⚠️PRICE INCREASE SOON⌛️ Subscribe now to get access to AI-powered forecasts by CI Markets. Only $25/mo: https://completeintel.com/markets

In this episode of The Week Ahead, we’re diving into some key topics that are making waves with Deer Point Macro, Tracy Shuchart, and Albert Marko.

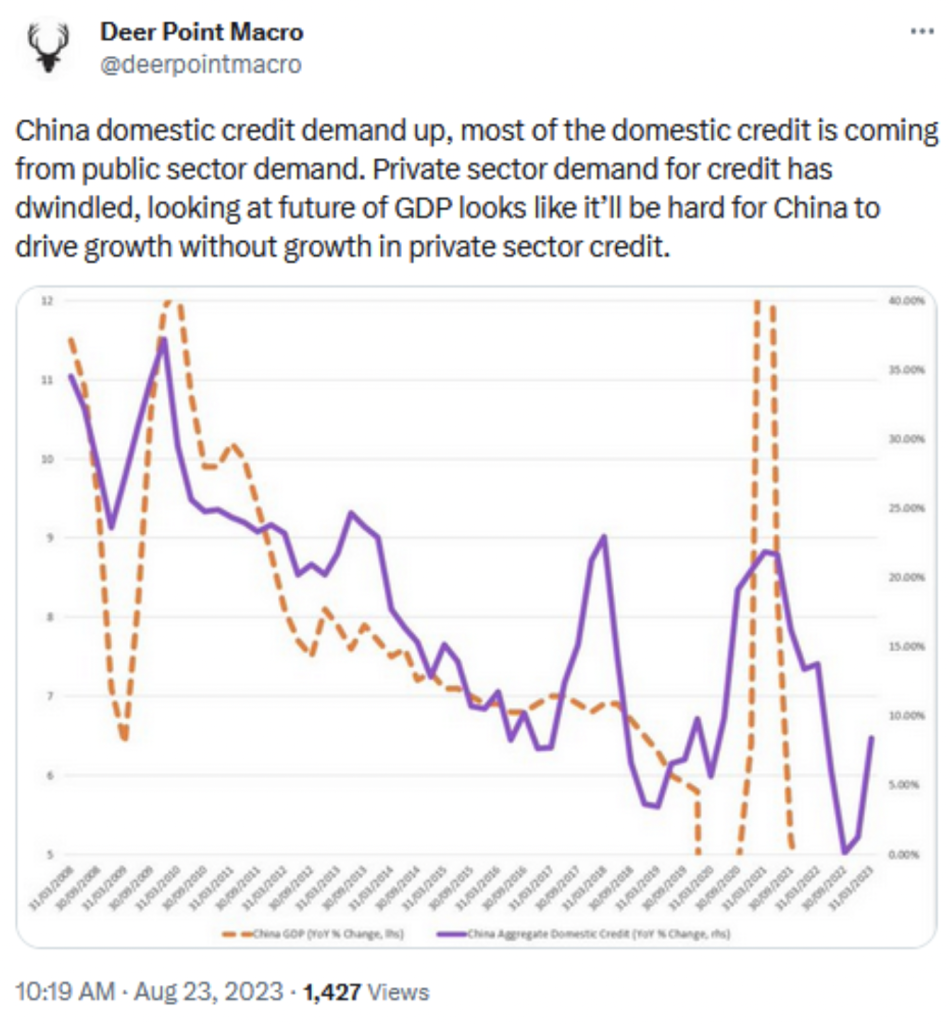

First up, Deer Point Macro takes the lead in discussing the mystery behind China’s credit growth. For years, credit growth has fueled China’s economic progress. But recent times have brought some twists and turns. What’s the deal with the current credit growth, and how is it connected to the country’s economic landscape? Tune in as we explore who’s borrowing, who’s extending credit, and how credit markets might just hold the key to fixing China’s real estate scene.

Next, Tracy Shuchart steps in to shed light on Saudi Arabia’s latest move to cut crude supply once again. You might remember we talked about their 1 million barrel cut last month. But now, whispers suggest another extension. What’s the bigger story behind these cuts? Could this signal weaker demand from China? Join us as we discuss whether OPEC is waiting for a sign that China’s demand is on the upswing before easing up on the supply cuts.

Lastly, Albert Marko takes the stage to expose the drama around the upcoming presidential election. Yep, it’s that time again, and the spotlight is on none other than Donald Trump. With the first Republican debate making headlines, everyone’s wondering if it’s truly Trump’s race to lose. But with a hefty 65% of voters viewing him unfavorably, could the Republicans face a major divide? Could they struggle to find a strong contender against Biden? We’ll dissect the major issues that will shape this campaign.

Join us for insights, discussions, and a deep dive into what lies ahead. It’s all happening on this episode of “The Week Ahead.” Don’t miss out!

Key themes:

1. China’s credit growth

2. Saudi cuts crude supply again

3. Trump’s to lose?

This is the 77th episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

Deer Point Macro: https://twitter.com/deerpointmacro

Albert: https://twitter.com/amlivemon

Tracy: https://twitter.com/chigrl

Transcript

AI

Attention traders, investors, and portfolio managers. Your trusted AI-powered forecasting app called CI Markets will be increasing its subscription price as of September first. Take advantage of its 94.7% forecast accuracy of more than 1,600 assets across stocks, commodities, currencies, indices, and economics.

Subscribe for $25 per month until August 31st only. Invest smarter with CI Markets. Subscribe today and secure your spot before the price increase.

Tony Nash

Hi. Everyone, and welcome to the week ahead. My name is Tony Nash, and today we’re joined by Deer Point Macro, Tracy Shuchart, and Albert Marko. It’s a really great week. We’ve got a lot going on with the Fed meeting soon and talking about everything in Wyoming. We’ve had quite a few things happening in tech and markets. There are some things that we need to talk about as a carry-over from last week. We talked about China last week. This week, I want to start with China’s credit growth. We’ve seen the CNY devalue even more over the past week, and it’s really important to understand China’s credit growth within that context. We’re also going to talk about Saudi crude cuts. They’ve been extended another month. That’s indirectly what we really want to talk about. As a part of that, we want to talk about Chinese demands, so Tracy is going to cover us there. Then I was going to bring us into the US presidential election. I know that’s over a year away, but I think it’s important to start paying attention to what’s going on. There was a Republican debate this week and a big interview with Trump and Tucker Carlson. We’re going to talk through some of that and figure out really what’s happening in the presidential election at this early date.

Tony Nash

Before we get started, I’d like to cover a couple of items regarding CI Markets, our forecasting platform for stocks, ETFs, commodities, currencies, and economics. On September 1st, we’re raising our prices from $25 a month to $50 a month. Subscribe to that product before the end of August before we have to raise those prices. The second announcement is we have released portfolios for CI markets. This allows you to see your stocks and ETFs and commodities and other things in a portfolio configuration where you can see the forecast for all of those assets on an individual and combined basis, together over a 12-month horizon. You can see the return by month, the expected return by month, the expected total value, the individual stock and ETF and commodity price in each month. It’s really, really interesting. I hope you guys can check it out. If you subscribe before the end of August, you get that with your CI Market subscription. Thanks very much.

Tony Nash

Guys, thanks so much for taking the time for this week. Deer, I want to start with you, and thanks for coming on this week. I really appreciate it. Credit growth has really fueled China’s economic growth for a couple of decades. That’s really not a surprise to anybody. It’s pretty tightly correlated with GDP growth. Recent credit growth looks fairly positive, but GDP looks pretty dire. You put out this tweet this week.

Can you help us talk through what’s happening there. Who has credit to extend and who is borrowing?

Deer Point Macro

Thank you so much for having me on, Tony. To that, I think the easiest way to discuss what’s happening in China now is through this idea of what is known as a liquidity trap. To explain that in very simplistic terms, just think about where the central bank is trying to ease monetary policy to fuel consumption or fuel economic growth. But instead of that happening, you have a hoarding of savings or the paying down of debt. What we’re really seeing in China is there’s not a lot of social demand at the private sector level for credit. Banks obviously have to lend. The only person that really has an appetite for credit right now is the public sector. Essentially, what banks are doing is they’re lending to the public sector. But as we know with what happens in China, a lot of that public sector debt is not utilized really effectively. As a function of that, I think China is seeing extreme contractions in GDP just because they don’t have the ability to actually produce with debt assets that are actually going to help grow the economy. Instead, as most people know, they built things like Ghost Cities or governments essentially doing other things with that money that are not all that effective. When I’m looking at China, I think the easiest way to see what’s happening is they’re just stuck in a liquidity trap and they’re not able to really fuel consumption. With most Asian nations, Japan, China, etc, They don’t have a very high consumption rate in general. These are nations that are much larger in terms of household savings. But the fact is you would think that as interest rates started to come down, whether it be from the private sector and general corporations, etc, you would assume that there would be demand for credit from the private sector in aggregate, but we’re just not seeing that.

Deer Point Macro

It seems like most of that’s being funneled into government entities.

Tony Nash

That’s great to know. Obviously, not efficient credit extension. But we’ve also heard about a mandate over the past week or so where the PBOC has instructed banks to help prop up the currency. Those banks only have so many funds or so much funds. They’re spending some of their funds on propping up the currencies, and they’re extending some of their funds for loans. Can they do both?

Deer Point Macro

I don’t think that they can do both for a significant amount of time. There’s been other things that have happened, as you mentioned, the banks. China also raised, I think it was the one year high bore rate, which is essentially the cost to short the the Taiwan, and they were hoping that that was obviously going to alleviate some of the tensions in the offshore market from shorts. But really, that hasn’t done a lot. Then the third thing that China is actually doing is they’re utilizing FX forwards. Essentially, the PBOC is buying the Taiwan and forward markets as well, hoping that that eases pain. But thus far, none of that has really helped the situation in the Taiwan. Again, I think that at some point these banks are going to have to choose either lending or doing what China is telling them to. Obviously, with the political situation of China, if you go the opposite route, there’s going to be hell to pay. Most of these banks will probably try to continue as long as they can in the sense of trying to facilitate a stronger year on because that’s the government mandate currently. That could to further credit contractions probably going into the next quarter.

Tony Nash

Okay, so you talk about the debt trap, and we have a huge amount of CNY denominated debt domestically. A lot of it, this has continued to roll over from, say, the 2007, 2008 period, very difficult for them to write off, so they continue to evergreen it. Can or is it in China’s best interest to devalue CNY so they can make USD through exports to repay their debt, their CNY-denominated debt, at a devalued CNY? Is that a plausible solution, at least for some of the debt that they have?

Deer Point Macro

I think for China that’s probably the most plausible solution because if we look at overall macro leverage, so just overall leverage in China’s economy as a whole, I think it’s like 228 %, something around there, I believe, off the top of my head, if anybody knows better, please correct me, as a percentage of GDP, so obviously China does need to deliver it. The problem is they haven’t really been able to do that. No, I would agree this is probably the best route for China going forward. The BIS does release those numbers. It should be interesting, again, like I said, in the next quarter, if we do start to see leverage start to come down. Thus far, we haven’t seen that. That data is only up into Q1 of 2023. As of now or the latest data point, China does continue to add on leverage. But I do think that obviously using US dollar exports, et cetera, to help drive down the overall leverage in the system would be the best route for China. But it is most likely as well going to come at the cost of slowing economic growth.

Tony Nash

Yeah. Just so you know, our complete intelligence forecast, we forecast 1,300 assets every week. We have CNY going to about 7.5 by December or in Q1. I can’t remember the specific time, but we do have it continuing to devalue to about 7.5. I think that would really help with some runway for them to pay down some of this legacy debt. Now, you mentioned that 200% debt to GDP. That, I don’t believe includes these local government finance vehicles, right? Those LGFVs. I mean, this is something like… I mean, officially it’s $2 trillion. I think it’s probably double that in reality. Is that included in the debt to GDP number that you’re talking about?

Deer Point Macro

No, it’s not. If you started to include that, I believe when we look at it, it would probably be much worse. That figure includes things like central government debt, sorry, federal government debt, as well as the entirety of the private sector. You have things like household and corporations in that figure. But no, the locales aren’t actually or the municipalities aren’t included. If we were to include that, like you said, it could probably be somewhere in excess of $8 trillion. That figure would just… It would worsen it overall. The problem is China is having this massive increase in macro leverage. But at the same time, what we’re actually seeing, and I put out something on that as well, if you purchase power, parity, adjust, China’s productivity metrics, productivity is starting to come down. So it’s declining as well in terms of overall output, and it has been for a very long period of time. I think one function of that is, China has been using a lot of money, but it hasn’t been at the expense of adding more capital per worker, etc. So as a function of that, what you’re getting is you’re getting a declining labor force and capital consumption or the depreciation of capital that’s depreciating at a more rapid pace than population growth.

Deer Point Macro

What you’re essentially having is you’re just continuously having lower and lower productivity that’s coming out of China. I think that that’s obviously going to continue to hurt them as well. Because me personally, I’m a big believer in Robert Solow’s, the solo growth residual. I think absent some of these factors of production and increasing the capital stock, and if you use debt in the right way, you can get massive payoffs. But if you use it in the wrong way, you’re just going to continue to have to divert future income and current income to the repayment of useless debt. I think that that’s where most of the world is. The US, as Lacey, Hant, has said, is in a very similar situation. But China is probably three times as bad as the current state of the United States.

Tony Nash

I just want to interject here. I think it’s easy for us to poke at China with the assumption that these guys just don’t know what they’re doing. There are incredibly, incredibly, incredibly smart people in think tanks, in the economic planning unit and other places in China. They have some of the smartest people in the world focused on these problems. But the political reality in China is one that does not allow them to do what we would normally do in an economy with an open account. These guys aren’t stupid. They’re really, really bright. One of the things, and this is a favorite topic for us here, so I want to bring you into this is there have been there’s been a lot of discussion this week about the Bricks meeting. Albert’s about to laugh here. Yep, a big eye roll. We had Brazil’s President say that countries want to use their own currencies and people proclaiming the death of the dollar and all this stuff happening. What does, say, a BRX currency usage look like? Does that look like a single currency? Or does that look like an atomization of emerging market currencies used for cross-border debt and trade?

Deer Point Macro

Yeah, that’s a good question because I think that when you talk to people who are very pro-bricks, they don’t even know the answer to that question. Some people say it’s going to be this commodity-backed currency. Okay, if you believe that it’s going to be gold, because most of these people believe that for some reason it’s going to be gold. What’s very interesting is Alpine Macro actually put out a chart on this, which I believe is a Montreal-based sell-side shop. But essentially, if you were to look at gold as a percentage of total reserves for bricks and aggregate before they added these other six, bricks and aggregate, about seven % of total reserves are gold. You take the G7, it’s about 45 %. Right now, China alone has, I think, as a percentage of total reserves, gold accounts for about 4% of that. Saudi Arabia, who just joined because I did something on them recently, I know the number off the top of my head, their gold reserves as a percentage of total reserves is 10 basis points. When you start to look at these things, I don’t think it’s going to be gold. The next problem is, well, can it be the Wang?

Deer Point Macro

Well, the Wang doesn’t have… They have capital controls, so that wouldn’t be very efficient. Obviously, if China did open or get rid of capital controls, you would see a max exodus of money from China. That would come at the detriment of Chinese growth and the Chinese economy. Then for me, it’s like, well, what else are they really going to do besides settle trade and these currencies, which is all fine and dandy. But one of the greatest or one of the most ironic aspects of this is if you look at Argentina and Brazil, people who have been using settlement, what you actually see is you’ve now seen a spike in PBOC swap lines. What seems to be happening is these people are more than happy to settle trade in year one. But after they hold these, and I know Albert talks about this as well, it’s not like the euro dollar system where you can essentially create liabilities and you can do something with that. They just sit on the balance sheet of these banks, so they’re pretty much useless. What then happens is all of these central banks go, Okay, let’s utilize swap lines and swap these Taiwan back to the Central Bank of China and get dollars back.

Deer Point Macro

The funniest thing about Argentina as well was it’s like, Let’s use Taiwan to pay off all of this debt, but then let’s get a $7 billion aid package from the IMF that’s in dollars. I don’t think that this is really going anywhere besides settlement. But settlement and other currencies has happened for a long period of time. But I tweeted about this today, but what I care more about is invoicing, which in very simplistic terms is, what’s the denominator of foreign domestic exports? What’s that vehicle currency that’s being used? Nobody is invoicing in any currency other than the dollar because I just don’t think that it’s possible. You would have volatility without getting too complicated. But that affects things like exchange rate pass-through. If you have massive volatility and exchange rate pass-through, it slows domestic exports. It changes the pricing of domestic exports, and then you have a real crisis on your hands. Even in terms of invoicing, I think that’s much more important than settlement. If Bricks comes out and says we’re invoicing an X currency, that will be where things start to get more interesting.

Tony Nash

Yeah. I just want to ask all three of you guys. Okay, of the BRICS currencies, if they had to choose one to be the main vehicle for them, which one would it be? Now it can’t be the CNY because they’d have to open their capital account. Let me do that. CNY, Brazil Real. Raise your hand when I say one that would be vital. CNY, not you, dear, of course. CNY, Brazil Real, South African Rand, Russian Fun Tickets, and Indian rupee. Like Indian Rupee.

Albert Marko

You forgot horse shit. That’s what it is. That’s the answer. It’s horse shit.

Tracy Shuchart

I think you could do the Indian Rupee, but I don’t think they’re interested to be in the mix.

Tony Nash

Right. Let’s talk about that. Brazil, Real. I mean, nobody wants to real, right? Not even Brazil. They’re going around, same thing. Nobody wants… Those central banks are just not credible.

Tracy Shuchart

They’re all just-.

Tony Nash

Russian Ruble, same thing. Not a credible central bank, not a credible currency. The only one, even the PBOC, honestly, not a credible central bank. Smart people, but they’re so mysterious, not a credible central bank. The only one that has a credible central bank is the Bank of India. Am I wrong?

Albert Marko

If you put a gun to my head, that would be the only one. But we’re talking about a group that some of their members are defaulting on debt. Other members have militaries piled up on the mountainside against the Chinese border. Other ones have civil war. What are we talking about? What are we talking about? This isn’t like a group of France and Italy and Germany getting together with China. None of that’s happening. We’ve gone through this whole cycle of gold is going to dethrone the dollar. And then it was the Europe and then it was crypto and now we’re back at gold. When do we just stop this horse shit nonsense that people pedal out there saying the dollar is going to die of some horrible death and China is going to take over with bricks. It’s just simply not going to happen in our lifetime.

Tracy Shuchart

Albert Welles and chose violence today.

Albert Marko

Every time I wake up in the morning in Twitter, there’s this new BRICS guy coming out, and some people selling a newsletter about the dollar going to die of the horrible death to the Chinese. There are so many geopolitical issues that have to happen. There’s so many food security issues that have to happen, debt problems that have to happen, so on and so forth. We are so far away from the dollar dying that none of us are going to see this in our lifetimes. I’m really… On one hand, I’m just pissed off. On the other hand, I feel really sad for retail investors and youth coming up in the educational systems that hear this crap coming out of people’s mouths.

Albert Marko

My point of view, it’s not going to happen. It’s not worth thinking about. You want to talk about vacuums and trade and geopolitical issues, where the Chinese and the Indians can patchwork themselves in? Sure. But that’s only until the United States gets their act together.

Tony Nash

It’s not the margin, right? I mean, it really is. It’s some marginal cross-border activities, and like Deer said, ultimately, they end up converting it to dollars anyway.

Albert Marko

If the Japanese and the Sweden want to interact on any trade, that goes to the New York Fed to get converted. Otherwise, it doesn’t work. That’s what people don’t understand. Snyder talks about this multiple times in his Eurodouble University thing. That’s just the way the plumbing works right now. And there is no other mechanism that can dethrone that at the moment. I’m not saying something can’t happen in 100 years or whatever. At the moment, that is how it works. It or not.

Tony Nash

Yeah. Look, if the euro hasn’t dethroned the dollar, and there are some very smart central banking people in Europe, if the euro hasn’t dethroned the dollar over the last 20-some years, then the CNY is not going to dethrone the dollar.

Albert Marko

That’s exactly right. I mean, Europe has had a bustling economy with manufacturing and purchasing power for their citizens. I mean, they had every component there except for the military geopolitical part. And it failed. Now it’s half the size of what it was versus the United States market. If you can’t look at that and say, What’s China going to do? Then I can’t help you people anymore.

Tony Nash

Okay.

Deer Point Macro

I would be- What.

Tracy Shuchart

Else is – problematic for CNY is also the fact that they’re known as currency manipulators, and this does not help them in the long term trying to be seen international currency. What we’re seeing right now is exactly that happening, and it rears its head every once in a while. If CI Futures is right and we go to 7.5, for a fact, that’s pushing the limit of…

Albert Marko

China’s economy is 400 or 500 times leveraged. What are we talking about here? China.

Deer Point Macro

And then to, and maybe, Tracy can speak about that as well. But even to India, which we all agreed would be the most practical currency to settle trade in. What was it? A month ago Russia was like, Hey, we don’t want to take payment in rupies because the rupee was depreciating. Now you have Iran joining and it’s like what? People are going to take Iranian, Tolmond in the settlement of trade, which is devalued like a million %. I mean, not really, but obviously that currency has become an absolute cluster. It’s like, how are they going to settle trade? I think with the UAE and Saudi Arabia joining, those would actually be the only two currencies that would make sense. But again, both of those are hard pegged to the dollar. So essentially, you’re still trading in dollars. You’re essentially…

Tracy Shuchart

Trading in dollars.

Albert Marko

The only reason they would even consider the dirum and the Saudi is just because in the real is because it’s pegged to the dollar. Forget about debt.

Tony Nash

Maybe they’ll ultimately back into that. One thing I want to go back to, Tracy, you talked about trying to be a currency manipulator. I’m sorry, the other side of me is going to say this. Everyone’s a currency manipulator. I know. The US is a currency manipulator. Everyone’s a currency manipulator. But they.

Tracy Shuchart

Have to be careful how much they let the Yuan go because everybody’s watching that. Because everybody knows they’re doing that to help their experts, et cetera, et cetera. It’s just a little bit more obvious where they are concerned. We all know that.

Tony Nash

Yeah. That’s fair.

Albert Marko

But yes, that’s. The Renminbi is nothing more than a Ponzi arbitra scheme for more dollars for the PBOC. Absolutely. That’s all it is.

Tony Nash

Yeah, absolutely. I just wanted to say that because I know in fairness, people will make comments saying.

Tracy Shuchart

Oh, no. Yes, I agree with you. Everybody’s the manipulator.

AI

Heads up for a short break.

AI

Are you using the potential of AI in your portfolio management strategies? With an impressive 94.7% forecast accuracy on average, you can confidently integrate AI into your approach with CI Markets. Visualize the potential volatility of your portfolio over the next 12 months and gain insights into specific assets that might experience fluctuations. This empowers you to make informed decisions on when to buy, sell, or hold. CI Markets covers a wide range of over 1,600 assets, including stocks, commodities, forex, indices, and economic indicators. Imagine running limitless portfolio scenarios to optimize your gains. Curious about the outcome of removing or adding certain assets? Wondering how your portfolio might evolve in the next 3, 6, or 12 months? CI Markets equips you with answers to these crucial questions. Whether you seek a streamlined portfolio analysis, wish to explore diverse scenarios, or aspire to track your investments with precision, CI Markets is the ultimate tool for you. Ready to learn more? Visit us at completeintel.com/markets.

AI

Thank you, and now back to the show.

Tony Nash

Okay, great. Let’s move on to crude oil. Tracy, last month we discussed Saudi Arabia extending their million barrel-a-month cut into September. There’s been chatter this week about another extension of Saudi’s cut into October.

I know that on the face of it, that’s a thing. It doesn’t really matter that much. It’s more the same. I’m just wondering, is there a bigger story here? Is this indicative of Saudi worries about crude demand?

Tracy Shuchart

I think that not necessarily. I think Saudi Arabia right now feels very in control of the market for the very first time in a very long time. I think that’s good news. That is good news for them. I think they realized after many years of having tips and flooding the market, that didn’t really work out for them economically as well as they may have expected. Really at this point, I look at this as in really this is Saudi Arabia is feeling very in control of the market right now. They are the swing producer. I know we’ve seen all these… EIA recently said, it expects this big production increase from the US. I have mentioned on prior weeks that I think will probably start seeing less production in Q4, and they’re a little bit more optimistic than perhaps they should be at this point, which would not be very surprising.

Tony Nash

On the one hand, we have Atlanta Fed GDP now, which is forecasting like 20% GDP growth for the US in Q3, right? It’s actually more like six, but it’s ridiculous.

Tracy Shuchart

Yeah, we get it at 5.9%. But.

Tony Nash

Then we have what appears to be the bottom falling out of China’s economy. Over the past week, we have Brent that’s I think it’s trading at 83 today. It’s down or something this week. Even with this announcement, crude prices are falling. Is it possible that Saudi Arabia or OPEC or somebody piles onto more supply cuts given some of the uncertainty, especially in China?

Tracy Shuchart

That could be an absolute possibility, although we are starting to see bigger pickup in, say, freight, demand and flight demand coming out of… I think I posted something today being Thursday about we are seeing a pickup in areas in China that would affect fuel demand, which is very interesting.

I think that if we look at overall commodities, people are starting to get interested in the commodity sector again, money is starting to pile in as far as ETFs. We’re also seeing the CRV index hasn’t been falling. If you look at this, China is going to bring down the entire world because of its poverty and explosion, and we’re all going to go into this big depression, big of the bit. No, no, no. Crv index, it’s still maintaining levels pretty well and well above the 200 A of your technical person. I think that things are not as dire as one may think. Again, this narrative that we’re all way into this what a recession, which has been the narrative for most of this year for the oil and gas markets, that still hasn’t really gone away.

Tony Nash

Okay, so I’m looking at your tweet now, and it says that China’s freight volume expense is 7.1% year-on-year. But isn’t that against a China that was effectively closed a year ago?

Tracy Shuchart

Well, absolutely. They say that as well. But those numbers are up from when they were in June as well. We’re seeing a little bit of a pickup there. We are seeing a bit of pickup if we look at the flight data. Domestic demand is a little bit below 2019 levels, If you look at international travel, they just opened up international travel. A while, we’ll probably need another month to really see how that data factors it.

Tony Nash

Okay. Are you seeing strong… What’s your expectation for crude demand? Do you think we continue where we are? Do you see strong growth into the end of the year? Do you see uncertainty? I guess in general, what’s your feel for crude demand?

Tracy Shuchart

Yeah, well, I think we talked about this in another episode where I said I thought that China demand has been very strong for the first three quarters of this year, but I do expect Q4 for that demand to come off because they have been stockpiling. Because I think I believe that when they issue new quotas for the tea pots, it’s going to be less. That’ll be the end of August. We’ll have to see. I could be wrong. That’s just my gut feeling that we’ll probably see demand from China queue for subside a little bit. That’s seasonal as well. I don’t think that’s going to really affect global demand entirely.

Tony Nash

Okay. The other part is given the issue with dollars in China and defending their currency, do they want to spend their dollars on crude since they have so much stockpile?

Tracy Shuchart

Of course not. They don’t need to. They have enough stockpile to have it. They can essentially pull back on purchases, even with their demands being the same as it was all year. Even if demand increases in China, they can effectively pull back on purchases because they have been stockpiling in their SPRs, in other words.

Tony Nash

Okay, great. Albert, Deer, do you guys have any thoughts on crude demand and China demand going to the end of the year?

Deer Point Macro

I just have a question for, unless if Albert wants to go first, but I have a question for Tracy.

Tony Nash

Go for it.

Deer Point Macro

Yeah, so, Tracy, don’t you think that if you’re the Saudi’s, and I know Laurie Johnson put out a piece on this today, or not really a piece, but somebody was essentially saying Saudi Arabia, the central bankers of oil, but now it seems like they’ve lost their ability to be able to control volatility. But what’s interesting is that when we’re looking at what’s happening, you’ve had oil at this let’s say $70, $80 range for months now. But even with that, Saudi Arabia, their fiscal balance is continuously in a deficit. I assume some of the cuts are to that because MBS is spending money like crazy and they’re essentially trying to balance the budget. But now what’s happening is the higher it seems that they are… The more cuts they do, the higher it’s going to take their breakeven price. It seems like they’re essentially digging themselves into a hole. Then I’m wondering, okay, and somebody brought this point up to me as well. Let’s say oil stays trade or range-bound. Do they just flood the market with oil to essentially get a cash injection into themselves to help smooth over the fiscal situation from where it’s standing today?

Deer Point Macro

Because I focus on the Middle East just as a function of family ties, but everybody thought that they were going to just be printing money. When you compare it to the rest of the Gulf, it seems like they’re having a bit of an issue just from smoothing things over. I’m not sure if you have any thoughts on the possibility of something like that where they just flood the market just to get a cash injection to try to help smooth over the fiscal aspect because their break-even price, I believe now with the cuts is like almost $90 or something around there.

Tracy Shuchart

Oh, their fiscal break even? Yeah, the fiscal break even is high. Yes, they are needing cash a little bit. Do I see a scenario where they’ll flood the market again? No, absolutely not. I think they learned their lesson. 2020 was a horrible experience. I think they feel more in control than anything right now. And you know what? It’s filled the gap of that, of the deficits in whether they’re making in crude oil, they’re getting back in dividends from a ranfo. And that’s filling that financial void, so to speak. And so I do not see a scenario at this point, and they’re still making money on the dividend side as being investors in a ranco, even though it’s state-owned. How they work that investment within their own country means they’re getting back money from a rampo via a dividend, believe it or not. That’s actually filling that fiscal void.

Deer Point Macro

Last question here. If you were to look like project out into the future of possible nations that look attractive from a commodity standpoint? Me personally, I’m slightly biased and I have political biases as well. With that being said, I do not favor Saudi Arabia personally, but we won’t go into that. But if I’m looking at places like Qatar or maybe even Kuwait, do you think that those might be, or the UAE even, do you think that those might be more attractive opportunities? Obviously, there are ways to get access to those as well, just from going into the year. Or do you think that Saudi Arabia is going to be the outperformer in terms of OPEC nation? I know Qatar isn’t part of OPEC, but just let’s just say.

Tracy Shuchart

If we’re talking about Qatar, that’s more of looking at the gas point because they did leave OPEC. If I were looking for opportunities and markets that would… I would probably be looking in markets that were under talked about and not so established. I think we talked about Aza-Vijem before, especially as far as gas is concerned to Europe. I think some things have been very attractive in Africa, even though there is huge geopolitical risk there. But I think there’s a lot going on there as well. As far as if I was investing in natural resources, I think Saudi Arabia is always going to be your state and.

Albert Marko

Your gold standard?

Tracy Shuchart

Your gold standard, yes. Your oil standard, your gold standard, they’re always going to be fine. I mean, Aramco is on its way to be the second largest company in the world. Again, if I was an investor, I’d be looking for opportunities probably outside of those big nations that they were already looking at and that we have been looking at for 100 years.

Albert Marko

It’s hard to get around Saudi Arabia, especially in the Persian Gulf area, because, I mean, Aramco does such big deals and they lock in the oil trade all over the area. I mean, the Dubai is pretty much subject to whatever the Saudi want to do. Qatar also, I mean, they have political ramifications if they ever decide to split off from the Saudi’s. Aramco had just a huge tender from what the rumors were in Iraq, and they locked up that supply too. So it’s really hard to get around Saudi Arabia in my opinion. I have a small budding oil brokerage firm developing at the moment, and the supply is just so tight. Even with the Chinese, most likely going to come off a little bit just because of their economic situation. In Q4, the supply for Q1 and Q2 in the next year is just taken everywhere from jet fuel to diesel to whatever refined product you want to even quote out.

Tony Nash

Even if demand isn’t there, say, from China.

Tracy Shuchart

It doesn’t matter.

Albert Marko

Taken into it. It doesn’t matter.

Tracy Shuchart

It’s hard for these cuts to filter in. That’s what people don’t understand. We’re just starting to see June cut. Forget about the July, August, September new cuts from Saudi Arabia. That isn’t even.

Albert Marko

People are overlooking or not talking about as much, at least in the public and Twitter domains of how bad the shortages are because of the Turkish pipeline being shut down in the Mediterranean. Because it makes all the costs going from Basra to Fugira around to the Suez and up into Europe exponentially more expensive. And nobody really discusses that. I know that there’s diesel shortages in Europe, in Northern Europe at the moment.

Tony Nash

Great. Think we could talk about this for another hour. This is a topic, and we’ll resume this maybe next week.

Tony Nash

I want to move to a completely different topic, and this may be the PG-13 section of the of the show. I want to start talking about the US election. I want your unedited version of the US presidential election. Last night, this is Wednesday night in the US. Donald Trump was on Tucker Carlson for a very softball interview. The rest of the Republican candidates had a debate.

I’m really curious, what are your thoughts right now? Because the prevailing narrative in the US is that Trump has this massive lead on DeSantis and everyone else, and that Ramaswani is overtaking DeSantis and all this other stuff. Can you help us think through what’s actually happening?

Albert Marko

Listen, Vivek Ramaswani, he’s a car salesman. He says all these ludicrous things that the generic voter of the Republican Party likes to hear at the moment. But once you start getting into the weeds and the details of some of his policies, they’re just absolute insane. And then it won’t happen. Not that they’re insane, they just won’t happen. Like, getting rid of 75 % of the government and being non-interventionist across the world and this and that. He’s just full of shit. It’s a guy that I don’t even take seriously at the moment. From my opinion, this is a DeSantis-Trump two-way race at the moment. The media is desperate to not allow DeSantis to get any momentum because if he does beat out Trump for the GOP candidacy, Biden’s got no chance. And the media knows this, the Democrats know this, all the polling out there, whatever they want to throw out, I don’t believe not even a single poll out there at the moment. And it’s still a little bit too early. This is still fundraising season for most of the candidates. I know they had this first debate. I didn’t even bother to watch it.

Albert Marko

I saw some types of notes and whatnot. But until late September, October hits when things get serious and money’s really starting to get spent, then we can talk about what the polls look like and so on and so forth. But there’s a lot of complexities to the US election, specifically the primaries that people don’t really quite understand, especially the European audience and the Asian audience, actually, even some of the Americans. In some of the states, it’s not a Republican versus only Republicans in the primary to vote. They’re open primaries. Some states don’t even have registration of a Republican or Democrat. So you have no way of polling somebody in one of those states like Wisconsin, for instance, to say, Oh, yeah, the Republicans nationally like Trump by 74 points. Well, it’s not a national race. It’s a state-by-state delegate race. And on top of that, some of them are proportional versus or all or nothing. So the proportional races, if Trump doesn’t win the outright majority, well, okay, he might win 40%, but then 60% of the delegate vote is for not Trump, which they’ll end up consolidating towards DeSantis, in my opinion, in some of those states. It’s a little early.

Tony Nash

We have these guys like Assa Hutchinson and these sorts of guys who are in, and there’s no way they can win. Why are they in? Why are they in right now? Why are guys like Tim Scott and these guys, why are they in the race right now?

Albert Marko

Well, different reasons. Tim Scott and Vivek are most likely running for a vice presidential seat. Assa Hutchinson is looking to raise money and then distribute it out to whoever the leader is where he can get political favors at that point because they take that money. The money they don’t spend it can actually donate it to a PAC or a Super PAC to whatever candidate and whatnot, and then they get political favors and that and the return for that.

Tony Nash

Okay, so that makes sense. When do some of these guys at the bottom say with, say, 3% or less, when do they start dropping out? Is that October?

Albert Marko

October. That’s when the money starts running out. Desantis and Trump obviously have the most money of the two candidates, and that’ll start showing in advertisements and debates and so on and so forth.

Tony Nash

Okay. Do you know how much DeSantis and Trump have raised? Is that posted or reported?

Albert Marko

It’s posted somewhere. I don’t know offhand of what the numbers are, but I mean, like Ken Griffin came out and said DeSantis has all the money in the world he needs to run.

Tony Nash

Okay.

Albert Marko

Then if you compare that with Trump, Trump is going to be really looking for grassroots donations, but that’s not going to be really enough to offset some of the corporate spending. And certainly Trump is not going to use his own money to run this time around.

Tony Nash

Right. Yeah. A lot of these stories saying that DeSantis should just drop out, this thing, when you see that stuff, what do you think?

Albert Marko

I immediately think that they’re manipulated post media narratives. They’re planted on purpose. I know people that used to do this for a living. I know the game of how that works. They call up a couple of anchors, a couple of journalists and say, Hey, here’s a sack of cash. Run the story. And that’s just the way it works.

Tony Nash

So do you think that the DeSantis campaign is wise to that? And that they’re… All these guys saying DeSantis should drop out. Are they just trying to do that?

Albert Marko

When have we ever heard of a top two or top three candidate so early being told to drop out? I mean, Biden and Bernie Sanders and Elizabeth Warren were in a three-way race for six months, and no one said one of them should drop out. The only people saying that is so they consolidate the votes to their preferred candidates, and they don’t want DeSantis to run.

Tony Nash

Okay, so since we’re talking about DeSantis, I want to ask two questions. First, I want to ask, why does Trump fear DeSantis? Or does he?

Albert Marko

He, of course, he fears DeSantis. Desantis is a popular candidate, especially with the independence. I mean, everyone wants to look at the Republican votes, so on and so forth. What about the independent vote? Independent vote is like 60-20 in favor of DeSantis at the moment.

Tony Nash

Okay. And the independents are usually the swing in elections.

Albert Marko

Of course, especially in the Rust Belt of Wisconsin, Pennsylvania, Michigan, so on and so forth. A lot of the states that have open primaries, a lot of the independents voting candidates.

Tony Nash

So why do the Democrats fear DeSantis? Or do they think he’s a joke or do they fear him?

Albert Marko

No, they fear him. He’s been an effective governor for years since COVID. He’s completely destroyed their COVID narratives and the state’s been bustling. Tracy and I both live in Florida, and we can attest to it. This state is just buzzing. The real estate market’s up, the job market’s up, the migration is up, construction is up. I don’t think the only city that’s lost population is Miami because Miami is well, Mimi.

Tony Nash

Because crypto guys went back home. Yeah, exactly. Albert, while you’re on this, I just want to do a promo for Florida as a destination. If you’re moving to California.

Tony Nash

I just want to encourage you to move to Florida because it’s so beautiful. Just go right past Texas and go to Florida. Deer, you have your hand up.

Deer Point Macro

Yeah, I got a drop in a minute, but I did want to ask Albert a question. I’m young. I’m in my late 20s, but I’m born and raised in South Carolina. I lived there for 24 out of the 28 years of my life. I feel that when I look at Nikki Haley, even yesterday, I feel like she’s the only one that really on the stage actually had a bit of a plan. It seemed like DeSantis was very scripted. I think she was right to point out that Veevik has essentially no international relation experience. She strikes me as really a traditional neocon in South Carolina is very famous for those even McMaster, etc. And so when I look at her, she reminds me somewhat of the GOP after Reagan before Trump, in the intermediate up to Bush. But I’m not sure if you have really any thoughts on her. But me personally, I’m biased. She was my governor. I like her as a person.

Albert Marko

She wrote a book not too long ago, what, like three, four years ago that was critical of the Republican Party, specifically Trump. She burned a lot of bridges. She’s not going to have any donors to support her because of that. She took an educated guess and a gamble of going against Trump early on, and then that backfired on her. And at that point, her political career as a presidential candidate is pretty much next to nothing at the moment because of that. So she’s most likely running for DeSantis’s VP spot in my opinion.

Tony Nash

Yeah, dear, I’ve heard the same that she upset so many people in the National Republican Party. Yeah. She burned so many bridges that she could have popular support in some areas, but the party will never support her.

Albert Marko

No.

Tony Nash

With the way she treated some people.

Albert Marko

Yeah. You don’t write a book and then air out all the grievances for money and get away with it in the Republican Party or the Democratic Party for that matter.

Tony Nash

If you’re a politician, you have to play party politics.

Albert Marko

Yeah, I could write a book right now and up in both parties if I really wanted to, you know what I mean? But I don’t want to be a target. But she needed the money and she did, and that’s that. She has to look at the consequences politically.

Tony Nash

Okay, so, Albert, we’re going to wrap this up because it’s early in the election cycle. But if you were to give people some advice, especially the people in, say, Europe and Asia who have opinions on US politics, one would be national polls are worthless right?

Albert Marko

Yes, they are.

Tony Nash

Okay. The other would be a lot of the guys on the Republican side who are in are probably in for three more months and then they’re out. Is that right? Absolutely.

Albert Marko

That’s correct. Most of it is fundraising. Other guys are in there for hopefully a VP spot or even a cabinet spot.

Tony Nash

Right. And so that’s the third thing. Watch the fundraising. Watch the fundraising. The fundraising is what allows these people to last.

Albert Marko

That’s exactly right. I mean, you’re not going to be able to take a taxi cab from South Carolina to Wisconsin to go to a rally. You need planes, you need grassroot offices sprinkled around you need advertising campaigns. You need people on the ground. That’s just the way it works. If you don’t have money, it’s a pointless endeavor.

Tony Nash

Good. Okay. There’s more to come here, guys. We’re early in this election cycle. Albert is a political expert. I don’t know how much you know his background, but he is a political expert. And so we’ll draw on him more and more through the US presidential campaign season. So, guys, thank you so much. I know Deer is gone, but he’s incredibly valuable. And we love his insights. Albert, Tracy, thank you so much. You guys are really generous with your time. So really appreciate this. Have a great weekend and have a great week ahead.

AI

That’s it for this week’s episode of the week ahead. Please don’t forget to rate us and review on whatever platform you are watching or listening to this. Thank you.