In this episode of The Week Ahead, we have Joseph Wang, Tracy Shuchart, and Ralph Shoellhammer.

Joseph kicks off by talking about inflation, the Fed, and banks. He looks at the recent CPI numbers and asks whether they suggest inflation or not. The conversation revolves around the Fed’s plans and a survey indicating two more interest rate hikes this year. We’re also examining changes in the money supply and whether it’s going back to normal levels.

Tracy gives us an OPEC update. The latest report forecasts oil demand growth for this year and the next. She gets into the impact of OPEC’s supply cuts, particularly Saudi Arabia’s extended cuts, and how they shape the supply situation this quarter.

Lastly, Ralph presents the case for why Europe needs nuclear energy. He shares insights from his report on the topic. Ralph explains the importance of energy density and its link to nuclear power. Safety concerns about nuclear energy and European perspectives on restarting nuclear plants are also discussed. We’re also looking at Germany’s energy mix and recent shifts in energy prices.

Key themes:

1. CPI. Fed. Banks.

2. OPEC Supply Deficit

3. Why Europe Needs Nuclear

This is the 75th episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

Joseph: https://twitter.com/fedguy12

Tracy: https://twitter.com/chigrl

Ralph: https://twitter.com/Raphfel

Transcript

AI

Plan and forecast the performance of your investment portfolios with an impressive accuracy rate of 94.7%, all thanks to the power of AI. Get ready for this exciting new feature, exclusively available on CI Markets. Coming very soon.

Tony

Hi, everyone, and welcome to The Week Ahead. I’m Tony Nash. Today, we’re joined by Joseph Wang, by Tracy Schuchart, and by Ralph Shoellhammer. I’m really excited to have the view on Central Banks and some of the macro stuff that we’re looking at with Joseph. He’ll help us look at CPI, PPI, Fed, banks, and the health of what’s happening in the US banking system. Tracy is going to help us look at OPEC. We’ve had some really interesting monthly report come through from OPEC, and we’ll look at the impact on crude prices. Then Ralph is going to help us look at nuclear in Europe. There’s some history there since Fukushima and nuclear plants closed down. We’re just going to look at some of the economics and impacts of why Europe needs nuclear now based on a report that Ralph just published.

Tony

Guys, thanks for joining. I really appreciate it. I know this has been a super busy week, and I always appreciate you guys coming to talk to us on Friday. Joseph, if you don’t mind, let’s start with you. We just had a CPI print and, of course, PPI this week. Obviously, everyone sees it. We’re in that phase where everyone sees it through their own prism.

Tony

Some people are saying it’s great, inflation is over. Some people are saying, We’re going to see a resurgence of inflation, and Core doesn’t reflect a weakening of inflation, all this other stuff. Do you see these prints as inflationary or disinflationary or neutral? How do you see these prints?

Joseph

Well, first off, thanks for inviting me. It’s a pleasure to be here. Thank you. Yeah, it’s great to meet everyone. This week’s CPR print, as we know, was unambiguously pretty good. We’ve had two good CPI prints over consecutively, and that very much shows that inflation is decelerating. Right now you can think of it in two ways. If you’re a team, and inflation is over, you can look at this, and then you can look at some model of where shelter inflation will be for the coming months. You can think, Well, there’s probably going to be more disinflation coming down the pipeline. Maybe inflation is really over. We’ll go back to the world wherethe world the way it was before. There are other people, of course, who would point to what happened in the 1970s. In the 1970s, you saw inflation rocket higher and then go back down. When it looked like it was going to go back down and stay down, it just did a 180 and rocketed higher. Those people would point towards things like, well, you have commodity prices rising, again, oil has been steadily rising over the past few weeks, and you also have wages that seem to be stuck at around, say, 4 or 5%, which is not consistent with 2% inflation.

Joseph

You have these two caps right now, and that actually is being mirrored in the Fed as well. This past weekend, Governor Bowman gave a speech where she basically strongly suggested that she’s not just open to another hike, but more than one hike since they used the term hikes, so in plural. That’s one faction. I suspect that let’s say, Governor Waller, and maybe Chair Powell would be partial to that. But on the other hand, you also have, let’s say, John Williams, who is President of the New York Fed, one of the top three people in the Fed, give an interview within New York Times where he’s setting up the groundwork for rate cuts next year. I actually think that overall, if you look at the evidence, I think it makes sense for there to be rate cuts going forward next year, but definitely not going back to, let’s say, zero, probably just going back a little bit with an acknowledgment that inflation is definitely decelerating, but probably going to decelerate towards a rate that’s going to be higher than pre-pandemic. In a sense, what I’m trying to say that there’s some truth to both those camps.

Joseph

Now, we could have a situation where inflation slows down but doesn’t go back to where it was before, and that’s still consistent with a higher for longer framework. The Fed looks at interest rates through the lens of real interest rates. So real interest rates are nominal interest rates minus inflation. If you look back over the past several months, inflation peaked at about 9% year-over-year rates. Now it’s come down to about, say, four-something %. That’s normal. At the same time, Fed raised interest rates from zero to over 5%, and maybe they’ll go a little bit more. As inflation has come down, if you want to keep real interest rates constant, it makes sense to cut nominal interest rates a bit. I think that’s what they’re setting up to do next year. It doesn’t mean that we’re just going to go back to a low interest rate world. I suspect that we probably hold around 4%, 4.5% if we cut rates there for some time. I think that’s the… I think that that’s how I read this inflation print, showing deceleration, but not towards a world that it was before.

Tony

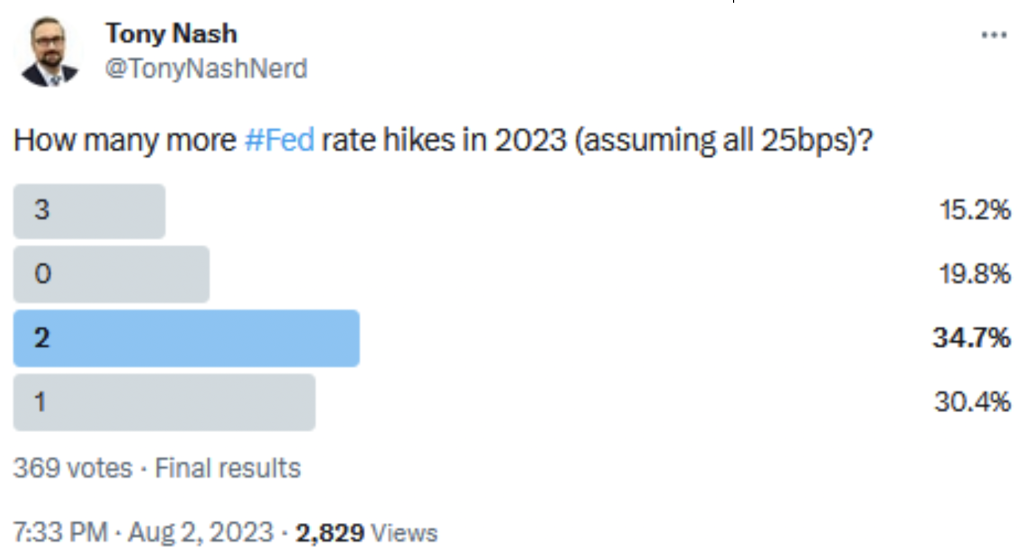

Yeah, it’s weird that we had been at low interest rates for so long. In the US and Europe and obviously Japan. There is this expectation, I think, that we’re going to snap back at something. We’re going to wake up from this dream, and it’s all going to be over with, and we’re going to be back at very, very low interest rates, very, very low mortgage rates. I think on some level, we’re arguing about the details about whether we are inflationary or disinflationary or whatever, because I think what you said about hire for longer is true regardless. We are at least for a period of time, it seems like we’re at a higher level. Now, we took a survey last week and my Twitter followers are fairly educated people. Most of them view, I think, I can’t remember the percentage, I’ll put it up on the screen when we publish this, but the majority had two or more hikes before the end of 2023.

That was before this week’s CPI print. What’s your view of that? Do you think it’s possible that there are two hikes before the end of 2023?

Joseph

Two sounds like a lot to me. When I think back to the last dot plot, Fed FOMC members overwhelmingly suggested two more hikes this year. The data has broadly come in line with their expectations. I think if we have another hike, we could have one more hike. But two, that doesn’t seem reasonable to me in line with the data and in line with what the FOMC members guided towards last time they released their dot plot. I think we could have one more. But right now, not next meeting, we’d really have to see, again, inflation reaccelerate, maybe wages go higher again. Basically, we’d have to see stronger than expected data. Right now, I think the doves on the committee have more political power simply because we’ve had two pretty benign inflation prints.

Tony

Okay.

AI

Heads up. It’s time for a Week Ahead break.

AI

With CI Markets, you can access AI-powered market forecasting for as low as $20 a month. Get 94.7% market forecast accuracy for over 1,200 assets across stocks, commodities, currencies, equity indices, and economics. With weekly updates and one-month and three-month error rates, you can rely on CI Markets to help you make informed decisions. Join a growing number of satisfied users who already transformed the way they invest and trade with CI Markets. Don’t miss on another opportunity. Start forecasting with confidence today for as low as $20 a month. Visit completeintel.com/markets to learn more.

AI

Thank you. Now back to the show.

Tony

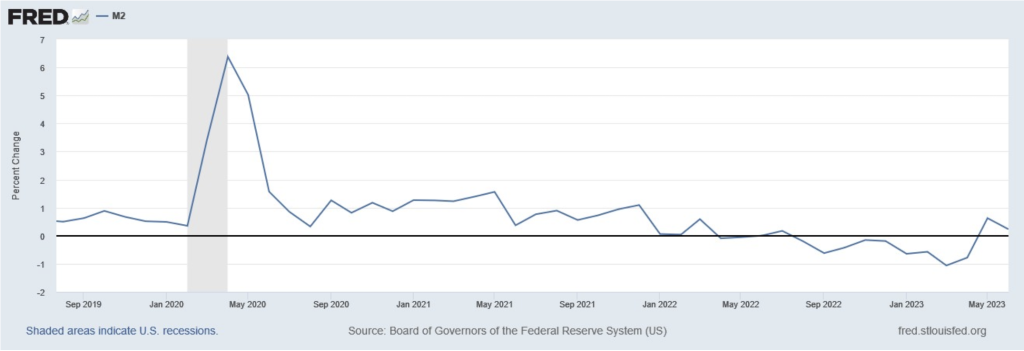

Great. I want to talk a minute about money supply and potential for QT. I’ve got a chart on the M2 money supply.

This is month-on-month growth rates for M2. Now, I did some work, I think it was last week, looking at the trend growth rate for M2. If we had kept the trajectory we had been on in 2019, we’re still about $2.1 trillion above that. I know in ’22 and in the first, say, four months of ’23, we actually saw M2 contraction, and then we saw a little bit of expansion in May and June. What’s your expectation in light of where rate hikes are going? Do you think the Fed will continue to gradually rein in the money supply, or do you think we’ll resume on this incremental, slow growth of M2?

Joseph

I’d be cautious when trying to map M2 to other economic variables. In the past, there was a school of thought, monetarism, that placed a high emphasis on money supply, so much so that the Fed, actually for a period of time, actually tried to implement monetary policy by changing the money supply. That experiment was not successful. If you look at what happened over the past decade, say, Japan, must have really increased their money supply, but did not seem to get inflation upwards. I don’t really focus on money supply when I think about the world. I think in the past, you could have made an argument where banks are making loans, creating credit, increasing money supply, and so we want to focus on that. But post financial crises, money supply is strongly influenced by Fed actions. When the Fed does QE, for example, that increases M2, and when the Fed does QT, that decreases M2. What you’re seeing right now, I think, is largely just the impact of quantitative tightening. The Fed is shrinking their balance sheet, and that mechanically has been shrinking M2. At the same time, we’ve been having very good growth, and financial assets have been going to the moon.

Joseph

I’m cautious when I think about money supply in the modern economy. Going forward, as the Fed continues to tie in their balance sheet, I would expect M2 to continue to decline, especially since the banks have significantly cut back on their lending. When you look at loans and leases from banks, you know that they’ve basically been relatively static for about since the end of last year.

Tony

Okay. You think we’ll see incremental QT on the Fed balance sheet?

Joseph

Incremental time? Absolutely. In fact, I think it’s going to go on for a couple of years. There is a discussion. There is some thought as to what would happen with QT when the Fed eventually cut rates. Like I mentioned before, Fed is laying down the groundwork to cut rates sometime next year. Now, traditionally, when you look at the Fed, the thinking is that you don’t want to step on the brakes and the acceleration at the same time, so it would not make sense to both be cutting rates and to shrieking your balance sheet. But Chair Powell, at his recent press conference, was pointedly asked about that, and he seemed open to be letting QT continue even if they were to cut rates next year. I think that that’s just a strong suggestion that the Fed really wants to get back to a smaller balance sheet. I think they have everything in place to make that happen over the, let’s say, another two years.

Tony

Okay. Now, you said they may cut next year or they’re likely to cut next year. Just because they say next year, I think there’s this belief that it’s going to happen, boom, it’s going to happen in January, it’s going to happen in February. We’re going to see rate cuts right away. That’s not what you’re saying, right? You’re saying sometime next year.

Joseph

Absolutely not. I think the common thinking is that the Fed is hiking, there’s going to be a recession, everything’s going to implode, and so they’re going to have to do emergency cuts to save the economy. What I’m seeing, what I’m thinking is that we actually just gradually, inflation comes down, growth slows a bit, or maybe not, I don’t know, but definitely inflation is going to be lower than, let’s say, the 9% annual rate we had in the past. In order to keep real interest rates in line at where the Fed feels is restraining, they’re just going to cut nominal rates a bit. Maybe just a little bit of an adjustment next year as inflation comes down. Now, inflation, I don’t think it’s going to come down to 2%, but it’s going to be lower than it was in the past. But then it was in the past several months. Yeah, sorry.

Tony

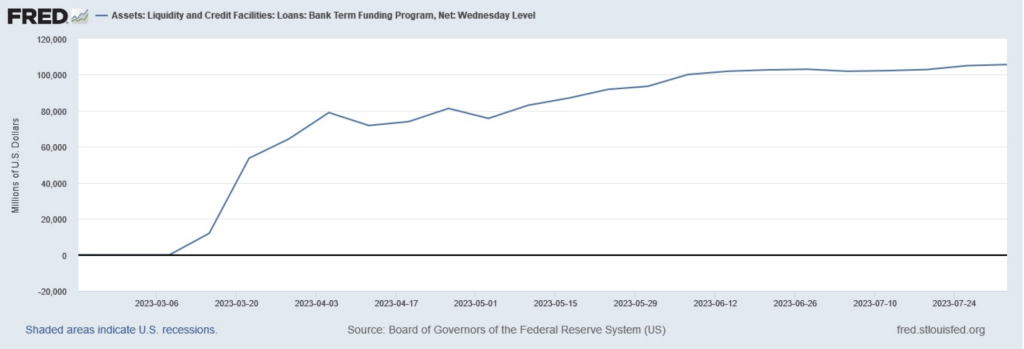

Right, past, say, 18 months or whatever, right? Yeah. That would be a nice, fresh relief for a lot of people. Hey, let’s move on to bank health, Joseph, because I know since March, there’s been a lot of interest with the BTFP, the Program for Regional Banks to borrow from. I know that that’s really a lot of your expertise is there. We saw the BTFP hit $106 billion, I think, last week. I’ve got the chart up on the screen.

It seems like banks are going more and more to bar from the BTFP. Can you help us understand what is going on with regional banks and what is the health of regional banks look like given the continued expansion of the BTFP?

Joseph

Yeah, the BTFP is an emergency lending facility that the Fed offered around March when we had a panic in the regional banking sector. The BTFP is really a sweetheart deal because you’re able to borrow basically borrow at one very advantageous rates, but you’re also being able to borrow at par value rather than market value. For example, if you had a treasury security and because the rates went up, it was now trading at $0.80 to the dollar. You can actually take that treasury and borrow $0.100 of the dollar against it from the BTFP facility. It’s a sweetheart deal, and I think it’s expected that banks would take advantage of that. I wouldn’t read that as stress in the banking system. What I think is more telling about liquidity stress in the banking system is federal home loan bank borrowing. When banks have stress, what they usually do is not go to the Fed discount window because there’s a stigma there. What they do is they go to the lender of second to last resort, which are the federal home loan banks, and they did that in size in March and April. When we look at federal home loan bank data, we’ll see that their loans are actually shrinking significantly.

Joseph

Banks are not borrowing as much from the federal home loan banks. They’ve cutbacks significantly, and that tells me that the liquidity situation is improving significantly. Now, I’ve also been following bank earnings reports over the past couple of months, and by and large, banks are doing fine. What I think is happening now is that a lot of the regional banks are having their profit margins, their net interest margins squeezed a little bit because they’re having to pay a little bit more to retain depositors. Even as interest rates go higher on their assets, they’re also going higher on their deposit liabilities, and that’s causing their net interest rate margins to contract a bit. They still remain historically healthy. They’re just not as fat as they used to be. I don’t think that’s a reason for concern, especially, again, we don’t expect the Fed to just keep hiking rates or whatever. Eventually, the Fed is going to cut rates even by a little bit and maybe not to the low levels before, but they’re going to cut rates a little bit and that’s going to give these banks a bit of a breathing room. Now, I would also take a step back and look at what happened with the regional banking sector over the past few months.

Joseph

Now, back then in March, it would seem like the system was imploding. There’s a lot of doom and gloom, but that was never my view. Another way to look at it, which is how I look at it, is at the end of the day, Fed hiked rates. A lot of the more speculative industries in tech imploded, and all the banks that built their business models around those sectors also went down. You saw Silicon Valley Bank, obviously, First Republic, obviously, you have the Crypto Banks. Crypto Banks also got taken down as well. I really think of that as more of an idiosyncratic thing rather than a sector thing. I’m not really worried about the bank system.

Tony

Great. Okay, so that’s good. From your perspective, the US banking system seems okay, if not good. Yes. Inflation seems to be okay if not it’s trending in the right direction. It seems to me from that perspective, the Fed banking system perspective, the US seems to be okay. That’s what you’re telling us.

Joseph

I think the US is doing well. I mean, if you look at, let’s say, first quarter GDP, it was growing above trend. If you look at second quarter GDP, it actually accelerated. If you look at GDP now, which is the forecast for this current quarter, which is very volatile and will get revised, it actually points towards further acceleration. What we’re seeing is that inflation coming down, wages continue to be strong, and of course, credit conditions that everything seems to be not very concerning. Now, if you look at credit spreads, for example, they’re very benign. They’ve gone up from their lows, but they’re still within historical ranges. From my read, the US economy is doing well.

Tony

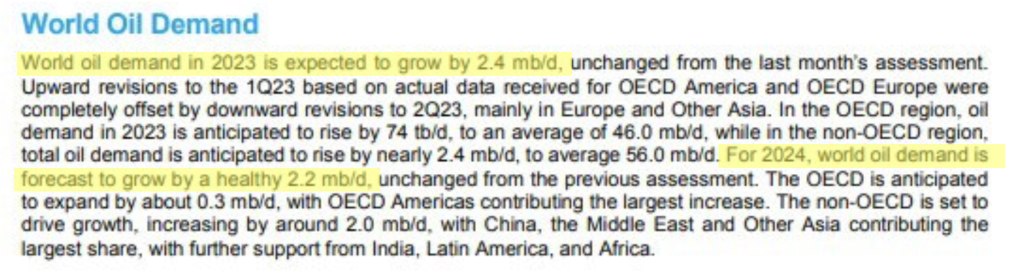

Great. Fantastic. That’s so good to hear because, again, we see all these polarized views, everyone trying to make their market, and so it’s really good to hear that refreshing perspective. Thank you, Joseph. Thank you very much. Hey, Tracy, let’s talk about oil and gas markets a little bit. You were telling me this week about the OPEC update that came out, and the report says that demand will grow by 2.4 million barrels per day this year and 2.2 million next year.

With OPEC supply cuts that are still underway in Saudi Arabia just extended—we talked about this last week—how big do you expect the supply deficit to be this quarter?

Tracy

Well, I personally think that it’s going to be about 2.1 million barrels a day. We did have IAEA come out. They think it’s going to be about 1.7, which is actually huge for them because they become the anti-oil and gas group. They’ve been on that trajectory of we only need renewables. To them say that they expect a deficit as well as they also are expecting an increase in demand is quite impressive for that particular organization. But if we look, we have demand at 103 million barrels a day. That’s literally all time highs well above 2019. We’re not seeing demand diminishing at any time and both groups because the IAA report just came out this morning. Both groups expect an increase in demand at 2024, although IAEA has pared back their initial estimation from the last report that came out. It does come in a bit lower than the OPEC report, but that generally is the case. They’ve been very conservative on their demand estimates.

Tony

Where is that demand coming from?

Tracy

Well, particularly in Asia. We’re seeing a lot of flows in Asia. Obviously, we’re not really seeing a lot of that demand come from Europe as we see manufacturing slowing down. But we are seeing demand growth in the United States. It’s coming in month after month. We’ve had upward revisions from the EIA. Demand continues to be very strong and to increase every month in the United States. Really, the areas that we’re looking at where we’re seeing the softness in demand is really just coming from Europe at this point.

Tracy

I think that going forward, I just wanted to bring China into this a little bit because we just had China’s seaborne import numbers come in. They slump below 10 million barrels a day, which is down toward July, which is down about 13%, month-over-month from June three-year highs, which is very high. Meanwhile, their onshore crude stocks have climbed at a rate of about a million barrels per day for three straight months. Not surprising, China likes cheap oil and gas. That means that-.

Tony

I do too.

Tracy

They also had refinery throughputs were very low during the spring turnaround season. We’ve also seen a slow recovery in domestic demand, particularly from the manufacturing sector. I think that we should be prepared to see a little bit of slowdown going into the fall of Chinese imports as prices rise because they’ve already built up that socket. Although I don’t think their teapot refineries and their state-owned refineries still have quotas that they have to keep up with and export quotas are coming out in a couple of weeks here. We’ll find out how much if their export quotas for diesel increase, that means they’re going to likely have to buy more crude. Now that depends and where are they going to get it. Because right now what we’re seeing with lower Russian crude supplies, the tea pot refiners are basically leaning deeply into discounted gray market, uranium oil right now. Just that’s the general picture of what’s going on in China right now. Again, I would expect to see imports from China soften for the rest of H2.

Tony

Okay. The demand is coming from the US and from Asia. Is China back to 2019 levels? They’ve exceeded it?

Tracy

No, not yet.

Tony

Okay. How far are they? Are they still a long way or?

Tracy

No, they’re not a long way, but they’re definitely a couple of million barrels a day below what we’re seeing. Again, because the manufacturing sector, again, because we’re not really seeing that recovery, they’re doing a lot to stimulate some demand. They just took off the airport, the airline travel restrictions for international flights and things of that nature. But you know what’s going on with China right now with the property sector still in the shambles.

Tony

We’re at 103 million barrels and China is not up to… That’s a record and China is not up to 2019 yet. Is most of that growth the US?

Tracy

A lot of it is going to the US and a lot of it is coming from other PACAC Asia nations.

Tony

India, other places?

Tracy

India, Vietnam, Thailand, Malaysia. We’re all seeing growth in those areas.

Tony

Very good. Okay. With this growth, how do you expect that to impact… With the supply deficit, how do you expect that to impact crude prices? Of course, there will be upward pressure, but how much upward pressure are you expecting?

Tracy

It depends. Again, I think we talked about this last week. Nobody wants oil prices to spike over 100. It’s bad for everybody. It’s a bad for economy. Price, and it’s bad for OPEC because nobody wants their product and can’t afford it. I think they’re going to do their best to regulate the market. But I think that we’re in a era of higher for longer right now. I would not be surprised if we stayed again in that $80, $90 range for Brent, which OPEC is very comfortable there.

Tony

Okay, great. Can I ask you a question about EIA report? Because you put stuff out on this every week and it looks like US production is rising. Why is that happening?

Tracy

It’s not.

Tony

Oh, it’s not.

Tracy

Okay. It’s the weekly reports. It has been rising. It has been rising for the first half of this year. But I would pay attention to the monthly reports and not the weekly reports, even though they’re lagging by two months because it’s pretty much just a guesstimate. What we are seeing right now, and from what I’m hearing within the industry, is that all those rigs that have been coming offline all of this year are starting to impact production. That is not surprising. I think that we’ll probably see decline starting in August.

Tony

Okay.

Tracy

Headed into the fall as far as US production is concerned.

Tony

So less US crude output.

Tracy

I believe so for the second half of this year.

Tony

Second half of this year. Okay, very interesting. Thank you for that. Thanks very much for that.

Tony

Stay on energy, Ralph. You put out a report, I think it was this week, looking at why Europe needs nuclear. We’re really interested. You did it through this organization, MCC Brussels. It’s an amazing read, very interesting. I’d like you to make the case for us of why Europe needs nuclear. I’ve got a couple of charts to look at.

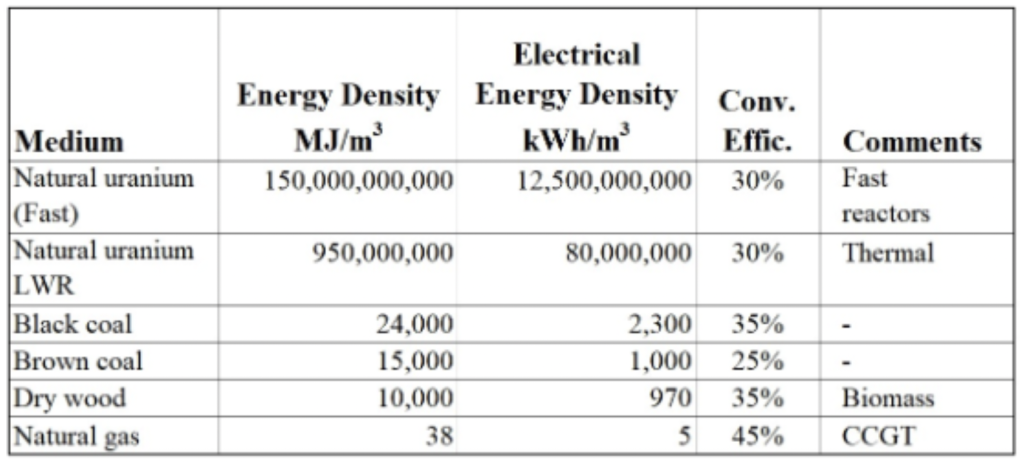

The first one is looking at energy density of nuclear versus other stuff. Why is energy density important? I know maybe that sounds a bit stupid, but what does it mean and why is that important?

Ralph

Actually, it’s a fantastic question to start this conversation. Just to give you a number that I think really highlights this. If we take uranium as the most commonly used main resource for nuclear power plants, pound by pound, they produce 16,000 times more electricity than, for example, coal does. I think this just gives you a little bit of an impression of the tremendous energy that is contained in the potentially nuclear power plants. There’s a famous letter that Niel Sboar wrote to Winston Churchill in 1944 where he informed him about the Manhattan project. He basically talks in the entire letter about the energy content that can be released via nuclear fission. This is, on the one hand, which many critics correctly point out, a fairly, quote-unquote, old technology, the first fission took place in Germany in Berlin in 1938, and only seven years later, devastatingly. But the time frame, it was actually very tense. We had the first two detonations of nuclear bombs, of course, in Japan by the US military. But that shows you that we had the technology for a significant amount of time. The reason why I’m mentioning this is because very often that is used as an argument against nuclear.

Ralph

It’s like yesterday’s technology. I think it’s actually making the case for nuclear because the point is we actually know how to do it and we have been pretty good at it. Just to give you two examples. The Canadians in the 1970s, they basically built a new reactor every year. The French in the ’70s did the same thing. The French had one of the least carbonized or one of the most decarbonized electricity grids in the world that really was a nuclear success story. We see the same now in the province of Ontario. I don’t know how many of you viewers and listeners are following Canadian politics. Usually, that doesn’t sound super exciting. I guess for Americans, the idea of Canadian revolutionaries is something like an oxymoron. But there was something…

Tony

They see like a Canadian expert.

Ralph

Well, there you go. At least we have won on our side. In Ontario, that basically was something like a small energy revolution with the new government by the, in my opinion, hilariously named progressive Conservatives of Doug Ford now pretty much abandoning, actually deliberately repealing the so-called Green Energy Act the province has adopted. In 2009, they have now repealed it and they want to go back all into nuclear. Sweden has now announced they want to build 10 new additional reactors. Pretty much the only outlier here is always Germany. But of course, since Germany is Europe’s most important economy, it matters what they do. But just very quickly, for one second, go back to the tech logic part. I’m a political scientist. I’m not a nuclear physicist. People say, Oh, how can you talk about this? That’s a fair criticism. This was my biggest fear when I wrote and when the report was published and when I was reaching out to get input that I will get huge pushback from people who really know the technicalities of it. But they pretty much all agree. You will not find a nuclear physicist who will tell you that, for example, producing electricity via nuclear power is a bad thing.

Ralph

They will say there is regulation that makes it uneconomical. They will say that the political conditions are against it. But nobody will say, Oh, no, we actually have better means of producing electricity because we really don’t. When it comes to this one thing, it is the best available. Yes.

Tony

No, that’s the case, Ralph. I know Germany and Italy and other places closed nuclear plants after Fukushima in Japan. Why did they do that? Was it just such a bad investment or return? Or was it just political sentiment? Why did they do that?

Ralph

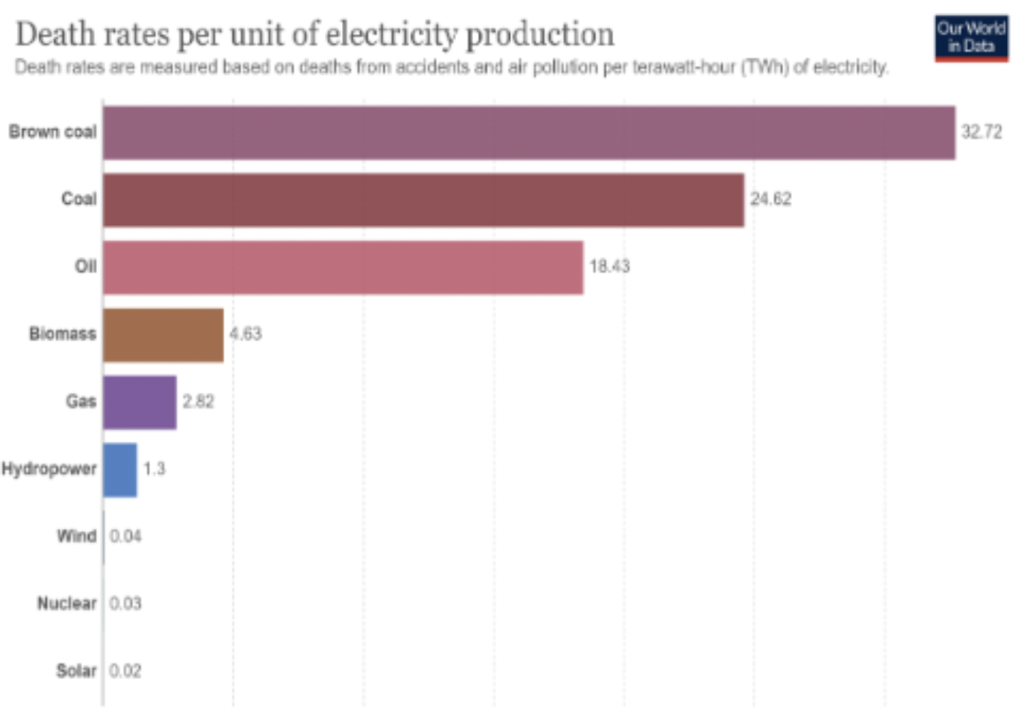

Now, I usually refrain from hyperbolic statements because I think it embodies the debates. But if we take Fukushima and Chornobyl, those are the two examples. Fukushima, and this is factual, this is from the Japanese authorities. One person allegedly, supposedly died seven years after the incident after cancer that developed potentially because of radiation. They really had to get to a huge stretch to find one casualty of after what happened in Fukushima, which really was a once-in-a-millennium tsunami. Again, you could say Fukushima tells you stop nuclear, but I think you can make the opposite case, that nuclear power plants, their quality has gotten so good that they pretty much survived a tsunami with barely anybody dying. Just to give another example, in the 1970s, I can’t speak Chinese, so I’m not saying the name of the dam because I’m probably going to ruin it, but a dam broke in China that killed between 26,000 and 240,000 people. Again, the numbers were let’s take the lower end. Let’s try to be very conservative in our estimates. Twenty-six thousand people died. We have millions of people today living in areas close to hydroelectric plants to dams. Nobody is terrified of it, but they are theoretically, or by body count, if we want to use that crude measure, they are much more dangerous than a nuclear power plant. What I’m trying to say is…

Ralph

Let’s take a look at that.

Tony

Yeah, let’s take a look at that, actually. You had a good chart looking at the death rates per unit of electricity production. It seems a little bit grim, but it’s very interesting looking at coal, oil, biomass, gas, hydropower, and so on. And so… Obviously, nuclear is very, very low. There are more deaths by wind than there is through nuclear.

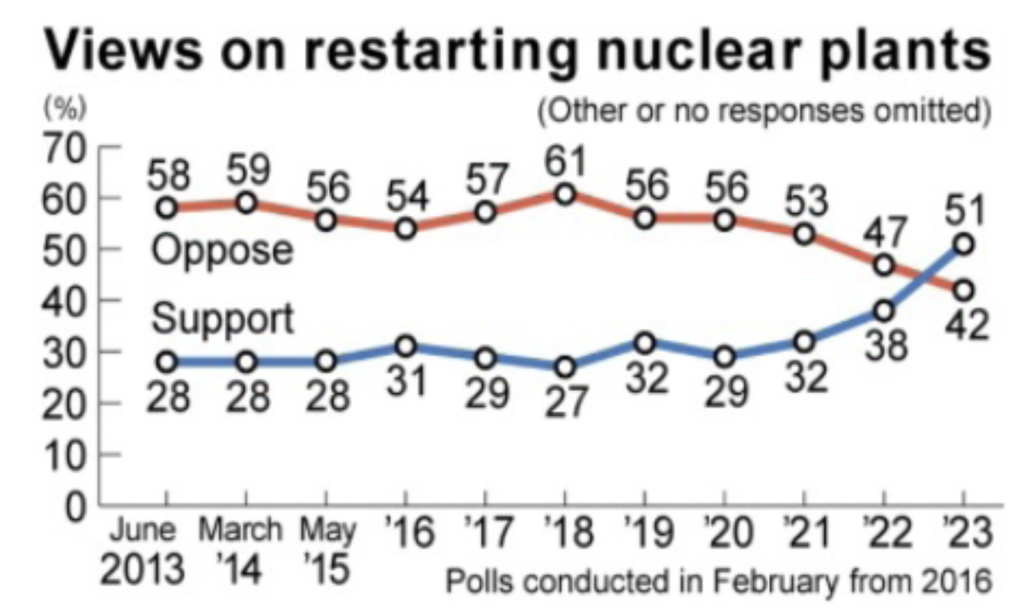

And so I asked the question about why did Europe, or at least Germany, Italy, and some other places closed down some nuclear plants? It looks like polling is showing that people in Europe are more open to reopening or restarting nuclear plants.

Ralph

Yes, that’s true. I think the main reason is that this was a hyperbolic part because people were, for lack of a better term, I would say they have been lied to or they have been brainwashed. Let me give you another example just recently. All of you American listeners probably know Tulsae Gebert, the one—and I don’t know, she’s still a Democrat, she’s not a Republican—but the little bit of a firebrand and she’s very entertaining. But she had this massive tweet where she said, President Biden must do something because Japan is releasing former cooling water in Fukushima back into the Pacific Ocean and this will have a huge impact on the food supply in the Pacific is going to be radiated and everybody is going to die. The one good thing that Elon Musk did with X, formerly Twitter, are the community notes because the water that the Japanese are releasing is better than the drinking water quality in most European cities. A banana and a beer, if this is your diet of choice, will expose you to more radiation and that water. But people are just saying it. It’s just this comment, days, nuclear was involved, it must be deadly.

Ralph

This is really the mentality that most Europeans have imbibed. But what last year, of course, did with the energy crisis is that all of a sudden people realized, Wait, give me a moment, if my electricity bill, my heating bill doubles or triples, if all of a sudden I cannot simply rely on a plug in my gimmicks and they work? Then you take a second look at this and you say, Well, but okay, like microbial, which by the way, just as a quick add-on, was a fact of mostly producing plutonium for the Russian military. It was a sidekick, was the electricity production, at least in the reactor in question. People say, But does that really also apply to German reactors? Does that apply to Swedish reactors? Does this apply to French or Canadian reactors? And people, good for them, they are taking a second look and just as a last point. It’s good that they do because we need, and I think also what Tracy said, really dovetails with this or actually precedes this, the world remains hungry for energy. The International Energy Agency pretty much, I think what did they say? They said peak is going to be in 2019, and by 2030 it’s going to be at 75 million barrels a day or something.

Ralph

Now it’s like, “Oh, it’s probably going to be 105 million barrels per day. I’m sure that in four years they’re going to say it’s going to be 120,000,000 barrels per day.” The world needs that energy. The last point, the argument that, Oh, forget about nuclear, wind and solar can do it. I’m an agnostic when it comes to energy. If we get the solar energy to really harness the power of sun, radiation, I’m all for it. But currently the capacity factor, basically the factor that says what is the percentage of the ideal conditions under which an electricity producer produces electricity? For wind, onshore and offshore, depending where you are, it can be up to 30% to 40% and the ideal conditions. But for example, solar in Europe is 11 or 12%.

Tony

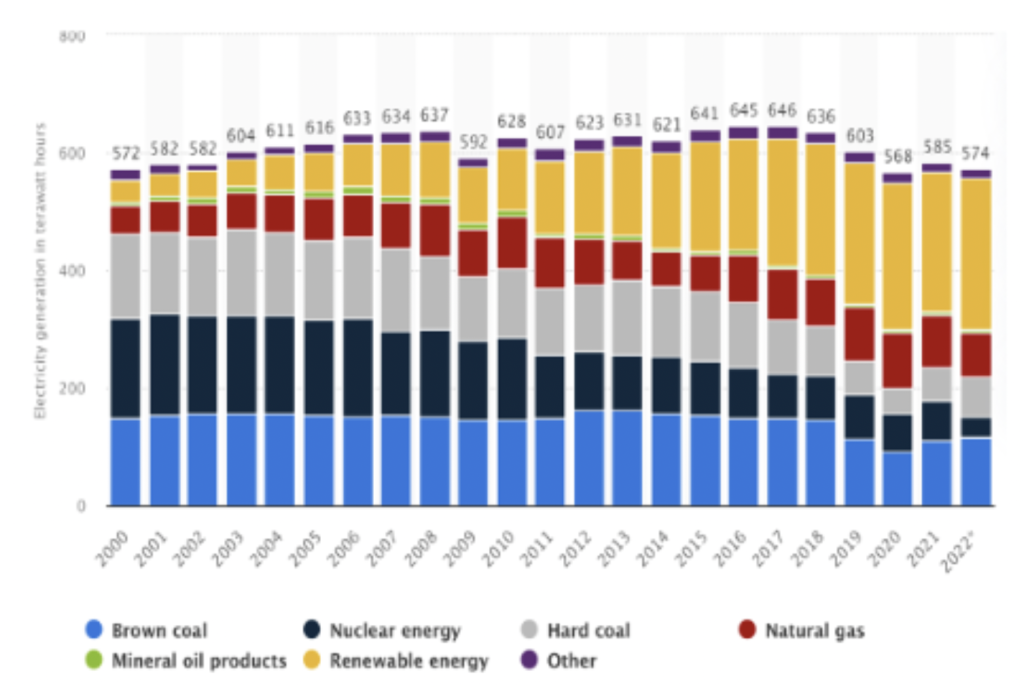

Let’s talk about that. While you’re on that, let’s talk about the German energy mix. Since Germany is the manufacturing driver of Europe, you have some charts in on the German energy mix and energy prices. It was really great to have those side by side.

Can you talk a little bit about how renewables came in in Germany and then what happened to energy prices in Germany?

Ralph

Yeah, this is another one of those stories. I think Tracy recently posted a picture of, I think, a new Ford electric vehicle that cost $150,000. The reason why I mentioned this is because what they do, for example, in the EV sector is very often they never tell you how many EVs they sell. They only tell you their percentage change. They sell one EV this year, they sell two next year, and the headline is EV sales increased by 100%. This is the same thing they did in the German electricity market. Everybody now says, Ralph, what you’re talking about nuclear? Look at it. Now, 65% of electricity in Germany is produced by wind and solar. Yes, of course it is. If you take everything else that’s not wind and solar, you’re going to end up with 100% wind and solar. It’s just going to be hugely expensive. This is the other trick they say, they only look at electricity produced. They don’t look at electricity consumed because they don’t tell you that Germany is now buying energy or electricity, to be precise, from the Czech Republic, from French, and from other states. This is a game with numbers in defense of particularly wind and solar, which I believe, and as I said, I’m an agnostic.

Ralph

If they improve these technologies or if we finally get these miraculous batteries that we’ve been promised now for 20 years, that’s the game changer. If the technology changes, I’m the first one to say let’s look at this again. But at the moment, it’s statistical tricks that try to basically justify one inferior form of electricity production to a superior one. It’s the same thing. I always get down these emails that says, Well, we modeled. We have this model that says that Germany can run 100% on renewables. But I think they are running the experiment right now. I don’t need your model. They are trying it while we speak and it’s not working. It’s the same. You have some guy who is in reality and then the other one waves to study at him and says, But your reality is wrong. It’s very Hegelian, it’s very German in a sense. This idea that reality has to adapt to theory and not the other way around. This is a little bit. Yeah.

Tony

Do you know how much governments in Europe have put toward renewable energy in the last 20 years? I’m just curious if you know that number. It’s got to be hundreds of billions or trillions, I would think.

Ralph

There are different estimates. In the last 12 years, I think overall we’ve spent worldwide four trillion. The bulk of this was spent in Europe and China. I can’t give you the precise numbers. Again, because a lot of this is done, let’s say, directly and indirect financing than the whole subsidy scheme. It’s very tricky to get the real numbers. I think they are much higher than we think. It shows you another thing. I know that you know much more about China than I do, so I hope that we can have a conversation about this one day as well. But this is another thing. I say, Look at China. Look how massively they expand their renewables. Which is true. But if you look at the numbers, I think Dr. Anesh, recently in a podcast said that I have very much faith in the things that he says—he says if the Chinese would keep up expanding their renewables as they do at the moment, and if we assume that they don’t have to be replaced, which is of course a huge assumption that is unrealistic, as he himself says, it would take them 211 years to go fully renewable.

Ralph

Even the world’s leading spender on renewables, and they know this, this is why the Chinese still invest in coal and still invest in nuclear. Europe is a little bit in the energy sector. The shift is happening. It’s like an ocean minor that tries to turn around. But as a concluding remark, without energy, de-industrialisation is a fact. Again, we can turn and twist the numbers. We have the statistics, we have the numbers, we know what the companies are doing. We know where BASF is going, we know where other companies are going. This is a very harsh reality. So far, again, if this is possible one day, I’m the first one to be for it. But so far, the favored sources of electricity and energy have not delivered what they were promised to be capable of.

Tony

It looks to me, based on your charts, that as renewables have taken over more of the fuel source in Germany, prices have risen by 70, 80%, something like that. Given the subsidy that’s gone in from European governments, it just seems odd that that’s the return. The 90% rise in energy prices.

Ralph

Just as a quick thing on this. As I always say, I’m an agnostic on this, but it’s frustrating in the sense, particularly for consumers. We constantly hear with this border fraudulent way of calculating it, the so-called level cost of energy. We are constantly taught that wind is the cheapest of all forms, followed by solar. But every statistic we look at, Germany, Denmark, Great Britain, everywhere, cost of electricity increased proportionately with the share of renewable. Again, as an agnostic here, but somebody needs to explain this to people. They see the large electricity bills and people on TVs, they’ll tell them, Oh, this is also cheap. It’s amazing. Well, okay, then where is the cheap electricity? This is, I think, the frustrating thing.

Tony

I live in Texas, so I’m shamelessly pro-oil and gas, but we have, I think, the largest wind energy field in the US. That started, I think, in 1995 under a guy, an obscure guy we used to have as governor called George Bush. He started that program for the Texas government. We have one of the largest wind fields in the US, but we still struggle every year to get it to take over an increasing proportion of the grid here. Increasingly, natural gas is becoming the no-brainer solution for us, although we spend more on alternatives here in Texas, but the reliability is in things like net gas. Look, my bias is out there on the table. If something’s better, I’ll take it. But it sounds like Europe’s gone to the point where alternatives have hit a wall for now and they really need to do look at a different energy mix. I think your report, I’d encourage everyone to check it out. I think it’s very, very interesting. I think every nuclear investor, which I know there are a ton of really aggressive nuclear investors out there, they should read your report and they should just throw it out to everyone that they know so they can all read it.

Tony

So very good. Guys, this has been fantastic. Thank you so much for taking your time. I know we’ve covered a lot, and I really appreciate your time, guys. Have a great weekend and have a great weekend. Thank you so much.