Get $200 OFF your CI Markets subscription: https://completeintel.com/save200/.

Welcome to “The Week Ahead” with your host Tony Nash. In this episode, we discussed three crucial topics:

1. Deposit flight, banking and deflation: Hugh Hendry discusses several topics in the episode. He talks about his willingness to buy during a significant market correction and expresses his belief in a potential credit event.

He also discusses the impact of higher interest rates on government policies, the devaluation of the Chinese yuan, and the relationship between the Federal Reserve and regional banks.

Hendry mentions the challenges faced by China due to its real estate market and the potential consequences of collapsing property prices. He highlights the fragility of the euro dollar system and predicts the end of the bond bull market.

Hendry also discusses the impact of green technologies on China’s power generation sector and expresses skepticism about their viability.

Overall, he shares his perspective on current market conditions and his strategies for investing, acknowledging the uncertainty and potential for significant changes in various factors.

2. How broken are wind and solar?: Tracy Shuchart highlights how higher interest rates are discouraging people from participating in green initiatives, despite governments wanting to promote them.

Tracy also mentions the potential for further consolidation in the banking industry, particularly among smaller banks, due to unrealized losses. She predicts that bailouts for more banks may be necessary and expresses concerns about banks not taking on sufficient risk.

Additionally, Tracy discusses the recent write-downs in the wind and solar industry, attributing them to rising interest rates. She suggests that higher rates undermine investments in the Green New Deal and the Green transition. Tracy also talks about the challenges in the US solar industry, the impact of tariffs or import bans from Asia, and China’s advantage in terms of resources and supply chain.

Lastly, she mentions her investment strategy in hard assets due to her belief in upcoming problems and emphasizes the importance of old and hard assets in her trading strategy.

3. The “melt up”: Albert Marko discusses the challenges faced by younger generations in affording homes due to artificially high real estate prices in the US, caused by cash buyers and low mortgage rates.

He also discusses the uncertainty surrounding the actions of the Chinese government regarding real estate valuations and the potential impact on their credit rating.

Furthermore, Marko highlights concerns about the banking industry, including the potential for consolidation and the risks faced by smaller banks.

He expresses skepticism about a potential “melt up” in stock prices and emphasizes the need for caution in the current market situation. Overall, he stresses the importance of monitoring economic factors and preparing for potential market disruptions.

Join us for a clear and concise analysis of these important topics in plain language you can understand. Stay informed for the week ahead! Don’t forget to like, subscribe, and share for more valuable insights.

Transcript

Tony Nash

Hi, everyone, and welcome to the week ahead. I’m Tony Nash. Today, we’re joined by Hugh Hendry, Tracy Shuchart, and Albert Marko. We’ve had a big week with the Fed meeting and the press conference. We’ve had some results come in. We have some relief in markets the back half of the week. But there’s some pretty critical things we want to talk about. The first thing I want to talk about with Hugh is banking. He’s talked for the last year about deposit flight and banking and potential for deflation in ’24, so I want to talk through that. Tracy has talked quite a lot this week about the wind and solar models being broken. We’re going to talk a little bit through that. Then we’re going to talk about the meltup in equities with Albert. That’s a little bit sarcastic. Let’s get there.

Tony Nash

We’re having a quick promotion for our CI Markets platform. This is our platform that forecasts currencies, commodities, equity indices, individual stocks, and global economics. Right now, you can get 40% off of prepaid annual subscription. It’s a limited time deal. That brings the price down from our normal $500 a year to $300 a year. Visit completeintel.com/save200. Use the promo code SAVE200 at checkout.

Tony Nash

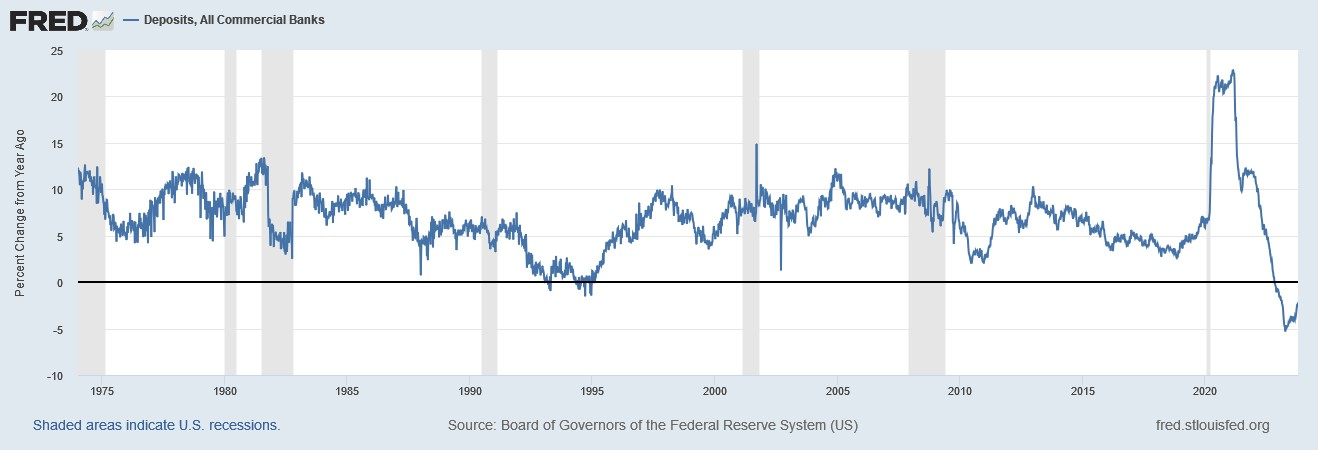

At the start. Hugh, thanks for taking the time. I really appreciate this. You’re in a beautiful location, and we’re all jealous. You’ve been talking about deposit flight since Q2 from US banks. Of course, this happened because of the duration risk at commercial banks when depositors moved money to money market funds and treasuries. We’re still seeing deposit flight. According to Fed data, this is on a year-on-year basis through I think last week. The gap appears to be narrowing a bit, but how stable is the US banking system given this deposit flight? Can you talk us through a little bit of that?

Hugh Hendry

Well, it’s a global issue, and it really relates, again, back to there are two agents within the economy which have been caught out, if you will, with the feds very aggressive hiking cycle for the last two years, one being the Treasury. I think the legendary Stan has been out for the last 10 days or so, lamenting on the Treasury’s decision not to extend majorities. And of course, the other was the banking sector or the wider financial sector, because there was something extraordinary in that period, late 2020 and all of ’21 when the majority of the private sector refinanced their rates. And of course, that made the Fed’s rate hiking somewhat impotent, or it certainly took a lot of time. And we’re still digesting the 4.9 % annualized growth. It took a lot of the potency of historic rate hikes out of the thing. But there was a transfer of interest rate risk within the community. So the household sector and corporates have been spared. And of course, that was then put on the balance sheets of insurance companies and those buying treasury bonds. The long dated, the US Treasury has been trading as low as 50 cents on the dollar.

Hugh Hendry

So the capital flight was twofold. Mostly, it is the income arbitrage. Why? I said, there’s still trillions of dollars on site accounts earning basis points. And slowly but surely, people need the money, and they either go to their internet account or they do something about it and they transfer, that’s flight. And then the other issue is the impairment. A bank essentially is a hedge fund that either owns treasury bonds or these index-linked securities called loans to the private sector. And we’ve seen a big impairment on the government bond holding. We know officially that’s half a trillion dollars, more than half a trillion dollars. And so that could be motivate a credit flight. That’s been very, very modest. That was only there in March of this year. But of course, here we are. And a lot of smart folk are getting really concerned about a slowdown in Q4, Q1 of next year. And we’ve yet to really see cyclical credit charges rise within the banking sector. So it’s an influx. The regional banks are trading at 40, 50 % discounts to NAB, which is a reflection of that uncertainty. And the only thing is perhaps that uncertainty is going to become less as we roll into the months and quarters ahead.

Hugh Hendry

But you’d imagine that the story is going to be adverse.

Tony Nash

Sure. We’ve heard people talk about credit events and these sorts of things. You say the uncertainty will become less. Do you think there’s a possibility of a credit event in the near term? Or do you think we’re largely past that?

Hugh Hendry

I do. The big thing in my world is Stan Druckenmiller. Stan is a god. I feel very uncomfortable because I differ from Stan in that I still believe in the prevailing cyclical behavior of our economy and the major participant being the Fed, which is to say that this leveraged economy, which needs more and more debt, really, as the dynamic for incremental GDP growth, By repricing the debt dramatically higher, I’ve been of the view that there would be a systemic economy-wide credit event. I still hope to this that over the next 12 months, you will see the Federal Reserve cut rates very, very rapidly and head back to zero. Then in that 12 to 24-month period, we might be talking about the Federal Reserves, but balance sheet again moving to $15 or $20 trillion. I still think there’s one last cycle of that nature stands like, No, no, they can’t do that anymore. Again, but that requires, your central question in the thrust world is the credit event. I’m assuming a credit event. Then lastly, I’m assuming a global credit event because, again, the private US sector largely vaccinated itself against the Fed, but overseas agents and primarily the Chinese government and the Chinese serial fakesh GDP thing, if it worked, the transmission was zero Fed rates, and it clearly doesn’t work.

Hugh Hendry

And so the fear that I have more widely and the need for the Federal Reserve to come back down to the SERC region would be a further profound movement, especially in the cross currency, you’re seeing it with the Yen and then the Chinese, the Juan, really seeing the anchor around the 7:30 and heading closer to 8, if not in the direction of 9, I think that would precipitate enormous need for the Federal Reserve to change tack dramatically and aggressively.

Tony Nash

Let’s talk about China for a minute, because Albert said, I don’t know, six or nine months ago that if the Fed heads to six, China is going to be in a lot of trouble. We’re at 5.5 right now. From your perspective, why does that cause problems for China? I know we have this big real estate issue in China. We also have commercial real estate issues here in the US. Why is Fed policy such a big problem for China right now?

Hugh Hendry

Well, it’s the global over valuation of everything. For a property, we could just as well discuss the private equity industry and these are trillions of dollars large. The last 15 years, Professor Michael Pettis out of Peking University calls it the Bezos. Sometimes fraudulently, but in 90 % of the cases, we just mistakenly over-egged just how rich we were and how good the prospects were. And so assets, typically at the economic level, match the liabilities. So asset values are inflated, which allows a huge amount of debt to GDP. So it’s a collateral. And we start to see collateral in.

Tony Nash

Sorry, just a second. You’re-

Hugh Hendry

Then you have to, again, my. Oh, heavens, you lost me a bit.

Albert Marko

That’s all right. We got you back.

Tony Nash

We got you back. Yeah, we got you back. We got you back now.

Hugh Hendry

Okay, forgive me.

Hugh Hendry

Let me check if it jumps to my Wi-Fi. It should be working. Anyway, the impairment of assets and the need to distribute wealth from the Chinese have pursued that years and they’ve robbed the wealth of the consumer. And now the question of just how much more they can rob the consumer of their wealth because you’re seeing it in severely low sales figures like private consumption. So the consumption to GDP excluding the government sector is astonishingly low. The ability to bring.

Tony Nash

You talk about assets being valued very high. We have that in the US with the real estate prices right now. We have that in China with real estate prices, even though things have come off a little bit, I think the hope with rising interest rates was that some of those real estate prices would come down both here and in China. We haven’t really seen it that much. Albert, what do you think? What’s the problem? Why are the prices so sticky right now?

Albert Marko

Well, I mean, first of all, you have cash buyers selling from up north and buying the south. And on top of that, you have people with two and three % rates that simply don’t want to or can’t move to any other homes at the moment. There’s no inventory and it’s keeping the prices artificially high. It’s a political problem both ways because the boomers have a lot of cash in the real estate market, which they don’t want to give up. But then you have the youth vote where there are crying that they can’t afford a home and they’re still living with their parents. It’s a problem both ways. I don’t really see how it gets resolved, to be honest with you. As long as you have those cash buyers willing to step in on any type of dip in the rates, I don’t see housing in the United States really crashing per se.

Tony Nash

Okay. Do you guys see the Chinese government allowing the valuation of real estate to fall dramatically? Because that effectively takes the savings that Chinese consumers had. And if they collapse real estate prices, then a lot of that savings that the Chinese had really gets disappeared overnight, right?

Albert Marko

To be honest with you, it’s over my pay grade because to try to figure out what the Chinese want internally and how it affects their credit rating and their leveraged loans and politically, it’s too hard for me to even think about it.

Tony Nash

Hugh, what do you see there?

Hugh Hendry

Well, on both fronts. With regard to the US, I would say, I think it’s pretty obvious what happens. If rates stay at this level or higher, property prices and other risk asset prices, I think, could fall 40%, especially in the property. Or rates, they collapse very rapidly and therefore you don’t have that 40% reduction.

Tony Nash

Okay, so you’re expecting rates to fall pretty dramatically in ’24. Is it like this? We’ve got a huge demographic of people who are, say, baby boomers and they’re voting and they don’t want their wealth to disappear. We’ve got all of these commercial real estate loans that are being marked down pretty dramatically. The Fed will have to reduce rates so that that big voting block of boomers doesn’t lose wealth and so that commercial real estate valuations don’t fall dramatically. That saves the banking system. Is that where you’re going?

Hugh Hendry

I guess where I’m going, we’ve got all of those zombie real estate loans. We’ve got all of those bank holdings of treasury bonds. It’s trading an enormous haircut. We have presently the cyclical credit cost in the bank PNL was really, really low. And then finally we have the diversification model blowing up. Everything correlated. The 60-40 equity bonds thing, everything is correlated. And my guess, again, is if we just stay at this level, it’s going to… There’s going to be a big reveal. There’s going to be more of the March episode where we’re going to see we’re going to see corpses. And I think we’re going to see the economy just sees. And the seizure comes rapidly, bankruptcy and hemmingway. On the China front, regardless of the painting the tape, if you will, by the authorities, Chinese properties, we’ve determined the Chinese Communist Party, we’ve determined that prices haven’t fallen. Their problem is the people have marked it. They’re like, Oh, O’Meard is way below, and it’s not producing anything. And it had the luster because in people’s heads, mentally, they had it. They were factoring in, I don’t know, seven to 12 to 15 % annual price appreciation.

Hugh Hendry

And now they’re like, it’s zero, and it’s probably negative if that’s huge. The only, not the only power, but a very powerful force available to the Chinese administration is to revalue the property in dollar terms. Yeah, that’s a very effective way. And you could say, Oh, the domestic population don’t see it. They only see it in renminbi. And that’s the scenario that takes you to a nine-.

Tony Nash

A nine to the dollar? Yeah.

Hugh Hendry

A nine to the dollar. And that’s profoundly deflationary. Again, that will take you into the zero interest rate. And I just think I’ve been talking about this for two years. I’m running out of rope for that talk. This is a first quarter, first four months of ’24. We got to see it. Then that’s my expectation.

Tony Nash

You expect notable deval of CNY in the first quarter of ’24?

Hugh Hendry

Yeah.

Tony Nash

Okay.

Hugh Hendry

That’s very tied to where we are just now, and it’s all coming out of Tokyo and that hitting the 150, the dollar Yen. And in heaven’s do not… I was at the laundry in Gustav here. I was having my chocolate croisson. I was like, there was news out overnight. The Japanese government like, Oh, we got it. Our poles are down. The good folk are taking in the ass with price inflation because the Yen has been very weak. They’re like, Hey, we had this great idea. We’re going to have a supplementary stimulus package. We’re going to spend $200 billion or whatever. And I thought, What is? So my life is I ask myself questions why is sky blue? What is the primary surplus deficit in Japan? I should know, but I was like, you got to revisit that. And really, really, really far. It’s huge the deficit, enormous, and they keep adding to it. And you remember, the Japanese 10-year is 91 basis points, roughly. We hit 500 basis points in the US. Five hundred basis points, if you put… And with short rates in the US being five and a half, being minus 20 basis points in Japan, Japan’s interest servicing in terms of its lean on the budget, 7.7 %.

Hugh Hendry

And the US is at 4.4. I mean, imagine if Japan really. The world is a perilous place. But for all the peril, for the good for watching this, you just got to say, the S&P is a remarkably robust institution. It may be reliant on those seven stocks, but it’s also reliant on that flow that comes in all the time.

Hugh Hendry

So. When I say I’m looking for a credit event, unfortunately, we live in an over leveraged environment where that’s possible and it’s happening more frequency than 100 years of data would suggest. And that again, speaks to just the quantum of debt that’s outstanding. But it has to be now. It has to be here we are in November, and I’m talking about… I’m still talking about this in April. Closer to me down.

Tony Nash

Yeah. You always take a very different perspective on things. What else are you thinking about right now as you look at markets? What are the big pain points that you’re seeing right now?

Hugh Hendry

I mean, for all that I’ve said about the rates coming down, the major drama of today is that the what I call the crazy faction, the the Peter shifts of this world. The whole dollar being dethroned. I was lamenting there on the perilous nature of the Japanese fiscal balance sheet. And of course, Druckenmillers and everyone else will tell you that the problems of the thing just stopping, the entitlement, the inflation, which was a 2035, 2040 thing is like, come on, we’ve got to start answering it now because it’s getting closer. But with the rate rise, we’re talking about it being 2025 to 2027. That’s an environment where that would be a hundred years since the denouement of the previous global currency regime, the gold regime, which eventually became gold was replaced by dollar treasury bills. And again, we’re coming back to this notion of impairment in the reserve currency asset and what happens. And so I’m doing a lot of thought about if the whole thing breaks down, what do you want? A lot of people previously have said, Well, you would own the likes of Apple. But actually, Apple doesn’t work because Apple just sells iPhones and services, and it gets dollars, but we could be at a point where who wants dollars?

Hugh Hendry

You’ve been an arbitrage. Well, maybe Bill Gates seems to be buying all that agricultural land. Actually, if I’ve got steaks, if I’ve got cattle, that’s not cash, but that’s something you actually need for life. I’m trying to think, what do you own if you get profound impairment in the reserve currency asset is something that’s occupying me?

Hugh Hendry

I think that’s the real question, right? Is what is it? If it’s not dollars, what? We’ve been talking about that here on the show for over a year.

Albert Marko

Bullets.

Albert Marko

You own bullets.

Tony Nash

Yeah, exactly.

Tracy Shuchart

You know I’m all about hard assets.

Tony Nash

Right, you are.

AI

Heads up for a short break.

AI

Are you using the potential of AI in your portfolio management strategies? With an impressive 94.7% forecast accuracy on average, you can confidently integrate AI into your approach with CI Markets. Visualize the potential volatility of your portfolio over the next 12 months and gain insights into specific assets that might experience fluctuations. This empowers you to make informed decisions on when to buy, sell, or hold. CI Markets covers a wide range of over 1,600 assets, including stocks, commodities, forex, indices, and economic indicators. Imagine running limitless portfolio scenarios to optimize your gains. Curious about the outcome of removing or adding certain assets? Wondering how your portfolio might evolve in the next 3, 6, or 12 months? Ci markets equips you with answers to these crucial questions. Whether you seek a streamlined portfolio analysis, wish to explore diverse scenarios, or aspire to track your investments with precision, CI Markets is the ultimate tool for you. Ready to learn more? Visit us at completeintel.com/markets.

AI

Thank you.

AI

Now back to the show.

Tony Nash

Tracy, you put out a tweet earlier about… Because he was talking a little bit about an event and some difficult things and difficult trade-offs. During the Fed meeting, you tweeted out where Powell had said, The Fed has been working a lot with financial institutions to make sure they have a plan for how to deal with unrealized losses. If we’re seeing this credit event, you tweeted this out saying, read, taxpayers prepare for bailouts. What do you think about the magnitude of that? Do you really think this is coming? Do you really think bailouts for more banks is coming?

Tracy Shuchart

Absolutely. I think we’re still set to see a lot more consolidation in the industry. We have still a lot of small banks in the US, like 4,500 small banks. We are seeing more and more consolidation. I think that is set to continue. I don’t think anything… I don’t think what we saw earlier this year with SPV and that mini banking crisis is set to end. I think that we’re still going to see problems within some of these smaller banks, especially with what they are exposed to. Moody’s even came out and said that some of the smaller banks are sitting on 650 billion dollars worth of unrealized losses right now. I think that is going to be a problem for smaller banks, and I don’t think we’ll see further consolidation. This is nothing new. This started in the banking crisis of 2007, ’08 with the fall of Lehman Brothers. We saw a huge consolidation with the larger banks. I think now it’s going to be bigger banks swallowing smaller banks.

Tony Nash

More of that. Albert’s told us before that the Fed hates regional banks and they hate smaller banks. Why is that, Albert?

Albert Marko

Because it counteracts any type of tightening policy that they’re implementing. The regional banks will do what they’re going to do because they’re at the forefront of mid-sized companies. I’m not issuing loans out. I know they don’t like them. I think what Tracy was saying about bank consolidation is probably right. I think what he was saying about the credit issues is right because, from what I’ve heard, Bank of America is insolvent. That’s a looming problem that I don’t think anybody’s really talked about or addressed. You want to talk about a Lehman moment? Imagine if BSA crashed. They would have a problem there. That’s something I’d want to certainly keep my eye on in the next 6-12 months.

Tony Nash

Yeah, but okay, let’s say that’s true, and I’m assuming it is. Does it surprise anybody that a systemically important bank is insolvent? I mean, they’re backed up by the US government. Do they really have any worries?

Hugh Hendry

Well, the worry is the what do we call a disintermediation? It’s the banks sponsor and spread economic vitality via the credit transmission. The impairment and them not feeling good about their world means that they are not risk-seekers. Banks get such a… It’s hard being a bank. Everyone hates you when you’re a bank. They hate you because you take too much risk or you take too little risk. You can’t really win. But we’re in an environment where they’re not volunteering to take risk. That just tends to mean that at the margin, the economy will suffer. That’s not a good thing.

Tony Nash

Small companies suffer or mid-sized companies suffer because they can’t borrow, right?

Hugh Hendry

Indeed. But it’s more than that because we can go, again, esoterically into this matrix like world of the euro dollar system. And Jeff Snyder, who just the locus of all knowledge about the euro dollars and the euro dollar system, he thinks it’s broken. I don’t think it’s broken. I think it’s just that system, which creates unregulated lending. And with infinite leverage is not showing up. That it’s not excited either by the remuneration or by the risk reward payoff from extending new credit. And so, again, we’re at an environment where it feels very fragile, it can break. And we’ve just gone through the most preposterous attempt to restart the credit mechanism via the IPO window. And you look at that and it’s like the scoring being carried across the river by the frog halfway over and the scoring kills the frog. He’s like, What are you dying, croaking words? Why did you do that? Because that’s who I am. It’s like, Why? That’s really the best companies. Birkenstock, Arm, which is just a huge plaster on SoftBank. I think SoftBank is a zero company in my world, and that was a desperate attempt to stave off bankruptcy and the market’s all through.

Hugh Hendry

I see credit just being pulled and yanked away everywhere. But then, so how my mind works is I work with irony and paradox. The world’s greatest investor, Stan, and the world’s second greatest investor, someone like Jeff Gundlach, they’ve worked around. Within three to five years, the US Treasury System model doesn’t work. It stops. It stops because of where rates are, it stops because you’ve got a debt multiple. The debt is a multiple of GDP that you’re running deficit. You’re having to borrow more and more every year. It becomes like this S curve. They’ve said, This thing breaks. The dollar breaks within five years. Okay? Stan is like, Yeah, I’ve really bought a lot of two year, but I can’t see how the long end of the market comes down. My mind is a mess, but I work with drama. I think everyone takes their intellectual leadership. Everyone is very fearful. We’ve seen the bonds trade there. They’re getting a rally to four and a half. But I… We’ll see. I just think that the bond bull market that began 40 years ago in 1982 will end in that spectrum that style and emerges with the Treasury.

Hugh Hendry

But the people who are either shorting or saying, I won’t own bonds will be the ones who own it when we get that credit event. So my idea is if you look at TLT, it fell from 180 to 80 decline. I think it can go back to 140 to 160. And in that environment, I want to be shorted. Markets are likely to give you drama and irony. When we started the bull market, we were in a profound recession with the Fed hiking rates. And from early 1981 to the summer of ’82, if there was anything going on in your mind, you had to clearly see the visible trace of inflation declining. Michael Steinhardt bought bonds. He bought treasuries, and he was sued by his clients. That’s the crazy stuff. So I’m expecting a crazy, very sharp halt in the economic progress of the US and where it becomes less of an outlaw and it joins Europe and China with their travails, the Fed does something very, very dramatic. And then fast forward two years and we’re talking about, hey, listen, the Fed’s got a $20 trillion balance sheet and the treasury model doesn’t work. It’s the end of the dollar system.

Albert Marko

Oh, thank God.

Hugh Hendry

We can’t.

Tony Nash

Honestly, that’s the most plausible scenario I’ve heard about the end of the dollar system, Hugh. I mean –

Albert Marko

Yeah, I would agree.

Tony Nash

-cny and other currencies and commodity-based currencies and all this other nonsense. But the Fed doing itself in is the most plausible scenario I’ve heard. Albert?

Albert Marko

Yeah, of course, that is. I mean, the issue I have with this is this is a Yellen versus Powell conflicting policies that’s ongoing that’s causing a bigger problem. I think Yellen’s actions certainly would shorten the lifespan of the dollar without question, and you can see that. But Powell was pretty clear that if long rates were to suddenly fall because of Yellen, he’d have to step on the gas and tightening again. That’s the only thing I’ve heard about that during the Fed minutes. Maybe Yellen can get us to 4.7, but that’s going to be hard beyond that. It’s just not going to be enough this late in the cycle to get the equities where she wants them for political optics, in my opinion. They’re definitely going to have to use the dollar, take it down to 100 to rally a market. But that’s just my opinion.

Tony Nash

What do I know? They’ve got some good progress over the past 24 hours, right?

Albert Marko

Yeah. Oh, God, yes, they did. We were at 4,400 October 18th, 19th, whatever it was.

Albert Marko

It was a.

Albert Marko

Couple of weeks ago. It’s unbelievable what they’ve done.

Tony Nash

That’s right.

Hugh Hendry

Okay. I think you give them too much credit. I think these things just pop up. But on that the dollar and all this nonsense that it’s going to be other countries that take it down, the dollar system ends when it’s rejected domestically by the US. When the US says, This is not working for us. That’s how it ends. I think that becomes closer. You’ve already seen a dramatic devaluation by the Japanese. And if that leads into the one, then the will be so great that it’s actually the US that comes and brings global leaders together and says, We got to think of a new way of doing this.

Tony Nash

Yep. I think as you talk about Japan and China, I think the best proxy for what’s actually happening in China in my book is Korea. We have to watch the Korean won. We have to watch Korean economy to really understand what’s happening inside of China. It’s a microcosm, very small microcosm, I believe, and I’ve watched it for years of what’s actually happening in China. It’ll be interesting to watch that play out.

AI

Heads up for a short break.

AI

Want to take control of your investments and predict the stock market? CI Markets is the self-directed trading platform that provides 94.7% accurate forecasts for over 1,600 stocks, ETFs, forex, commodities, market indices, and economics.

AI

With CI Markets you can manage your own investments with ease and supercharge your trading experience. Sign up for CI Markets today and get 40% off your annual subscription with the code SAVE200.

AI

Thank you and now back to the show.

Tony Nash

Okay, so as we watched the wind blow through Hugh’s hair and we all wish we were in Saint Barth’s, Tracy, let’s talk about wind and solar for a minute.

Tracy Shuchart

Nice segue.

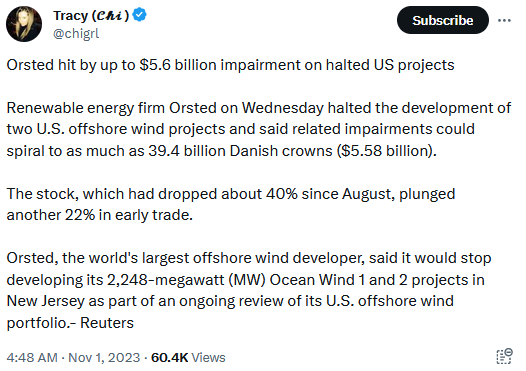

Tony Nash

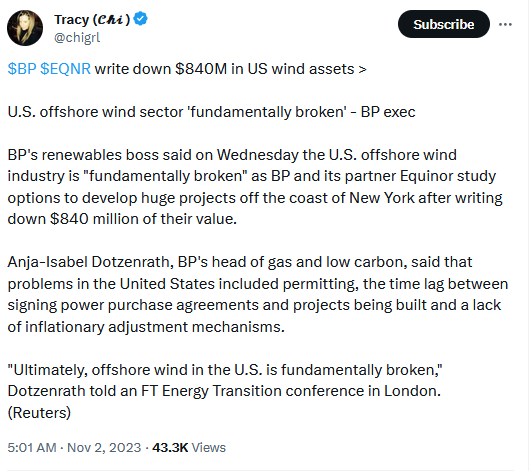

You like that? We saw some serious write-downs of wind and solar this week. First on Wednesday, we saw Orsted abandon two US offshore wind projects. The estimated write-down was about five and a half billion US dollars. Orsted is the largest offshore wind developer in the world, and they had already received about a billion dollars of subsidies from the New Jersey government. If Orsted can’t make offshore wind work, who can? We also saw Equinor write down $840 million for Offshore New York. Both of those guys are blaming government delays and red tape. But I think it’s a little bit weird that those companies that have benefited so much from government subsidies and regulation are now blaming governments for their losses. I guess the real question is why is this happening now? Probably cost of money, but that’s one of the questions I want to go into. But the irony, if we look at wind, is these next tweets that you put out where one talks about Sunrun taking a $1.2 billion charge, which Sunrun is the largest solar installer in the US. Then in the very next or the previous tweet, you talked about how coal hits a record in India with 16.1% growth in September.

Tony Nash

What’s happening? We’re supposed to be in this green new period. I know that you and Albert and I have a bias against the viability of these business models, but I think we need to try to figure out what’s really happening here and why are these guys doing these huge write offs?

Tracy Shuchart

Well, I think at this point you have to understand that first you have supply chain issues and all the things that existed before. Obviously, there’s still inflation. But the core of this is rising rates. Because all of these projects take a lot of money and a lot of borrowing to make them come to fruition. With rising rates, these projects become unviable, economically speaking. With inflation rates and such as… Let’s step back a few months when we go Orsted, for example.

Tracy Shuchart

A few months earlier, asked, or I think it was mid-October, sorry, they basically said to New York, if you want us to make this project viable, we’re going to have to charge you 55% more per kilowatt, meaning we’re going to have… You’re going to have to pass this on to your consumer, obviously. What are you going to do as a utility company? The utility company just said this is breathtaking enormous. We didn’t expect this whatsoever. And so they denied the request. And that’s really what brought on them bearing down the write down and said, okay, well, then we can’t do this project. We’re going to walk away from this. And so I think that you’re going to find that happening more and more as these projects balloon in price, even with government subsidies, they’re ballooning in price and they’re just not affordable without charging the consumer more and without charging the utility companies more. Nobody want… Even New York, which is about as liberal as you’re going to get, said, No, this is a red line on this project. It’s going to cost too much money. It’s going to cost us too much money. It’s going to cost our consumers too much money.

Tony Nash

Okay. Is the Green New Deal and the Green transition, all that stuff really something that only works in a NERP and ZERP environment? Is this a canary in the coal mine of different types of investments in industries that we’ve seen?

Tracy Shuchart

Absolutely, I think it is. They’ve only thrived in that environment. As soon as we see rates rise and these projects balloon in price, they become more and more economically unfeasible.

Tony Nash

Okay. Because the opposite factor of your coal tweet and your solar tweet was so interesting to me because you just have to wonder, as interest are the cost of money. As money costs more, we can’t spend on these things like wind farms and solar and all this other stuff because the installation cost is so high. Are the running costs high? Maybe, maybe not. I think there’s different data saying different things. But the really cheap cost of coal when money is expensive is really to me on a volume basis.

Tracy Shuchart

Absolutely, it is. If we take, for example, what just happened this week is that we had the German economic minister basically was approached by one of their nuclear facilities that said, We can bring this back online. We can do this cheaply. They said no, and opted for more coal because that was even cheaper than bringing that project back online. We’re seeing… Higher interest rates are literally doing the opposite of these government’s brand new jobs.

Tony Nash

You guys, correct me if I’m wrong, but if I recall correctly, it was 2008 and ’09 after the financial crisis that Spain and Germany spent huge amounts of money subsidizing solar. That really led to China developing a lot of their solar industry. Is that right?

Tracy Shuchart

Yes, absolutely. You said you guys, I didn’t know who you wanted to answer. All three of you. Yes, absolutely. Here’s the problem is we’ve seen what’s happening right now is I put out a tweet about what’s happening in the US solar industry, and I got a lot of responses that said, Well, just place tariffs on China, which we have, or ban imports altogether from Asia. Now that’s easier said than done because if we did that, first of all, we’re not that far down the supply chain enough, or we’re not built out enough in the US to cover those needs yet. Manufacturing wise, we don’t produce enough to cover our own needs at this point. Then we also have a problem is that if you cut these people off, you ban this, then you balloon solar project budgets by 10 billion footlong. You’re pricing everybody out of the market. We’re not talking about solar panels for your roof. We’re talking about big commercial projects that are fed into utility grids.

Tony Nash

Right. Okay. What does that do for… China makes more solar than anybody. They’re the green leader. They’re doing EV cars than anybody. As money costs more, how does that impact the ability of China to grow their green power generation sector?

Tracy Shuchart

Well, I think that… I mean, China is going to grow the green power sector, but you have to realize this is coming off of a very, very, very low base. Everybody’s just looking at, Oh, my God, they’ve done X amount, which is really just the rate of change, but it’s not really the biggest part of their entire energy makeup. If we look at what they’re doing, coal is still a majority of their power. They can take the rest of that. The thing with China is that not only do they have the minerals, but it’s easy to produce there. Their permitting process is totally different. They also process these minerals. Because it’s not just sticking them out of the ground, you need to process them. They’ve got the whole supply chain already there, and they’re 20 years ahead of us.

Tony Nash

Right. Just for reference, and tell me if I’m wrong here, but I believe coal is still something like 74% of power generation in China. Is that right?

Tracy Shuchart

Yeah, correct.

Tony Nash

All these green products are being produced by coal?

Tracy Shuchart

Correct.

Tony Nash

Okay. Go ahead.

Tracy Shuchart

Essentially, yes.

Tony Nash

Okay. Hugh, what’s your view on this? As green technologies become more expensive to build, those factories become more expensive to build, that thing, what’s the impact on a place like China? Because we just talked about Chinese currency having a deval, all this other stuff. Do you think there’s a major impact on China and their position as the ability to produce green technologies?

Hugh Hendry

Well, I thought you were on a pretty sound footing with the cost of money and the engagement with the green technology. Whilst, of course, indigenous or domestic sources of energy are very much from coal in China, at the margin in terms of globally, China dominates solar panels. The Europeans had a goal, but we have a goal. Our economic models require investment on the basis of a return on investment. The Chinese have a different system, again, which is predicated on the Fed being at zero. The Chinese system creates GDP growth, not wealth, because it doesn’t require the reciprocal of a return. But the big issue that we had with the Huawei or no way, the cell station software companies like Ericsson and Nokia, those stocks have disappeared. They’re still quoted, but they’ve fallen 90 odd % in the last 15 years because there’s just no economic vitality, no return, no profit return. Whereas the Chinese dominated because they’re like, We strategically want to own these areas. And so they will own those areas at the expense of a return. And that has serious repercussions for the rest of the world. But for sure, the great capital cost of implementing these huge green schemes into electrical grids in the West, they do not work with the present price of money.

Hugh Hendry

And then I have to confess, I’ve been so grotesquely wrong on the uranium sector. And when I say I’ve wanted to participate, I’ve participated in uranium bull markets. And again, I’m suffering from too much drama. People get it. Chemical, I think, was it this week or a week ago? They had results. Stock was zooming, zooming, zooming. People talk about the Magic Seven and the S&P. I mean, look at those uranium stocks. Incredible, right? But I was going to push it back to Tracy or Albert. The capital cost of a new nuclear scheme keeps going up, and at the present, interest rates is really, really hard, and it requires an increasing tariff subsidy from the government, which is unwilling to give it for solar and wind. Is it more willing to give it for nuclear? I’m not so sure. What’s keeping it going? Question.

Albert Marko

I don’t know. From personal experience, that was not nuclear, but for oil terminals, I had a colleague of mine looking for financing to build out a terminal for major oil companies, and this financing was minimum 12%. That’s just not doable. That ruins the economics of anything you want to do, whether it be fossil fuels or nuclear or whatnot. It’s just not conceivable, in my opinion.

Tony Nash

Minimum 12% for an oil terminal. Imagine what a small company loans are. That’s crazy. Tracy, I want to come back to you on this. We saw wage growth is slowing in the US. Consumers are starting to be fatigued. We’re starting to see companies not able to push margin and price like they have been. Do you believe that US consumers are willing if, say, these green technologies are more expensive and say, the production costs are more expensive for electricity, are there consumers in the US willing to spend more to know that their power is generated by solar or wind or something else like that?

Tracy Shuchart

Absolutely not. There’s already been a million studies on this. If you’re seeing utility companies balk at these prices, trust me, the US consumer has already said, We love to be green, but if it’s going to cost me an extra $1,200 a year, thanks, but no thanks.

Tony Nash

It’s a nice to have.

Tracy Shuchart

Especially, as long as their power is on and they have heat and they have air conditioning.

Tony Nash

Right.

Tracy Shuchart

Let’s be honest, the American consumer cares in theory, but doesn’t care when it comes to their pocketbook. It doesn’t care when it comes to their budget. Especially when you have inflation ripping. We could talk, food prices are still high, gas prices are still high, utility. Still inflation is hurting the consumer. Obviously, they’re not going to… It sounds nice and all, but when it comes down to it, and again, there have been a lot of polls and studies on this that the American consumers just not. You are feeding my kid lunch.

Tony Nash

Even the Germans are opting for coal.

Tracy Shuchart

Even the Germans are opting for coal, which is completely crazy to me. But that’s a whole other story, and we’ve talked about that often.

Tony Nash

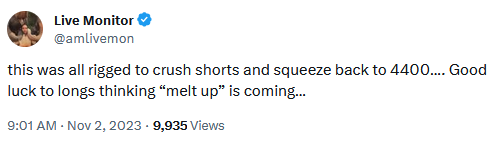

Many times. Okay, great. Thanks for that. Albert, let’s talk about the melt up. We’ve seen it over the past couple of days in markets. They obviously turned since the Fed meeting. Albert reported fairly well on Thursday. We had 78% of companies beat on earnings this quarter. Yet, and it’s hard to imagine, you put out a sarcastic tweet about a melt up saying this was all rigged to crush shorts and squeeze back to 4400. Good luck to Longs thinking the melt up is coming. Why are you killing the melt up vibe?

Albert Marko

For me, the Fed and Treasury, they love long rates up here, higher for longer because it’s doing the dirty work for them, so they don’t have to take the political blowback of the markets crashing down or whatever problems that arise from it. Right now I’m glad that I’m a thousand miles away from you because you might punch me at the moment. But I think in 2024, I think they rally long rates hard again. I think equities certainly aren’t pricing in five and a quarter on the 10-year as anything other than a passing phase. With rates rallying again, they bring down the equity back into a range of 4,150 to 4,500, which they seem to love to keep us in this range to crush longs at the high and crush shorts at the-

Tony Nash

You’re at the precipice of doom and hope, right?

Albert Marko

They’ve been doing this back and forth.

Albert Marko

It’s silly. They’ve been doing this back and forth, and it’s killing money. Left and right portfolios are getting absolutely crushed. I’ve run through the numbers. The net buying required for them to move the long end is like the market cap of Apple. It’s not really that big a deal for them to move it back and forth. That includes the 10, 20, and 30 years. My bond take isn’t really bullish equities, simply because I think what they’re using the long rate for the duration of 2024 to keep the market in check. I think after the election, I don’t know what happens after that because they don’t really have the political restrictions involved.

Tony Nash

Let’s talk about the Magnificent Seven for a minute. Everyone’s favorite, Jim Cramer, came out and praised the Magnificent Seven. You talk about, if we strip those out, the S&P is in negative territory. Can you tell us about those stocks and how they’re used to goose markets?

Albert Marko

Well, I mean, there’s no… I mean, I’ve said this for how many years? Three years? Two or three. That they used about a dozen stocks, a dozen tech stocks to rally the market whenever they felt like it. I just think this mag of seven stocks just going into the atmosphere whenever the markets seem to want to break down into the 3,900s or 3,800s, it’s a bit silly. How can you really look at this market with seven stocks holding the whole thing up and saying that it’s a healthy market? For me, I can’t do it. I just can’t do it. I need to see something or a credit event like Hugh talks about or some bank breakdown or something happens where this corrects this market into normal territory. I just don’t like it, to be honest with you.

Tony Nash

Okay, so what’s normal territory? Sorry, go ahead, Tracy.

Tracy Shuchart

I call this tech trade, this Magseven or Feng or whatever you… Whatever the hot ones are today, the Pav loves dog trade. It’s the tech. It’s that everybody wants to be in the tech sector since 2009. That’s all they can do. You know what I’m saying? They’re just conditioned. Every dip gets bought, not realizing that we’re in a completely different environment than we have been for the.

Albert Marko

Last time. I don’t think that rate hikes are to be done with. I think that inflation comes back a little bit over in Q1, Q2, and I think they have to hike again. Could you imagine Powell hiking in 2024? What a disaster that would be.

Tony Nash

I think you want to see it, though.

Albert Marko

I do want to see it. I like chaos. I might as well see it. It gives you some opportunity, buy or sell, whatever.

Tony Nash

Okay. When you say take markets down to normal levels, what does that mean to you?

Albert Marko

I think fair value is 3,800 in my opinion.

Tony Nash

Okay.

Albert Marko

That’s a 3,600. That’s just my opinion. Who knows?

Tony Nash

Okay. We could potentially see that in Q1?

Albert Marko

I think so. I would love to see that in the end of Q1. I would absolutely love to buy that going into an election.

Tony Nash

Great. Okay.

Albert Marko

I see Hugh over there pacing already.

Tony Nash

Yeah, Hugh and you are on opposite ends of the spectrum.

Tracy Shuchart

Oh, yeah.

Albert Marko

I’m Waiting for the onslaught.

Tony Nash

Right. Come on in, Hugh.

Hugh Hendry

I’m the heavens. I was just looking at the so far interest rate expectations curve. And since, was it last Thursday when we had the 4.9 annualized GDP, the markets have now pretty much priced a quarter basis point cut from June of next year at the margin. And you get it in the commentary of the Bill Gross, Ackman, Gundlach, Stan. Everyone’s back channel. Something is just giving and breaking. I’m in the market where I want to buy things. I always give people my confession. I get a bit of a aromatized because I made 50 % in the month of October 2008, made 32 that founding year. But my huge regret is what happened five months later. Because five months later, at the end of March 2009, the S&P had fallen 60 %. I was on a train in China, a slow train. I wasn’t buying that damn S&P. I said to myself, The next time we get a 3, 4 standard deviation type correction in a principal macro asset class, I’m buying it. I’m damn buying it. I’ve been doing that via limited cost call options on the TLT, the ultra-long. The last two months have been, I’ve just stopped using Twitter, to be honest. I’m just-.

Albert Marko

Oh, yeah.

Hugh Hendry

But if you look at the charts and the bottom where we’re etching into that TLT market, the next step is I want to physically… I want to start buying more and more of it. But to move, I still maintain that for it to move, it moves and it moves rapidly under duress that something breaks in it. That’s just my gut. That’s how I’ve set the world works. But just to clarify, I want to buy things, but in a world where everything is overvalued, I have to buy this grotesque pig-like entity of the US out for long treasury. My expectation is that it probably moves on the basis of some pretty ugly economic events taking place in the next six months.

Tony Nash

I think we’re all fairly uncertain, right? Are we all in that place where… I know, Albert, you and Hugh are on opposites, but I think I get to read that we’re all a little bit uncertain.

Albert Marko

Well, we are, we’re not. I do think that this market has come down, and I think Hugh does also in some manner, fashion, or whatever triggers it. I think we’re pretty much on par there. We’re just so overvalued. How does it break? What breaks? And does the Fed step in and make this soft landing that they’ve created the narrative of for the past two years now? I don’t know. I don’t know. I don’t know what breaks.

Tony Nash

Go ahead, Tracy.

Tracy Shuchart

This is why this is one of my myriad of bases for old and hard assets right now. Just going to throw that out there now because I’m the only one that I know that I can trade trade every year.

Tony Nash

You can find that back in six months.

Albert Marko

For me, it’s just like they haven’t fixed inflation. And if they haven’t fixed inflation, especially with Europe and Asia completely in a zombie status at the moment, I think there’s going to be problems in the next 6-12 months. That’s the basis of where I’m getting at.

Tony Nash

Yeah, I suspect, and we’ll close on this. I suspect that we already know what’s going to break, but we just don’t want to let it break yet. That’s my suspicion. I don’t think it’s a big mystery what’s going to break, but we all know what’s going to break. It’s just we haven’t let it break yet. When that happens, then all the things that you guys talk about is going to happen. Does that make sense?

Albert Marko

Fair enough.

Hugh Hendry

It’s hideous. What’s the thing that’s going to break?

Tony Nash

Well, what have we talked about? We’ve talked about banks, we’ve talked about real estate. We’ve talked about Japan, we’ve talked about China. There’s enough out there that we’ve talked about that can break, that can bring about some dramatic change. I don’t know that there’s going to be some mysterious thing that’s going to come to the front of where, Oh, we never thought about that. I suspect we already know what it is. It’s just a matter of us allowing it to break and the timing of it.

Hugh Hendry

Yeah, okay.

Tony Nash

You don’t accept that?

Hugh Hendry

No, I think what Powell said, again, if we just take when the wheel stops, where does it stop? Let’s say it stops on dollar Yen. You’ve gone from something traded 100, 110, now trades 150.

Tony Nash

Oh, gosh. It traded ’76 in 2012. I mean, the magnitude of the range of that is huge, right?

Hugh Hendry

But the ’76 was when you had the systemic, the tsunami, the nuclear thing of that nature. Without that, and it was a very short, compressed moment. It was 110 for 15 years. It’s now 150. They’re walking back the yield curve control, the movement in the 10 year again. These are standard deviation. These are irregular movements. And your 90 basis points, and like I said, interest and you’ve got the overnight rates are still negative 20. And yet, the Japanese government’s interest expense on that is almost eight % of GDP. We’re saying the US is within five years of breaking. I mean, where’s Japan? And again, what I love about Japan, because my thing is irony, it’s paradox. So Japan was the instigator of quantitative easing. They’re this great bogeyman of the of the consensus, the printing of money, which is really the printing of the capacity to print money. Japan had to do it 27 different ways and still doesn’t seem to print money. What if actually the Japanese quantitative easing, they actually found the resolve to print money, that they actually used all of those JJB bank reserves as collateral to borrow dollars and then to take term and credit risk into China.

Hugh Hendry

I’m talking about over the… They did it silently in an invisible manner via the Euro dollar system over the last 15 years and probably powered and contributed to that S curve in Chinese property. And then when the Evergrande thing went over, surprise, surprise, but that’s when the Dollar, Yen, if you will, the Yen strength peaked. And it’s been downhill ever since. Now we’re 150. And I feel like the famous words of Bruce Kovner, when it was at 300 is like, Call me crazy. But market’s whispering in my year 100. It was 100. It’s now 150. Call me crazy. Market’s whispering 300. It’s all there. It’s in front of us. It’s right there. Right there.

Tony Nash

Yeah. I really do think it was well laid out. I think we know one of the things that’s going to break and it’s going to happen and it’s not a mystery. It’s just the magnitude and when and it’ll happen. It’ll happen. It’ll happen in the next three months, six months, whatever, but it’ll happen.

Hugh Hendry

I think what we’re saying is we can see a profound disturbance in the force.

Albert Marko

There’s a better way –

Hugh Hendry

Profound disturbance there. But what we don’t know is the knock, how it reverberates, but it’s going to knock something. My estimation will see it knock into the Chinese Remembers rate. And I think that’s perhaps the most systemically important price level just now that the world is confronted with.

Tony Nash

I think you’re right. Guys, this has been amazing. Thank you so much for your time. Really appreciate the thought always that you guys put into this. So thank you so much. Have a great weekend. Have a great week ahead. Thank you.

Albert Marko

Thanks, guys. Thanks, Tony.

Tracy Shuchart

Thank you.

AI

That’s it for this week’s episode of The Week Ahead.

AI

Please don’t forget to rate us and review on whatever platform you are watching or listening to this. Thank you.