Explore your CI Futures options: https://completeintel.com/futures

In this episode of the Week Ahead, Tony Nash hosts a panel discussion with Albert Marko and Adem Tumerkan, covering the economics of electric vehicles (EVs), trading the debt ceiling, and China’s post-Covid opening.

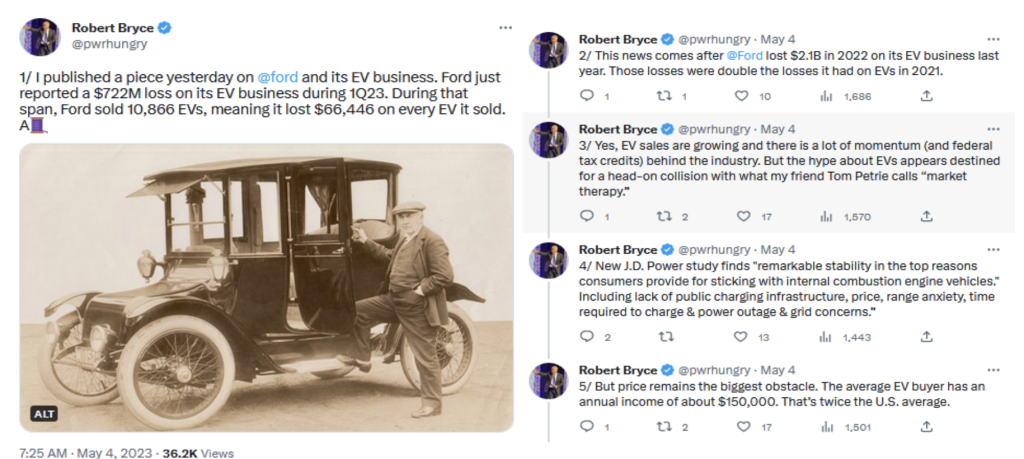

Albert delves into the economics of EVs, highlighting Ford’s significant losses of $2.1 billion in their EV unit for FY 2022 and an additional $722 million loss in Q1 2023. Tony references insights from Robert Bryce, revealing that Ford incurs a hefty loss of $66,000 on each EV produced. The panel discusses the EV drive on Capitol Hill and among car manufacturers, linking it to influential donors invested in ESG and carbon credits. Tony raises questions about companies’ motives, while Adem expresses concerns about the saturated EV market, Ford’s losses, and Tesla’s price cuts. They explore strategies such as spinning off EV units and meeting emissions standards with carbon credits.

Shifting the focus to trading the debt ceiling, Tony highlights a sense of optimism and hope despite previous negative news. Reuters suggests a debt ceiling rally is on the horizon. The panel anticipates an agreement unlikely before mid-June and assures that a default is not expected. They interpret Janet Yellen’s varying statements as a strategy to create market turmoil and pressure Republicans for a better debt ceiling deal. The influx of California’s income taxes in mid-June may affect the Republicans’ stance. The panel predicts market volatility and suggests a potential stimulus package later in the year to appease voters during the election season. Adem analyzes the impact of the debt ceiling on bank reserves and liquidity, predicting potential fragility in the system. He recommends focusing on the longer end of the yield curve and discusses the possibility of a credit crunch and its consequences.

Adem sheds light on China’s disappointing post-Covid opening, highlighting structural issues, high debt levels, defaults on infrastructure projects, and a weak consumer base. Tony emphasizes Adem’s recent tweets revealing the reasons behind China’s weak reopening. Adam elaborates on China’s weak reopening, explaining the negative impact of its current account surplus on consumer demand. Tony contrasts Asian economies with high savings due to historical volatility to credit in the West, which is based on stability. Adem highlights the Chinese government’s repression of consumption, leading individuals to save, which funds state-owned enterprises and infrastructure projects.

Looking ahead, Albert focuses on the debt ceiling while also mentioning the importance of monitoring oil prices and the potential for a secondary inflation event. Adam emphasizes the significance of China’s retail sales and current account data, as well as the crowded trades in the tech and regional bank sectors. He expresses contrarian views on shorting tech and recommends investing in longer-term bonds.

Key themes:

1. Economics of EVs

2. How to trade the Debt Ceiling

3. Anemic China

This is the 66th episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

Albert: https://twitter.com/amlivemon

Adem: https://twitter.com/RadicalAdem

Transcript

Tony

Hi, everyone, and welcome to the Week Ahead. I’m Tony Nash. This week we’re joined by Albert Marko and Adam Tumerkan. There’s a lot going on with debt ceiling and Fed, and obviously we’ve seen markets late in the week start to it really accelerated a bit. And we have a few things to talk about this week. First, we’re going to start with EVs. We saw some numbers come out with Ford over the last couple of weeks, and I wanted to cover this. So we’re going to go to EVs a little bit, the economics of EVs. We’re also going to talk about how to trade the debt ceiling. We’re getting into that part of the debt ceiling discussion where it’s kind of on and off again, and so this is where it gets really fun. So we’re going to talk a little bit about that, what’s going on in Capitol Hill, and kind of how to trade it. And then we’re going to talk about China. We’re going to talk about kind of anemic China, and Adam’s going to go into that a fair bit. So, guys, thanks so much for taking your time today. I always appreciate this.

Tony

Albert, I wanted to talk to you about EVs. We saw that Ford reported a $2.1 billion loss for their EV unit in fiscal 22. And then with their Q1 earnings, they reported another $722,000,000 loss. So if they keep that up, that’s almost a $4 billion loss for this fiscal year. If they keep that up we’ve got some Tweets up from a guy named Robert Bryce. I don’t know him, but it’s a really good thread. So I wanted to put it up, and I’m sure he’s a great guy. So if you guys want to follow him, that’s fine. But what he’s saying is that Ford loses $66,000 on every EV it sells, which just seems crazy to me.

So we see the reality of Ford’s P and L, and then we hear kind of the unicorns and rainbows of EVs. And I’m just curious, can you walk us through some of the economics of EVs? And we see Tesla making a profit now, but we see Ford kind of having a tough time with it. So how does this work out?

Albert

It doesn’t work out. They’re all lost. They don’t make any money. I mean, Tesla doesn’t make they can report that they’re making money, but they’re not really making money on the cars. They might be making a little bit of money with tax manipulation or services subsidies. Yeah, that’s one of the things. The costs are so high that without government rebates, no one can afford EVs. Porsche, I believe, was they said that their cars are about 140,000 for the base model take on EVs. If you were to buy them right off for them making no money, that’s what it would cost. But a lot of these companies, they need government rebates to be able to be in this game long term. And that’s where this little drive or the EV push out of manufacturers is coming. The reality is that manufacturers need government subsidies, government help, stimulus bills, so on and so forth. So they have to play ball. Politically, the material that is needed for EVs is much higher than normal combustion engines. So there’s just no value add, there’s less jobs that will be produced. So that’s a little bit of savings on the manufacturers.

Albert

Now, the big one that absolutely nobody is talking about is recalls, depending because of the fire risk to the manufacturers once fires start popping up. I mean, you saw a couple of Tesla, but once they start happening because of certain defects in the materials or the engineering, those costs are unknown right now to manufacturers. Nobody wants to talk about that yet.

Tony

Yeah. In the neighborhood next to mine last year, we had a Tesla autopilot crash and it burned and the fire was so hot that it melted the pavement below the car. Both people in the car died, and the fire department could really do nothing but wait for it to burn out.

Albert

Yeah, I mean, you even have instances of spontaneous combustion of Teslas and other EVs in the garages as they’re charging overnight. And they’re just this is really an unknown thing that manufacturers are going to have to struggle with, and investors are going to have to try to figure out how to price in when they’re talking about going long. EV companies or GM, Ford and Tesla.

Tony

Yeah. I guess one of the questions I have in terms of the economics is on some level it’s a little bit more like a laptop manufacturing process than a traditional car manufacturing process. I mean, when I talk about EVs and people, I say, look, it’s a laptop with wheels. And I know that’s a huge oversimplification, but you’re sourcing a lot more electronics, you’re sourcing batteries, there’s a lot of code, there’s software updates, all of this stuff. Right. So I’ve always wondered, for the traditional automakers like the Fords and the GMs and the Porsches and these sorts of guys, I don’t really know that it’s necessarily something that they have an advantage for. Maybe they have an advantage on the distribution. I have no idea. But the manufacturing process is very different. And Ford even now has three different business units, one for commercial, one for consumer, and then one for EVs, because the entire process is so different from the traditional auto manufacturing process.

Albert

Yeah. And the costs associated with retooling factories and opening up new factories really still hasn’t been factored in, in my opinion. I think in the future you’ll start seeing some massive drawdowns in finances from these companies.

AI

With CI futures, you can access AIpowered market forecasting for as low as $20 a month get 94.7% market forecast accuracy for over 1000 assets across commodities, currencies, equity indices, economics and stocks with weekly updates one month and three month error rates and top ten and bottom correlations. You can rely on CI Futures to help you make informed decisions. Join a growing number of satisfied users who have already transformed the way they invest with CI Futures. Don’t wait. Start forecasting with confidence today for as low as $20 a month.

Tony

Yeah, and so a couple of things. So Inflation Reduction Act. Without the Inflation Reduction Act, would the earnings of guys like Ford look a lot worse?

Albert

Oh, absolutely. Without those rebates kicking in and all these other inflation tailwinds, it’d be a lot worse. It’d probably be a third of what they’re reporting being just wiped away.

Tony

Okay, and so what is the drive on Capitol Hill for this? I mean, I know we have the AOCs in that group who are pushing the Green New Deal. I understand that, but say, you’re generic politician, why are they pushing for this? Because EVs are typically bought by people who make $150,000 a year or more. Okay? And so it’s not a broad base of the population who can actually use this stuff right now. So why are politicians angling for this? And as I asked that question, I live in Texas, and this week, Texas has started discussing putting a tax on EVs because EVs don’t pay gasoline tax, so they’re not paying for any road care. Right? Gasoline tax? Part of what gasoline tax goes for is road maintenance and new roads and that sort of thing. So Texas is looking at, I think it’s $300 a year for EV owners, and that will go for maintenance and upgrades of roads. But on Capitol Hill, why is there such a push for this?

Albert

Mainly because the donors behind the politicians are so heavily invested in ESG and carbon con, I mean, carbon credits programs and whatnot. So that’s where the push comes from. It comes from Wall Street.

Tony

Okay? And then the companies like Ford and these other publicly traded companies, are they just trying to get kind of the valuation uplift in the short term? I mean, that’s kind of what I assume is they’re getting a valuation uplift because they’re kind of doing EVs, and then by the time, say, the downside comes, that CEO will be out of the seat. Is that kind of the game they’re playing? Or is there something more and I know this sounds really cynical, I know there are people watching who really support EVs. So give us some comments or whatever, but I’m just curious, are they true believers that we have to have electric automobiles? Or are they more focused on kind of shareholder value, value creation short termism, and then they’ll worry about all the details later on?

Albert

That’s exactly right. They’re sitting there just to boost their stock price and then satisfy their investors. I mean, anything EV was just flying in the stock market, and they’re just playing it. I don’t blame them. I mean, I’d probably do the same thing if I was the CEO and sit there and raise money off of the stock valuations afterwards, there’s no question. I mean, if they really wanted to do something for the end for clean air and whatnot, they would have had bi fuel with natural gas like the Saudis and the Germans used to have, it’s clean burning.

Tony

I lived in Asia for a long, long time. Every single well, probably not now, but up until a few years ago, every single taxi in Hong Kong was natural gas powered. And so very clean, right?

Albert

Very clean. And there’s no cheap. Yeah. There’s no adjusting the factories. I mean, it’s just a couple of bolts, couple tanks and whatnot. It’s a kit that can bolt right on.

Tony

Right? Yeah. Adam, what do you think about this on the EV front?

Adem

Yeah. So I agree. I think the EV market is getting kind of saturated, especially at a pretty bad time, like you said, Ford, they reported huge losses on every EV they made. We saw the price I’m sorry. Yeah, the Tesla price cuts recently. And I think that there’s just going to be a glut of cars manufacturers trying to get sales going at a time where you have auto loans increasing pretty significantly. Negative equity is increasing on cars. These car prices are falling not as much, but in year over year terms they have so we’ve seen negative equity build. We’ve seen. Like Capital One, I believe. Wells Fargo. They already started closing and divesting their auto loan underwriting area. So I just think it’s going to be there’s only really two options you would have as a car manufacturer if they were able to restrict inventory the last couple of years to keep prices higher. But when you’re having others cut prices like Tesla, I think it’s just going to start leading to potentially a price war, which will be good for the consumer, but it’s not going to help these companies.

Tony

Right. So do you think we’ll see, and I know this may be a little bit early in the game, but would we see a company like Ford maybe spin off their EV unit and let it accept those losses and let the shareholders kind of hold it until it becomes profitable? Or do you think it’s so core to their business that they’ve got to hold onto it?

Adem

I think if it keeps losing money like this, they might have to do something like that. But I do think every car company kind of won’t. They’re banking on EVs for the future with probably more government subsidies. They’re going to do more infrastructure. So I’d imagine they want to keep those things. But yeah, it’s definitely a possibility.

Tony

And they help to balance out their overall emissions standards. Requirements, right. All the cafe standards. So I guess they have to keep it for that.

Adem

Some kind of net neutrality, like carbon credits or something. Yeah, they would need something. So them using EVs I think it can net out for them.

Tony

Yeah, okay. And you make a good point about auto loans. I mean, with that happening, and especially with the price point that EVs are at and with interest rates rising, I think that’s a huge factor that we see coming as people start to look at their spend every month and how to allocate it and what to do. I think it’s going to be a really interesting trade off that we see, and I hope these guys can figure it out. I hate to see the subsidies continue to pile on, but let’s see what happens there’s.

Let’s talk about the debt ceiling. Obviously, we’ve got things going between, say, US. House of Representatives leader Kevin McCarthy and the White House with Joe Biden, and Biden has delegated a couple people to negotiate on his behalf.

All that’s great. There was a lot of excitement this week that we may have an agreement by this weekend, which seemed really kind of silly when people got excited about it. But this debt ceiling debate comes up almost every year. Not every year, but almost every year. I think we saw back in 2011 and even more recently than that, where national parks people and other federal government employees were kind of furloughed and all this sort of thing.

Tony

I haven’t expected it to. We also hear Yellen say that the US. Government will be out of money by June 1. I’ve never expected a debt ceiling agreement by June 1. We’ve always expected volatility toward going into the end of May and in early June. Most of the people who I see who’ve been around the block a little bit expect the same thing, although we hear a lot of kind of hand wringing in a lot of the financial media, which it’s serious. If there really is a default, that’s serious, but default really isn’t on the table. So, Albert, you know Capitol Hill a lot better than I do. Can you kind of give us an idea of what’s happening on the ground and what some of the implications are of the discussions that are happening right now?

Albert

I’ve tweeted this and said this many times, but both sides are let me put it in a way that one of the GOP guys told me. Both sides are in World War II and entrenched in their positions, just waiting the other one out. Normally, I would say the debt ceiling thing, it’ll get done, bunch of grandstanding, so on and so forth. The problem this time around is that the majorities in the Congressional, in the House and the Senate are so thin that it’s a problem, right? It’s a problem from actually finding a deal because you could always get 1012 House members to defect just because they got elections coming up and it wouldn’t be a problem. But the numbers don’t work this time around for that. And the failsafe for some of the hardcore Republicans in the House is that they can call a vote for McCarthy’s leadership, which would stall any kind of legislation from going through. On the flip side, in the Senate, you don’t really have the Democrats unified to get the debt ceiling done because of some of the because some of the details involved of workers worker rights, I think it was like, that requirement to find work for unemployment.

Albert

Some of the EV stuff, some of the cuts, and a couple of programs that the Democrats were actually venmo against. So, like I said, I don’t think the deal is going to be done until probably mid June. The whole June 1 deadline is complete nonsense. Just ignore that. The US. Will be able to pay their bills up until late August or early September in any case, but they’ll have a deal done well before that. It might cause some turmoil in the market, which you guys can talk about trading. It probably setting up stimulus or economic deal coming in September or October of this year.

Tony

Okay, so there’s a lot there. So I want to ask we can talk about the White House and we can talk about Capitol Hill, but Yellen is a key player here. And depending on the day, either the treasury finds money we found $10 billion that we didn’t know we had or it’s super urgent and they don’t know where they’re going to get the money. Depending on the news flow and the day and the time of week and how negotiations are going, that sort of thing, how do you think Yellen will play this, and why does she continue to come with messages that differ by the day or every other day?

Albert

Well, I mean, things are fluid both economically and politically at the moment. They want a scapegoat for a little bit of market turmoil because of political PR narratives that they need to push out for the election. So Yellen wants the market to sell off a little bit and have the Republicans take blame for it so she can get a better debt ceiling deal done and a stimulus bill or an economic package in the fall. She wants to recharge her TGA account and use it at will.

Adem

Right.

Tony

Now, California also had a three month delay on their income taxes for whatever reason, cold winter or something like that. So that money will start coming into the treasury in mid June, right. Or should be in the treasury by mid June. So could that potentially be a reason for the Republicans to drag their feet knowing that more money will be in the treasury in mid June?

Albert

Well, listen, I wouldn’t give the Republicans or anyone in Congress that sort of competence when it comes to those things. I mean, I’m seriously, like, I talked to a lot of them, and it’s mostly deer and headlights when you start bringing this subject up. Disbelief in deer and headlights. This is really reserved for the financial guys that see what the political side is doing.

Tony

So do the financial guys know what they’re doing?

Albert

I mean, a certain upper echelon certainly does. The guys throwing out zero day trade, zero day equity call options to rally the market, they sure know what goes on.

Tony

Right, okay. And then you talked about stimulus package in kind of late Q Three or early Q four. What do you have in mind there? Why would that happen?

Albert

It’s election season. They got to pay off the voters mainly. I mean, I say this all the time, and I’ve given this free advice to people. Look at corn and wheat and farmers in the election time when Senate when the Senate has a lot of races going up, that they always give them a big deal in 2020. Was it they gave them huge ethanol waivers to boost corn prices, pay off for voters.

Tony

Okay. Potentially. And tell me if I’m wrong here. Okay.

Adem

So.

Tony

The debt ceiling plays out. The Fed raises another one or two times, people get freaked out about a potential recession. We do see growth slow in Q Two, q two and Q Three. And so there’s such a feeling that we may have some recession or that certain sectors are hurting. So then that justifies some sort of rescue package. Is that generally what you’re thinking?

Albert

Pretty much. That’s the political script I’m going off.

Tony

Okay. Wow. Okay. So we could see Volatility over the next month or so, but then I guess going into August, September, as this stuff starts being talked about, no politician will vote down a package like that in election season. Right? Of course. Not likely to go through. Okay. Adam, can you talk to us a little bit on the tactical side? How are you looking at the debt ceiling as a potential trade? What are you keeping in mind and what are you looking at in terms of trading the debt ceiling?

Adem

Yeah, so I actually was writing about this yesterday. I think the debt ceiling negotiations right now happening, are happening at probably one of the worst times, because when the debt ceiling lifts and the TGA refills, let’s say they refill it by 500 billion, that’s a transfer of bank reserves from the primary banks to the TGA. So you’re essentially draining their reserves. And then over time, these primary banks who are pretty much forced to buy the Treasury’s bonds, they sell them out to foreign entities, institutions, whoever else wants the bonds. Because you don’t just sell 500 billion right off the bat. Right. I mean, the liquidity would be crazy. So they do it, like, slowly. Well, the problem to me that’s interesting is, one, the TJS, they’re expecting, the Treasury Department and some estimates shows they’re probably going to have to raise the debt ceiling by about a trillion dollars by the year end. It’s a big cash grab. They said about 550,000,000,000 in this debt ceiling raise alone. Problem is bank reserves, while still elevated compared to pre COVID, they’re down 25, 23, 25% over the last year. They’re down about a trillion dollars already because of the deposit flight into money market funds.

Adem

Fed’s quantitative tightening. Then on the other side you have global liquidity has plunged over the last year, mainly on the back of the G Seven tightening, doing their own tightening programs. I don’t know, it reminds me of so in 2019. Remember the September squeeze? The treasury had issued a lot of deadly suspended debt ceiling and then you had corporations do early tax filing. Bank reserves were down to like 1.5 trillion back then. And then the repo rate blew through the roof and the Fed lost control, essentially had to essentially restart QE and keep the repo market open indefinitely. So I don’t know if that’ll happen today. It could be nothing. But I find it interesting. I was reading a paper by the Fed and they’ve admitted that’s why they do QT so slowly monthly and they build it up because they don’t actually know what the right amount of reserves should be for stability. They’re like, it could be 1.5 trillion, it could be 3 trillion. They don’t actually know until in hindsight. So I don’t know, it could be nothing. But I do think they’re going to be doing the treasury is going to be doing a huge cash grab at a time where liquidity and bank stress, especially we’ve already had three of the largest US bank failures, credit Suisse went under.

Adem

So liquidity is not looking great and they’re about to just suck a lot of more liquidity out while the Fed is also doing their QT, rolling up bonds. So on the trade side, I would say it’s probably going to create some fragility in the system. I like the longer end of the curve. I just think that the inverted yield curve right now is just not sustainable. It’s killing banks funding costs, it’s causing deposit flight. With the Fed’s overnight, the overnight reverse repo is still above 2.3 trillion, which is what’s interesting because bank reserves have been leaving, but money market funds and the overnight reverse repo hasn’t dropped below 2 trillion. So it’s showing that the QT, which was supposed to take away from money market funds and overnight reverse repo, it’s actually just taken away from bank reserves. So I assume that the treasury will be the same thing when they do the cash grab. It’s just going to pull out reserves instead of cash. Overnight cash. For anyone who doesn’t know, the overnight reverse repo is a place where banks and institutions park money, like idle money or that’s something they need to invest in short term, high quality assets, basically treasury bills.

Adem

So they’re borrowing the bill from the Fed and then they’re collecting yields, selling it back at a little bit of a higher price because there’s a dearth of bills. So I don’t know. I mean, the short end might go up when they raise the debt ceiling because of the new supply, but I think the long end is going to just keep going down. I just think growth anemic the consumers tapped out, student loans coming back online one way or another. Mortgage forbearances are ending. I think they’re just starting to end. And household debt is already at 17.5 trillion. Banks are tightening loan demands down like every the last quarter. So in a credit based economy, it’s hard to see any momentum.

Albert

Go ahead. All reasons for an economic package in the fall.

Tony

Yeah, it sounds like it. And we talked about a credit crunch a couple of weeks ago on the week ahead and it sounds like a lot of that is headed our way. Probably late summer, right? I mean, we’ve already got it in the making, right?

Adem

Yeah. I was like arguing with people on a Twitter space in December. I was like, yeah, I think the Feds are going to be done by halfway through summer. Because the higher you keep the rates, even if they pause here, the unrealized losses on the bank balance sheets don’t go away or their NIMS are going to keep getting crushed. Because now you have money flooding out into money market funds. So you have to raise the short term deposit rates. Like I was looking at ally Banks quarters recently. Their NIMS are down, their profit guidance was down and they raised the cost for basically subprime auto loans, which basically the B’s through ease rating on the subprime ratings, it went up like 700 plus bips over the last year. It’s hard to see the consumers at this point who are pretty much getting tapped out. And you can’t refinance a car, you have to roll it into a new car. I fail to see what the momentum will be going forward without any kind of government cut. I mean, the only way that the Fed can fix the banking thing is by cutting interest rates, letting their assets appreciate, take pressure off the unrealized loss, let their share prices go back up so they can do some equity capital raises.

Adem

I mean, otherwise they’re just going to dilute themselves out here. Yeah, I don’t know if you guys have any different view all over again. Yeah. And on the credit crunch, actually, we already know US. Banks have tightened dramatically, especially commercial real estate. Commercial real estate? That’s not an if, it’s a when at this point.

Tony

Oh, yeah, we talked about that four weeks ago on the weekend ahead. We are on stuff.

Adem

Yeah. Yeah. You guys did a great job. I mean that thing, it’s a ticking time bomb. Not to mention there’s 125,000,000 sqft still under construction right now and there was another 200 million planned, but we can assume those will be cut. But the thing that’s really interesting to me is if you look at Europe, so they do their own bank lending like surveys and the recent moment, the ECB sorry, my cat jumped in my lap.

Tony

All right.

Albert

I got two of them. Trust me, they’re all right.

Adem

Yeah.

Albert

They just know not to go on my lap.

Adem

I’m sorry. The bank lending survey for Europe, it was terrible. I mean, it was absolutely terrible. The banks were tightening, but the loan demand, especially in the property market, the enterprise market, the consumer market, all of them, is down 80% in the property market. And it was one of them. I mean, they did it on the top four. Spain, France, Italy, Germany. And it’s just if you have no credit, right, credit drives consumption at this point. If you have negative or flat real wages, which technically the US real wage has barely budged in 40 years, you have to subsidize to achieve credit. That’s the only way you can get the consumer or the spending. If the house is too expensive or the car is too expensive and your wages can’t justify it, credit makes up the difference. And I just think credit, I mean, we learned from Jaime Minsky, right? Private debt can’t go up forever, and I think we’re starting to see that at this point now.

Tony

And it’s painful when we hit that. Very painful.

Adem

It’s a big deleveraging cycle. I mean, look at Japan, europe, 1929, after 2008, after every time you have a deleveraging cycle, it’s pretty painful. And I think that’s what to them, the Fed, that’s the plague scenario for the Fed, right? You can’t have any deflation. Yeah. So they’re going to probably do big stimuluses. I don’t think they’re done. I think COVID was like the new playbook.

Tony

Yeah. I spent a lot of time in Japan through that deleveraging cycle and would go there probably every couple of months. And I don’t really think people, especially in the US, understand what that’s like, to be pretty stagnant for decades. And I think if that’s what happens here, it’s going to be a shock to many, many people.

Adem

Yeah, I agree. Japan, what’s interesting is, if you look at, like, Japan and Germany, South Korea, China, and I know we’re going to talk about China, they all run these massive current account surpluses. They have no demand in their own economies. They have to export that rest to get their growth. Otherwise you’re going to have unemployment and deflation because you’re going to demographic nightmares.

Tony

Right.

Adem

Demographics on top. Japan has like a 30% net savings rate. China’s is like, what, over 40? Germany 30. Saudi Arabia 30. If you’re not consuming, you’re saving. Right? And I think America is low in the UK, too, have very low personal savings rate. And it’s like, well, yeah, because they’re buying everything. They’re absorbing all these countries Gluts, right?

Tony

And the retail investors save because where are they going to get return, right? So they just got in the habit of not getting a lot of return for a couple of decades and. That’s a hard habit to break. It’s a very hard habit to break.

CI Futures is our subscription platform for global markets and economics. We forecast hundreds of assets across currencies, commodities, equity indices and economics. We have new forecasts for currencies, commodities and equity indices. Every Monday morning, we do new economics forecasts for 50 countries once a month. Within CI Futures, we show you our error rates. So every forecast every month, we give you the one and three month error rates for our previous forecast. We also show you the top correlations and allow you to download charts and date. You can find out more or get a demo on completeintel.com. Thank you.

Okay, since you brought it up, Adam, let’s move to China. Okay, you had some really good charts on China that you published earlier this week around structural issues in China. And I want to look at the soft. We’ll say that kindly, kind of the soft opening that China had.

Tony

I don’t know that the word soft really fully captures it. So can you walk us through kind of these charts and why China’s reopening has been so weak so far?

Adem

Yeah. For context for anyone. Yeah. Basically, China was under COVID lockdowns. They reopened all the mainstream pundits. Everybody was saying it was going to be like unleash inflation across the world, and it was going to be like this huge thing. But I remember I just thought, like, since 2018, China has been deleveraging. If you look at their household debt to GDP, it’s been flat. And it’s almost as high as the US is actually. Their governments are pretty much tapped out. They’re in debt up to their neck. The BRI, the Silk Road, basically initiative, brick, whatever it was when they were their loans are defaulting like crazy. Yeah, Bellen Road. Thank you. I’ve heard, like, multiple names for that thing. But yeah, I mean, they have they’re dealing with defaults from these countries. And I see a lot of people, they’re like, oh, doesn’t China want to get their properties? And I’m like, well, but they defaulted for a reason. None of these infrastructure projects generate profit. They don’t generate returns. So you’re just transferring it from one country. Now China has to deal with it. I just think China’s consumer is very anemic. I mean, their current account surplus.

Adem

So for anyone who doesn’t know, a current account surplus basically, is when you export capital and goods relative to import. So the US. Is a big deficit nation. China is a big surplus current account surplus nation. But it also means weak consumer demand, because if you’re not importing and you’re exporting the rest, that means that you can’t fulfill your own demand at home. Like we just talked about, Europe, Germany, especially Japan, South Korea, all these countries have massive, chronic current account surpluses because they have no demand economy. They don’t have purchasing power for their consumer, so they find it abroad.

Tony

One of the other things that I’m sorry, just to interrupt you, that I think it’s really hard for people in the west to understand is there is huge savings in Asia, particularly because those economies historically have been very volatile. And credit is credit. There is implied trust in credit when you take out credit. And so Americans particularly are used to a very stable market, which is why we’re so levered up, because we trust the market to be pretty stable, right. In Asia, those markets have been so volatile for so long that you look at what is the crisis of this five years in, say, South Korea, right, going back 20 years, the LG crisis, all this stuff. There’s always something going on, right? And so this is part of the reason savings is so high. Of course they’re net surplus countries, but they also don’t really trust their policymakers and they don’t really trust their markets. So they always have to have something in the mattress to make sure that they can make ends meet when the next crisis comes.

Adem

Yeah, that’s actually a really good point because Michael Pettis wrote a really good book called The Great Rebalancing and recently, Trade Wars or Class Wars. But he basically was saying that these countries, like you were just saying, they have to have a high net saving. The government effectively steals productivity from its consumers, and it has no social safety nets. Like, in America, you have like, what, the 30 year fixed mortgage? You have Social Security, right? You have unemployment insurance. You have all these things that just always promote consumption. Like, they’re always there to just keep liquidity going. But in China, they don’t do any of those things. A lot of these countries don’t. So they depend on having a higher personal savings. But it’s also more insidious because the governments, like in China, the state owned enterprises, they take the money that the individuals are saving because they have a closed capital account. It’s not like America’s banking system. So they depend on their people. They force them to kind of save, meaning they’ve repressed their consumption so they save more, and then they use that money to fund infrastructure projects for the SOEs they’ve been doing it, though, for 20 years.

Adem

And that’s the kind of thing we’ve been hearing about China. Like, oh, China is going to take over the world. They’re going to grow, they’re going to become a demand driven economy. But we saw with Japan after their crisis in 91, they tried that. That’s actually what blew their economy up. They had trade tensions with America. They were running chronic current account surpluses. Their demographics started looking shady. They had asset bubbles, especially in property eerily similar to China today. And then America did the Plaza Accord. They basically said, hey, you and Germany, you guys are running mass chronic account surpluses, meaning we’re absorbing it. We’re running the deficits here, and you’re pricing out US. Manufacturing. You need to let your currencies appreciate. You need to allow more imports and less exports.

Tony

The end was, I think, at 220 or something then, or 240. I can’t remember the number.

Adem

Yeah, it had like a 40% appreciation between 86 after the Plaza Court and 91. And in the same time they started importing, their exports to GDP dropped, but it popped their asset bubble. And two, their household debt to GDP, because when you have a stronger currency, you’re promoting more imports. Their household debt to GDP went from like 52% to 70 in five years. It’s insane. So China, I just see these countries, and they don’t want to have their currency appreciate. They don’t want an open capital account.

Tony

Look at China this week. They devalued to over seven. Yeah.

Adem

Seven. Yeah, they went back to seven. To put it in context, I always see people say, like, oh, the BRICS currencies. But the US has run massive fiscal deficits. Huge. Right. 31 trillion in debt, massive bet easing, $9 trillion balance sheet, whatever, 89 trillion. But the DXY, the US dollar relative to foreign currencies is up 30% in that same time period. Meanwhile, China, which has run massive current account surpluses, which is supposed to be good because of the inflows, their currency, is actually down since in the same period, it’s been like flat. If you look at every bricks currency, they all run chronic current account surpluses. Brazil didn’t, but now it does. It’s actually becoming a huge one. All their currencies, they’re down dramatically since 2008. So it just shows you that these people, they don’t have the consumer to have the imports, and they want to promote the exports at all cost. And they do it by China. They maintain their currency. They keep it cheap on purpose. Cheaper on purpose. It’s like a currency mechanism.

Tony

Yeah. To goose their exports. Right. They need a little bit more exports. They see the value added manufacturing moving away to, say, Vietnam or Thailand or Malaysia or Mexico or something like that. And so you can still get really good basic stuff in China, but the value added stuff is going to be somewhere else because labor isn’t as cheap as it once was. Right.

Adem

And that was with those three charts I was talking about. But I want to hear if Albert had any insight on this or anything.

Tony

Yeah. Albert, what’s your thought on China?

Albert

Everything you said was absolutely correct. From China cash economy to the dollar and how it works in the world. There’s not really much, to be honest, that I could really add. I mean, the only thing I can add is I know that China had staggered their reopening on purpose to help out on inflation and with yelling. And domestically, they’re not stupid. They know the problems that they have. They know the problems that they face and what they could face repeating what Japan had made mistakes in the future. They’re not dumb but I don’t really like when people make assumptions where China is like, oh, China’s peaked and it’s just going to be the end of China and so on and so forth. Let’s just take a step back here because China still can stimulate their economy on a short term basis to the moon. What happens is long term is a different story, but it’s short term. They can do whatever they want. They’re just pragmatic and they’re not going to do something silly like that. Everything you said I agree with everything about it, especially the dollar stuff. It’s like everyone wants to dismiss the fundamental details of economies and their currencies and just say, oh, well, it’s going to happen because of political A, B, and C.

Albert

It’s just not the case.

Tony

And as you said, the Chinese bureaucrats and policymakers, they are not stupid. They’re actually very smart. But within the bureaucracy, there are just things that they can’t mention. There are policy directions they’re not allowed to go, all sorts of things. So we sit on this side of it going, why aren’t they doing X? Why aren’t they doing y don’t they know it’s because they can’t even mention these things or their career is over.

Albert

Yeah, they have a different dynamic. We can have congressional members say all sorts of stupid things like Bernie Sanders does all day long, right. Or whatever Republican you want to throw out there. Also, they just say dumb things all day long. Right. You cannot do that in China. There’s political repercussions. You will end up in jail if you do. You mentioned some things, right?

Tony

While we’re here, I want to ask you guys about this with China. We had this for a couple of years. We had this kind of China wolf warrior diplomacy, right, where they were very aggressive, diplomatically. They would say really abrupt things and China was the ascendant power and they really needed to assert themselves in diplomatic circles. Right before the COVID reopening, they switched on a dime and they became much more accommodative, much more collaborative. There are still moments of wolf warrior statements, but for the most part they’ve become much more, I guess, softer than they did than they were before. What are your thoughts on that in terms of kind of the political economy, I guess? How does that reflect China’s view of its economy? Albert that’s a good question, Tony.

Albert

Put me on the spot on that one. I mean, a lot of China’s rhetoric and political economics is twofold, in my opinion. One, to stabilize their domestic economy for whatever sectors they’re targeting, but also has aspect of how they’re going to be dealing with trade negotiations going forward with the European Union, in my view. So they do a balancing act of what rhetoric they can throw out there.

Tony

Yes, I think that’s right. Adam, what do you think about that?

Adem

Yeah, I agree. I think the Chinese government, they must know that they’re kind of in a little bit stuck right now. And I agree with Albert. They could, if they wanted to come out and say, hey, you know what, we’re going to completely rebalance our economy. We’re going to be demand driven here’s. Massive vouchers, massive subsidies, open the capital account, let the wand appreciate, go out and spend, import, blah, blah, blah. But yeah, they don’t want to do that. They’re doubling down on the supply side. We’ve seen I mean, look at, we were talking about EVs earlier. Look at China’s auto to exports to GDP. It already took over Germany. It’s about to surpass Japan in just the last three years. I mean, they really are subsidizing the export sector. And I think it’s a problem because if the rest of the world can’t absorb it, like we saw with Vietnam recently, they laid off 6000 workers. Vietnam is one of the largest textile countries producers, exporters. They laid off 6000 factory workers because they said demand is drying up for Nike and shoes abroad. And it just makes it interesting because they can’t consume that stuff at home.

Adem

They don’t have the purchasing power to buy Nike in their own country. So they depend on the exports. So now they have to deal with unemployment. And I just think China’s worried about that because you’ve got official youth unemployment.

Tony

Of over 20% official youth youth.

Adem

And the problem with the youth one is that I was reading there’s another 11 million Chinese graduating college this end of May or in this cycle. So you already have 20.4% youth unemployment and now you have a tidal wave of new graduates coming in. Yeah, it’s just a problem. I just think it just shows there’s a lot of mismatches in the Chinese economy. And I was actually looking at data from Kaikeson Cakes in Global and they were showing how the state owned enterprises wages growth has far outpaced the private sector’s wage growth in China. And it just shows they’re both sinking. Right? I mean, wages aren’t rising in that country over the years they have, but the growth of that wage increase isn’t going up that much at this point. They have a negative CPI, so they’re having deflation basically at this point, their PPI, their producer inflation, which is like wholesale prices, which is important for China because China is an export economy. So they’re essentially exporting that deflation that’s been negative over the last year and even in month over month terms. So yeah, I don’t know, I think that their leaders are aware of it because the CCP has like a social contract with people, right?

Adem

It’s like, hey, we’ll give you jobs, we’ll take care of you, security, and you keep us in power, we’ll take.

Tony

Care of you or we’ll kill a few million of you.

Adem

Yeah, it’s worth watching, right? China has always been really sensitive about civil unrest because I think if I remember China’s throughout history, each time their empires kind of fell. It was because of internal, like, strife, as most do. Yes, most do. And I think that when you have an economy or not economy that too. But a population that large, you really got to be careful. Half of them get the pitchforks out or something. It’s quite a lot.

Tony

So, Adam, you mentioned a really important phrase, and I wonder if it could be helpful for the world economy. You talked about China exporting deflation. Okay. So typically you export deflation when you overproduce something. And so could China exporting deflation help us get over the inflationary hump in the world economy right now?

Adem

Oh, absolutely.

Tony

Accelerate us getting over that hump.

Adem

Yeah, that was like my thesis back in December when everyone said China was going to unleash inflation. I was like, no, because their domestic economy is weak. I think even with the Reopening, they were going to have deflation on the CPI side six months later. That’s what happened. And then on the producer side, you had their supply chains reopen, not to mention internal demand week. And since their exports, I mean, their current account surplus in the first quarter, 2023, it was the highest ever in the same period. You would have thought that they would have seen soaring imports right, from reopening, but they haven’t had it. Their consumers, just anemic whatever the reason is, probably because of property prices, or like you guys said, they’re skittish. They’re wanting to save the money at this point. But if you’re saving, you’re not consuming. And the Chinese banks, the Chinese economy, you have to export that capital. You have to find some use for it because it can’t just sit in there. You owe interest on the deposits, right. So you need to make an asset to be able to pay it. Otherwise you’re losing money. And I think that’s why we’ve seen them very happily start buying US.

Adem

Bonds again. Same with Japan. I just don’t see how that trend will change. And which with them exporting the capital to America, I do think it’s going to push weight down on the long end of the curve, which is also somewhat deflationary in the long run. And also, like you said, with their manufacturing capacity, you said they’re overproducing compared to what they make. And perfect examples, cars like EVs. They’re just dumping EVs and autos, like.

Tony

All over all across Southeast Asia.

Adem

Yeah, and this is the problem. I was talking with someone, they’re like, oh, but the production side, it’s good, they’re importing stuff. And I’m like, yeah, but there’s always like another side of the coin. Right? And I don’t think Southeast Asia, Russia, especially now, they’re even getting nervous about it. You’re crowding out their manufacturing capacity. Right. Like, how do you compete when you’re subsidizing the hell out of your manufacturing export sectors, and then it’s flooding into these economies, and it’s pricing their own manufacturing out. And the ASEAN, the Southeast Asian economies in Russia, they’re all big exporters, too, so it’s hard to see them not doing some kind of trade barriers or then they’re going to start subsidizing their own manufacturing.

Tony

Well, that’s it.

Adem

That is it. And the problem is, though, you can’t and that’s why I don’t like the bricks argument, because if they’re all dependent on exports, they all run current account surpluses. Problem is, you can’t all run a surplus together at the same time. Right. Someone has to have a deficit. Yeah.

Tony

This is also where when people say China and Mexico are going to partner up on value chains or whatever, those guys are competitors. Those guys aren’t partners. Those guys are competitors.

Albert

Yeah, we’ve mentioned this so many times, especially the arguments that I’ve had where nation state interests take precedence over anything else. And you will see trade barriers pop up. Like Adam says, you will see trade wars happen in the next decade. It’s just the reality of it. As nations contract, they need to shore up their own domestic economy and domestic workers. And this is what you’ll happen.

Tony

Yeah, it’s the next wave of populism. It’s just survivalism, and that manifests itself in populism. Okay, guys, just real quick before we close up, what are we looking for in the next week or so? I mean, I know the debt ceiling, but say, Albert, you’re watching the debt ceiling. What else are you watching?

Albert

Oh, man, I was all about debt ceiling.

Tony

No, you can go into that, too.

Albert

Obviously, debt ceiling narratives are going to come out. They’re going to be up and down all week long. The only other things that I’d be watching is actually oil, to see what’s going on with oil at the moment. Because the debt ceiling narratives give a recessionary outlook or a bullish outlook, depending on what side you’re on. And oil is going topsy turvy. I honestly think at $65 of oil is probably the floor because under that, production issues come across. So I would love to see it at 68, 67. So I can go long, but I’m going to be watching oil because I also have a thesis of a secondary inflation event coming in the second half or late this year, early next year.

Tony

Great. Okay, Adam, what are you looking at with the next week?

Adem

Next week? I don’t think any big things I’m looking at over the next week, but things I am going to pay attention to. I think China’s retail sales and their current account data monthly. Japan’s as well. And Germany. Those are the three I like to follow globally. But I also think with the debt ceiling in the market right now, I think I was looking like tech has really bit up recently that trade has gotten really crowded. Yeah, US. Tech and then you have short regional banks has also become very crowded. And it’s hard because I don’t mind shorting tech. I don’t have anything right now. Into it, but like, Nvidia and these things, I mean, I think they’ve just gotten way out of control with the AI Hype.

Albert

With tech. Good luck. If the debt ceiling thing gets done, I’ll tell you.

Adem

No, I agree. And then the regional bank thing I do like as a contrarian that it’s so shorted and crowded. Same with bonds. The ten year bond right now is like near record shorts. So I like the longer end of the curve. I think yields are going to keep going lower. I just think there’s an incredible savings glut in the world overnight reverse. There’s just so much damn money deposits they pumped in. And now that the banks are starting to curb back lend loans, you got to do something with it. And the government is the last borrower at that point, right? That’s the idea. If businesses aren’t investing, if the consumer is tapped out, then the government steps in to borrow, and I think that’s what they’re going to keep doing, but it’s going to drain reserves. So I think even though regionals are extremely shorted at this point, I think looking at a few, I do think banks are going to have more trouble throughout the rest of the year.

Tony

Okay, very interesting, guys. Thank you so much. This has been huge. This has been such a great episode. So thank you very much. Have a great weekend. Have a great weekend. Thank you so much.

Adem

Thanks, everyone. I really appreciate it.