🔥BLACK FRIDAY SALE!🔥 80% OFF CI Markets! Get it for only $99/yr: https://bit.ly/3uscpEI 👈 🔥 Promo ends Nov. 28th ⏳

Welcome to “The Week Ahead” with your host Tony Nash.

1. The Upcoming USD Squeeze. Michael Ncoletos discusses the potential impact of a US dollar squeeze on the global economy, focusing on the factors contributing to the potential strengthening of the US dollar and its implications on emerging markets, particularly about their dollar-denominated debt. He also highlights the significance of interest rates and the cost of money in determining investment decisions.

2. Year-end market check. Bob Iaccino discusses the current state of the markets, emphasizing the impact of higher interest rates on the tech sector and the significance of the energy market in relation to inflation. He also mentions the potential impact of technology stocks on the economy and expresses concerns about the future performance of tech stocks in 2024, particularly in the second half of the year. Additionally, he discusses the potential for Argentina to dollarize its economy and the challenges and potential for success of a conservative government in Argentina, drawing parallels with other countries and global political trends.

3. China, US & geopolitics. Albert Marko discusses the recent election in Argentina and expresses skepticism about the potential for significant change under the newly elected leader, Milei. He mentions that Argentina is burdened with a significant amount of debt and that it would be challenging for Milei to make substantial changes without a strong support structure or clear policy direction. Marko also raises concerns about the influence of leftist forces in Latin America and suggests that Argentina may be set up to fail. He expresses doubts about the feasibility of Milei’s plan to dollarize Argentina given the country’s debt and limited dollar reserves. Overall, he indicates a reserved judgment on Milei’s potential impact and suggests that the composition of Milei’s cabinet would be crucial in determining the direction of Argentina’s policies in the next 12 months.

Transcript

Tony Nash

Hi everyone, and welcome to the Week Ahead. I’m Tony Nash. Today, we’re joined by Michael Ncoletos, Bob Iaccino, and Albert Marko. We’re going to talk through the upcoming US dollar squeeze, which Michael has just published a stellar piece on this. We’re going to talk with Bob about year-end markets and see what we’re heading into. Then we’re going to talk to Albert about some geopolitics, specifically about Argentina, but how does that apply more broadly? Looking forward to the discussion. Guys, thanks so much for joining us.

Tony Nash

Hi, everyone. We started our Black Friday sale at Complete Intelligence, and you can subscribe to CI Markets for $99 for the whole year. That’s 80% off our normal price of $500. Starts today, and it goes until November 28th only. Go to completeantel.com/BlackFriday and subscribe to CI Markets for $99. Thank you.

Tony Nash

Michael, actually, you and I met a few years ago when I was giving a presentation on China, and I used one of your charts on the weakening advocacy of Chinese debt issuance. It was so great that you were there. I didn’t know you were in the room, and the humility you had around that was just astounding.

Tony Nash

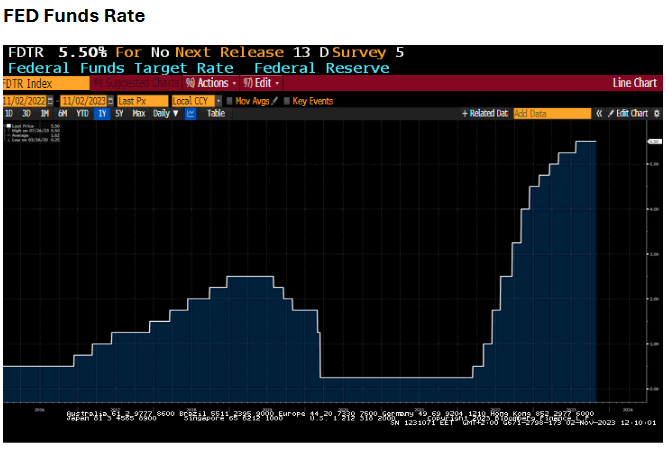

I follow you really closely. And we’ve been talking about the dollar for a long time. Albert talks about the dollar a lot, and you published a paper a couple of weeks ago about the coming US dollar squeeze. This is really, and pardon me for oversimplifying it, but it’s really a story of interest rates and viable alternatives to the dollar. Obviously, there’s a lot more to it. You outlined a seven-step process. Would you mind walking us through that? I’ve put up a chart on the Fed funds rate to get us started. Would you mind walking us through each of those steps as an overview?

Michael Ncoletos

First of all, it’s great to be here. I also enjoy your work, so I share your thoughts about your work, and thank you for sharing with everyone and love the discussions we’re having. But sometimes you bump into someone by luck. I think we bump into each other by luck. That’s right. I think it was in the came of Ireland, right?

Tony Nash

That’s right. That’s right.

Michael Ncoletos

I’m Greek and you’re from Texas, right?

Tony Nash

Yes, that’s right. Worlds of way.

Michael Ncoletos

We met in the came of… That’s-

Tony Nash

Not a bad place to me.

Michael Ncoletos

How small the world is. A few weeks ago, I was thinking about the dollar, which I’m one of these people who think that the dollar is unlikely to weaken unless the US government or the US Fed decide to do so. And the thinking is we’ve been reading a lot about the US deficits, about the situation in the US and fiscal responsibility. And we’ve seen a lot of people talking about the new currency, the BRX currency that could replace the US dollar as the global reserve currency. So I try to lay out why I think the dollar is not going to go lower. And by lower, I mean it’s going to squeeze higher for a few reasons. After a 13-year expansion of the US balance sheet, which I think the balance sheet reached around $9 trillion, if I’m not mistaken, the Fed decided to stop that and to start raising rates and then to start QT. So in the first phase, the Fed just started raising rates. And by that when you raise interest rates, you effectively drain liquidity from the world in the US dollars because a lot of dollars, as simplified as that can be, are going to go to the currency which has the higher interest rate, assuming that there are no capital controls or nothing else.

Michael Ncoletos

So that was the first step. The second step was that the Fed stopped QE. And by stopping QE, stopped reinvesting the treasures that you had bought and the mortgage-backed securities, which again by stopping reinvesting means that these new issuance need to be bought by the market. So when the market needs to buy them and it’s not the US government, more dollars are used for that. You need dollars from the market which would be used for something else to buy these treasures and these mortgage-backed securities. Then the Fed moved a step further and started QT, which means it started reducing its balance sheet. But when you reduce the balance sheet again, which means you need more money from the market to start buying these treasures, more liquidity started to drain. Now to put all this together in an economy that is going through, let’s say, a Cold War, you want to put it this way with China, in a world where there is reshoring and in a world where there are a few wars going around. So there is a supply issue in terms of how inflation is created. You have less oils and oil prices go up.

Michael Ncoletos

You’ve had an inflation scare across global which has translated to real inflation. Now, in normal conditions, when you have a supply-driven inflation, the remedy is not to raise interest rates because monetary policy is effective when inflation comes from the demand side, not when it comes from the supplies. The Fed of San Francisco published a research paper a year ago, I think, showing that two-thirds of the inflation in the US was coming for supply reasons. So the question I ask myself is if what I’m saying is correct, and I’m pretty sure the people of the Federal Reserve are pretty aware of it, why are they raising rates and increasing the deficits when this is clearly not going to do much on the inflation side. Okay, we’ve had the pause, we’ve had an inflation coming down, but we need to see where it’s going to stabilize. So the question is, when you have fiscal deficits and fiscal deficits are around seven and eight % of GDP and you don’t have the central bank buying treasuries to fund that deficit, it means that these bonds, which according to a report I read, I think next year it’s eight trillion, eight trillion need to be financed from the US government.

Michael Ncoletos

So eight trillion dollars need to be found from the global market to fund that deficit. Now, most people are aware of the dollar and how it works, but most people are not aware of the Euro dollar market. You’ve raised it a few times, but most people don’t understand. The Euro dollar market are effectively all the dollars that are not included in the US M2. We can go into specifics what’s included and what’s not. It’s very technical, but I don’t think it doesn’t make sense to do this discussion on. So all the dollars that are not included in M2 are the euro dollars, which are outside the US, which it’s equivalent in size of the US dollar mark. So M2 is around 20 trillion. Imagine that there’s another 20 trillion or maybe more outside of dollars. So what’s the problem with that? When the dollar goes up, you effectively create an issue, especially on emerging markets. Why do you create a problem in this emerging market? Emerging markets because they do not have hard currencies, tend to issue debt in dollars. They tend to issue debt in dollars, the interest rates go up, their bonds go lower, so they have a funding need.

Michael Ncoletos

They either need to put dollars in to bridge the gap or they need to start selling bonds. It’s not as easy as one would think.

Tony Nash

Michael, let me… Let me just pause there and ask you a couple of questions. You said the US needs to raise $8 trillion in debt next year. Is it possible to have a failed auction?

Michael Ncoletos

I guess it could be, but why would there be a failed auction? The rate, the interest rate will go high.

Tony Nash

Right, that’s the answer. I hear a bunch of the dollar naysayers go, Well, the US is trying to put so much debt out there, they’re just going to have a failed U. S. Treasury auction. But what you’re saying is, no, they’ll just… The U. S. Will just offer a higher interest rate on that in order to sell that. Is that right?

Michael Ncoletos

Yeah. Let me put it this way. There is this chart floating around, especially on Twitter about the liquidity of the U. S. Treasury market. This is ridiculous, and I’m saying it’s ridiculous because the U. S. Treasury market has an average trading volume of like 15 trillion a month. The next one, the next one is the eurozone with six trillion, and then it’s Japan with three and China with two trillion per month. So if US dollar bond liquidity is going down, imagine what’s happening on the other markets. We’ve seen the Japanese bond market are not trading for a day. We’ve seen no… When we talk about liquidity, and I’m not saying that liquidity is going up, I’m saying it’s going down, but it’s a relative discussion. It’s not an absolute discussion.

Tony Nash

That’s key. And everyone understands.

Michael Ncoletos

What does that mean? You’re going to buy what? Japanese bonds.

Tony Nash

Currencies are relative. It’s all relative. And I think that’s something.

Michael Ncoletos

That currency are relative. And what’s more important, people need to understand that the dollar disposition is a derivative of the US capital market system. The US capital market system is so efficient, at least in terms of anything else that we see right now in the world. So when a government, whatever government buys trades in US dollars and accumulates US dollar FX reserves, they can buy at the split of a second US treasuries, and they can sell at the split of a second US treasure. There’s no such issue. Now imagine doing the same, accumulating one, for example, or rubles and FX reserves, and then one day needing to sell them, A, there’s no liquidity. B, if you manage to sell them, there are capital controls. You need to take them back. How will you take them back when there’s capital control? So the most… The next most efficient is the Eurozone. And the Eurozone is not one market, it’s Germany, France, Italy. So when we talk about the Eurozone, we’re not talking about the 20 countries. We’re talking about three or four countries within the 20 countries. So again, when we talk about the US dollar, it’s a relative discussion, but it’s also a relative discussion of the capital markets they are representing.

Tony Nash

Right. Okay, good. I just wanted to get that out of the way..

Tony Nash

The other point I wanted to raise was you said emerging markets need to raise their debt in US dollars. I don’t think that’s really well understood by a lot of people. So if you’re in like an Indonesia or Sri Lanka or whatever, if you need to sell debt to international investors because you’re not really going to raise that in domestic markets, are people overseas going to take the currency risk along with the sovereign risk?

Michael Ncoletos

Well, let’s put this. Turkey has interest rates at 30%. They should debt at 30% or are they going to issue debt in dollars, which would be at like 6, 7%, whatever the number is right now. They’re going to try that and they’re going to hope that the economy recovers. And as the economy recovers, their currency is going to become stronger. So the debt repayment is going to be cheaper. In theory, all very nice. But when the dollar goes up, it creates a squeeze on the world, on the growth, on the collateral, on everything, which makes things much worse for all these countries. Unless they have current account surpluses, which once they have, they can sustain that period for a longer term than the others. But again, they’re going to get squeezed as well. There is no hope. So all these countries that raise debt, dollar debt or foreign-denominated debt in the last 10 years because rates were at zero, now are facing issues because what we’ve seen the discussion that happens right now in US banks about the collateral that banks have and that the treasures that they hold have a mark to market loss, as we’ve seen, which effectively that doesn’t…

Michael Ncoletos

It’s not the case because the Fed made a…

Tony Nash

BTFP.

Tony Nash

BTFP, which they accept at face value the bonds. Now imagine what the US banks are facing, countries facing it without the BTFP to protect them at face value and with them needing to refinance that debt at the worst possible time. So if you’re asking me, the squeeze will not go in the liquidity of the US Treasury Bank. The problem would be in Turkey, China, Russia, Indonesia, Egypt, these countries and all the others are going to face Argentina. They’re going to face issues when raising debt because their capital market is not deep. When you buy these bonds, you marry them. If you don’t marry them, you’re going to be selling at a deep discount the day you decide to sell them. Okay, and you have more issues. So we tend to talk about the US. And I want to make a point. The US financial situation is not good. Definitely, and I’m not saying it’s good, but I’m saying the way the world is structured and the US being the global reserve currency, it’s less bad than whatever everyone else is facing.

Tony Nash

Yeah. I hadn’t thought about the sovereign debt issues before today, but now that you mentioned that, that’s Silicon Valley Bank all over the world at a central bank level, right? At a finance ministry level.

Michael Ncoletos

Let me put it simple. I’ll put it as simple as possible. When you can buy US treasury two year treasure, 4.9 %, 4.92 %. So five %, let’s say five %. You buy 5%, you buy US treasures, the safest asset in the world. You gain 5% a year and you sleep like a baby. So when you invest, you need to think, is there something that’s going to give me a higher return and it will be relative to me sleeping like a baby and gaining 5%? This is as simple as that. Because if I’m gaining 7% and I’m not sleeping at night, it’s not worth it. I need a higher return, and this higher return goes with the countries that are hard to find the finance.

Tony Nash

That’s right. Bob, what do you think about this?

Bob Iaccino

Well, I think the perfect end to that extremely impressive summary of what’s going on in the global markets is the sleep at night part that a lot of investors seem to ignore when we’ve gone through, let’s just call it multi-years bull markets and equity assets. Because they tend to… Investors tend to forget, and I’m speaking a little bit more to retail because I believe institutional investors know it, but sometimes they don’t. Let’s take the example of the hedge fund, for example. Hedge funds are supposed to perform when equities are performing, and they’re supposed to outperform when equities are collapsing. One of the things I like about this format versus the traditional financial media that unfortunately I’ve been a part of in theory since 1999 is that they tend to have this view that positive performance is the only performance that matters, and outperformance, they’ll put somebody on TV and they said, You’ve outperformed the S&P this past year. The S&P is up 12%, you’re up 15%. But when the S&P is down 24 %, and that particular person is down 18%, they’ll come on and say, Well, you’re down 18% this year. Well, you’re still outperforming to the opposite side.

Bob Iaccino

It’s one of the things I talk about a lot, and I’m digressing a little bit, but outperformance to the downside to me is much more important than outperformance to the upside. To Michael’s point, if you can make 5% and sleep at night, that to me is worth an extra 5%. That’s just the way that my internal math works. It’s not some technical formula that I can explain. You need to double my return to take away my sleep at this point in my career is basically what I’m saying.

Tony Nash

Yeah. Our traditional investors, are they looking for 30% returns a year? They’re not necessarily looking for 30% returns a year. That’s crypto level, right?

Bob Iaccino

When I was part of the investment committee of the fund to funds that I was a principal at, we went into these big investors. I’m not going to mention the fund because it’s dissolved at this point. But we had 10 years of returns where our worst year was down 46 basis points. Our best year was up 8%. That was what the fund was designed to do. But when we went into large, large allocators, they would say, God, I just love your returns, but you represent nothing but risk for me. Why? Well, because you don’t have a lot of money under management at this point, and we worry that allocating to you would affect your performance, which it would have, but whatever, didn’t happen. That stuck with me for a very long time where these large institutional asset allocators are very worried about sleeping at night because their management fee matters more so than beating their last year’s performance by a % or two. That’s something a lot of investors don’t understand. Again, I’m digressing a little bit, but it goes to the point of how much it matters that the safest asset in the world is between four and a half and 5% depending on what duration you put on it.

Bob Iaccino

That matters a lot, and that will continue to draw very large capital for a long period of time. That capital won’t necessarily leave those assets for a 25 basis points here or there or 50 basis points here or there.

Tony Nash

Interesting part-.

Michael Ncoletos

Can I add something, Tony?

Tony Nash

Absolutely.

Michael Ncoletos

I think we’re 100 % involved. You’re being paid to wait for the first time in your life after 20 years. You’re being paid to wait.

Bob Iaccino

That’s a great. Way to put it. That’s a great way to put it.

Michael Ncoletos

You’re being paid to wait. For the last 20 years, this hasn’t happened. So you’re being paid to wait. And when there is a correction, if there’s a correction or if there’s a recession, or there’s a depression or whatever, I won’t go into what could happen, you will have money on the side, being paid and being able to deploy it as you wish, having the most liquid asset in the world, which at that point would probably rally, which you’ll be making a couple of gains as well. And you’ll be doing the best thing you can do.

Bob Iaccino

If I can add to that, Tony, we have five trading days left in the month of November. Really four. Friday is a lost day, so to speak. We have four or five trading days left in the month. Let’s call it four and a half in the equity markets. You’re about to post your greatest November percentage-wise on record to the upside for equities. The volume is barely half of what it was in October. Now, it’s not going to make up the rest in four trading days. I guess it theoretically could, but it’s not. What does that tell you about the overall stance of the institutional investors? Honestly, in huge dollar amounts, they have not been involved. Because what Michael said, they’re being paid to wait. If you look at the overall makeup of this particular earning season that we’re basically finished with, it’s been good. But we have the weakest buyback numbers announced since 2016. We have the largest negative reaction on individual stocks that have missed earnings expectations since 2011, largest drop on misses. We have the largest cut to estimate since the second quarter of 2020. What does that tell you that these analysts and these investor relations parts of these large companies are thinking?

Bob Iaccino

They’re worried. They’re not mentioning recession as much. As a matter of fact, the lowest mention of the word recession, I believe since 2022, but they’re not positive overall, even though there’s beats on the outright figures.

Tony Nash

Because the risk appetite is mitigated by what Michael is talking about.

Bob Iaccino

By what Michael is talking about, exactly.

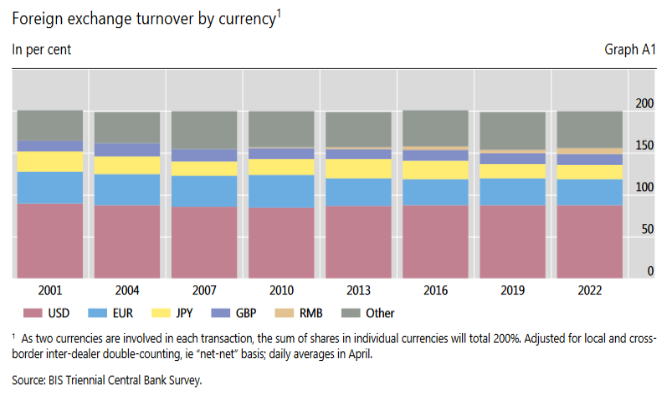

Tony Nash

It’s great. Let’s get back to this USD thing for a few more minutes, and then let’s move on to markets and talk real deep with Bob. Michael, you have chart showing the foreign exchange turnover by currency. Of course, it’s overwhelmingly USD. Of course, we’ve had some growth in CNY since, say, 2010. But on a relative basis, where is that CNY taking market share from? Is it taking from British pound or where is it taking that market share from? Is it from the dollar?

Michael Ncoletos

I think I say mostly from the euro.

Tony Nash

From the euro? Okay.

Michael Ncoletos

Yes. But again, China has done like 40 swap deals since 2016. They’ve been trying to make their currency more usable, let’s say, as simple as that. But again, everyone who trades in China and Yuan, they will do it at the equivalent of a Barker size trade. They will not do the extra mile to accumulate the FX to zero. So if I’m buying 10, selling 10, I’ll use that 10 to do it in one. But if I’m doing 30 and 40, but the 10 is only the bilateral trade going both ways, I don’t want to accumulate the Chinese.

Tony Nash

Right. Here’s one of the key things there that I don’t think a lot of people, a lot of these CNY cheerleaders understand is if people accumulate CNY, they’re trusting the People’s Bank of China, right?

Michael Ncoletos

A, and they trust them. They’re going to get their money back when they want it.

Tony Nash

Right. But when we look at the currencies on this chart, it’s the Fed, it’s the ECB, it’s the BOE, and the BOJ. Very highly covered, and I wouldn’t say transparent, but relatively revealing on some of the decisions they’re making. I don’t remember the last time I saw a PBOC press conference open where people could ask questions, real questions. Until we can have that level of questioning of a central banker, it’s really hard for a country or a company to accumulate that currency because they have no idea what the policy of that central bank is going to be. Is that fair?

Michael Ncoletos

Tony, before you get your… You have to take off the capital controls.

Tony Nash

Yup.

Michael Ncoletos

The right mind when I accumulate the currency which has capital control. We’re talking about the Bricks currency, okay? There’s a discussion. Two out of five countries have capital controls. Two out of the five have capital controls, and half of them don’t trust the other half within the Bricks. We’re talking that this is going to be the alternative to the US dollar? Okay.

Tony Nash

It’s great. Put them in the ring together.

Michael Ncoletos

Okay. If you want to believe in Santa Claus, you can believe in Santa. But as things stand now, this is no option. Sorry.

Bob Iaccino

Santa Claus, is that real?

Michael Ncoletos

Sorry.

Tony Nash

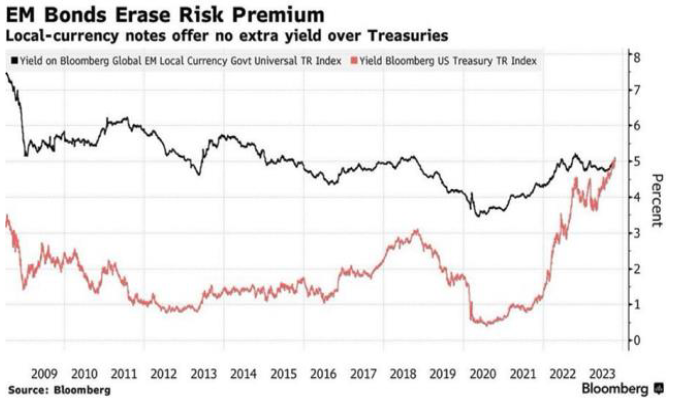

Yeah. We’re not going to reveal that on this show in case there’s kids watching. Let’s take this full circle to… I know there’s great chart on risk premium from EMs to the US, and I know we covered this a little bit, but seeing that risk premium really disappear, what is that? Effectively, that sucks all the money back to the US. Like you said earlier, what’s the point in investing in emerging markets if you have a guaranteed return, a US dollar denominated guaranteed return?

Michael Ncoletos

It comes back to what we talked about earlier. Again, I agree with you 100 %. If you’re getting 5 % for the safest asset, you need to at least get the double in order to get the risk. Okay, obviously it depends on the risk anyone can take. But let me put it this way. When you take risk, you need your upside to downside risk to be skewed on the upside. So if I’m willing to make 5 % to lose 5 %, there’s no point of having the discussion. If I’m losing to make 10 % to lose five %, that’s a two to one or a three to one, then it makes sense for me to make the investment. So a 10 % return is something I’m starting to consider in order for me not to put it at the five % and sleep at night. So to quantify what Bob said easier, I’m thinking in terms of how much you’re going to make in terms of what you can lose. So two to one, three to one, whatever that is. But it should be something bigger. So if it’s one to one, why bother get something riskier with the same return when I can buy something which there’s no risk or at least there’s never no risk, but there’s very small risk.

Tony Nash

Right. And the other thing that I try to reinforce with people that is so basic that some people look at me and think I’m stupid by saying this, but interest rates are the cost of money. And if money costs five % in the US, money should cost a lot more in riskier markets, right? That sounds really stupid, but that’s just the basics of it. So –

Michael Ncoletos

No, it’s simple. It’s very simple. Unless you’re safer than the US, which safer doesn’t mean only a fiscal situation, which is better. It means you have rule of law, you have an open capital markets, you have a democracy. There are a few things when you say safer. It’s not just numbers. So if you have an overall safer economy, then you should justify a better interest than the US. If you’re not safer than the US, then you need to justify a higher cost of money. As you said.

Tony Nash

Okay. Hi everyone. We’ve started our Black Friday sale at Complete Intelligence, and you can subscribe to CI Markets for $99 for the whole year. That’s 80% off our normal price of $500. Starts today, and it goes until November 28th only. Go to completeintel.com/BlackFriday and subscribe to CI markets for $99. Thank you. We always hear about China being in the ascendant. Albert, as we saw that Chinese vessel with smoke coming off of it yesterday, is China a real competitor right now if they don’t have a Navy to enforce their policy?

Albert Marko

Nope. Simple question is absolutely not. They don’t have any maritime, naval force to enforce any of their trade activities globally. Everyone points out. I think I’ve seen some charts out there of, Oh, look how many ports that the Chinese own. Yeah, but those host nations can evict the Chinese at any point in time with absolutely no repercussions. So it’s like-

Tony Nash

So does DP World out of the UAE, and do they command a world trade? They don’t. They run them out.

Albert Marko

They don’t. Yeah, it’s exactly right. These comments of China being a competitor to the dollar or the US in the near term is just a lame argument. It’s silly. I don’t take any of it seriously.

Tony Nash

Great. Michael, do you have any view on the timing of this squeeze? Are we in the middle of it now? Is this something that’s coming in a few months? When do you expect the intensity of it to really hit?

Michael Ncoletos

Well, the Fed doesn’t need, first of all, to raise rates anymore. You can stay here and the problem will continue. As the deficits grow, more dollars are needed from the market. I guess next year is going to be a bit tricky, unless, of course, because, and I mentioned this in the paper, because we have US elections and because of US elections, you never know what the government will do. Maybe they do another QE. Or if it’s not a QE, it’s something with another name, not to call it QE, and they throw liquidity into the system, this thing might pose. But I think positioning in the dollar in the next couple of years, you’re going to see the dollar much higher.

Albert Marko

I agree with that. That falls right into my political outlook, where in order to combat inflation, they’re going to have to keep the dollar high. That’s just either raise rates or keep the dollar up to a level where it just suppresses inflation over the long run. That’s same view as me.

Tony Nash

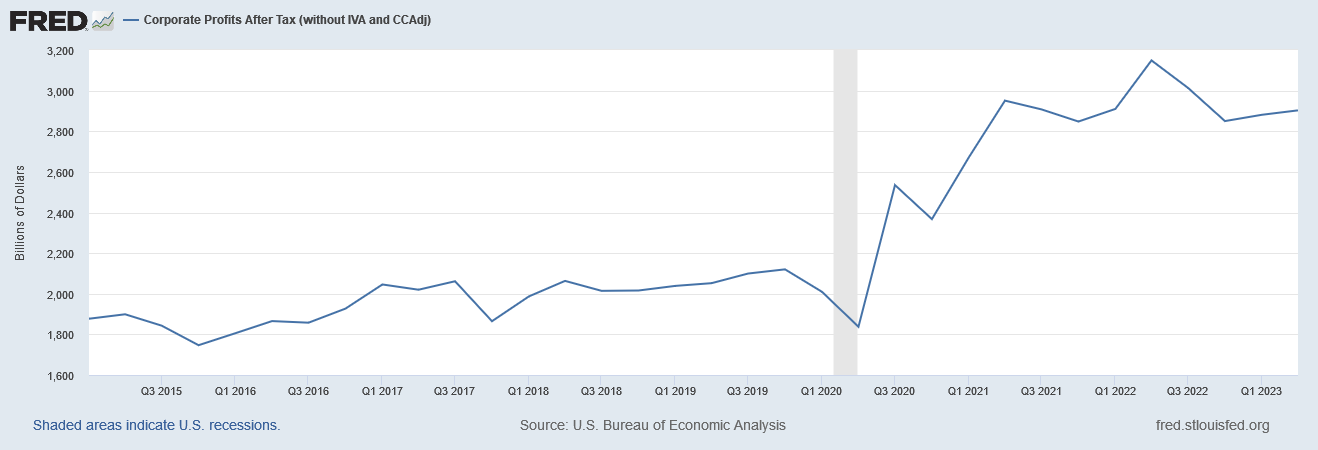

Interesting. That’s great, guys. Okay, so let’s move on to the next topic on year-end markets. Bob, you already mentioned there’s only a few trading days left in November, and I know you cover a lot of markets every day. I’d really like to get a sense check on where we’re going into the end of the year. We have higher interest rates globally, like we just talked about. Inflation seems to be abating, at least for now, and we can debate the magnitude of that. We have some geopolitical factors, but they seem to be easing, especially US, China, these sorts of things, seem to be easing up a little bit. Of course, there’s the Iran, Hamas thing, but that’s relatively local. Spending seems to be slowing. Us retail sales and all this stuff are down. We’ve had some dire retail outlooks for the holiday period. At the same time, corporate profits peaked in Q3 2022. You mentioned earning surprises and stuff earlier, but they’re slowing. I’ve got a chart up showing corporate profits, and they’re down fairly at a significant level since 2022. What are you looking at as we go into the last month of the year?

Bob Iaccino

One of the things I’m looking at from an equity market perspective is what’s going to break first. The reason I say what’s going to break is because I think it is a matter of what and not if. I think the soft landing scenario, you would have to believe that the Fed was possible of creating a soft landing. They were capable of it, which I don’t in order to. You would have to allow the Fed a victory lap regardless of… I mean, I agree with what Michael said when you have supply-side-driven inflation, the Fed doesn’t really have a lot to do with it. But they have been successful when you look at the data in slowing the housing market, and that’s about it. You need to see others slowing in order to believe that inflation is actually going to get to their 2% target, or they need to accept something higher than the 2% target. Now, whether they know it or not, they left the door open for that a couple of years ago. When Jerome Powell said, Because we’ve been below 2%, I’m paraphrasing, of course, he said, When we’ve been below 2% for long, we may need a little bit of time above 2% in order to reach an adjusted average of 2% inflation.

Bob Iaccino

I still don’t know what an adjusted average is. We didn’t learn that in statistics class. We just learned average. He could actually, at some point down the road, say, You know what? We’re between 2.8 and 3.1% is okay for now, which to the point of the elections next year that Albert brought up, and I think that could be one of the things they say going into the elections. They could actually put pressure on the Fed to say, Well, we’re allowing it here for a little while, and we’ll reassess in 2025 to see if we need to do anything more. Also, wages are growing at a rate. When you look at the three-month average of real wages, you’re seeing a level that isn’t consistent with 2% inflation. It’s much more consistent with about 3.2 to 3.8, 3.2 on the core, and you’re pointing it on the headline. So the driving factor for me going into next year really is energy. I’m a little biased because crude oil is the thing I trade the most. But as you mentioned, I look at 29 markets every single day, and when those are boring, I go to individual equities.

Bob Iaccino

But energy markets to me are the number one thing because despite crude oil and crude oil is trading at about $74 on NIMEX right now, 78 on Brent, that’s still high historically. We actually talked to Tracy Shuchart, chigirl about that on a recording that will release this coming Wednesday. I’m sorry, this coming Wednesday, but she’s the one who brought it up and it struck me because we tend to think as $70 oil as being, Well, that’s okay, we’re back down below $3 a gallon. But that is still a relatively high price historically. Put that up against the higher interest rates. I got in trouble for on a Bloomberg TV interview about a year or so ago where I mentioned that there were somewhere in the range of 37-40% of C-suite people in the S&P 500. But the last time we had rates this high, they were in high school. Some of them weren’t born. The journalist that was interviewing me at the time got offended because she was in high school the last time rates were at this level.

Tony Nash

You could be bragging, right?

Bob Iaccino

I know. She should have been like, That’s me. That’s me. And she said to me, Well, they could read, Bob. And I could tell she got offended by that. And I said, I didn’t say that they couldn’t read. What I said was, and I’ll go to the old Mike Tyson quote that I bring up a lot, Everyone has a plan until they get punched in the face. And these people are about to get punched in the face with rates they’ve never had to deal with. You take Silicon Valley Bank as an example. They’re out there having DIE parties, and I’m not judging that, rather than hedging their to maturity interest rate risk, right?

Tony Nash

Right.

Bob Iaccino

Because they never had to do it before.

Tony Nash

Yeah, there was at zero interest rates, there’s really no… You have the nominal, say, punishment for risk, but nothing beyond that. Now, your punishment for risk is multiplied over the nominal cost.

Bob Iaccino

You brought up the cost of money, which is a very real thing for consumers as well as investors. We’re going to go into… The holiday season is a big deal to me, and energy prices are a big deal to me. How much more do consumers themselves even at their higher wages? Because while we’re looking at potentially 2.8 to 3.2% inflation next year, that’s on top of the inflation that we’ve already had. The news media tends to do consumers a disservice by saying inflation is falling. That does not mean prices are falling, and the three of you know this. That does not mean prices are going down. That means the $30,000 car that became a $38,000 car is now a $40,000 car. The increase is not as much, but prices are still increasing. You pile on higher energy prices, which is not a guarantee, it’s not a given. I think there’s a lot of trouble going into maybe Q2, Q3 of the markets next year.

Tony Nash

Yeah, I’m with you all. I feel like the consumer is really stressed, but I hear this stuff every day with people telling me the consumer isn’t stressed. But I see it in front of my face every day when I go out into –

Bob Iaccino

They say they’re stressed. Paul Krugman and put it… I work a lot about it. It was about a month ago, and I just recently found it and retweeted it because of the just complete ridiculousness of his stance, saying that consumers are complaining about their financial position, but it’s not as bad as they think. I’m like, What the hell are you talking about? Somebody says they can’t pay their bills, and Paul Krugman is out there saying, Yes, you can.

Tony Nash

Right.

Bob Iaccino

Are they talking about?

Tony Nash

He pay my bills if he wanted.

Albert Marko

Paul Krugman is nothing more more than democratic mouthpiece at this point. He doesn’t say anything relevant to anything economic at this point in time, in my opinion. Every time he speaks, he just says something more ludicrous that is just absolutely out of bounds.

Bob Iaccino

I can agree more, and I don’t care that he’s a democratic mouthpiece. Just say you are. Don’t throw yourself in the Nobel Prize-winged economist anymore, even though that’s technically a fact.

Tony Nash

I’ll say this in Krugman defense. I had his international finance textbook grad school, and he writes an amazing textbook. We’ve got to give them.

Albert Marko

That’s the problem is because the guy knows he’s a smart guy. There’s no question that a smart economist, financial guy. But for him saying these ridiculous things that, Yeah, you can pay your bills, even though everything’s 30% more than it was three years ago, is insane.

Tony Nash

Right, and cards are loaded up and all that stuff. I want to ask you about tech. We have a massive concentration of equity risk in tech right now. I’ve got a chart up on the screen showing the relative concentration in tech compared to other sectors. It’s interesting, you mentioned energy, and if anything, people are less concentrated in energy than they were a year ago. Tracy Shuchart actually posted this earlier this week. What are your thoughts on tech? We just saw this OpenAI nest over the last week. OpenAI is the peak of tech right now. The governance in OpenAI is terrifying. We all saw it play out and live. I would submit that the governance in OpenAI is more representative representative the governance in tech than not. We have this concentration of investment in tech, which is risky anyway. Then we have governance issues playing out, and people want to act like that’s not relatively normal in tech. Can you talk to us about your views on tech and what you see? Is OpenAI, do you you reflective of governance in other tech areas?

Bob Iaccino

Well, I have no insight in a company like OpenAI, but what I do like to look at is an equity sector backtest and describe what the four sections of equity market performance look like to me. One of them is recovery, which is faster growth, slower inflation. Another one is deflation, which is slower inflation, slower growth. Then you got reflation, which we went through a bunch of years of with faster growth, faster inflation. Then you have stagflation, which we all know what that is. It’s faster inflation, slower growth. In three of those scenarios, scenarios, is in the top five in terms of their historical returns. Worst-case scenario, they’re in fifth place if you have slower inflation and faster growth. But I think we have a better chance of stagflation or deflation over the medium medium term and performs poorly in deflation, but doesn’t actually perform that badly in periods of stagflation. Now, granted, we haven’t had that many. But the number one one performer faster growth, faster inflation, and faster growth, I’m sorry, faster inflation, slower growth is energy. That’s why, again, I look toward energy because in third place in both of those backtests is technology.

Bob Iaccino

If energy is rising and it’s having an effect on inflation to where we have inflation not quitting, I want to be in tech, even though that might point to higher yields. But when you look at a yield equity backtest, the only time when tech suffers is when the yields further out are struggling, specifically the 10-year yield. If the 10-year yield is rising, tech tends to underperform. If the short-term yields are rising, let’s say that the Fed is hiking and the market thinks that it’s going to work, tech outperforms again. It’s difficult for me to see stocks going up without seeing tech going up. But my base case is actually the stocks don’t perform that well in 2024, specifically in the second half of 2024, which would mean stock tech would lead to the downside. Does that make sense?

Tony Nash

That makes total sense. Do you think-

Michael Ncoletos

Can I add something to that?

Tony Nash

Yes, please.

Michael Ncoletos

Well, I agree agree 100 with both. Technology mostly the ones that do not have a bottom line are a duration asset. When the duration gets hit, they get hit as well. It’s as simple as that. When they have a a bottom then it’s a DCF, and depending on your discount cash flow or whatever, net present value or whatever you’re doing, then you can assess a value which may be doing better or do well. But again, I think you hit it right on the nail on the head. I view it the same way. I just wanted to add that.

Tony Nash

Albert, what are your views on tech?

Albert Marko

As long as the higher interest rates are remaining, I don’t know what tech is going to be how they’re going to be able to perform going into 2024. Obviously, the Fed likes to use the Mag Seven stocks to pump markets, but long term, they’re so riddled with debt and they’re holding it and their interest rates are just higher for longer. As long as the market is offside again on this pivot or rate cuts, I don’t see what tech is going to be able to do in 2024. We’re already at stratosphere levels on tech. I think think we have 35 times earnings or something like that. It’s absurd. I agree with Bob. I don’t see much of what tech could possibly do. Would I not want to… I mean, I’d sure as hell want to hold it if the market shifts, knowing full well what the Fed can do. But for me, I don’t see much play here going up.

Tony Nash

Sorry, NVIDIA is 116 times earnings. Right now.

Albert Marko

Oh, sorry, I was probably referencing 2021 levels.

Tony Nash

Just to break that down, as the market is saying that it will take 116 years of earnings to properly value the equity price price That’s what the market is saying right right now, I mean, you guys trade more than I do, so I just want to make sure I have that right.

Bob Iaccino

That was the very first definition that was given to me as well. Yeah, the very first one one I’ve ever I’ve always held that in the back of my head because even if you’re looking at 35 EPS during times of bull markets, the things that people are buying are between 28 and 40, and then they get as high as 116, obviously. But to what Albert said and to what Michael reiterated in the simplest of terms, again, thank you for that. When these companies raise money, they like to go to the public markets. And if the public markets aren’t doing well, they are not going to to like the yields do because the vast majority of them are not that cash positive. We’re not talking about the big seven here. We’re talking about the vast majority of the tech sector. Now, how much has to happen for the tech sector to drag the big seven down? Well, I think that’s more a matter of taking profits than anything. One of the biggest moves lower we see in these high flying names, and I’ll throw Apple in there, even though Apple is probably more of a value stock than a growth stock that it used to be, they will sell those because they don’t want to lose on the other positions.

Bob Iaccino

They’ll sell them to cover options positions for margin calls, things like that. That’s when those start to get hit. There was the big news story about Michael Burry of the big short short betting against the SOX, the Semiconductor Index. They talked about how he took $47.6 million position. We took it an option, so it’s not $47.6 million. Again, the legacy media doing a terrible job at everything. And by the way, sidebar, legacy media would want us to argue about this stuff rather than agree and have a consensus as to what things are looking like. That’s why I like these formats so much more, because if we do agree, we should be allowed to agree. And it’s part of the reason I got kicked off CNBC for having that fight. But anyway, when you’re talking about moving forward, what can happen to the tech sector, we all acknowledge and understand that tech is going to lead the future of all nations. Nations. So you’re buying a currency, the first definition I learned of buying a currency is you’re buying a share of stock in that country’s economy. Economy. So you’re advanced in tech, the currency tends to benefit from that, hence the US dollar remaining strong for a long, long time, among all the other things Michael mentioned.

Bob Iaccino

But when you’re looking at tech falling, tech will be the first thing that people buy dips of. It will also be the first thing that they cover when those buying of dips don’t don’t if yields are higher for longer because these companies will need to manage a lot of their cash flow based on higher yields they have not had to do for two decades. I think that backs up both what Albert and Michael are saying in terms of why yields actually matter. They don’t matter for inflation today. They matter for the condition of the economy 18 months from now, two years from now, and how we adjust to these inflations. Because, again, I don’t even know how many of us on this stream are old enough to remember those rates. I remember my dad dancing because he got 6% on a house. He was thrilled because his first house was at 14% or 12%. This is a very new phenomenon, even rates where they are now. I wonder if the Fed will blink. I don’t know if they will or not. I’m curious about it.

Tony Nash

I remember my parents with a double mortgage in the early 1980s. Yeah. We have a lot of treasury people and a lot of CFOs who I don’t think… I don’t know if they’re ready for the… Yes, they can read, but I don’t know if they’re ready for the lessons that they’re…

Bob Iaccino

My father literally danced. He had a friend who had an accordion and knew how to play it. He danced the Tarantella for about 15 minutes because he got 6%. I’m sorry, I’m a child of immigrants, and that’s what we live with.

Tony Nash

Fantastic. Okay, great. Thank you for that, guys. Guys. Hey, talk about Argentina for a little bit, but because, of course, we had that big election in Argentina, and we saw a radical radical and according to Bloomberg, a madman, Milei, elected in Argentina. He’s got great hair, of course. This Bloomberg snip that I’m showing on screen right now, evidently, Bloomberg believes he’ll only help rich people and that only rich people want Argentina to end their economic slump. Bob, you’ve made some comments about media, and this is the stuff that we see there.

Bob Iaccino

Turning off Bloomberg as you speak.

Tony Nash

Yeah. With the Milei win, of course, the MSCI Argentina Argentina rally up 22% since October 31st, which is great. Great. Albert, what can Milei actually change? If you were in charge of Argentina, well, first of all, what could he change? Then if you were there, what would you change?

Albert Marko

I don’t know what he can change, to be honest with you. Argentina is riddled in debt. I have a suspicion that a lot of the debt is not reported in some special vehicles vehicles whatnot, and they’ll probably find out when they unload that just as as the interest-

Tony Nash

Yeah.

Albert Marko

-in office. Office. He doesn’t really have… Listen, I like him. He’s quite a character. He says some crazy stuff, some stuff that makes a lot of-

Tony Nash

I can see you liking that.

Albert Marko

Yeah, and I do. And I like the guy personally. But he doesn’t have a support structure. I don’t know who is going to be in his cabinet at the moment. His rhetoric for elections is far different than actual policy when you’re in charge of things. I don’t know-

Tony Nash

I’ve heard it’s hard.

Albert Marko

It is hard. And I don’t know what he can actually do. And I’m afraid that if he starts just firing people left and right and all these different institutions, that has to be all rolled up into something else. I mean, you just can’t just eliminate an entire ministry of so and so without some repercussions. I don’t know what he can actually do. I don’t really have a positive outlook for Argentina, regardless of him or anybody anybody else. In charge for the next 12 months. But like I said on Twitter, I like to reserve judgment until I see who his cabinet positions are. Until you see that, it’s really hard to make an assessment on the guy and what he’s going to be able to do for Argentina. He’s talked about dollarizing Argentina. Which in principle I agree with. It would absolutely stop hyperinflation in Argentina. But the reality is with what dollars is he going to do this with? Their debt is enormous and they don’t even have enough dollars to dollarize. It may be a five-year plan, perhaps, but but it’s not going to happen. I’m sure Michael can sit there and tell you more about the dollar and how they could possibly dollarize, dollarize, I don’t see a viable way that his election rhetoric can match up with policies going forward in the next 12 months.

Tony Nash

Bringing up Michael is a good point. Michael, you live in Greece?

Michael Ncoletos

Sorry, did I understand? In order for Argentina to dollarize, it will need another, like braided Balls type of trick. The US government has to be on board and they need to fund the Argentinean economy and make quite a few deals on this, make a few agreements, which I think is not that unlikely given that we’re also going into a geopolitical conflict, if you want to put it this way. So if you look at the Cold War between US and Russia, you had spheres of influence. I guess we’re going to go through that again. And it feels to me that Argentina is closer to home in terms of the US. The US will want to bring Argentina into their sphere of influence and help the new government in that sense. That’s my feeling. But this has nothing to do with economics, has to do more with a geostrategic view.

Tony Nash

Okay.

Albert Marko

Yeah, the problem-

Michael Ncoletos

I know with other things.

Albert Marko

Yeah, the problem with that is is has been notorious of installing leftists throughout Latin America. Look what happened with Brazil and then Colombia. Also. I have a suspicion that Argentina is set up to fail. They don’t want a conservative in there to actually succeed in economic policies.

Tony Nash

Can we just ask… Michael, you live in Greece a decade ago or so. They were facing very difficult economic times. When you look at Milei, just your top-level assessment, do you think he can be successful?

Michael Ncoletos

Well, Greece had a blessing and a curse. The blessing and the curse was the the in the sense that because we had a hard currency, things did not collapse. That was the blessing. The curse is that because we had a hard currency, it took us 10 years to adjust. So it depends how you want to see it and depends how, as Albert says, what the cabinet will be and what the policies will be. It comes down to pure policies and economics economics how they’re going to deal with this. If they want to be serious, they’re going to get the heat for 24 months and then they’ll be okay. If they don’t want to be serious, this can last for another 20 years and we can be having this discussion every five years.

Albert Marko

I’m going to have to agree with option B on that one. I just think that it’s going to take a long time for Argentina to pull out of this. Even with the policies, if he enacts some policies that are good, that’ll probably be credited towards the next leader of Argentina and not the not Milei.

Tony Nash

Let me just wrap this up. I know Bob needs to go, and I know we need to give our viewers a little bit of time to digest this stuff. Whenever there’s a win like this, and I’ve heard this in the the over the past couple of of days. Person on the right wants to believe that it’s a signifier of a bigger movement. Like, Milei’s win means that geopolitics is moving to the right, all this other stuff. Do you think think real or do you think it’s just a one-off?

Albert Marko

I think that there’s certainly a building momentum for conservative governments out there. But the fact of the matter is a lot of the leftist players control the markets and the media, and it’s hard to actually displace that in the near term. I think it’s going to be at least another… It’s either going to be another decade before conservative government stay gold or they’re going to need some some black swan or economic economic to the point where people are just fed up and don’t want to hear it anymore.

Tony Nash

Which is what happened in Argentina, but the question is-

Albert Marko

Yeah, we’re talking about a global thing. Yeah, that’s exactly right. We need a global thing. I think a good indicator would be what happens in in Holland. The next election coming up right now.

Tony Nash

Okay, just real quickly tell us what’s happening there.

Albert Marko

Well, the leftist government has absolutely butchered the economy there, and I think the people are pretty much fed up. But the problem problem is if the Conservatives get in there, do they have enough to actually have a majority in Parliament to lead lead coalition? I don’t even think that’s possible over there at the moment.

Tony Nash

Okay.

Albert Marko

We’ll see.

Tony Nash

Interesting. I think there’s a lot to come come Argentina, as you say. If he doesn’t have the people around him who can help him lead, it’s going to be extremely difficult for him to have much of an impact. I am so grateful for your time and your thoughts. I really appreciate this. Thanks. Have a great holiday weekend and have a great week ahead. Thank you.

AI

That’s it for this week’s episode of the week ahead. Please don’t forget to rate us and review on whatever platform you are watching or listening to this. Thank you.