Access AI-powered markets forecasts for free with CI Markets Free. Sign up here: https://completeintel.com/markets

Welcome to the latest episode of “The Week Ahead” with your host, Tony Nash! We’ve assembled a stellar lineup featuring Tavi Costa, Albert Marko, and Tracy Shuchart.

📈 Tavi on The Fed, Inflation, and Geopolitics: Tavi takes the lead, unraveling the intricacies of the US stock market’s divergence from emerging markets. Get ready for a deep dive into the impact of inflation on earnings and a critical look at the Federal Reserve’s monetary policy. Tavi also shares insights on commodity prices, injecting a touch of sarcasm on the potential actions of the Fed.

💥 Albert on Iran’s Aggressive Moves: Albert steps up to discuss Iran’s recent bold actions, including attacks in Pakistan, Syria, and Iraq. Explore the motivations behind Iran’s sudden assertiveness and the potential outcomes of these strategic moves.

🌊 Tracy on Red Sea Issues: Tracy guides us through the complexities of Red Sea issues, examining the stability of crude prices and potential triggers for a spike. Dive into the impact on the shipping industry, including insurers’ adjustments and airfreight companies considering alternative routes.

Experience the power of AI in forecasting Markets. Subscribe to CI Markets Free: https://completeintel.com/markets

Transcript

Tony Nash

We’re joined by Tavi Kosta, Albert Marko and Tracy Shuchart. We’ve got a few key themes. The first, Tavi is going to talk to us about the Fed equity outlook in geopolitics. Albert’s going to talk to us about Iran. They’ve had some cross border skirmishes, and we’re trying to figure out if Iran is acting out. And then Tracy’s going to talk to us about the Red Sea. Why aren’t crude prices moving? What’s happening with freight supply chains and all that stuff?

Tony Nash

Before we get started, I want to let you know about a new free tier we have within CI Markets, our global market forecasting platform. We want to share the power of CI Markets with everyone. So we’ve made a few things for you. First, economics. We share all of our global economics forecasts for the top 50 economies. We also share our major currency forecasts as well as Nikkei 100 stocks. So you can get a look at what do our stock forecasts look like? There is no credit card required. You can just sign up on our website and get started right away. So check it out. CI Markets Free. Look at the link below and get started ASAP. Thank you.

Tony Nash

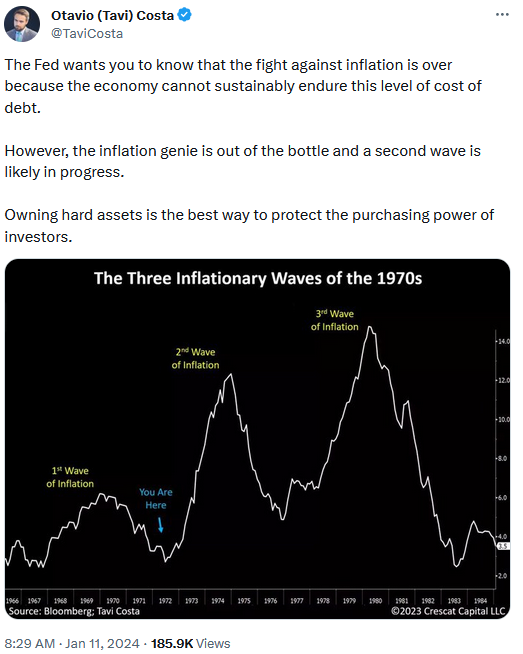

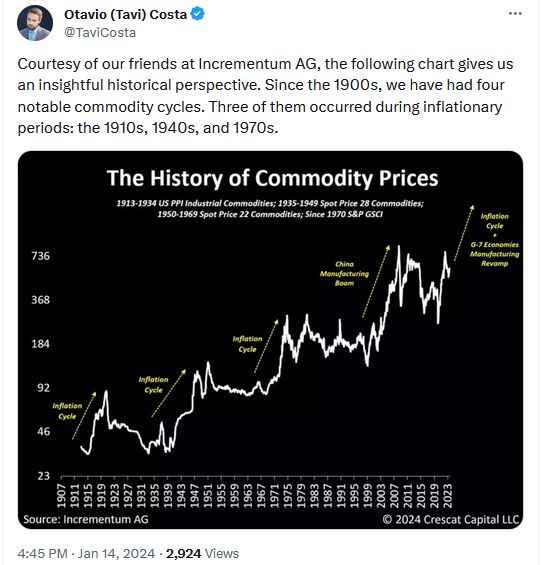

So, Tavi, thank you so much for joining us today. I know you’re in Brazil and it’s really not easy to coordinate schedules with you. So thanks again. Really appreciate this. I want to look at one of the tweets that you put out earlier this week looking at the Fed fighting inflation. And in this you talk about three inflationary waves of the 1970s. And I’d really like to kind of understand the context, kind of what do you think that means for the situation that we’re in now and how do we handle this going forward?

Tavi Kosta

Well, first, thanks for having me again. Well, I think there’s a lot of importance of analyzing what’s happening with inflation because of the behavior in markets that we may see unfolding due to those changes. It is of my view that 2021 and 2020 marked a significant change in the investment cycle. And I believe we’re now seeing structural forces in the inflation front that will mark the different regime in terms of cost of capital, in terms of cost of debt, in terms of even how we value assets. And so those structural forces to me are relevant. Number one is what we call the pillars of inflation. Those are, deglobalization comes first. I mean, that’s probably the most important one. I think a lot of analysts and Wall street in general is seeing some of those. Let’s see the Red Sea events and some others as kind of isolated events, and they’re not. I believe they are all interconnected in a big way. We’ve seen some of those big changes today in terms of even geopolitical problems relative to countries that we haven’t seen in decades now starting to become more problematic. That’s one of them. And we’re seeing the reshoring of developed economies and others that are causing the demand for commodities.

Tavi Kosta

And not only that, but also the reliance of the Chinese economy and other authoritarian regimes is being reduced in a big way. The second, I think, pillar of inflation has to do with what government developed economists have been doing, which is the reckless amount of fiscal spending. I mean, even if we look back in the 1970s, we certainly didn’t see this level of government spending and support that we’re seeing. And even if you exclude things like interest payments and other entitlement payments and so forth, there’s still a really significant portion of the spending that is very inflationary. Number three would be what’s happening as well with the labor markets. Labor markets for the first time that I can recall since the 70s probably, we’re seeing finally the cost of living being so high that it’s causing folks to actually demand higher wages and salaries. And that’s just something that evolves over time. And as we’ve seen, one aspect of this that there is room to grow is the fact that a lot of corporations are still paying their employees some of their lowest portions in terms of employee compensation relative to profits we’ve seen in history.

Tavi Kosta

And so there’s certainly room for not only protests and other issues heating up here that will become more and more widespread. And then I would point out to one thing that has been to me a main focus, which is the chronic under investments in natural resource industries that we, I think Tracy also covers that very well. And it’s related to the fact that supply of commodities and natural resources, those industries have been neglected for so many years now, if not decades. And that is creating a problem with especially the corporations and management of those firms being extremely conservative at not creating new projects and new developments of mines and other projects and other resources. That is creating also the limited supply of those things moving forward. And so if you ask me, I think this is the beginning of a hard assets environment where you want to be invested in resource rich economies and resource rich even companies that produce those assets over time too.

Tony Nash

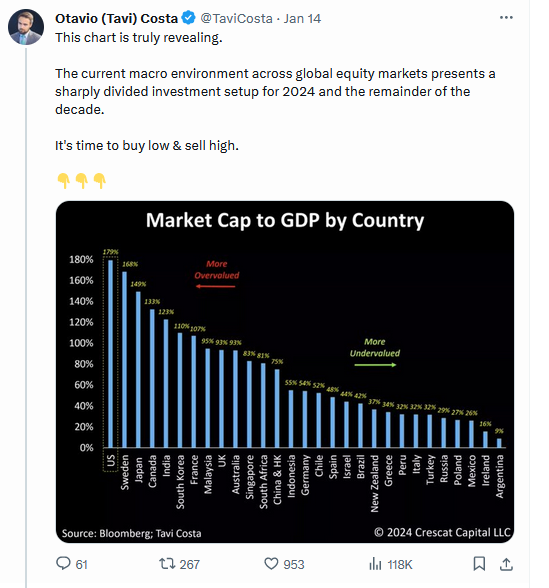

Okay, so there’s really a lot to pull apart there. But just looking at your last bit. So first of all, you really validated a lot of what Albert’s been saying for the past couple of years and a lot of what Tracy’s been saying for the past couple years. And what I’m hearing you say is the Fed may be saying that we’ve conquered inflation, but we actually haven’t. There’s more to come. So when you talk about investing in resource rich economies, you recently talked about us stock market valuations versus the rest of the world, especially emerging markets. So what are the factors behind the divergence in those markets? And what of those markets that are, say, underrepresented? What’s appealing about those markets?

Tavi Kosta

Well, first of all, I think there are some decades resource businesses are usually terrible companies, especially in the mining space where I, and most of those companies make no money. They’re very capital intensive and they’re highly dilutive. They burn a lot of capital. But there are some specific decades that are very interesting to own them, and they usually are linked to inflationary decades. So if you looked back in the 1910s, the all those three decades actually coincided with periods where inflation was running hotter than usual. And so, yes, you see the operational costs and other things rising at those periods, but the hard assets overall tend to really outperform even the cost structure, but also other assets like financial assets overall. And so that is one very important aspect. And the other thing has to do with why they have been neglected for so many years to not only. Well, they’re not really growth companies, and that has been one part of the market has probably attracted most of the capital we’ve seen in the last decade or so. Technology has been a big portion of. Well, and that has to do with, I think with the cost of debt being so cheap, allowing investors to not focus in bottom lines and profitability.

Tavi Kosta

I think somebody, maybe David Einhorn, made a point about we should measure how many, the frequency of analysts actually listening to earnings calls nowadays. I mean, you’ve probably seen, there’s a good chart of CFA level two people. The volume of those have been drastically declining. It’s just another way of seeing how fundamental analysis is just over. I mean, no one really does that. And I am of the view that we’re going to go back to that. We see decades that are like that and the same will go for mining. So why do I think those things look appealing? Because historically, when those companies start being extremely conservative, that’s the time you want to start getting exposure to it. And there are many ways you can measure that. My favorite one is looking to aggregate capex, and you can see that across not only the overall commodity space of producers, but also specifically in different parts of the commodity industries like agricultural commodities, energy, or you can look into the mining space and even break down into the metals as well. And what you’re going to find is that, yeah, overall, most of those companies have been extremely conservative, and it’s just hard to believe that that’s not going to drive the prices of things in general moving a lot higher.

Tavi Kosta

And I’ll point out to one more thing that I think is very relevant. I am of the view that gold is going to make new highs. And not only that, but we enter a new cycle and we can get into the reasons for that. But I’ve never seen a gold cycle that doesn’t coincide with a commodity cycle. And so to me that’s really what it comes down to. It’s just another way of betting on the idea that precious metals will enter a cycle. And if that happens, we’re probably going to see other commodities follow along.

Tony Nash

Okay, let’s talk about that, because I want to understand your gold thesis. Can you tell us why you think gold is going to run up?

Tavi Kosta

Well, I think there’s two pools of capital that really move the markets in general. There’s the 60 40 portfolios, the pension funds and all those kind of more idealistic investment strategies. And then you have the other side of it, which is central banks. And those are very relevant. And we have to understand where are those guys allocated and where they’re likely to move towards. So let’s separate the two. One of them is what is called the 60 40 portfolios. I mean, that has been the most successful way to be invested probably in the last 20 years or so and maybe 30 years. But now with this new investment cycle, I believe we’re entering where we’re seeing changes of correlations and so forth. I think we’re going to start favoring other assets. And to me this is the first time in 45 years that the downside volatility of gold versus treasuries is actually in a way where gold is less volatile than treasuries. And so I would think that those funds running those types of analysis will start favoring gold as at least a portion of that 40% of their portfolio in safe havens. And so it starts seeing that moving from zero to five to percent ten on the gold side.

Tavi Kosta

I think that would be a very significant and meaningful dynamic of flows into the space. The second one is central banks. Well, central banks, if you look at the history of them, the way you do it, at least the way I do it, is looking at their assets and the composition of their assets throughout history. And you can go back all the way to the 70s or even further, but what you find is that gold used to be a really big portion of their balance sheet assets in the past. And to be more specific, back in the late 70s, after the gold standard ended, we actually went to a period where central banks were accumulating gold, believe it or not, and their central bank assets actually peaked at the end of the beginning of the about 74% of their international reserves. So central banks have different priorities. They own things not because of a risk perspective. They own things because they want to create stability to their monetary systems. And so they need something credible. And so since then, treasuries and other sovereign institutions or sovereign instruments got really cheap, and so they accumulated those assets it makes sense.

Tavi Kosta

So on the back of that we had the success of six to 40 portfolios, the declining of interest rates, the improvement of growth stocks. And so everything is kind of linked to that significant change. And so now we’re starting to see the beginning of purchases of central banks. And you may say, wow, that’s pretty significant. Those are record amounts of purchases. But what is really significant is the fact that they are just 20% of their central bank assets today in gold allocation. So what if we go back to the median, which is about 40%, which is double from where we are today, and I think that’s very plausible. So coming from those two parts of the market, I would say that that can be a very important segment, or I should say attraction of capital to this industry. And not to go on a lot further, but there’s more to this. But I’ll keep it short.

Tony Nash

It’s a great overview. Just a quick question about gold and Albert and Tracy. I want to bring you guys in in a second, but I feel like there’s, on some level, at least from retail, there’s almost a substitutional factor between, say, gold and crypto. Crypto was kind of used as that counter dollar Deval asset. And now that we have crypto or say bitcoin spot funds coming out, that sort of thing, will that take away from the gold market as kind of a counter dollar deval, say asset for retail to hold? I know you were just talking about central banks, but I’m talking kind of that marginal, say retail or portfolio investor, will they see the crypto or bitcoin ETFs as a substitute to gold?

Tavi Kosta

Look, I think the reason for the gold being so unfavorable across the retail investors has been the fact that it just hasn’t performed very well. And a lot of people like to just ignore the metal because of that factor. When to me, as a contrarian, I love that factor. It’s exactly why I don’t go to a restaurant or a bar and I talk to a person and they’re telling me they’re buying claims of properties looking for gold and silver and copper. No, they talk about crypto assets and other things. And so to me, it’s a totally a contrarian opinion. I think there’s no marketing that is better than making money. And the fact that we haven’t made a lot of money in gold certainly is unfortunately a negative situation. And so do I think that will change? Yes, I do think that will change. I don’t think you’re going to get rich buying gold. I’m never going to say that. But I think there is a symmetry to buying assets that are linked to gold that are likely to be performing way better than the metal itself. That to me is what is very attractive about the space.

Tavi Kosta

And as we see people actually being successful and making every gold cycle, there’s a new period of new billionaires and successful investors that emerge. And I’m trying to be one of them. And that’s certainly my goal. And I think there’s a lot of other people creating credible vehicles that will do the same. And I think that that will attract the capital from the retail. You know, the fact that retail is not very interested to me is actually probably a positive factor instead. But

Tony Nash

Interesting.

Tavi Kosta

Yeah.

Tony Nash

Tracy, you follow precious metals and miners. What’s your thought on gold appreciation?

Tracy Shuchart

I think the bigger question here, just kind of jumping on to your question on the bitcoin gold thing. I think the bigger question here is do we think that these bitcoin ETFs are going to hurt or help the underlying asset? I think that’s a more interesting question than does the bitcoin trade hurt or help the gold trade, in my opinion.

Tony Nash

And I guess for me, a bigger question regarding related central banks is CBDC versus gold. Is that something that offsets the underlying value of gold? I mean, I don’t know how realistic that is for, say, the Fed, but obviously it’s a discussion point and I’m just not sure about it because I really don’t know. Albert, what are your thoughts on gold?

Albert Marko

What are my thoughts on gold? If we’re talking about trading it in a range between 1700 and 2300, I would absolutely agree.

Albert Marko

You should have it in your portfolio and diversify. Hoping that it goes to three, four, five, 6000 is just pure lunacy in my world, right. I’ve been told from treasury secretaries that they’re going to cap it at 3000. They’ll never let it because it affects the US dollar. When you’re sitting there trying to fight someone like the Fed or the treasury, especially in a commodity like gold, you’re never going to win.

Tony Nash

Right.

Albert Marko

But like I said, he’s right. Gold sitting there at 1718 1900. Why would you not have your portfolio allocated in an asset? Which is clear that for whatever reason the central banks are know buying gold for their portfolio, they’re clearly doing. It’s whether as Tavi was saying, or whether I believe, because it’s arbitrage for dollars in the long run. So doesn’t matter which argument you make, they’re certainly doing it right. So onto the other point about investing in commodity rich countries. Absolutely. We’re in a cycle where commodities are becoming much more hard to get. The supply chain disruptions are problematic. The only concern I have is when you start investing in those countries, you really have to look at the politics behind who’s leading those countries, because some of them are left leaning, some of them are right leaning. The left leaning countries tend to favor climate change and environmental policies that sometimes is contrary to mining and whatnot. So that’s the only tidbit I’d throw in there with that.

Tony Nash

Yeah, that was actually my next question to Tavi is if we look at that chart that he has on kind of the premiums across stock markets, the market value to GDP and more of those countries that you look on the right. My question is around geopolitical risk. How do you factor geopolitical risk into investing in these countries, not just those that have precious metal mining, but also the ones that are on the right that aren’t necessarily hit the valuations, that haven’t necessarily hit the valuations that are, say, a median valuation.

Tavi Kosta

Well, it’s an important question because the risk is not taking away of the trade at all. As we know, markets will prioritize different things at different times. And right now, certainly the risk of the political side has been, I think, the largest thing that has been causing this big difference in valuations of companies in the mining space specifically because I can speak a little better about that. Know, one thing that you can see today is the fact that if you buy, let’s just say a project and mining project in Peru versus in Canada, you’re going to pay a much higher premium in Canada. For obvious reasons. But the thing is, because of ESG issues and other things, for you to put that project into production in Canada will take you 15 years, while you can do that in Peru. Depending on the project, depending on the situation, you can maybe get that into production in three years. And so I’m not joking. I mean, we have a project in Bolivia now that is actually going to get into production hopefully in about three years. And government has been very supportive. Why? Because they know they need people to be employed, so they want the projects to go ahead.

Tavi Kosta

And so when do we start actually shifting the prioritization from markets, giving a premium to the political jurisdiction rather than maybe the speed of getting a project into production? I think that we’re going to see some of that shift. I personally think that that’s going to be an important one because I want to own more projects that will actually get into production in this cycle, not the next one. Because buying an exploration project, you only going to get into production in 15 years from now. So why even bother? So that to me is an important aspect.

Tony Nash

Interesting.

Albert Marko

That’s really difficult to do. I commend you on that one, especially trying to find something that’s going to be productive in the next two, three, four years. That’s tough.

Tavi Kosta

Yeah, it all depends on the idea, right. This project I’m talking about has infrastructure already ready to go. They spent over $2 billion in infrastructure and found a discovery. And the discovery now is the big discussion, can we get this discovery into production? And so you need permits, you need all sorts of things. You need to build some infrastructure there as well because it’s 40 km away. And if you’re trying to do that in Canada, boy, good luck. It’s going to take you a while to get those permits and approvals and you got to talk to the natives and all those things in Bolivia, you might be able to get there much quicker, especially if you don’t have to build a lot of infrastructure. So this is a very specific case that I’m talking about, but that certainly is one to consider. There are other projects like the ones we’re looking at that are in similar positions.

Tony Nash

Yeah, you have to be hyper aware of the politics on the ground in these cases. Right. So I don’t think we can underscore enough the importance of geopolitics, especially in the environment of higher interest rates. Right. When that cost of capital rises, the downside of geopolitical risk is much more painful. So let’s switch to us equities for a minute. Tavi, given where us stock valuations are. What’s your outlook on earnings? We saw massive earnings growth with inflation in 2021, especially in early 2022. As inflation grew, so did margins for companies because they could push stuff onto their customers. With inflation abating, where do you see earnings coming from? Are we at the point in the cycle where earnings growth comes from cost and staff cuts? Does that stuff become the focus?

Tavi Kosta

Boy, if that happens, I don’t know how the population will keep moving because the widespread labor strikes to me are a big portion of all this. And I’m going to start actually putting out some stats on this because I don’t think people are doing enough. The point of how much corporations are getting paid relative to how much the labor market is getting their share. And so that’s going to change. I think that’s going to create an even more inflationary problem. But to your question, look, I’m not of the view that we’re going to see a soft lending. I’ve been of the view. I’m not going to say. I think most of the managers that are writing 2022 that absolutely nailed 2022 had issues in 2023, and the same guys that nailed 2023 had a terrible 2022. And so who do you know that did well in 2022 and 2023? I mean, that’s very rare to see because most people fall into one of the two categories. They’re either inflationary or deflationary. And you can strapolate those moving forward. The deflationary likes technology and some other things, and the others like value stocks and commodities and other things like that, I’ve been of the view that this profusion of macro indicators suggesting that we’re going to see a recession will eventually happen.

Tavi Kosta

And when I say eventually, I think six months, twelve months is probably very plausible. I think it’s going to happen. And so if I’m of the view of that, and I don’t think there’s a lot of big themes in the short side that look attractive. I mean, the dominance of mega cap companies, is that something that will continue? I don’t think so. I highly doubt we’re going to see that this entire year. I think that that’s going to be fading. There are issues with companies maturing debt in 2024 and they have to reissue that debt, along with the government that has $8.2 trillion of debt, has to be reissued. What’s the resolution of all that? We all know the average interest rate right now is 3%, but interest rates itself is at what? I don’t know. Interest rates are below four. The majority of them are above four or 4%. So talking about that, it’s going to be a big change in interest payments and margins that will get squeezed. And then you extrapolate that in corporations it could be even worse. And so yield curve inversions, deeply inverted. Now steepening. Well, how many times have we seen that in the past?

Tavi Kosta

So I’m not the one who is going to bet against history. And maybe history is wrong and all these indicators are wrong and we don’t even see a lending, maybe we’re going to see actually a booming economy. And I’m completely off here, but I think there’s. Yeah.

Tony Nash

All of these things sound like headwinds for earnings. Do we see a return to earnings growth in 24 or do we see flat earnings for the next several quarters? Because I’m just not sure where that earnings growth comes from. Albert, what do you think on that?

Albert Marko

I don’t know why it matters. I mean, they’re using seven stocks to pump the market in bonds. What does it matter? I mean, I agree with them to a point. Things don’t look really that great historically. You’re looking at most likely a recession. I just don’t buy the recession talk for 2024 for only one reason, is there’s an election in the US for that reason alone, and they’re willing, and they’ve shown that they’re willing to pump money into the economy, into the markets. They’ve done it multiple times in the past. And from what Yellen’s actions are, I don’t see it stopping now. Twelve months from now, completely different story. That’s a completely different era. And the situation changes after that. But for the next six months.

Albert Marko

I think they’ll probably launch the market close to 5000 or 5300 or something stupid.

Tony Nash

Tavi, what do you think?

Tavi Kosta

Can I ask a question?

Tony Nash

Go ahead.

Tavi Kosta

I find an interesting point because I thought about that too. I mean, this is an election year and so forth, and the Fed to me was a total political shift. What happened recently, I can’t explain. Well, what exactly happened when inflation is where it is right now and anyways, and it’s decelerating and there’s no point there. But the year of 2000, the year 2008 was also, both of them were peak of the market in eight was a very terrible market. Both were election years. How do we put so much weight on the fact that it is an election year when history shows that actually there were some really brutal years during election?

Albert Marko

There’s a key difference, though. Back then, China and the Europeans were not complete zombies like they are today. They’re dead right now. So all that money, all the inflow coming into the US markets is helping, is helping the US stock exchange. There’s no question about that. Flies into bonds, it flies into the equities. It goes everywhere. There’s no one right now to hold us accountable of what misdeeds we’re doing. Back then, you could have said, okay, well, I’m going to take my 30% or 40% of my portfolio and put it into China, or I’m going to put it into the European economy. Can’t do that right now. That’s one of my main contentions is that part alone, it really stops any kind of argument. It’s like, okay, well, then where’s the money going to go at this point? Who’s going to stop the political actions of Janet Yellen from this point on?

Tony Nash

That’s fair. And if we look at Tavi’s chart from earlier, a lot of those European countries are relatively overvalued as well. Right? So if you want to stay relatively safe, do you want to put it in Europe? Well, it looks overvalued. Do you want to put it in Japan? Well, you have the currency risk and you have, according to Tavi’s chart, overvalued. Right.

Tony Nash

So I think it’s a good point.

Albert Marko

You also have a very politicized Fed and treasury at the moment. Obviously, like Michael Green was saying the other day, the treasury secretary is an appointee of the president and pushes aims. No question about that. But the other thing is, a lot of fed members were ousted last year for more liberal minded MMT in the frame of Lael Brainard’s MMT type economy. Right. So this is why I think that this is a new regime. They don’t care what happens in a year.

Albert Marko

They think they have full control, which I completely agree with Tabi, historically, you can see that that doesn’t really play out very well in the long run, but because of, there’s nowhere else for money to, right, And they have almost full control politically at the moment. I just can’t see them allowing a recession to happen only for political optics. Sure, the data can say this and that in a few sectors and whatnot, but they manipulate the BLS, they manipulate the CPI numbers. So for me, they can do whatever they want and they’ll make some kind of chart to make it look like we’re not in a recession, even though 90% of America is already in a recession as it is.

Tony Nash

Tavi, what do you think about that?

Tavi Kosta

Well, I think I’m happy to be wrong on the recession call if that means precious metals and other hard assets will do much better because the Fed and other institutions are stimulating the economy just because of elections. That would be good for copper, that would be good for zinc, that would be good for a lot of things.

Albert Marko

100% because they’ll lower the dollar to help the market up. If they lower the dollar, God knows what commodities are going to do.

Tony Nash

Yeah, and I think you guys are kind of saying the same thing. You’re saying you don’t expect a recession in 24 and you’re both saying maybe in twelve months this stuff happens. And I think at least we’re in.

Albert Marko

A different timing issue, whether it’s six months, twelve months, 18 months, that’s all it is because we’re on the same wavelength that commodities are the definite to play here.

Tavi Kosta

The beauty of starting the year, sorry to interrupt, but the beauty of starting the year is that you can see all these calls for 2024. And if you think about that chart, the very first chart that you’re referring to that shows the waves of inflation that I think it’s a critical chart to think about. One of the things that is overwhelmingly the consensus view right now is that inflation is over, that it will decelerate. Just look at the two year yields and what’s been happening with the rate cuts price in, in the markets right now. Most of those things, I think, reflect maybe some sort of recession play as well. But the recession thing, the thing is, the recession thing is from a sentiment standpoint, it’s not as attractive as the inflation reacceleration. The inflation reacceleration to me looks much more of a play because there’s room for that, for people to have that view. Right. It’s 100 people that have the opinion.

Albert Marko

Yeah, completely agree with that. That is much more better of a play than it is to play with recession, which is way more political right now. But the secondary inflation wave absolutely is a great play right now.

Tony Nash

Tracy, what do you see there in the secondary inflation?

Tracy Shuchart

Well, absolutely. I’ve been very vocal over the last month, actually starting in December, late December, that I thought this problem in the Red Sea was going to lead to a bigger disaster than everybody thought that it would. And it’s played out pretty much as I predicted. And I think that right now we’re not seeing these effects in the numbers yet as far as extra fuel consumption, extra insurance rates, extra.

Tracy Shuchart

Let’s not get into too much of Red Sea stuff now. I don’t want to spoil the third, but. So you’re saying Red Sea will be a driver of a secondary wave of inflation?

Tracy Shuchart

Absolutely. And I think that hasn’t shown up at the data yet, but it will a few months down the road. And this could be a very big problem, not only for the election, for the government, but also for central banks.

Tony Nash

Right.

Tavi Kosta

Tracy, can I ask two questions to you, if you don’t mind? Tony? Just I think critical here, and it’s not Red Sea related, but one of them is how much do you think is sustainable, this increase of energy, or should say oil production in the US specifically? And the second question is how much of a war premium is currently priced in, in oil prices today?

Tracy Shuchart

I think.

Tavi Kosta

Two different questions.

Tracy Shuchart

Well, I’ll do the easiest one first. There is no war of premium price in, well, prices right now. Nobody is expecting it. And that’s partly in the fact that we’re not seeing hooties lob missiles at Aramico facilities anymore. And so if that should happen, which I do not think it would happen, that obviously would be driver for oil prices to move higher. So I don’t think that geopolitical risk is factored into the market right now. The market’s pretty, being pretty relaxed about it because really no oil facilities end or no oil production has been hurt at this point, even though we are finally starting to see tankers avoid the Red Sea. But that’s kind of a new development. And then the first question was, what was the first question?

Tavi Kosta

Oil production in the US.

Tracy Shuchart

Absolutely. I think that oil production in the US, I think. Can you cut out that part until I say oil production in the US? Oil production in the US. Let me start over terrible today. And to answer to your first question, I think oil production in the US is set to slow. I think expectations are very high. I think that 2023 came as a surprise to most markets because even though we had declining ducks and we had declining rig counts, oil production continued to move higher. But what we are getting from the. So I think this is a two part thing. I think, one, what we’re getting from these wells is getting gassier and gassier. That means lighter and lighter. That means stock. That is really, you can only use for chemical production, petrochemicals and things of that nature. That’s what kind of, we’re kind of getting out. And what I think that we also saw is that with this wave of consolidation in the industry and we’re seeing all the big majors start to suck up all these smaller companies. What they’re doing is they’re sucking up production. So what we saw is these smaller companies try to produce as much as they can to look as attractive as they can for an acquisition, and as a result, we’re seeing some major big deals over the last year, and it’s expected to continue. That trend is expected to continue within 2024. And so that’s kind of what I mean by all these majors are not expected to grow production. None of them are saying we want to grow production in the US. They’re buying production growth, if that makes sense at all. I think that is part of the reason that oil production continued to rise in 2023, much to most people’s surprises, because we have these smaller companies really trying to produce as much as they possibly could to be attracted to these majors.

Tony Nash

Yeah, I mean, if these guys are disincentivized for doing capital investment, then of course they just have to buy the assets that are already developed. Right? The smaller assets. I mean, it’s a way of backing into it instead of doing it greenfield. As they’ve done in decades before. So in hindsight, it looks natural, but looking forward, it would have been kind of a hard thing to expect that thing.

Tracy Shuchart

Absolutely.

Tony Nash

I think. Okay, great. This has been fantastic, Tavi. I’m going to move on to some geopolitical issues with Albert.

Tony Nash

Hey, I’d like to make sure you know that you can access our AI driven market forecasting tool called CI Markets for free. No streams attached, and it does not require any credit card information. Go to completeintel.com/markets to subscribe. CI Markets is the perfect addition to your analysis toolbox. This free account includes Nikkei stocks, major currency pairs, and global economics. Of course, we offer much more in our paid account, but this lets you experience CI markets before making a financial commitment. CI Markets uses the power of AI to help you make better trading investment decisions. It’s absolutely free. Again, go to completeintel.com/markets to subscribe to CI Markets free.

Tony Nash

Albert, we saw on Tuesday, we saw that Iran launched some attacks against Pakistan.

Tony Nash

Pakistan retaliated midweek. Earlier in the week, Iran launched attacks against Syria and Iraq. So what’s happening here? Why is Iran suddenly acting so aggressively? And what outcome do they know?

Albert Marko

Honestly, it’s just theatrics, deception more than anything else. I mean, the Iranians didn’t actually attack Pakistan military installations themselves, right? And the Pakistanis also didn’t retaliate versus the IRGC directly themselves. They just threw some lobster missiles back and forth at some proxy militant organizations, nothing more. This is nothing more than hyping up the whole Houthi Red Sea issue to probably drive up oil prices at the be. There’s no threat of expanding regional war with the Pakistanis and the Iranians, which is absolutely absurd since both of them are within the sphere of influence of Moscow.

Tony Nash

And Beijing.

Albert Marko

Yeah, and Beijing to a lesser degree, though. I mean, the Beijing. Beijing is a trade partner, whereas the Soviets actually supply them with defense equipment and whatnot. Right. And advisors. And it’s a different dynamic. I would associate more influence on Moscow than I would in Beijing in this part of the. Yeah, you know, I don’t see much of anything coming of know.

Tony Nash

Zuran is kind of portrayed as kind of this puppet master in the Middle east of the Houthis and know, Syria and other places. Are they really?

Albert Marko

Well, yeah, they are. I mean, they supply arms, weapons, narcotics, trade through multiple areas of the world through the Middle east. And they fund a lot of the proxies and operations out of there. There’s no question that they’re definitely a player. Most of this is just testing the United States’ resolve, the west’s resolve in the region and to, you know, we’re don’t. To show the entire muslim world, hey, we’re know, don’t discount us. We’re not, you know, like I said, as some kind of grand scheme of undermining the entire west.

Tony Nash

I just don’t get it. I just don’t get kind of, especially this week’s tactical movements by Iran. Maybe it’s to prop up the oil price, but. I know this sounds kind of crazy, but would they coordinate that with Pakistan beforehand and say, hey, we’re going to take out these militants on your side and then you can take out these militants on our mean.

Albert Marko

Yeah, of course.

Tony Nash

In the west.

Albert Marko

You think they. Oh, yeah, of course. The IRGC and the ISI, I’m sure they have connections, you know, winking a nod. We’re going to throw missiles over here. Don’t be surprised. Yeah, we’ll respond with missiles over there. Don’t be surprised. Of course you’re going to have that communication. You’re not going to just do something surprise in the middle of the night because that can lead into a serious conflict.

Tony Nash

Okay, so there’s really nothing to see here.

Albert Marko

Not really.

Tony Nash

And we’ll get into the Red Sea in a minute. But that is really backed by Iran. That’s not really backed by Russia, is that.

Albert Marko

I mean, obviously, I’m sure the Russians would have some sort of notice about what’s going on over there, but realistically, it’s the IRGC of Iran that’s pushing the Houthis to do these sort of things. I mean, the Houthis get total funding from them, so they can’t just sit there and do something all willy-nilly without approval.

Tony Nash

Right. Okay, interesting. So that segues perfectly into Tracy’s red Sea segment, and both you guys jump in here as needed. But Tracy, you know, we’ve all seen what’s happening with the Red Sea and the Houthis and the US kind of bomb strikes and all this. You know, crude prices really haven’t budged since mid December. So why we saw European gas prices plummet this week. Why have they not budged? And what would make them spike at this point?

Tracy Shuchart

Well, I think as far, and I’ve been saying this for a week now, weeks now, this is a shipping and insurance issue. So if you were invested in container ships at the start of this, you did really well. They’re starting to back off now, but they spiked this. Oil prices did nothing. Natural gas prices did nothing. Globally, we’re oversupplied on LNG and natural gas. I don’t expect that to subside anytime soon. As far as a long term investment prospect, I think that some of these individual companies are attractive. But as far as actual futures markets, net gas is just not attractive right now. And then if we look at oil prices again, the Houthis aren’t lobbying missiles again at Aramco facilities as they once did. That spiked oil price at $7 in a day. Right. And tankers until the last week or so have been largely unaffected and have been able to traverse the Red Sea with no problem at all. And you have to understand, because Iran has ships traversing the Red Sea in oil products as well, the Saudis are staying out of this for the most part. They’re not getting involved, which means there’s not that tension between the Houthis and Saudis right now and the Emiratis. So there’s not that threat that they’re going to be lobbying this little city. So there’s oil facilities. And so I think that’s why oil has been largely ignoring this right now because there really hasn’t been a direct threat at this point.

Tony Nash

It’s really notable to me that the Saudis and the Emirates have been really quiet on this. I think it’s really fascinating, especially given that the Saudis and the Emirates were involved in Yemen for so long for over a, I mean, there’s a story, because there’s not a story there, there’s just something going on, right.

Tracy Shuchart

No, I agree, absolutely.

Albert Marko

Yeah, this is, this is what we’ve been saying, Tony. Listen, I’ll be the first one to throw up the flags, the red flags, and say, hey, there’s a real conflict happening right now. But I mean, the Saudis just completely dismissed it, right? They don’t want to get involved. The US is going to. I mean, they had to act because of the shipping lanes and whatnot. But nobody else is really taking this seriously. Listen, this was a serious problem. Oil would be at $95 right now without question. And because the market hasn’t moved on it, I don’t think anybody’s taking this seriously.

Tony Nash

Well, you’re not even seeing brentured or Dubai or any of those grades spike up.

Albert Marko

No.

Tony Nash

Nothing consumed in Europe, right?

Albert Marko

Nothing.

Tony Nash

No action in WTI. That’s not a surprise. But you’re not seeing spikes in brentured or any of the Dubai grades or anything like that. I mean, it just doesn’t really make that much sense to me given the geopolitical aspects.

Tracy Shuchart

I feel like. Can I just say, I think there’s.

Tony Nash

Absolutely. Yeah.

Tracy Shuchart

I think there’s probably some backdoor deal where the IRGC, Saudi Arabia, basically they said, you know what, we’re not going to hurt your tankers. Don’t worry about it. Everything’s going to be know. I think there’s some political backdoor deals and why. Perhaps we’ve seen the Saudis and the Emirates kind of quiet about it because I’m sure that there was a lot discussed regarding oil when this first happened and why it’s been mostly container ships again, I said up until this last week.

Tony Nash

Yeah, well, we did see that trip. I think it was the Iranian foreign minister to Riyadh about three or four weeks ago. So is a backdoor deal plausible? Yeah, it’s plausible. It’s definitely something that could be in the works or having been agreed already. Tracy, you mentioned insurers, and we saw insurers adjust Red Sea rates weeks ago, but we’re now seeing exclusions for us and UK vessels. What does that mean?

Tracy Shuchart

Well, you know, obviously that’s not good. They don’t want to touch us, UK vessels or anything. That’s going to Israel. That’s also going to be a very big problem for Israel, which is massively importing country. They don’t produce much except for some agricultural goods and some NatGas.

Tony Nash

But a lot of software.

Tracy Shuchart

Ans cyber security. That’s going to be a huge problem for Israel as far as getting good to their country. And it’s a very concerning problem for the US and the UK, which keep poking the bear know, I think that it just doesn’t look good. It’s not going to necessarily hurt the US because they can avoid the Red Sea. Merchant ships can avoid the Red Sea. That’s not really a look, it looks bad and it will be a problem for Israel getting goods to their country.

Tony Nash

Sure. Okay. So we’re also seeing air freight companies talking about goods potentially rerouting via air to avoid the Red Sea. And you tweeted about this earlier this week. So is that a real possibility or likelihood or is that just airline CEOs kind of pitching their business?

Tracy Shuchart

Well, this was DHL. There was a DHL thing. And really, I think they were really talking about their container ships. But if I were to speculate, depending on how long this lasts and how much insurance rates go up and how long these and how big these shortages actually get on container shipping rates, I think you’re going to see air cargo do extremely well because you’re going to start diverting what would be on sea onto air eventually. But that, again, we’re not at that point yet, but it’s something to be looking forward to as this kind of drags on. We saw Maersk come out this week and said this is going to be months instead of weeks. And so the longer this drags on, the higher the wait times, the more know, container shortages you’re going to see, which we’re particularly seeing in Asia right now, which is bad news for, you know, I would kind of start looking at air power.

Tony Nash

So this plays really well into Tavi’s chart about the three waves of inflation. Right. So, Tavi, we’ve got geopolitical risk, we have potential supply chain risk and other things. So how do events like this kind of accelerate the kind of worldview that you have around those three waves of inflation?

Tavi Kosta

Well, I think the three waves of inflation is really predicated. Again, it’s figuring out, or at least trying to identify are these forces, there’s always forces in the deflationary and inflationary side, and are they cyclical, structural? I would argue that they are certainly not what we saw in the, what we saw in the 40s. But majority of people, when I show that chart, they immediately say, well, this is not like the 1970s. And when you look back in the, we did see inflation developing through waves. In fact, I just haven’t showed this charts. But if you go to other economies, Germany, France and other Argentina, Turkey, and you look at their inflationary problems, they also develop through waves. And it’s just mathematical how things work. Things get really heat up and then on a year over year basis they decelerate. It doesn’t mean prices necessarily are contracting. They’re just accelerating the growth. And then you bottom at a certain level and you’re starting to see some signs of that. I still think CPI may fall a little more and I think it’s a total lagging indicator. You may see what’s the best way of trading this sort of my view, this overall potential for too much sentiment of further deceleration of inflation, and the problem is over.

Tavi Kosta

Well, it’s the fact that if you look at the commodity price, the equal weight of commodity prices, they’ve been on a range, trading on a range for about 18 months and they haven’t done much right, basically. They also haven’t done really bad either. They’ve been kind of going sideways for a while. And so what do I think it’s going to happen? Yeah, I think we’re going to retest the levels that we saw during that Russia invasion problem and probably going to go much higher than that at some point. And that’s what creates the second wave of inflation. So looking at the housing market is probably a huge factor here. I think there’s a reason why Warren Buffett owns home builders. I don’t blame him. I think there’s a total issue with housing inventories. Sorry, I got a notification on my phone. And I actually think that plays into the long term thesis of the inflation problem. I can’t imagine that building homes are not going to create a demand for commodities overall. The reshoring of economies won’t create demand for that. And this is all long term things that will at some point start driving the prices of those assets.

Tavi Kosta

And so knowing that the fact that the chronic issues in the commodity space have not been solved, I mean, access for capital is still the same situation. Over the last three years, especially in the mining space, things have been as distressed as they can be. Every company we own that is looking for capital now to raise, it’s all these difficulty of finding investors that are savvy enough that want to put capital into this. And so it’s really hard. And how do we build the next mines and the next supply of things in general? Well, we need capital and so all the capital is going into mega caps right now. Those things have to at some point translate into the markets. And I would think that the second wave of inflation could certainly happen this year. And I would say that it’s probably high conviction that we will.

Tony Nash

It’s just interesting to me that this started because of supply chain issues, a lack of supply, and then consumers have been conditioned to these higher rates.

Albert Marko

Well.

Tony Nash

This is higher.

Albert Marko

Well, this is the problem. Right. Tavi is right about pointing out the housing market. Right. It’s a political problem also because they need housing to be affordable and the only way to do that is to lower rates. Well, the moment you lower rates, you’re going to get next secondary inflation and the housing market go berserk. I guarantee you if they cut rates this year like half, like 50 basis points, that you’ll see housing market probably go up 15% to 20% immediately.

Tony Nash

Exactly right.

Tavi Kosta

And by the way, this is an issue I have with having such a bearish view overall, is because housing market is in a way an economy as well. So I’m not that bearish on the housing market personally. If you look back in the see the ratio of house prices versus the s and P, you’re going to find the house prices actually outperformed the s and p quite significantly during that decade. And if you go back to the was also the same thing. And the interesting aspect of this is, again, it’s a hard asset that outperforms a financial asset during an inflationary era. And do I think that could happen today? Yeah, I just don’t think that within the hard assets realm, housing looks very attractive relative to other things. But I wouldn’t bet against it. I think there’s better things to do.

Tony Nash

Interesting. Guys, thank you so much for this. I really appreciate your time. All that you’ve said today and have a great weekend and have a great week ahead. Thank you.

Albert Marko

Thanks, Tony.

Tavi Kosta

Thanks, Tony.