Welcome to “The Week Ahead” with Tony Nash, where we discuss the latest market trends and forecasts for the upcoming week with a panel of experts including Blake Morrow, Tracy Shuchart, and Albert Marko.

They begin with Blake by examining the strength of the dollar in relation to the euro, Japanese yen, and the resurgence of commodities. The conversation highlights the Fed’s indication of keeping rates high, the dovish stance of the European Central Bank, and the inflationary environment in Europe and the United States.

The focus then shifts to the Bank of Japan and the potential changes in their yield curve control policy. The speakers discuss the challenges the BOJ faces in moving away from ultra-loose policy, and the impact it may have on the Japanese yen’s depreciation and potential future appreciation.

The episode also covers China’s economy and the challenges it faces in shifting towards a consumer-based model. The speakers mention the potential devaluation of the yuan to boost exports, as well as the appreciation of the Mexican peso and the rally in commodities driven by a weak US dollar and China’s stimulus.

Tracy touches on the energy sector and the United States’ oil demand. The conversation explores the implications of rising energy costs on inflation and the global economy, as well as the slowing growth in margins for S&P 500 companies. They discuss the impact on luxury brands and high-end consumers, as well as the current status of AI in the tech industry, mainly with Albert.

Lastly, the experts discuss the role of large language models in improving search efficiency and potentially replacing low-level analyst jobs. They acknowledge the transformative effect of AI advancements in search capabilities, but caution about the accuracy of information provided by AI, especially in legal contexts.

Hi. And welcome to the Week Ahead. I’m Tony Nash, and today we’re joined by Blake Morrow, Tracy Shuchart, and Albert Marko. Thanks, guys, for joining us. Today, we’ve got a few key themes. The first is the dollar, and we’re going to talk about the dollar in relation to the euro, Japanese Yen, CY. We’re also talking about commodity resurgence and earnings.

Tony

Before we get started, I’d like to let you know about a promotion we’re doing for CI Markets, our forecasting platform for stocks, ETFs, indices, commodities, currencies, forex, and economics. For the next two weeks, we’ll buy the first month of CI Markets for you. Go to the link to find out more. At checkout, use the code 25OFF. That’s the number two, the number five, and the letters O, F, F. This will give you the first month free when you subscribe to our $20 or $25 a month plans. Get fresh market forecasts every week, accountable forecasts where CI discloses our error rates, and a growing set of capabilities. We’ve just launched the top 50 US ETFs, Nasdaq 100, Nikkei 100, FTSE 100, and so on. Check out CI Markets today and use the promo code 25OFF. Thank you.

Tony

Guys, thanks so much for being here. I really appreciate the time as always. Blake, it’s your first time here. Thank you so much. I appreciate it. I’ve heard great things about you and I follow you on Twitter. I want to start by talking about the dollar. We do see another, of course, another 25 basis point move by the Fed and the ECB this week. And after a couple of months of hearing about the dollar’s demise, which Albert and Tracy and I have laughed at every time we hear it, yesterday on Wednesday, we’re looking for strength to return the dollar. And we saw that Thursday this morning after the ECB meeting. Can you walk us through your case for dollar strength?

Blake

Yeah, sure thing. And by the way, thanks for having me here. It’s first time and hopefully not the last time. It’s really an honor to be here with you guys. This week was a unique week because we had the Fed, ECB, and the B2B OJ is happening tonight. And we just had some headlines come out less than an hour ago that’s really moving the markets. But it’s rare when you can get these central banks, you have a good understanding from a macro micro point of view, fundamental point of view, what to expect. And in this case, we had the Fed that… I think we’re all coming to the realization that the Fed, even though they’ve said this many a time for months and months and months, rates are going to stay high for probably a long period of time. And something they said yesterday that really caught my eye or caught my ear, rather, was that their internal economists aren’t even forecasting a recession, which means that if you were thinking thinking when we get in a recession, the Fed is going to eventually cut rates, they’re not going to. So that automatically, I was assuming that they would message that they were going to keep rates higher for longer and try to drill that in.

Blake

I didn’t think it would come out in that way. However, I also figured the ECB, which came out this morning, and if you saw Christine Le Gard, I almost thought her shoulders were really slumped over. She looked really not so optimistic, and she was very dovish, more so than I’ve ever seen her in over the last 12 months. I figured that was going to be the case because the European data has been really deteriorating. And so I figured that she would be somewhat dovish and maybe not lead us down the path that we’re going to get another rate hike, which I think that was the case today. So it just so happened that it worked out the way that I anticipated. But let me be the first to say, Tony, that doesn’t always happen by no stretch of the means. It did really work out according to the way I planned it this week.

Tony

Hey, take the win.

Blake

I’ll take it this time. I take plenty of losses, so I’ll take the win.

Tony

With Powell yesterday, one of the things that I noted that he said is he said policy is not restrictive enough or for long enough to have its full intended effect. And so that the hire for longer is just all baked into that sentence, right? And surely after that, he said, we have a long way to go. And so I think there were some people who walked away from that press conference thinking it was Dovish, and I just didn’t hear that at all. Did you hear Dovish comments out of the press conference?

Blake

No, I think it was pretty well balanced, but the higher for longer, I think it’s starting to resonate with the markets. But between that and between the ECB and now the BOJ, I think the markets are starting to understand, and really you’re taking the Bank of Japan, which is the last G10 central bank that has ultra loose policy, that might actually get removed or start the other direction as of tonight or tomorrow morning in Asia. And I think the markets might be getting the hint now. And I think we’re starting to see signs of it actually today would be the first day that we are.

Tony

And then ECB made comments about end of cycle. So she really wanted wants to be at the end of her rate rise cycle, right?

Blake

She does. And I think she’s probably feeling a lot of pressure from Germany. If you’ve looked at the German, especially the manufacturing PMIs just earlier this week, they’re horrendous. And when Germany is the growth engine, if you will, of the Eurozone, if you will, and they have plenty of seats in the ECB Board of Governors, she’s probably feeling a lot of pressure from Germany specifically. And so, yeah, I think she wants this cycle to be over. I think everybody does. But the problem that we’re all facing, and I think the best case or I shouldn’t say the best case, the best example of a stagflationary environment is what’s happening in the UK with persistently high inflation. But now you have growth that may actually go negative and then they’ve got a real big problem. I think Europe is facing that as well.

Tony

Europe, I think we’re hitting up against some energy derived base effects over the next few months where I think people may be declaring victory over inflation and the battle may not be over. But we saw, especially gas, really rise Q3 Q4 of last year. And so they’ll be measuring inflation against that. I’m not sure that is going to be the battle is won type of environment for Europe.

Blake

I want to defer to Tracy and Albert as well. But Tracy, you follow a lot of these commodities. I was really, really carefully watching cotton over the course of the last couple of weeks. It had been basing since I want to say, the fall of last year of 2022. And it just broke out of a base, literally this week. And when you see these commodities percolate, that’s going to make life a little tough, especially when you have certain financial conditions are looser than they should be with equities where they’re at with the trickle down effect. You got people feeling a little wealthier. Their housing their houses or their multiple homes haven’t really lost a lot in value yet. And then you throw that type of spending on top of commodities staying very perky. I think this last leg of getting inflation from 3 % to 2 % is like running the 22nd to 26th mile of a marathon. And that’s where they’re at. It’s not going to be the easiest part.

Albert

Yeah. What we really should look at is the core CPI. That’s still raging hot. All the points that you made were absolutely correct. We’ve discussed this for many months now, Tony and with Tracy that Europe is just a zombie economy. And the moment they start taking up in any which way, inflation starts to rage again. And then energy inflation is gaining steam, not only there, but also in the United States. And we have a problem. I mean, the chairleaders of… We’ve solved inflation because they have a three handle, which is a little bit silly and way premature in my opinion.

Tony

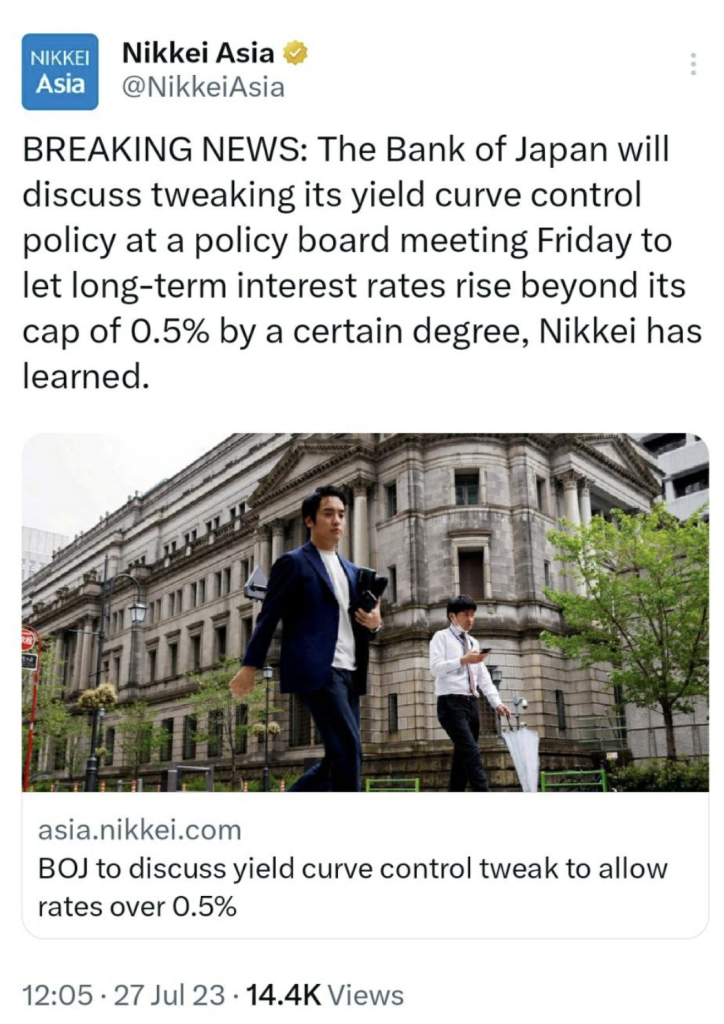

Let’s circle back, Blake, for just a minute to talk about BOJ. I know we’re going to talk about a lot of the commodity stuff in the next section with Tracy, but let’s circle back to BOJ. There are some stories out today on Thursday about the BoJ tweaking yield curve control to cap it by 0.5 %. So that is a pretty massive change.

I know they just changed their BoJ chair about three or four months ago, so he didn’t want to make any changes right away. But it sounds like he’s really starting to talk about some incremental changes. This is a pretty small change, but it’s actually a pretty big change. Can you talk to us about that a little bit?

Blake

Well, I think it is a big change because it would be a step in the direction that the markets don’t want to see. The last time Bank of Japan tried to move off the zero bound was just pre GFC, the financial crisis in 2008. So here they are again trying to move off the zero bound first starting with yield curve control tweaks. Now the BOJ, we have a new governor, BOJ Ueta, which is really interesting is he had been so in his academic papers that he’s written over the last couple of decades, how critical he’s been of the BOJ and where they’re at. He jumps into the BOJ driver’s seat and he ends up being just pretty much the same as Kuroda. Probably from a political standpoint, not wanting to rock the boat too much.

Blake

However, he also pulled a very similar move to Kuroda this last week where they leaked out from official sources to Reuters, probably every journalist from Vogue to who knows what, The Economist, saying that they weren’t going to tweak yield curve control. We saw move in the Yen move lower. So people like myself that were pre positioned waiting for this yield curve control leak, we got stopped out. I took some losses last week because of it. And then here goes today from the Nikkei paper suggesting that tonight or tomorrow morning in Japan, they’re actually going to make the tweak and move the band so they can allow it to trade up to 0.5 %. Now, that in itself is that tweak of that yield curve controller allowing it to move is basically step one of probably many steps of trying to normalize their monetary policy. But if you think about that, that’s the last central bank that we have that really is keeping ultra loose policy. And that’s I think the takeaway that the markets need to start looking at, especially equity markets globally.

Tony

Right. Very hard for them to continue importing inflation, but also very hard for them to fight against demographics in terms of the productivity value add in their economy. So they’re in a really rough place. So can we look at a number of currencies? I have a chart up now on several currencies. I want to just walk through some things with you as we look at where we are. First, on the top and blue, we’ve got Japanese Yen, which we’ve seen real depreciation since 2022. Can we talk about within the context of the dollar, if this BOJ policy really does go through, do we expect marginal appreciation in JPY or do you think it’ll really come back down to say 120 or something like that?

Blake

That’s a great question. I think over time, depending on how aggressive the BOJ has to be, I think 120 would be probably a realistic expectation from a technical point of view because you’d be looking at an equal leg move from the highs down to the lows that we put in in January of this year. So that would probably take us in the range of 120. And it’s not going to happen overnight, but it’s baby steps for the Bank of Japan. And I think that the first real key is going to be what I saw as channel support, which it would be around the 136 level. We start trading below 136, 135. I think a lot of longer term yen shorts might be looking to exit those positions at that point.

Tony

Okay. And then looking at CNY, China’s economy is in a really bad real tough spot and we’ve seen some devaluation there. What’s your expectation with CNY, CNH? Do you expect to see continued devaluation there, or are we in that zone where the monetary guys in China are comfortable?

Blake

Well, I don’t think they’re comfortable at all. And that’s a great question. And it’s a really, as you pointed out, it’s a really complex situation that China is dealing with. They thought their opening would be great. The issue that China has, and if you’ve watched China over the last 20 to 30 years, trying to shift their economy to a consumer based economy, hasn’t They’ve made a lot of billionaires and millionaires as you could imagine, but still a majority of their country is not in that situation yet. Yes, I get to eat five bowls of rice today versus 10 years ago, and they had three bowls of rice. Maybe that’s the difference for a lot of their population. But the fact of the matter is, is they’re really trying to rely on domestic demand, and they just said it in the Politburo meetings this week that they are struggling with that particular issue. So they have a few levers that they can pull, stimulus levers, reserve ratio requirements. They can try to spur domestic loan demand, but the real estate markets are a little iffie at best because a lot of Chinese, they have multiple properties that they own.

Blake

So trying to get them to leverage up and borrow a little bit more. It’s a hard or a tough ask for the Chinese people. So China’s got a few levers left and one of them happens to be with the C&H. And the C&H and the C&Y. Trying to get the Wan or the Renminbi lower to spur more demand from Europe, from the US, make their goods cheaper. But it’s hard for the the PBOC to pull that lever without looking too obvious, right? Because we know they have the lever, we know they can pull the lever, but we know politically it’ll be frowned upon. So I eventually expect the US dollar C&H to break above 730 and maybe even go towards 750. And that would be signaling to us as investors in capital markets globally that China is really feeling the heat. So can the US dollar C&H continue to dip, maybe down towards the 200 day moving average around 7? Sure. Do I think it’s probably a buy down there? I don’t trade it, but I think people that do are probably looking at that level as an attractive level to be on the long side.

Tony

Okay, yeah. I think one of the key things that I look at when I look, especially at Northeast Asian currency is you have this movement with the BOJ, which will likely appreciate JPY.

You have the Korean won that’s appreciating. China’s domestic economy is a mess and they really need to goose exports so they can use that industry to further develop domest. Given all the troubles they have at home, that might be an easy decision for them to make to devalue just a bit to goose some exports, especially as more industries move off of the Chinese mainland for a lot of political reasons. In terms of moving industries, I want to also talk about the Mexican Pesso. We had a viewer question about the Mexican Pesso, and we’ve seen the Mexican Pesso appreciate pretty nicely against US dollar over the last, say, nine months or something. Can you help us talk through and understand why the Mexican Pesso is moving in that direction?

Blake

Yeah, you bet. This has been the darling of the FX market. By the way, going back to China, I just want to say I’m not the best China expert. I have some European members in the forex analytics team that trade the US dollar C&Y and C&H quite aggressively. So they’re better. I just take from them what I can. But as far as the Mexican Peso, it is something that I trade quite actively and aggressively at that. It’s been the darling of the FX market as a carry trade. When you can carry the Mexico’s higher rates over anything else, especially the euro, the yen, the Mexican, M XN, JPY, the euro, M XN, dollar and Mexican Peso. The Mexican Peso has been the star. And the reason why is because the rates are extremely high and FX institutions will park their money in Pesos and they’ll sell other currencies. And that’s great in a market where stocks are rising, we see that volatility is low. Those we call carry trades. That is the carry trade. It’s like the yin of the mid 2004 to 2005 era. The Mexican Pesso is in that situation. The risk at this point is that we’re starting to see other LATAM currencies l ike…

Blake

Oh, I always forget the central bank. The Chilean Central Bank, BCCH, is that what it is? Anyway, they’re about ready to embark on a rate cut campaign. Now, Chile is not Mexico, but it is a La Tène currency, and you’re starting to see some of these emerging market currencies, banks go stop raising rates as well. Will they start cutting rates? If they do, that the margin that you’re going to get on that carries a little bit less. Then if you start to see equity markets really come under pressure, like let’s say the and P trades from 40, it’s trading around 4,500, 4550 right now. We trade down to 4400 or 4,300, you’re going to see the air come out of the Mexican pay zone. You’re going to start to see the dollar outperform, the yen outperform as the BOJ adjusts their policies. Even the EuroMexican Peso is probably going to recover after having such a big slide. So I’d be careful with the Mexican Peso as it trades below 17. I think if it trades back above 17, 1705, especially 1750, we’re probably looking at a squeeze well over 18 again.

Tony

Okay, great. Thanks. We don’t talk about Mexico a lot, so this is really interesting.

Albert

I like the Mexican pace, though, simply because the trade has increased tremendously between Mexico and the United States.

Blake

I cannot disagree with that. And I think Mexico is the US is China. And specifically when I played a couple of rounds of golf with a gentleman that he has a chip company that he’s actually migrated his employees from China to Mexico over the last three, four years because of cost, labor cost. And so I am actually a Mexican pesos bowl. People that know me know that I believe the dollar Mexican pesos is eventually going to be trading in the lower teens over the course of the next couple of years. But right now, the specific risk is that we trade back to 18 before 15. How about that? Maybe that makes sense.

Albert

Yeah, I’ll leave the forex stuff in the levels of the U.

Tracy

And that was the exact question I was going to ask. I was going to say, does it have to do with trade with the United States as we’re seeing a lot of manufacturing, which was big in, say, the 80s in Mexico, now returning to Mexico with trade to the United States or say US companies moving their manufacturing to Mexico rather than China per se.

Blake

Yeah. And Tracy, I gave you that one example. It’s anecdotal evidence, right? It’s not like something I’d hang my hat on. But I think that is a trend that we will see in the years ahead is as China’s labor force shrinks and it costs more to produce in China, the rest of the world is going to search for alternatives. Most of them, like a lot of Europe, is going to go to India. We’ll go to India. But Mexico is our next door neighbor and labor is still cheap there. So we will find alternatives and I think the rest of the world will away from China. That’s one of the issues that Tony, you brought up about China. They got issues. You try to change your whole demographic of your entire ginormous country, there will be repercussions. And this is one of them, I think.

Tony

And it’ll happen. It’ll start slowly and then people will realize it and it’ll hit heart pretty quickly at some point. So I think looking at CNY, CNH right now is really important because I think we’re in the early days of something larger happening over the next few years.

So Tracy, let’s talk about resources for a minute, I know that’s where you live every day. So we’ve seen strength in commodities over the last three months. I’ve got a chart up on copper, WTI and net gas up on the screen right now.

So why are we seeing a rally in commodities now? Is this really on the back of a week or dollar or is there something more to it?

Tracy

Well, I think we need to look at each one of these separately, to be honest. Just for example, Blake brought up the cotton issue and why is cotton starting to rally off the lows now. And that’s a China stimulus story right now because they have a lot of manufacturing to make a lot of cotton T shirts, etc. I think it’s really hard to lump all of the commodities together. So I would like to look at… I think we should look at oil or the energy sector in particular separately from, say, the metal sector, separately from, say, the softs.

Tracy

I think if you’re looking at the energy sector in particular, you are looking at a week or dollar. That always helps. And that all ends suddenly signs of life from China, meaning people are starting to believe China’s stimulus matters. Whether it’s come true or not, we really haven’t seen them say a whole lot until the last couple of weeks. You can even look at the hang saying on this in which we’re down 5 % on the year. And over the last weeks, it’s surging right away. Goldman just put out a note on Wednesday that said funds are piling back into China at the fastest pace in nine months over the last week, which is huge based on what they have said over the last week. It happened.

Tracy

Whether you believe them or not, the markets believe them at this point. And then as far as energy is concerned, we still have that supply demand issue. We have Russian S exports down. We have voluntary cuts filtering into global markets right now. And we are also seeing recession fears seeming to subside a bit because markets are seeming to starting to believe in this soft landing, or at least the commodities markets are.

Tracy

The equities markets, that’s a whole another story. And then if you look at the metals, again, I think if you look at the metals, this is again a China story. Suddenly, everybody’s believing China stimulus at this point. Again, I don’t know what exactly changed and what exactly changed the market’s mind, but I think it was helping a little bit of the property sector, which is definitely not enough, in my opinion, as well as the tech sector, the couple of announcements that they put out over the last two weeks. And so I think that’s really what we’re looking at right now. And again, a lot of it is the China story.

Tony

Right. So we’ve got Europe dead. We’ve got China dead with some commitment to them to maybe get stimulus, and we’ve got the US slowing down into the end of the year.

Tracy

Well, if we’re talking about the energy sector in particular with the United States, we have implied demand over the last several weeks has risen from 19 million barrels a day to 21.7 million barrels a day, which is huge. That’s over 2019 levels. And so we’re not really seeing And implied demand, you can take in different ways, but that is what product supply is implied demand. That’s what everybody takes it to be. So we’re not really seeing demand being lowered in the United States. We are also looking at a place in August where we’re going to see a lot of exports to China because Russian oil is getting to be more expensive right now. We’re above that price cap. And so we’re seeing China has put a lot of orders in for the United States, for WTI, Midland, for August deliveries. So we will see a reans here in the United States as far as inventories are concerned. And we still haven’t seen China overall. I mean, over this whole period that everybody’s thinking China is imploding, which they may or may not be. They’ve been buying oil hand over fist. And perhaps, yes, that’s a lot of it is going into storage.

Tracy

They can build storage out. But a lot of it, if you look at the refinery runs, are also huge.

Tony

I’m so glad you didn’t say China is talking up to go to war because I’m so tired of that.

Tracy

No, I don’t think China likes cheap oil, let’s be real. So they can get a huge discount from Russia, right? And get this price cap. And so at the time, it was $23, $20 below the price cap. Of course, who’s not going to stock up? India stocked up. Everybody’s going to stock up at that point, right? You’re going to buy high end over this. Actually, the best thing that the United States could are the best thing the West could hope for is that Russian oil is trading over that price cap because you know why? That doesn’t make it as desirable anymore. Nobody’s going to buy as much anymore. I think it’s short sighted thinking to say, Oh, my God. They’re trading over the price cap. Well, great. That means it’s not as desirable anymore. Why would I deal with the hassle of buying with them if it’s only a few dollars discount?

Blake

Do you mind if I interject and ask a question?

Tony

Yeah, absolutely, yes.

Blake

Okay. And Tracy, this is something I think about quite a bit just because we’re having this discussion or we’re having this discussion about crude oil and inflation, going back to the inflation question. It’s interesting. You watch crude oil rally and everybody cheers like, Oh, things must be getting better. But there’s always that inflection point, and I’m not sure where it is in crude or R Bob or whatever you’re looking at, but at what point do these higher energy costs really start to translate to, Oh, my God, that’s going to bite the consumer here in US globally, wherever you’re talking about. And crude going higher is not a good thing. There is that inflection point. I don’t know where it’s at. I don’t know if it’s at 80, 85 at 100. Do you have any thoughts on that?

Tracy

I think it really depends on the state of the economy and where we’re at. Our I think at $70, we’re still in that 70 to 80 range.

Blake

And I think that’s… Goldilocks, right? Goldilocks? That’s comfortable.

Tracy

It’s very comfortable, right? You’re not seeing $5 oil or gasoline prices at the pump. Not saying that’s a very comfortable position for oil to be in at this juncture. If we start to see oil prices spike higher than that, of course, that’s going to matter. And of course, this is all going to filter into energy runs the economy. You can’t do anything without energy. You can’t run a business because you have to keep the lights on. You can’t grow food because you need energy to grow food. So energy runs the economy. So at some point, yes, it’s going to matter. It’s going to filter in. It’s going to make prices higher. And I don’t think we’re going to see 2 % inflation anytime soon. In fact, even Powell doesn’t think we’re going to see 2 % inflation anytime soon. He said yesterday we’re not going to see this to 2025. I tend to think that ambitious goal because I think that no matter what we do at this point, if we’re looking at energy transition and we’re looking at all of these policies we want to put forward, we’re still lacking a lot of these materials, we’re still lacking a lot of energy for this.

Tracy

And this is going to be a huge problem that central banks just cannot counteract no matter… They may try. Actually, Peter Bookfire brought up a really good point yesterday when I was interviewing him. He said it’s easy to bring inflation down quickly with high rates. It’s harder to keep it down.

Albert

Tony, who told you that the more they rally this market, the more inflation is going to be a problem?

Tony

You did, Albert. You said it a long time ago. You said it.

Albert

Why people think that as they rally this market in silly, silly stratospheric levels, that they didn’t think that commodities in oil and wheat and cotton and every other thing is not going to run? Of course it is. Their problem is they’re running out of room now for rate hikes. So what they get, the only other option that I can see that they’re going to use is the US dollar. That’s the only thing they can do is take the dollar back up to the 108, 109 area just before you start breaking Europe and the rest of the world to try to team inflation because they don’t want to see 6, 7 % CPI prints going into an election year. That’s just ridiculous.

Blake

Isn’t it crazy, Albert, how the dollar can be weaponized? And it really can be, I believe.

Albert

Of course it’s going to be weaponized. It’s a reserve currency and Janet Yellen controls the policy. She’s going to do what she needs to do whenever she wants to do it. Unfortunately, that’s just the reality. It’s just the reality of the situation. And as I was saying, rate hike runway is pretty much ending. So the dollars is the only thing that they’re going to be able to use.

Tony

So your thesis is that US rates will top out at 6 %, and that’s going to crush China. Is that right?

Albert

Oh, yeah. China was never prepared for 6 % rates. Absolutely.

Tony

And again, tell us why? I want to make sure everyone understands.

Albert

Well, it’s just the debt level, the amount of debt that they had and the way they funded their debt. No one was, I don’t think anybody on Earth was thinking that 6 % % Fed Fund rate was coming. But here we are at 550 almost with probably another two hikes to go.

Tony

So we hit 6 % now. Now, China has been evergreening debt since 2009. They have all that debt for 20 years ago. They’ve continued to evergreen because they haven’t been able to pay it off and so on and so forth. Fed funds hit 6 % and the Chinese are practically begging the US not to raise anymore. Is that fair to say?

Albert

Oh, absolutely. And it’s funny because Yellen was just over there and then coincidentally, the dollar tanked underneath 100. As soon as she left for a day or two.

Tony

Total coincidence, Albert.

Albert

Total coincidence. Total coincidence.

Tracy

I tweeted that out. I tweeted that out. Absolutely.

Blake

Her getting psychedelics was total coincidence as well.

Tracy

That was the best part of the whole…

Albert

But I agree with Tracy wholeheartedly. I think 65 is the floor for oil, and I think probably 85 is probably a top for oil. It’s a comfortable zone that they’re willing to deal for the next whatever year or so.

Tony

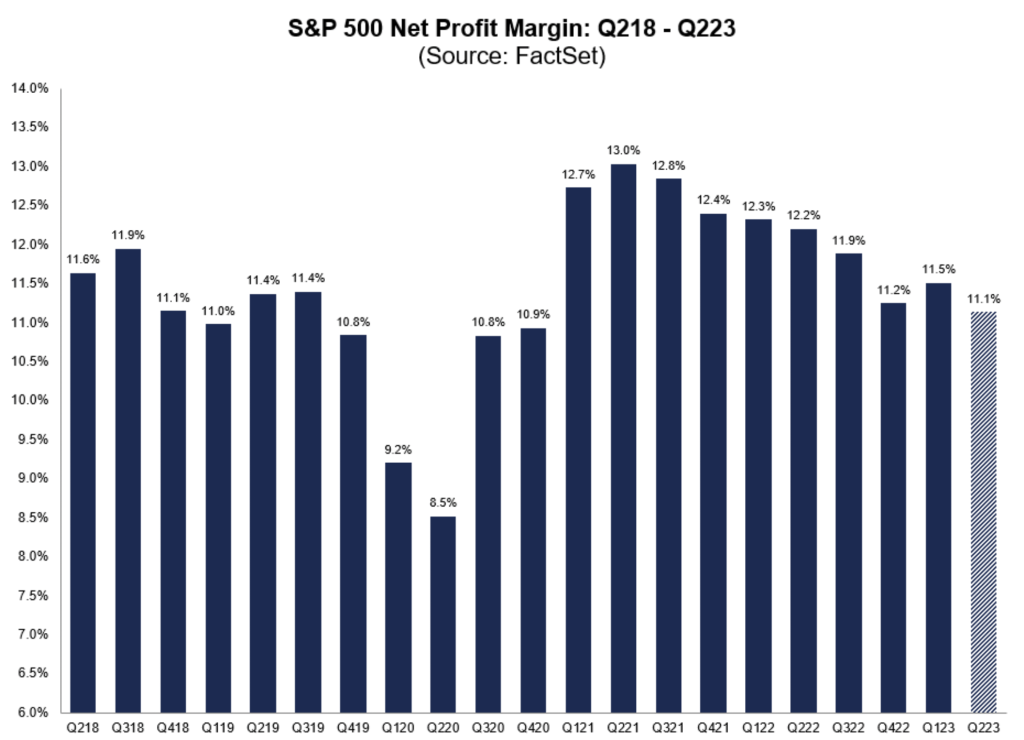

Great. Let’s move on to earnings, Albert. I just want to cover a little bit on earnings here. What are your thoughts on future earnings? So far, we’ve seen S&P 500 companies report the slowest growth in margins since Q4 of 2020.

So over the last probably year, year and a half, we’ve talked about the pricing power that companies have had since about Q2 ’22 where they were able to continue to expand their margins and raise prices on customers and customers would just accept it. That seems to have come to an end at least a bit. So is that what’s driving this margin compression? I’ve got a chart from faxing on the screen showing the margins of companies coming down to right around 11 %.

Albert

It’s not just that. We talked about this maybe six months ago saying that this is probably going to end up happening where margins are going to start ticking down second half of the year. And that’s exactly what we’re seeing. The issue is, labor rates are still advancing. Their fake CPI is still a little bit of tailwind for earnings, but that’s slowing down too. So they don’t have that inflationary tailwind to jump up prices as demand is starting to take down. Consumers at this moment are a little bit more price sensitive. They don’t really need a Rolex watch or a secondary home or a third boat and whatnot. So as that money is starting to dry up, margins are starting to dry up too. I think that it’s going to be a bigger problem for Q4 However, if I’m right and inflation is ticking back up, there might be a little bit of earnings tailwind into mid 2024 again. Of course.

Blake

Albert, since you and I just met for the very first time today, it sounds like you’re obviously following earnings pretty closely. How do you feel about the Reishmont group last week and then Louis Vuitton this week? What does that tell you about the high end stuff and the high end global consumer consumer.

Albert

The high end global consumer, I’ve always watched to see when they start retracting spending is when I start to get nervous. Whenever the big homes in Naples, Florida stop selling and Louis Vuitton start getting worried about their demand, that’s always problematic. Now, I personally love Brunello Cucinelli. That’s my brand. I’ve watched them for years, seen their stock price go from 38 to 80. And as recently this last couple of weeks, I’ve been noticing their ticker trending downward. And I looked at their sales and their stores are not getting as many people in. Their online stuff is going more to outlet than it is into the stores and out to top consumers. So yeah, I think the top consumers are about to pause. If not paused already, they’re about to start pausing in Q4.

Blake

Yeah. The Reishmont group, I think last week they were down 10 % in European trade. And Tony, that goes back to your point about China and they decided to solve the Chinese high end consumer. They’re the problem.

Albert

Yeah, they say that. But that’s more than just that. The Chinese high end consumer is one component of it, probably a real big one. But the Middle East is probably showing the same little drawbacks. North America and Europe is obviously going to have falling sales in the luxury market. So they can blame China, but it’s a lot bigger than that.

Blake

Yeah, right. Cool.

Tony

I want to talk for a second about tech, Howard, because I know you love to beat on AI, even though I run an AI company. I don’t take it personally. So on tech, I thought it was really interesting that Microsoft’s growth for Azure hit 25 %, but AI was only about one and a half % of that growth. So I think some real questions have come. People have really started to think about AI. If Microsoft can’t get money out of AI because they’re effectively the owner of Open AI, right? So if they can’t make money out of AI, who can? We’ve seen for the past two, or at least earning calls, AI is mentioned dozens of times on so many earnings calls, right? So when do you think we’ll start to see that? Or do you think AI is just a feature in larger products that just help people retain and marginally grow?

Albert

Yeah, I think that’s correct. I think that’s just the feature and the larger products. The only AI that I would be excited about is whatever comes out of Apple.

Tony

And Complete Intelligence, of course.

Albert

Of course, Complete Intelligence. Truly dollar money maker right here.

Albert

But as a stock that’s actually traded, Apple would be my number one for AI. From what I hear, they have a working AI internally that’s just off the chain. But Apple is really smart. They wait years to perfect something before they start releasing things. So I just think that AI is a little bit too premature, and I don’t really like the marketing talk by some people. It just throwing AI around as if it’s some godlike feature on an app. It’s not. So I think we got a ways to go for that.

Tony

Yeah. My view is large language models like JMP and all the stuff that Microsoft is starting to do is really just a synthesized search engine. It makes your search a lot smarter. It’s all it does. It’ll take out some low level analyst jobs to write some papers for you. It’ll make your searches better, that thing. But we’re not to the point where those LLMs are real money makers right now. They make those applications more useful. Does that make sense?

Tracy

Anecdotally, wasn’t there just an article out that saying AI is getting dumber?

Albert

Well, it’s garbage in, garbage out. I think you’re talking about where chat GPT was answering 98 % of math problems correctly, and then just recently it dropped down to 2 %.

Tony

It answered 2 % correctly?

Albert

Yeah, 2 % correctly. It’s just garbage in, garbage out.

Tony

I’m going to look that up.

Albert

Yeah, I posted it.

Tracy

He posted it. I actually read it before he posted it. It’s true.

Tony

Because I don’t need AI to do those problems. I can get 98 % of them.

Albert

That’s the thing, Tony. I always tell people, whether it’s technological or political, social, things happen. Things happen incrementally. There’s never some jackpot trade or technology that comes out that changes the world like we’ve never seen before. It’s just things happen in stages.

Tony

But to OpenAI’s credit, AI, I think, was a really far off imaginary word to a lot of people until chat tipit e was brought to market. And then I think people went, Oh, my gosh, this really changes things. And I think it did. I think it’s the biggest change to search that we’ve seen in 20 years. I completely agree. It’s made it a lot easier.

Tracy

You just have to make sure it’s correct, right? Because you hear these stories, some lawyer used this for a brief and they brought in a whole bunch of…

Albert

Legal trouble. Yeah, you got.

Tracy

To say it. It didn’t really happen.

Blake

Yeah. It’s definitely like an assistant and you have to go back and double check the work. I look at AI as the Google Glass of today. Yes. I’m sure at some point we’ll all be wearing weird things on our heads. Whether it’s…

Tony

I hope not.

Blake

Not. Whatever. Well, just wake me up when Ex-Machina actually happens, and then I’m going to go run for the Hills.

Tony

Right, exactly. Just circling back to earnings for a minute, Albert, as we finish out this earnings season, are you looking for… Are we recapturing earnings momentum, say, later this quarter or into the next quarter, or do you see things continuing to gradually deteriorate?

Albert

I think we’re going to gradually deteriorate into the end of the year with probably earnings starting to tick back up Q1 Q2 of next year in the run up to the election. Obviously, tech earnings, it’s the fabulous five of Microsoft, Google, Apple, NVIDia, so on and so forth. Those are the ones driving the market. So that’s the ones that I would be watching.

Tony

Very good. Guys, thank you so much for your time. This has been excellent. Blake, thanks for joining us for the first time. Albert, Tracy, thank you your time as always. Have a great week ahead. Thank you. Thank you.

Topics discussed: • Fed raises interest rates by 25bps. • US shares mixed, Treasury yields & dollar lower after Fed • Japan’s population drops by most on record

In this episode of “Peter Lewis’ Money Talk,” the CEO and founder of Complete Intelligence, Tony Nash, joins as a guest to discuss the recent developments in the global economy. The Federal Reserve’s decision to raise interest rates by 25 basis points to 5.25-5.50% is analyzed, with Tony providing insights into the potential implications of this move. He emphasizes the urgency to address inflation while also considering the impact on consumers and businesses facing higher inflation rates.

Contrary to some market perceptions, Tony interprets the Fed’s statements as hawkish, hinting at a more extended period of rate hikes and dismissing expectations of rate reductions in the near future. He points out the significance of base effects in measuring inflation, indicating that inflation rates may increase further as the effects of the previous year’s higher oil prices wane.

Tony and Peter also discuss the challenges faced by companies and consumers amid rising interest rates and deteriorating corporate earnings. They explore potential responses, such as companies cutting costs, possibly leading to workforce reductions, and how extreme weather conditions might impact the market. Additionally, the podcast delves into the situation in China, where there are concerns about deflation and potential devaluation of the currency to boost exports and stimulate domestic economic activity.

As the conversation touches on the European Central Bank (ECB), Tony suggests that Europe may experience a period of inflation due to the surge in energy prices but expects inflation to move towards disinflation over time.

Chapters

01:22 Fed Chairman Powell’s press conference 02:41 Decline in Japan’s population 04:09 US stock market reaction to Powell’s press conference 05:30 Chinese equities performance 06:08 Introduction of guests for discussion 07:20 Fed’s commitment to reaching 2% inflation target 09:07 Interpretation of Powell’s press conference 12:48 Uncertainty in economic data and Fed’s outlook 14:35 Peter doesn’t want to talk 14:38 Andrew questions recession definition 15:45 Peter comments on Powell’s statement 16:03 Tony on recession expectations 17:29 Tony on avoiding stagflation 17:43 Andrew on market volatility 18:27 Next phase: Fed holds rates steady 19:01 Andrew’s approval of Tony’s point 20:11 Tony on deteriorating earnings 22:08 Tony on layoffs and cost-cutting 22:35 Impact of layoffs and reduced savings 23:49 Andrew on climate investment opportunities 24:49 Andrew on climate crisis urgency 25:18 Tony on extreme weather and subsidies 26:31 Peter on Chinese deflation and impact 26:59 Andrew on Chinese deflation and global influence 28:21 Impact of China’s deflation 29:55 China’s need for devaluation 31:06 European Central Bank’s challenge 31:41 Base effect period in Europe 32:37 Replacement of Chinese Foreign Minister 35:27 Continuity in China’s foreign policy 36:54 Wang Yi as a temporary Foreign Minister 38:24 Wang Yi’s powerful position 39:12 Wang Yi’s role as stabilizer 40:57 No significant impact on China’s diplomacy 42:13 Introduction to the economy’s critical point 42:39 Concerns about achieving economic growth 43:20 Anticipation for the big stimulus package

Transcript

Peter

Every Monday to Friday this is Peter Lewis’s Money Talk.

Peter

Good morning. This is Peter Lewis, welcoming you to my podcast, Money Talk, for Thursday, the 27th of July. It’s Fed Day, and we have news and analysis on the Fed’s decision to raise interest rates. That’s coming up. This podcast is sponsored by Surfin Group, which is headquartered in Singapore and offers online financial services to 30 million customers across 10 countries. Thank you for making this podcast one of the most listened to financial podcasts in Hong Kong and Singapore. In today’s business and finance headlines, the Federal Reserve has raised the target rate for the Federal Funds rate by 25 basis points to five and a quarter to five and a half % in line with market expectations and with unanimous support from the Federal Open Market Committee. That brings borrowing costs to the highest level since January 2001. It marks the 11th increase since March 2022 when the Fed started raising borrowing costs from near zero to try to call the economy and ease price inflation. The US Central Bank resumed the tightening campaign following a pause in June after observing that the economy has been expanding at a moderate pace. Job gains have been robust in recent months and the unemployment rate has remained low while inflation remains elevated.

Peter

In a press conference after the meeting, Fed chairman drone Powell was perceived by financial markets as leaning more towards the Dovish side, raising hopes among traders that the current tightening cycle has ended. He emphasized how much the central bank has already done and the amount of time it can take for monetary policy to call inflation. We can afford to be a little patient as well as resolute as we let this unfold, he said. He added that it’s possible that the Fed could raise rates at the September meeting if the data warrants it, but also possible that the central bank could hold steady. Mr Powell insisted that the central bank would take a data dependent approach going forward when determining additional hikes and he then clarified that no decision to raise borrowing costs further has been made. Japan’s population has recorded the largest annual decline on record despite efforts to boost birth rates, data showed on Wednesday. The Ministry of Internal Affairs and Communications said the number of Japanese nationals fell by 801,000 in 2022 from a year earlier to 122.4 million. That’s the largest drop since records began in 1968. The population of Japanese residents has decreased for 14 consecutive years after peaking in 2009, but the population of foreign residents increased by 289,000 to 3 million.

Peter

That’s the first rise since the onset of the coronavirus pandemic in 2020. On today’s money talk, I’m joined by Andrew Ferris, the CEO of Econosis Advisory, and from the USA, Tony Nasch, Founder of Complete Intelligence. And with a view from Taiwan is Ross Fe gold, Business Development Director at SafePro Group. Us stocks swung into positive territory during Federal Reserve Chairman Gerome Powell’s press conference as he said there was disinflation. Even as he also said that central bank officials had not yet made a decision as to whether to raise interest rates again in September. But the main indices ended the session mixed. The S&P 500 saw a peak of 4,610 before pairing gains after drone Powell said he doesn’t see inflation returning to the 2 % target by 2025. The index ended the day virtually unchanged at 4,567, but at its highest level since April 2022. The Nasdaq composite lost 0.1 % to 14,127. The DAO added 82 points, that’s 0.2 % to 35,520, extending its rally to 13 days. That’s the longest winning streak since January 1987. And if the index rises for 14 straight days later today, it will match the longest streak in history, going back to June 1897.

Peter

That was roughly one year after the DAO was created in May 1896. After the closing bail, Facebook owner Meta reported better than expected results and issued optimistic guidance for the third quarter. The company returned to double digit revenue growth in the second quarter for the first time since the end of 2021, reporting that revenue in the three months ended June 30, rose 11 % to US$32 billion as advertising rebounded. Meta shares rose as much as 8 % in after hours trading, and prior to Wednesday’s close, the stock was up 159 % this year compared to the 19 % advance in the S&P 500. Chinese equities were low at Wednesday as the previous day’s euphoria over the Politburo’s statement of support for the beleaguered property sector and the promise of measures to boost consumption and the overall economy faded. Hong Kong’s Hang Seng Index retreated after Tuesday’s 4.1 % rebound and closed 69 points lower, that’s 0.4 % at 19,365. The tech index fell 0.9 % after a 6 % rally the previous day. And on the mainland, the Shanghai composite index slipped a third of a % to 3,223. The Hang Seng mainland properties index, which surged 14 % on Tuesday, retreated 1.8 % Wednesday.

Peter

And futures markets are pointing to a gain of 140 points for the Hang Seng at the open this morning, that’s around 0.7 %. And you can get more details on the latest market movements in my daily newsletter, which you’ll find at Peter Lewis Money talk. Sub stack. Com. Every Monday to Friday, this is Peter Lewis’s Money Talk. Let’s join our guests. We have with us in Prague this morning Andrew Ferris, the CEO of Econosis Advisory. Thank you for staying up for us once again on your world tour.

Andrew

Thank you. Perfectly all right, Peter. It’s a pleasure.

Peter

Okay. And over in Texas in the USA, we find Tony Ash, who is the founder of Complete Intelligence. Welcome, Tony.

Tony

Thank you, Peter. Thank you very much for having me.

Peter

You’re welcome. The Federal Reserve has raised the target rate there, as you heard, for the federal funds rate. So it raised the target range for the federal funds rates by 25 basis points to five and a quarter to five and a half %. That’s in line with market expectations and it was a unanimous decision from the FOMC. It brings borrowing costs to the highest level since January 2001. The Fed made minimal changes to its post meeting statements and failed to provide a clear indication of the FOMC’s future moves. The committee said it remained highly attentive to inflation risks and will continue to assess additional information and its implications for monetary policy, but it underscored the priority of bringing inflation back to the 2 % level. Andrew, let me ask you, how wed is the Fed to its 2 % level? Because it seems to me that if it is, there’s going to be more pain to come. The Fed is going to have to carry on raising rates and potentially tip the economy into recession to get there.

Andrew

Yeah, this is Peter. This is not an interpretation. This is effectively based in fact, because Powell was quoted in saying that he just doesn’t see that the 2 % inflation. I’m not quite sure what he actually said, or sorry, correction, the interpretation of what he actually said was whether this is going to stay till 2 % or we will not be able to get it there at 2 % in the year 2025. That is, well, I don’t know, strictly speaking, 24 months from now.

Peter

Yeah, that’s what I think he said. That’s what I think he did say, that he doesn’t anticipate it getting there to 2025.

Andrew

Then very, very briefly, of course, they’ve raised interest rates now to 525, 550. And then hopefully, let’s say, this will bring the inflation to %. And then, of course, the question is, is where they will be able to keep it at two % once the increases have failed it out or stopped? Because then, of course, the next expectation will be that they will start cutting interest rates. And if this will allow the inflation to begin to accelerate again, you know what I’m getting at? In other words, the scenario has to be a little bit more finessed. We don’t expect them to say, look, there is going to go at two % and then they will stay at 2 % despite the fact that it will start cutting interest rates. They are not saying that. But equally, they are not saying that enough is enough, 2 % will be there and that will keep the inflation there and that’s the end of the story. We don’t need to cut, we don’t need to increase. It’s a thankless task. Classical, have you stopped beating your wife? Kind of question. Whatever you say is wrong.

Peter

Tony, it is quite hard, isn’t it? To work out what is actually the Fed is saying. The markets initially took it quite positively, but then seemed to change their mind as the day wore on. But how do you see this?

Tony

I actually did not see it as doveish. It was interesting on the 2 %. He said we don’t see inflation hitting 2 % until 2025 or so. It could be later than 2025, his expectation hit 2 %. So on the one hand, we love the Fed raising rates, but on the other hand, we also have consumers and businesses paying higher inflation and seeing higher inflation. So there’s a real sense of urgency. At one point, Powell said policy is not restrictive enough or long enough to have its full intended effect. So he’s saying two things there. First of all, he doesn’t see policy as restrictive enough. Second of all, it hasn’t been in place long enough to have its full intended effect. He capped off that comment by saying, we have a long way to go. So this is the Fed chair saying these things. This is not some commentator. And so that’s the house of you. And when you keep in mind that it was a unanimous vote, to me, I actually saw this as a hawkish tilting press conference because there’s been this implied expectation that we’re going to get through 2023, and then in January of ’24 or so, we’re going to start seeing rate reductions.

Tony

But he made it pretty clear today that he doesn’t see rate reductions, certainly not in ’24 and probably later than that. So this elevated rate environment that we’re in right now, it sounds like he’s pretty comfortable here. Now, one thing also to keep in mind is we’re looking at year on year inflation with base effects. So this time last year in the US, crude oil was over $100. I think in June it hit $130 a barrel. And so if we’re looking at a 3 % core inflation rate in June with crude and secondary and torsionary impacts at $137, I think, once that comes down, that core inflation will rise even more. So there are other effects and he knows this. And I think what he’s doing is setting people up for September when those base effects really do come off and those inflation ratings are significantly higher likely. And people are saying, hey, you didn’t raise fast enough, or you didn’t continue raising fast enough. He’s conditioning people right now for the other side of these base effects, which will come in the second half of August and in September.

Peter

Yeah, I’m with you. I didn’t see how that was a particularly dovish statement. I saw plenty of things there which could indicate the Fed is going to continue. But I suppose, Andrew, the truth is in the matter, the Fed doesn’t mean now it’s until September. So we got four to two months of rounds of monthly data on jobs, inflation and consumer spending. The trend doesn’t seem particularly clear at the moment on any of them, does it? Andrew?

Andrew

Clearly, in terms of economics data, got a sound like an economist, the answer is yes and no, because the labor data, the job creation data have been strong. Inflation can down incredibly quickly if you think that a few weeks back, Peter, we’re talking at 6 %, and now it’s 3 %. But strangely enough, the PCE that used to be the favorite blue eyed boy or blue eyed girl to be politically correct, seems to have dropped out of the picture. So I’m not quite sure why now is the pure CPI inflation the one that we are gunning for. And yes, and hence the Fed has said that the turn economy do not see a recession, meaning two quarters back to back negative GDP growth, but definitely a slowing down in the economy. So what am I ended up with? I put all these things in a box, shake it out, let them drop on the floor, and I end up with the same mess.

Peter

So it is hard to read the words, but you mentioned something there that was noticeable in the statement, and that’s that Mr. Powell was saying the Fed now believes it can pull off a soft landing. He said the central bank’s own economists have now reversed their call that the US economy was going to enter recession. He said the staff now has a noticeable slowdown and growth starting later this year. But given the resilience of the economy recently, they are no longer forecasting a recession. What do you make of that?

Andrew

Sorry, is that me, Peter, you’re asking?

Peter

Sorry, I don’t want to talk to you. Yeah, sure. And then I’ll move on to Tony.

Andrew

Yeah, exactly that. And again, I always go back to the expression, what do they mean by recession? And given that they are in inverted commas American and they are in the Fed, they do mean two quarters back to back of negative GDP growth, which I will try to run with the numbers. I just can’t see this happening anytime soon under current circumstances. So if he means that, yes, I have no idea, he said this proudly that we’re going to soft land the economy and we’re going to have inflation down. And at the same time, as Tony also confirmed our suspicions, he says we’re going to bring the inflation down, but that ain’t going to happen till the year 24. If that, well, I hate when it becomes talmuric Bible interpretation of the words of the great master. And I mean, poor Powell, what else can he say? He will spell it out as clear as he can. And then we end up interpreting his words. And I think this is embarrassing.

Peter

Tony, he was rather self-congratulatory, wasn’t he, in his statement? He said, we’ve already done a lot already and we brought inflation down. He was saying, we’re going to get this soft landing now. Our own economists say that there’s not going to be a recession. He sounded rather proud of himself.

Tony

Yeah, but if you notice, he said our economists say there won’t be a recession. He didn’t say I, Jerome Powell, think there won’t be a recession. So he’s relying on the staff. So there’s deniability. And so I’ll tell you, at the beginning of ’23, what we were telling our clients is that we wouldn’t necessarily see a recession, but we would see very slow growth in Q3 and Q4. And I think that’s where this is just barely between 0 and 1 %. And I think that’s where Powell is heading. And I think that’s what he’s hedging toward is, the staff don’t see a they don’t see a recession, but we do expect a serious decelaration. And what he doesn’t want is a stagflationary environment where we do have a recession and we still have inflation. And this is I think is why he kept underscoring the fact that we have a long way to go. We’re not there yet. We’re not going to see recession. So he wants the optionality to be able to accelerate if needed and maybe not accelerate, but to continue to raise rates if needed. And I think he also doesn’t want to put the Fed in a position where they’re raising and then they’re lowering and they’re raising and they’re lowering because all that does is create uncertainty for people.

Tony

And it creates huge volatility, not just in markets, but also on the street, in the marketplace when people are buying homes or people are buying cars or buying groceries or whatever.

Andrew

Peter, I would like to add not only my full approval, but Tony has offered a pivoting point as far as I’m concerned. And that is, I will turn around to investment advisor stroke analysts and say, how dare you think that the Fed at any time is going to cut interest rates before year 25. Hello, they’re telling you this. Well, all right, it might change his mind as as data change, but unless the data are really spectacular, okay, we are going to be stuck with the number five for many years. I’m clearing my throat because we are now beginning to use the word 26 as opposed to just 24 or 25.

Peter

From what you’re both saying, really, it sounds like then that if economic activity slows in the final quarter of the year, the next phase, really, of this cycle is that the Fed just holds rates steady as inflation slows, which then means that inflation ingested, real rates are actually going higher, but it’s absolutely not going to cut. So am I right? Is that really what you’re saying? That’s going to be the next phase of this, assuming that we don’t get any more rate rises?

Andrew

I’ll jump again, Peter, and I will say yes.

Peter

Okay.

Andrew

Over to you, Tony.

Tony

Hey, Peter, I think that… Thanks for that. I think that we have to keep a couple of things in mind. First, rates are rising and companies and consumers are adjusting to that. Month by month, consumers put record amounts on credit each month. Consumers in the US had reserves to spend on price rises through, say, Q1 of 23, but now they don’t. And they’re having to buy things at these elevated prices on credit, and that’s a problem. Now, that’s on credit in rising interest rate environments, so that’s a problem. The other consideration is when we look at corporate earnings in the US, earnings have deteriorated in this quarter. We had great breakthrough earnings for Meta and other stuff, but they’re the exception, they’re not the rule. Earnings have deteriorated by about, I think, 3 % this quarter. I could be wrong there.

Peter

I think.

Tony

It’s.

Peter

Higher even. I think it may be higher than that, according to fact set.

Tony

Right. So we’re in a deteriorating earnings environment. And so companies are not able to continue to expand their margins like they have been able to do over the last two years. And so they’re feeling it on the financing side and they’re feeling it on the margin side. They’re also feeling it on the salary side because to hire people, it’s more and more expensive. And how mentioned payroll and salary quite a few times saying, really, inflation is a problem, but payrolls and employment are a real problem as well because they’re not slowing down.

Peter

And how is that then going to work its way out of the system? Is it going to be that there will be less vacancies advertised, or do you think there will actually be layoffs to try and ease the pressure before the latter?

Tony

I think there’ll be both. I think it’ll start with the former and end with the latter because when you have margin compression, when companies don’t have the margins or the earnings that they had in the past, they have to find places to cut costs. And we’re an environment right now where commodities generally are rising again. Those input costs are generally rising, but companies are going to have to find a way to cut some of their overhead so that they can get investors the earnings that they need. And so that’s going to have to come from somewhere. And it’s probably going to come in the form of headcount. Pex started doing this probably nine months ago, but it’s going to roll into other industry sectors as the margins begin to hurt.

Peter

And this Andrew is all going to come. Sorry, Andrew.

Andrew

No, no, no. Peter, you’re not in the place. You’re the boss here. I am not, again.

Peter

I was just going to say that really, what’s going to happen is that these layoffs are going to start, or the problems in the job markets are going to start also at the same time that people have used up all their paychecks from the stimulus and have run down their savings. So that’s presumably going to have quite a big hit on consumer confidence.

Andrew

Yes, but can I now… Yes, I cannot disagree on that. But can I twist the thing a little bit and bring two very important issues in here. And this is something that Tony has already touched. And I will, let’s say, try to stick my finger in the jugular, and that is what you buy in this market. Now, strictly speaking, if you really believe what Paolo is saying, I have no reason to disbelieve it at all, is really equities are going to be under pressure for the next two years by higher interest rates and a slow in economy. Okay, this is essential. And if you were to stick to bonds, then of course you will be permanently bedeviled at the time that the Fed may just begin to cut interest rates and therefore you’re going to be caught with a bundle of equities whose prices are falling. And in the middle of all that, I’m afraid I have to raise this because it really is really upsetting me. We are having in November, December, the COP meeting, that is the environment meeting of the United Nations, the 28th one taking place in Dubai. My God, what a horrible background situation.

Andrew

We are entering complete silence in the market. All the fires, the horrible weather. We’re back to the racism. We’re really thinking, Well, will the increase interest rates, decrease interest rates? There are two things here. There have to be colossal, but really colossal opportunities on climate updated investment because this is really ringing loudly and clear. Or on the other hand, given that I can tell you, because I observe this very, very closely for a number of clients, very little is being done. A lot is being done, but not anywhere near the 1.5 %. And given what has happened this year in the terms of the extremes weather we have had, and leave Greece aside, it was not just Greece, it was right through Europe, I think, Peter, to put it, let’s say, in a very gentle and diplomatically correct phrase, in the next five years, we are all going to be dead. So there will be a lot more things to worry rather than where their interest rates are going up.

Tony

Zilch.

Andrew

Influence in the market. Absolute silence. Nothing. Not one to use a good English expression, bloody word. I’m beginning to use to start to write in a great deal more without being alarmist. But this is the truth. This is what physically actually is happening. As Tony said, we’re going to have three more weeks whereby we’re going to die. Okay, if I was in Greece, we’ll have three more weeks where I’m going to die. Okay, so it’s not fun.

Peter

Tony, you’ve had the extreme weather as well, of course, in the US. Do you think this is going to start becoming a market issue?

Tony

I’m not sure. I don’t really have a view on that. It’s been hot in Texas this year, but I don’t know how much over normal it’s been hot. Last year it was pretty much the same pattern. So I honestly don’t know. The other thing that I… Just to add into what Peter said is, we have a situation where because of shutting down nuclear and other things, European countries particularly have started to rely on fossil fuels. And if we do enter a higher interest rate economic slowdown environment, there are very few economies, aside from Germany and Europe, that actually have the funds to subsidize the build out of green infrastructure.

Peter

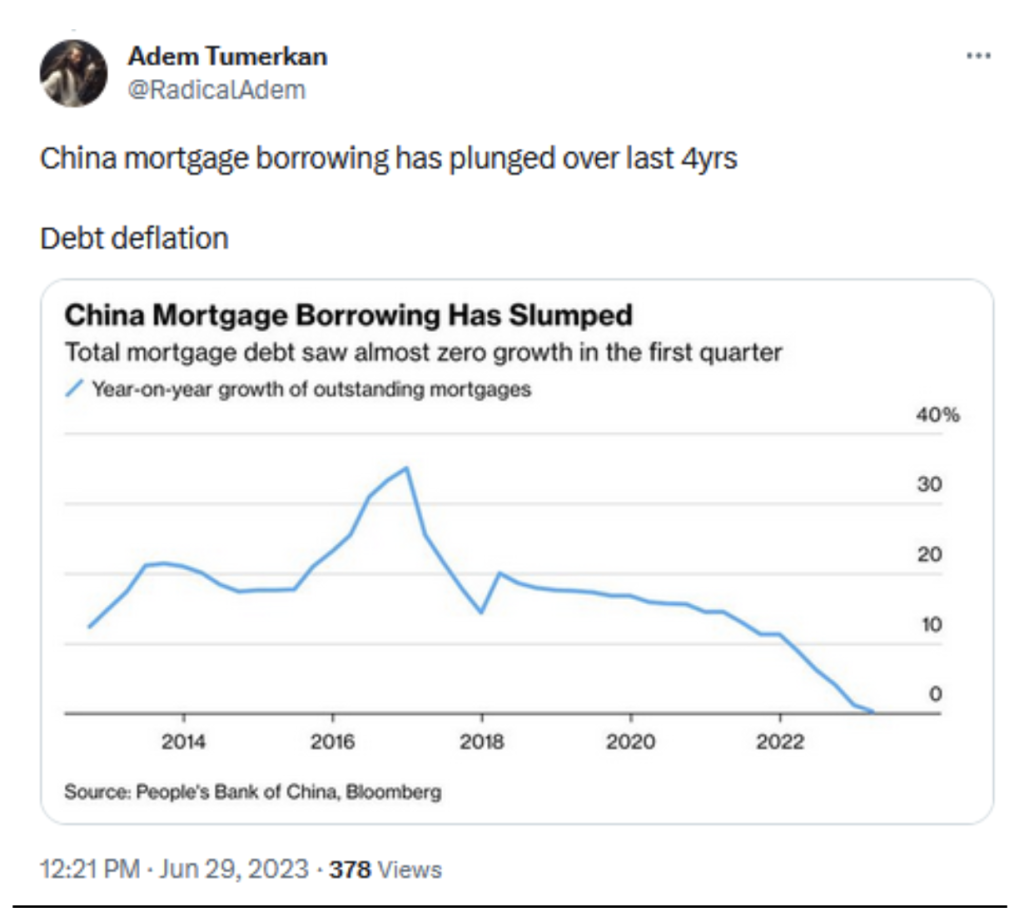

Andrew, let me bring up another subject then and see what you think about this if I throw it into the mix. China is very close to falling into deflation, isn’t it? Certainly, we’re seeing disinflation in China. What impact is that going to have on the rest of the world, including the US?

Andrew

Well, there are three things going here. This deflation is… Hello, Peter?

Peter

Yeah, I’m here.

Andrew

Sorry, very sorry. I thought I have lost you also as well. No, I’m here. We can hear you. Chinese deflation is completely domestically driven. It is a matter for the Chinese to worry about because it is not driven by external factors, it is driven primarily by the domestic weakness of the economy, number one. Number two is the Renminbi has been consistently weak, which means that as far as the Chinese export in inflation, you would always think it in terms of Chinese products are cheaper than ever. B oth because domest, the prices are falling and also because the Renminbi is weak. So that’s potentially it’s a deflationary rather than an inflationary pressure on the world. And the third point is one great big resounding warning that it is not true that we’re looking at global economy. We are looking at economies that have got very much phases on their own. And blessed the little boots of Japan, they’re still sticking to negative interest rates as if nothing has happened. A lot has happened, but their policy appears to be consistent, not necessarily correct, but consistent. So China cannot be a bad deflationary influence in the world.

Andrew

On the contrary, if Chinese goods are of some importance as input in other countries, then there are good news. They’re going to be cheaper.

Peter

Okay. Tony, what I was asking Andrew, just as you got cut off there, was the impact of China on all of this. China is very close now to slipping into deflation. Consumer price inflation is zero. On the producer price level, it’s already negative. What’s the risk that China exports deflation around the world?

Tony

I think China exporting deflation is really the status quo. That’s what they’ve done for the past 25 years. So if they go back into exporting deflation, which they were doing before the COVID supply chain inflation hit, it’s business as usual for China. But with the domestic CPI and PPIs as low as they are, because China is entering or has already entered a balance sheet recession, I think they may have to devalue to a level that they’re not quite comfortable with in order to actually export that deflation. So they need stimulus within China, but it’s really hard to see them borrowing more and taking more debt because their debt levels are so high. So there’s a real likelihood that we see notable devaluation of C&Y to really boost exports in China so that they can get more domestic economic activity.

Peter

Let me ask you finally, just very quickly about the European Central Bank. They’re meeting later today. Andrew, they’re expected to lift rates as well. I think the ECB is probably fair to say is in a more difficult position than the Fed, isn’t it?

Andrew

Well, to the extent that in absolute terms, they’re having a watching rate of inflation between 5 % and 5.5 % and everybody else apparently is having lower rate of inflation. And yes, politically it is tricky because there are equal voices. For example, the Italians asking for stronger, tighter monetary policy, and presumably everybody else is not so. So yes, they are not yet at the point that they are seeing some light at the end of the tunnel. Although somebody said sarcastically, yes, light at the end of the tunnel, there was another trend coming in the opposite direction. But yes, they’re having a tougher period because still the increases in interest rates are not paying off as clearly they are doing so far in the United States.

Peter

Tony, final word to you. The ECB, are they behind the curve?

Tony

I think they are a bit, but I do think that will enter again, like the US is in a base effect period because of high energy prices from a year ago in June. Europe is about to enter that zone where natural gas prices and energy price has really spiked in Europe. And I think they’ll have 2-3 months of very good inflation readings, meaning inflation moving in the right direction toward disinflation.

Peter

Thank you both very much. That was Tony Nash, founder of Complete Intelligence over in the USA, and Andrew Ferris, who is the CEO of Econosis Advisory.

Peter

I’m joined now by Ross Fe gold, who is Business Development Director at SafePro Group over in Taiwan. Good morning, Ross.

Ross

Good morning.

Peter

Now, China has announced the replacement of Foreign Minister Chen Gang. What month after he disappeared from public view, Mr. Chen had been seen as a close associate of President Xizhiangping, China’s state news agency, Xintong Rua, said on Tuesday that the country’s Parliament, the National People’s Congress, had removed Mr. Ching and remained and replaced him with the country’s most senior diplomate, who is Wang Yee, who was his predecessor as Foreign Minister. Ross, what on earth do you make of this? It’s quite an astonishing situation, isn’t it? We still don’t really know what has happened to ching gang.

Ross

Yeah, two key things here. One, as you said, we don’t really know what happened to ching gang. But two, and probably more importantly is, regardless of what transpired and what the reason is for Qngang being replaced after the unexplained absence, other than the brief mention that there was a health issue, is continuity. And especially with Wang Y ee coming back as Foreign Minister, and he was the more senior foreign policy official anyway, this is not going to herald a change in how China interacts with other countries, whether it’s the countries that it’s friendly with or the countries that it has a more transactional relationship or the countries that it has a difficult relationship, obviously. Most notable one in the latter group would be the United States, but also increasingly Japan, Australia and Western Europe.

Peter

But it does raise some serious questions, doesn’t it, about transparency? I mean, even by the standards of the opaqueness of the Chinese Communist Party, this is an astonishing situation because he was handpicked, wasn’t he, by President Jiz hongping for this role. He’d been the US ambassador, the Chinese ambassador to the US for just about two years, and then he was elevated massively into this position, and now suddenly, equally abruptly, has been removed from it. It suggests there’s some very odd things at the lease going on in the Chinese Foreign Ministry?

Ross

It certainly does. But unfortunately, as you said, this is an opaque and not a transparent government. So until they tell us more, we can only speculate. And I’m sure many of the listeners have heard or read about the various theories for why Qinggong was removed, other than simply being a health reason, allegations of corruption, extra marital affairs, even espionage. Maybe e will get more information from the government in the coming days or weeks, and maybe we won’t. That’s just the nature of the system. A lot of attention has been put on to the aspect that it was he J inping personally who elevated Q ingang above other potential candidates in the Chinese government to take on this role, which he did take on at a relatively young age compared to some of his predecessors. But our arguably, it also shows that he, when necessary, will change somebody that was close to him or somebody that he had mentored or elevated. If the facts demand that he does so, he’s not going to keep someone on who is a political liability. And perhaps ching on have become a political liability for reasons that we don’t know yet.

Ross

And that us, he made the change. So I’d be very careful, even though some people are rushing to say so, that this shows some weakness in C. J. Pink’s position. In fact, one might argue it actually shows the opposite.

Peter

But you could argue, couldn’t you, that when you’ve handpicked someone, particularly durably, without counsel and without proper due diligence, when that goes wrong and it turns out to be a bad decision for whatever reason, it would normally put your judgment into question, wouldn’t it?

Ross

Well, at minimum, it might put the due diligence. Did you do the right due diligence? It’s a question. But we see that even in more transparent and democratic systems where people were hiding something in their background in a criminal matter or extra marital affair. And then it comes out once they’re elevated to the next highest position. So I think it’s the due diligence aspect. And if there was something there with Qigong, not health related, did they overlook it? Did they just not know about it? Or did they know about it and decide that it’s okay, we’ll live with it as long as it doesn’t come out. But they were worried for whatever reason recently that it would come out. We just don’t know. We might never know. But again, I don’t think this is going to signal any weakness in C. J inping’s overall command of the government and the party.

Peter

What about Wang Yee? Is this a temporary move until Beijing can find a suitable successor? Clearly, they needed to stabilize the situation. They’ve got important meetings coming up, issues going on with the US, so they need a stable foreign policy. So he’s obviously a stable pair of hands because he’s done the job before. But is this just a temporary move, do you think?

Ross

The expectation is this will be temporary, but nobody could really define temporary. So as you said, they need a steady hand to come in and stabilize the Ministry in his more senior role Wong. He was more a big picture guy when it came to foreign policy decisions. And the person who holds the title of Foreign Minister, which Chngong had, is more about the operational aspects of the Foreign Ministry. Now, now, Long E has got to do both. This is a big bureaucracy, the Foreign Ministry I’m referring to, and it needs to be run day to day. So he needs to make decisions about spending budgets, promotions, things like that. So that’s a lot of work. I don’t think there’s any expectation that Long E will do this open ended, of course. Again, this being China, they might surprise us. But the expectation is that they will look for a more suitable, younger candidate who could do it for a number of years. And that would not be Wang Yee. And Wang Yee probably doesn’t even want to do it. He did it already. He had been promoted upstairs to the more senior role, and he’d probably enjoy that.

Ross

One more thing on this point. To their credit, especially when we think about competition with the United States, whether it’s the Foreign Minister or Wang Yee as the foreign policy guy, but within the party apparatus, they travel a lot. And that’s one of the reasons why often feels like the US or Western Europe are a bit behind in places like Central South America or Africa, or even more in more recent years, Oceana, the Pacific Island countries that’s gotten so much attention US China competition. But they really do travel a lot. And whether Wang Yee wants to take on that burden is also something he’s going to have to consider. It might factor in how long he does this job on a.

Peter

Temporary basis. It leaves Wang Yee in a very powerful position, really, doesn’t it? Because he’s on the Politburo. He’s come back to being the Foreign Minister. He’s probably one of the most powerful ministers we’ve seen in a long time in terms of his status. So presumably he’s got very close ties. He’s certainly very trusted by President XI J inping.

Ross

Yeah, without a doubt. And that’s why he was brought in to stabilize the situation. That’s why he does trust him, does look at him as someone who could stabilize the situation. But again, I don’t think the intention is that it would be a long term solution.

Peter