from a combination of labor and input costs. But overall, I mean, the revenue numbers are absolutely stellar. When they get to the other side of some of these input cost increases, those margins are going to be absolutely spectacular because those prices aren’t coming down anytime soon.

Sam

So I think it’s really worth watching some of those boring companies that people overlook a lot, that maybe at the end of this whole ripple out of COVID we had the COVID wave, now we have a whole bunch of ripples after this ripple. It may be that the boring companies all of a sudden have much higher structural margins than people anticipate, and I don’t think there’s a recognition of that in the system yet, not to mention the tech companies.

Tony

Hold on. Let’s talk about tech in just a second. I’ve said this a couple of times on the show, but Sam, you’ve nailed the price of our volume thing for ten months now, and you were, as far as I know, the first person out there to call this in consumer staples. And so I think it’s fair to take a victory lap here. You’re a pretty humble guy, but this is something that you’ve really called and really nailed from the very start. And these very boring companies that people a year ago just weren’t even considering have really shown persistent margins through the COVID ripples, which has been pretty amazing.

Sam

And I will say that there is a general tone that the pricing is going to slow through this year.

Tony

Talk about that a little bit. You talk about the slow fade of price over volume. Can you talk about that a little bit?

Sam

Sure. So it’s mostly that companies have taken a lot of price over the past couple of years. My favorite example is Wingstop. That company took a lot of price, saw its wing prices collapse, and then was like, oh, great, margins. We like these. They’re not moving their pricing down at all, but they’re also kind of back to quote unquote, their system, which is two to 3% price increases per year. Right. So you’re kind of beginning to see some companies begin to move back down. Kimberly Clark pushed price in the first quarter, and it’s unclear whether they’ll do it again later this year. But you’re beginning to see more of a normalization or close to a normalization in the go forward price push. That doesn’t mean pricing is coming out of the system. That means you’re going to be closer to the three to 4% type numbers that they’re seeing as their input cost increases. Right. Prices going back to covering basically only the increase in cost, not kind of adding to margin from here. So I would say it’s a slow fade towards that three to 4% type pricing algorithm.

Sam

But that’s going to take through the rest of this year. And we have yet to see any companies really beginning to talk about not pushing price. To be clear and back to the kind of the housing conversation that we were having earlier, you have to really back into it. But the pricing at Sherwin Williams was somewhere in the low double digits paint in a housing downturn. Whatever they were pushing, give or take, 12% price, that was where all of their revenues came from. It was nuts.

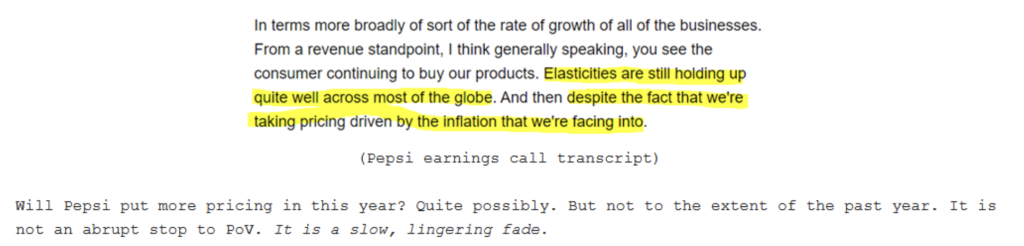

Bob

I wonder how much in terms of that forward guidance is a reflection of the fact that you can’t really come out and say publicly on your earnings call, hey, you know what? If you’re McDonald’s, like, hey, you know what? The people who buy our product have great income growth, and we’re going to just keep raising prices until we start to see a meaningful demand destruction dynamic going on.

Sam

But this is the funny part. They talk about elasticities are still good, and you’re like, okay, that’s code for and we’re pushing it.

Bob

Right. My guess, and this is it makes sense if you were sitting in their shoes, what would you do? You’d keep trying to push, given the fact that there’s such tightness on the production side. When I say production, I mean McDonald’s is really labor. There are obviously other input costs, but labor is a big part of their input costs. And so if that is constrained at some point and so in many ways, what you can do in order to continue to reflect that high nominal demand is just keep pushing the price incrementally up, up, up to see, as you say, if those elasticities start to deteriorate. And my guess as all these things that you’re describing is like, there’s no problem with the elasticity yet.

Sam

Yeah, one of the craziest parts is you’ve seen very consistent, call it low double digit pricing on a year over year basis for the last 18, give or take months from Coca Cola, and their volumes have been positive. And so if you’re Coca Cola, you’re sitting there saying, well, I can raise price and still have positive volumes. Okay. Keurig Dr Pepper, you look at their report, which is shocking because Snapple, whatever, and Dr. Pepper cool. They’re doing the exact same thing. And their elasticities, they’re beginning to see some deterioration in demand, but not much. So to your point, it’s difficult to see when you actually get these companies to go back to their longer term algorithms on pricing.

Sam

And it’s probably a slow bleed on it between here and there, but that’s still problematic for the Fed because guess what? Coke and Pepsi are the two things you serve at every restaurant in America. So if they’re raising prices, those restaurants are probably going to need to push price. If you have ketchup prices going higher, every single place that serves French fries is probably going to be like, why am I paying this much for ketchup? Come on. To your point, I think this is going to continue to filter through the economy until we actually see consumers push back. And you haven’t seen that happen yet.

Tony

This is core prices. Right. As service, we have to see SuperCore inflation actually subside a little bit, and then we’ll see that circle back, and then we’ll see some of these things decline a little bit. So it’s that kind of sequencing. Is that generally right?

Sam

Yeah, there’s some circularity to it.

Tony

Right. Okay, so let’s move on to tech. Really interesting, some text results. We saw Snap really just eat it last night. We saw Facebook the day before. Just be stellar. We saw Google stellar. We saw Amazon initially seem stellar and not be stellar. So can you talk us through a little bit what’s happening with tech earnings?

Sam

Sure. So it’s all about Opex, right? These companies, particularly the giant tech companies, had enough employees or too many, one or the other. And so you have Google that’s saying they’re slowing their hiring practices but still hiring key positions. Everybody says that and then they lay off a whole bunch of people. The real key here is that they have way too many people doing way too little for their bottom line. Facebook’s underlying earnings power is probably materially higher than it looks because they have too many people doing too little. Right. I’m sorry to say it, but the West Coast is going to see more layoffs and you’re going to see probably very similar growth trajectories from Facebook, from Google when they kind of get to the other side of this. And you’re going to have much, much higher structural margins coming out of that sector. I think it’s that simple. And you’re going to continue to have innovation, but you’re going to have it call it things that are a little more meaningful and a little more impactful to the bottom line and quicker. Right. That whole alphabet thing, that whole bet part of alphabet is going to shrink and shrink meaningfully over time, and you’re going to have much more targeted, much more targeted investments into things that can be hugely profitable over time.

Sam

So I think that is really going to be what you see. And that’s why Facebook was up, whatever it was, 15% in a day. When it comes to something like Snap. And I wrote a note about it about a year ago and called it Snap Foo, because that’s really all that company is. I mean, it is just situation, normal and it’s not exactly a great outcome. But when you look at it, it’s like Twitter, but call it more poorly run. And that’s where I think you can kind of dismiss whatever happens at Snap and just kind of look at what’s going on at Facebook. The potential demise of TikTok is probably the only saving grace for Snap in the longer run and will be call it a fairly positive tailwind for Facebook. I mean, if I was Snapchat, I would have my lobbyists on the Hill all the time calling for TikTok to get shut down in the US. It’s the only way they’re going to get incremental advertising revenue. So there’s some potential there. Amazon was a story of a consumer that was surprisingly strong and AWS getting just not looking that great coming out of the quarter. Right. You get a 500 basis point decline in the growth rate in April for AWS, and that’s problematic for a company that doesn’t make any money doing anything other than AWS.

Tony

Yeah, especially as Azure was growing for Microsoft as strongly as it was.

Sam

Well, it’s just better.

Tony

It’s a whole ecosystem, right. And so it’s interesting what you mentioned about tech jobs. We’re a technology company. For those who don’t know, we’re an artificial intelligence company. We see people in tech. We hear about what’s happening in tech. Many of those tech employees are dramatically underutilized with tech companies. There is a small portion of the workforce in tech that is working very, very hard. But many, many of the stories we still hear in these very large tech companies is effectively a four hour day. And so there is a huge amount of slack in these tech companies. So as Sam, as you say, it is about Opex, it is about headcount. And I believe we are going to continue to see those headcount reductions for the next couple of quarters. Maybe not at Facebook because Zuckerberg said they only have one more. Maybe he’s telling the truth, maybe he’s not. But there is a lot of slack in tech right now.

Sam

Yeah.

Tony

Okay. Hey, let’s move on to energy earnings. And Josh, you were making some comments about ExxonMobil this morning. Can you help us understand what’s going on in energy and particularly what you saw with ExxonMobil? Yeah.

Josh

So Exxon and Chevron had record Q1 earnings. So not record all-time high, but record for that quarter. Exxon had been rumored to be a buyer of Pioneer Natural Resources, where their CEO actually just announced his retirement. And there’s no announced deal, so we’ll see if there’s a deal there or not. One of the things Exxon said that would indicate that there might not be a deal is that they are interested, given their cash build and their strong balance sheet position, they are interested in doing acquisitions, but they’re interested in value over volume. And so Pioneer is a wonderful company, but it trades at sort of the extensive end of the range of sort of the large publicly traded producers and sort of way above where a number of different multibillion dollar oil transactions have taken place.

Josh

So I don’t know that we’d see Exxon go and do two or three or something billion dollar acquisition. I personally believe that companies like that should it shouldn’t be above them to do that size deal, but just historically they’ve chosen to sort of value size over value. So we’ll see if they shift. I guess I don’t believe them, but it is interesting in terms of hearing that. And then also just these results have been stellar.

Josh

But I’d say again, I think I’m a little more bearish than you guys. I think we’re sort of further along this sort of trend in the same ways we saw a ton of housing development, especially multifamily, to the point where I think we’re about to start seeing rents fall essentially pretty materially as all this new capacity comes on. And especially you just see it so vividly here in Houston.

Josh

For refineries, there’s just an enormous amount of capacity that came on. And there was this sort of trailing story. By the time it became headline news, by the time sort of the Lagging research analysts started to love refining middle of last year, by the time the government started to make statements about it, we were already in a position where we were getting into a surplus of capacity for refining. And I think that’s going to hit these guys earnings. Exxon, Chevron, the Integrators, as well as the refining companies significantly over the next few quarters. So I think we can have an oil shortage and a refining surplus simultaneously. And if anything, it actually really helps from a demand perspective where again, having too many apartments is terrible.

Josh

If you own the apartments or if you lent on them, it’s amazing if you want a bunch of people to move to your city and you want people to go spend money at restaurants and to start buying goods again and so on. So similar idea. I think we’ve had very wide refining margins, very high, historically high margins.

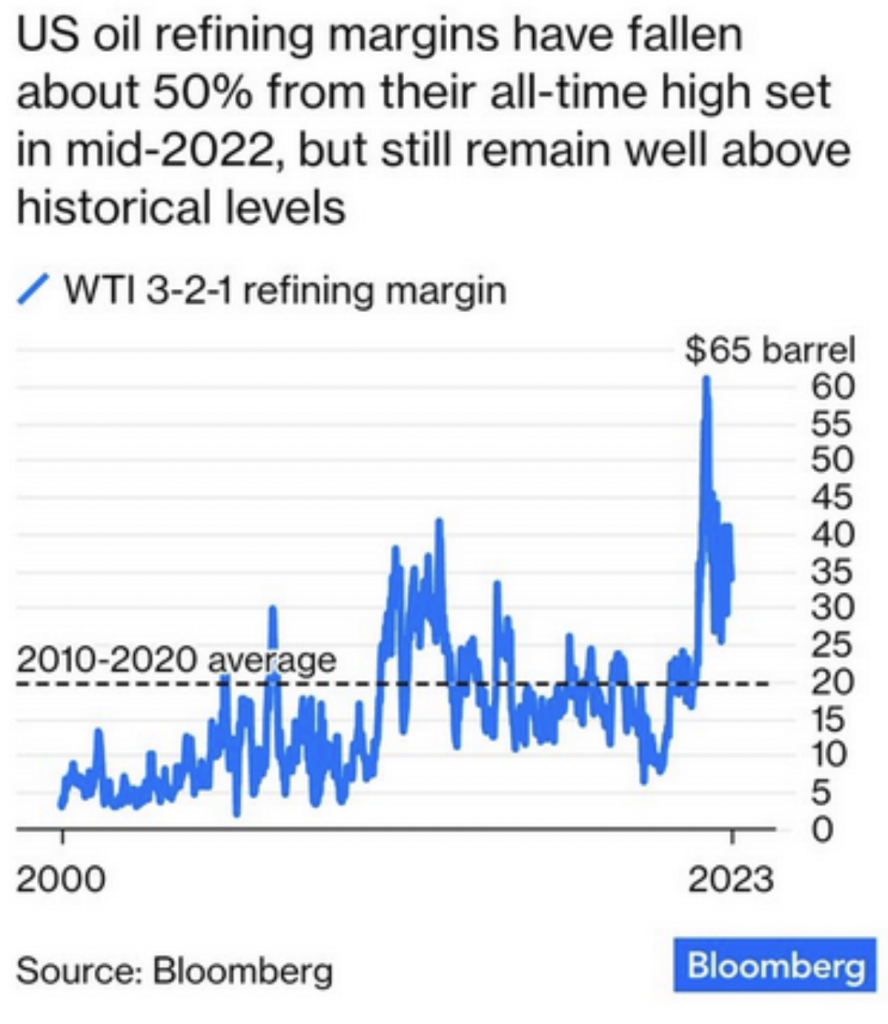

Tony

They’re down 50% right over the last. They’re down something like 50% over the last ten months.

Josh

Yeah. And again, I was saying, hey, they’re going to come down last year and people thought I was nuts. And they’re like, oh, you don’t own very many refiners, therefore you think and it’s like, well, I can sell producers and buy refiners if I want. Sure, I’ve been selling some producer stocks and buying some oil services, because I think that’s sort of a little bit of a tighter market. But no, I think there’s more to come. Even with US refiners having an advantage because of low local natural gas prices, there’s still a lot more compression to come. And pricing can still stay elevated, margins can stay elevated relative to where they were, let’s say, five years ago for refiners, but they can still go down even more, which means there’s even more room for oil prices to go up while it doesn’t actually affect consumers at the gas.

Tony

So Valero reported pretty well this week. So how are they continuing to report? Well, with margins falling 50%?

Josh

Well, Q1 margins weren’t so bad. They started to get bad towards the end of Q1, and they’ve gotten worse for refineries in Q2. So we’ll see. In terms of what it looks like, when I looked at the sort of on the ground data versus what Valero reported, there’s an inconsistency. So maybe Valero is taking share. Maybe they’re just sort of using backward looking numbers like the Fed and not sort of incorporating real time data. But we’ll see. There are various aspects of their specific business, right? I think they have a little more ethanol, they have a little more other aspects, biodiesel. So there’s aspects of their business that could do well even if crack spreads narrow. But I’m not sure exactly, but their report doesn’t make me think any differently about sort of the likely trajectory or refining margins over.

Tony

And then you mentioned services companies. We saw NOV report and it was a real disappointment. So is it just a bit early for services firms or what do you see as the opportunity there?

Josh

So we already went through a sort of boom and bust for natural gas. I mean, natural gas was down 80% or so from its high last year. And so there was a ramp up in service pricing and utilization oriented towards natural gas development in the US. And Canada that’s in the process of unwinding. So we have that going on at the same time that there’s sort of this longer cycle ramp up in oil development activity. And so one of the big things that prevented companies from drilling for more oil in shale here in the US. And in Canada was just an insufficient capacity of services. And so now that’s freeing up from natural gas. It’s getting redeployed to some extent. And that’s sort of the narrative from the rig companies and the pressure pumpers. NOV is a little different. It’s more oriented towards sort of new build activity. And so if you’re building new rigs and that’s sort of your business, you’re building new other equipment for de novo activity, things aren’t great for you. Your story, because of this natural gas softness, at least in the US. And offshore US, has gotten you’re pushed off.

Josh

But if you’re a rig company trading at a third of the replacement costs of your assets and half or a fifth or whatever of your book value, or a premium to your book value, but you went bankrupt and so you had to restate your book or you’re a pressure pumper similar sort of idea. Or various other service providers. You’re in a sort of different position than an equipment manufacturer, which is predominantly what an NOV is doing.

Josh

So again, there’s some complexity. There’s some noise and nuance. I would point to Schlumberger’s excellent earnings. I mean, it helps that Schlumberger is still very active in Russia despite sanctions. They sort of stole their competitors contracts and kept going. So that helps. But even beyond that, they’re very busy. Halliburton and Baker Hughes are very busy, and Weatherford had just blow it out of the water earnings. So I think there’s some nuance and sort of similar to maybe Exxon’s oil production business, and Guiana is going to be great. And similar for Chevron, for their Permian business, they’re going to be great. Those guys that refining businesses may not be so great in Q2, Q3. It may not matter for them. It may, but there’s a possibility for there to be some sort of differentiation between different sort of niches within that services space.

Sam

And to Josh’s point really fast here. Precision drilling, which is a very small driller, or smallish driller, had absolutely crazy day rates on a year over year basis. I mean, those things were nuts. So to Josh’s point, you do have to differentiate on the services side. There’s some doing great and there’s some that just not so much.

Josh

Well, they would say. So I had lunch with them a few weeks ago. They would say that those rates aren’t crazy, that those rates are sort of they’re barely back to where they were a few years ago when oil prices were materially lower, and they experience all the same inflation that everyone else is. So their labor costs are higher, their input costs are higher. Replacement costs for rigs are way higher. So arguably, and this is sort of the Super Bowl thesis for drilling rigs and similar for pressure pumping and so on, I mean, you have these businesses trading at a giant discount to replacement costs. They’re not going. And again, this is to the detriment of companies like NOV. They’re not going and replacing or building new rigs right now. They’re just using their existing fleet. So they get to sort of overearn until you get day rates to a point where it’s economic to be able to go build new rigs. But the cost of capital is so high in the oil services business that even if it was theoretically economic, which it’s not, you basically would need day rates to go up another 50 or 60%, which is huge, right? Because that would all be incremental to margins for these guys. It would basically double or triple their earnings. You would need them to go up that much and their stocks to double before you’d see a bunch of actually new rigs, not refurbishment, not movement from a diesel burning rig to an electric rig or whatever, but a full new rig build onshore high spec. You’re not going to see those until you see much higher day rates.

Josh

And that means it sounds crazy, but it’s still. So you guys were talking about food earlier and restaurants and I like McDonald’s ice cream cones and they used to be a dollar and now they’re two and so they’re still a great value, but they were a steal. And so it’s sort of you get to this point, I mean, the right price, you go somewhere else if they’re like $4 and you can go to Basket Robbins and get a much better one for six, but you’re not going somewhere else at two instead of one or 1.70 plus tax instead of one. Similar idea. I think on the I know ice cream cones and drilling rigs are very different, but you have this much higher bar and inflation has really helped too.

Josh

There is a lot of sort of complexity across the very broad oil services space and NOV made it look real bad oil states. It looks like it’s getting whacked right now. I was looking at my phone a little bit, I apologize, but I was trying to see what was going on there to be able to answer this question, actually. But Schlumberger Halberton, some of these other diversified services companies doing great. And the rig companies are actually, despite this crash in natural gas prices and a rapid drop off in natural gas oriented rigs, day rates are strong. So again, very sort of nuanced situation and variety of different outlooks for different companies focused on different aspects of it.

Tony

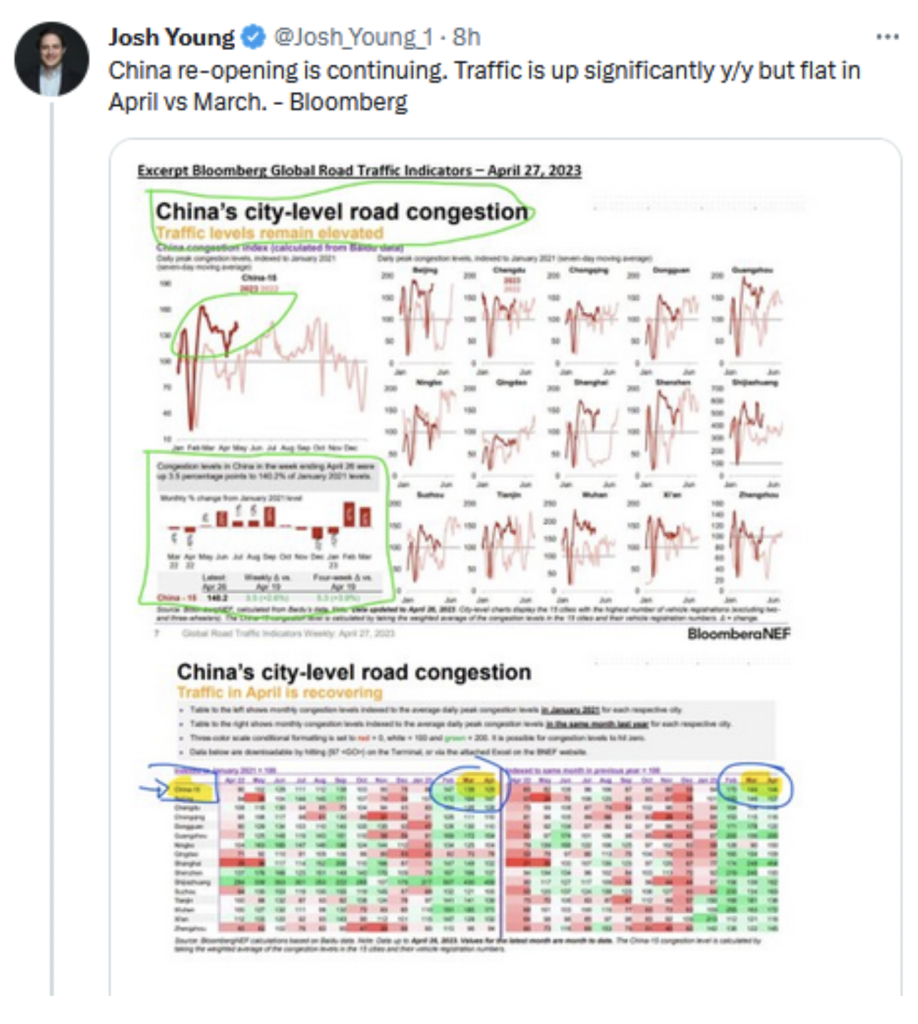

Josh, before we close up, let me ask you about China. You’ve been posting about China a little bit and you’ve talked about this for months in terms of their traffic congestion and what’s happening in China in terms of their opening up.

And I imagine this would affect global crude prices. Can you talk us through a little bit of your view on China’s traffic and activity and what are your expectations about how that will impact energy prices?

Josh

Yeah, so it’s been really interesting. China took longer to start reopening than I expected. Then they reopened really fast in certain aspects of their economy and then they were a little slower to start giving visas for international flights, for example. And so there’s sort of this lag and then China has some of the same problems that we have in terms of evisceration of certain aspects of the supply chain and capacity. And so they’re having trouble ramping their domestic flights even though there’s overwhelming demand. They just don’t have enough planes and they don’t have enough pilots. And it’s just the same sort of you just mirror stuff and for some reason people think that these things are going to be different, and they’re not. There’s this overwhelming bearishness towards China and about China, which is bizarre. It’s almost I mean, I won’t call it names, but it doesn’t seem to be rooted in the fundamentals. And so I think it’s important to take away, step away from the headlines and look at the actual data and the actual consumption of things. And there again, it’s a little complicated because they are in a real estate bust, but despite their real estate bust, they actually appear to have positive economic activity in aggregate.

Josh

And for oil, it’s been really interesting because there’s a sort of negative headline, “China disappoints” China whatever. The reality is China considering they’re in a real estate bust, which is a huge portion of their economy, their oil demand has been gangbusters, and they’re still only running at two thirds of their 2019 levels for international flights. So there’s a lot of tourism that’s not happening. There’s a lot of driving that’s not happening that would be related to travel. Their domestic travel is really impaired because of the lack of planes and pilots. And so in aggregate, across all of that, it’s sort of been, I think, disappointing if you look at oil price movements so far this year. But the fundamental good and absent some big thing breaking and again, the central government, the equivalent of federal government in China, not very levered. The local governments are levered. Some of the state owned enterprises are levered, but the central government of China could borrow a lot more money, and it looks like they’re sort of starting to do that. And there’s a lot of room for additional fiscal stimulus there, in addition to the monetary policies that they’re implementing.

Josh

It looks like there’s room for them to get to this incremental, let’s say, 2 million barrels a day of consumption. That’s roughly consensus and was sort of expected from last year to this year. I think there’s room for them to hit it, which is obviously the overwhelming bullish thesis for oil in the short to medium term, in addition to supply limitations. And, I mean, it looks it looks on track. Again, very messy, lots of hand waving. But I don’t know. I mean, it looks it looks pretty good, even considering all the negatives and complexities there.

Tony

Great. Okay, guys, thanks very much. I think it’s kind of a little bit of a mixed outlook leaning toward a positive outlook. I mean, I think we you know, we’ve got a good separation of views today, but but I think in general, it’s we’re in a we just had a really interesting week, and I think the next couple of weeks will be fascinating, seeing what the Fed does, how aggressive their statement is coming out of the next meeting, how hawkish they are. Seems to me that that’s what we’re kind of all looking for in addition to the rest of earnings season.

Tony

But, guys, this has been absolutely fantastic. Thank you so much for your time. Thank you very much. And have a great week ahead. Thank you.