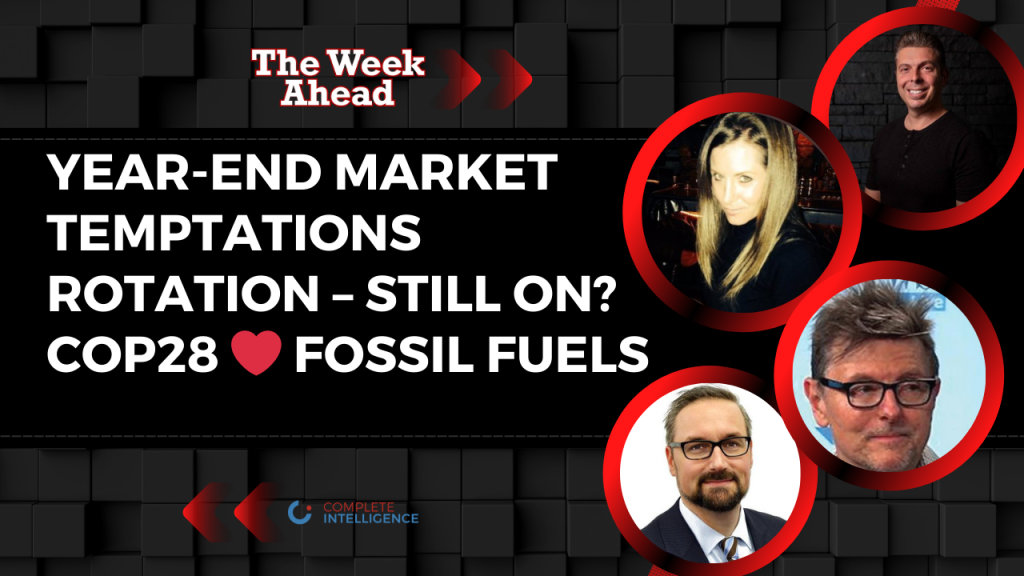

Year-End Market Temptations; Rotation – Still On?; and COP28 & Fossil Fuels

This Week Ahead episode is joined by Anthony Crudele, Michael Belkin and Tracy Shuchart. They discuss Year-end market temptations, Rotation – still on? and COP28 ❤️ fossil fuels.

Russia’s growing relationships; Upcoming Elections; and LatAm’s Battle of Ideas

This Week Ahead episode is joined by Albert Marko, Virginia Tuckey and

Ralph Schoellhammer. They discuss Russia’s growing relationships, Upcoming elections and LatAm’s Battle of Ideas.

BFM 89.9 Market Watch: Oil Prices Heading South

In this podcast, Tony Nash provides insights into diverse market sectors. Despite OPEC+ committing to supply cuts until March 2024, oil prices have reached a six-month low. Additionally, he delves into the Federal Reserve’s potential next move in light of job data.

Bullish economic resilience; Fed and inflation targeting; and Oil (OPEC) and Silver

This Week Ahead episode is joined by Jonny Matthews, Albert Marko and

Tracy Shuchart. They discuss various topics such as Bullish economic resilience, Fed and inflation targeting and Oil (OPEC) and Silver (ready for liftoff?).

The Upcoming USD Squeeze; Year-end market check; and China, US & geopolitics

This Week Ahead episode is joined by Michael Ncoletos, Bob Iaccino and Albert Marko. They discuss various topics such as The Upcoming USD Squeeze, Year-end market check and China, US & geopolitics.

BFM 89.9 Market Watch: Oil Prices Appear Irrational

In this podcast Tony Nash shares insights on various market sectors. They delve into topics such as US equity markets, tech valuations, oil markets, OPEC Plus meetings, and the performance of gold. The discussion also covers the impact of rising inflation and agriculture prices on the margins of agriculture companies, as well as the forecasted slowing demand from farmers.

The Stock Market. Gone! | Record Oil Demand & Growing Gas Supply | China, US & Geopolitics

This Week Ahead episode is joined by Tony Greer, Tracy Shuchart and Albert Marko. They discuss various topics such as The stock market. Gone., Record oil demand & growing gas supply and China, US & geopolitics.

Rates & earnings quality; Dollar and elections; and Death of new nuclear power

This Week Ahead episode is joined by Bob Elliott and Albert Marko. They discuss various topics such as Rates, market pricing & earnings quality, Dollar, commodities and elections and SMR: Death of nuclear power?

US Stocks’ Current Winning Streak: Sustainable?

In this segment, they discuss the recent performance of global markets, particularly focusing on the US stock market and trends impacting the outlook for the global insurance industry. They also feature an interview with Tony Nash, CEO of Complete Intelligence, who shares insights on the sustainability of the rally in equities, earnings in different sectors, the US economy, energy prices, and gold prices. Additionally, they cover the earnings report of Disney and Arm Holdings.

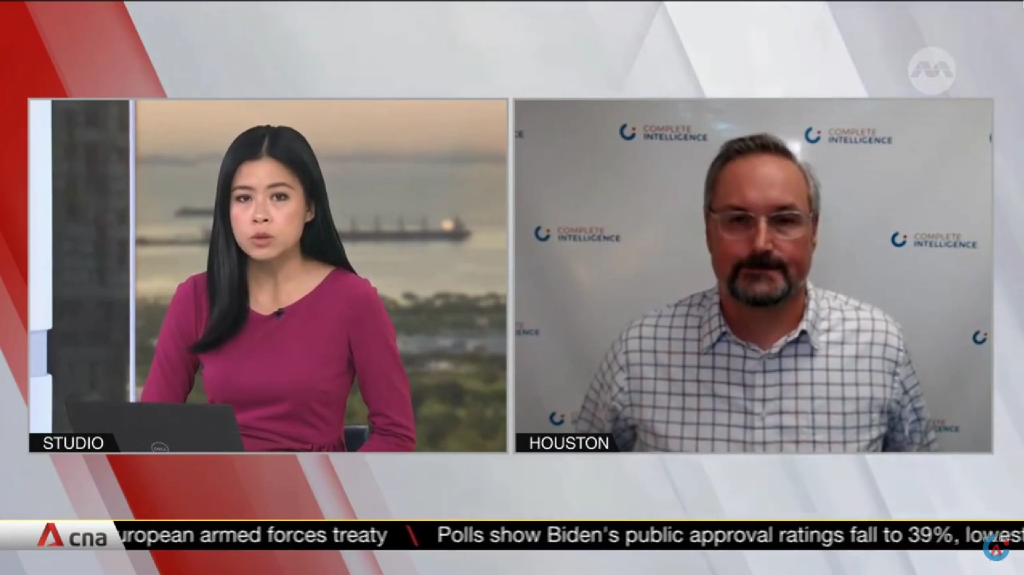

CNA: Oil Prices, Currency Moves, and Economic Outlook: A Market

The recent plunge in oil prices due to concerns over w demand, as well as impact of the Israel-Hamas conflict and weak trade data from China. There is also a discussion on currency movements, particularly the weakening of the dollar and concerns about China’s exchange rate policy.