CI Markets Premium for only $25/mo: https://completeintel.com/markets

This Week Ahead discusses three key topics: Inflation & Growth, Jobs, and Housing with Adem Tumerkan, Albert Marko, and Leo Nelissen.

First, we explore Inflation & Growth, where Albert shares his thoughts on rising inflation and what it means for the economy. Adem also addresses concerns about GDP and GDI.

Next, Leo takes us through the Jobs market, touching on Challenger job cuts and the US JOLTS data, and what it implies for the Fed’s plans.

Finally, Adem talks about Housing, highlighting the ups and downs in the US housing market and the role of the Fed in these changes.

Key themes:

- Inflation & Growth

- Jobs

- Housing

This is the 78th episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

Albert: https://twitter.com/amlivemon

Leo: https://twitter.com/growth_value_

Adem: https://twitter.com/RadicalAdem

Transcript

Tony Nash

Hi everyone. Welcome to the week ahead. My name is Tony Nash. Today, we’re joined by Adam Tumerkan. We’re joined by Leo Nelson and Albert Marko. Guys, thanks so much for joining us. We’ve got some key themes we’re going into. They’re broad and simple, but I will go to a lot of depth on them. The first is inflation and growth. The second is jobs. And finally, we’ll dive into housing. I know we could talk for probably three hours on these issues, but we’re going to try to collapse it into probably 45 minutes.

Before we get started, I want to let you know that we’re extending our current promotion on CI Markets. That’s $25 a month for CI Markets. It’s $240 if you pay a year in advance, for 1,700 assets. That includes individual stocks in the Dow, Nikkei, Nikkei 100, Nikkei 100. We’ve just added the Sensex on the Bombay Stock Exchange, Sensex 30. We’ve got commodities, we’ve got currencies, we’ve got economic indicators from the top 50 countries, all forecast over a 12-month horizon with with error rates, comparability, export, and portfolios. You can put all of your investments in a portfolio configuration and see how they’ll work out over the next 12 months.

Tony Nash

That is extended until Monday, September fourth. It’s a holiday here in the US, so we’re going to celebrate with everyone around the world. Get that stuff for $25 a month or $240 for a 12-month paid in advance subscription. Thanks very much.

Tony Nash

Guys, before we get started, just over the last few weeks, honestly, I’ve grown really, really weary of the hot takes of the Fed’s going to kill everybody and markets are going to die, or we’re in a new bull market and you have to jump on. I mean, life doesn’t work that way, typically. The whole point of a soft landing is to make markets a little bit boring. Am I off here? What are you guys are seeing differently there?

Albert Marko

No, I think that’s right. I mean, the Federal Reserve, with all the rhetoric that’s come out has talked about a soft landing and no recession and so on and so forth. I know that people don’t buy it, but look what they’ve done with oil and the market overall. They’ve kept us in this range where they tempt you with an ultimate crash and then they tempt you with market blow-off-top with all these newsletter guys selling whatever they want to sell. But their intention is to destroy excess money and they’re doing a damn good job of that.

Tony Nash

Yeah, that’s a good point. I mean, extremes are really good for selling newsletters, right? But what the Fed is trying to achieve is the slow suffocation of excess risk capital. That’s really what they’re trying to achieve so that we don’t have either of these extremes. Leo, what do you see on that?

Leo Nelissen

I agree with Albert. It’s basically, I mean, oil, equity markets are basically range-bound. Last year I said, I’m not really a trader, I mainly invest on the long term. But I said I think we’re basically in a range between the mid-3,000 points and mid-4,000 points where we are now at the upper bounds of that range. I think risk reward is getting a little bad at these levels, especially if you look at inflation, heating up again. But I think in general, I post some bearish charts, some bullish, but if you post bearish charts, most people think you are very bearish. It’s always, as you just said, there are always extremes. I think most people when they trade, they always think in these extremes. Either we are going up 10% or down 10%. I think that’s very tricky. But as Albert said, it’s a great way to reduce excess cash in the market and liquidity. But I think we could go down 10% again. But I don’t have any trades on that. I’m just basically waiting because it’s just up to inflation and we really need new signals from the feds. Everything else is just noise.

Tony Nash

Yeah. Adam, what do you think on that?

Adem Tumerkan

Yeah, I agree. I run into that quite a bit on Twitter and stuff. I get people… You post some data, whether it’s good or bad, and then half the crowd jumps on you and then the other half of the crowd just cheers it. It’s weird. I always try to tell people like, Nobody knows. Nobody knows what will happen. We’re just all bumbling around trying to make our best guess with the data available in a very complex world. I think it’s important you need to stay fluid and adapt to the markets and not take it personally. I remember I learned a long time ago that don’t confuse a profit and a loss with right or wrong because rarely do those two actually align together. One is your opinion and then one is an actual outcome. That’s something and I always try to tell people on those. But I agree. I think the market extremes right now are pretty steep. We saw it last year, everybody was expecting a hard landing. It missed. Now everyone’s expecting a soft landing and they think it’s fine. That’s what has me more worried now, is that everyone thinks it’s a soft landing?

Albert Marko

Yeah. It’s a consensus that whenever the consensus starts pushing out whatever narrative they want to, then usually it’s wrong. The recession calls for Q3 and Q4 for the past year, look at recession, recession, recession. Yet here we are with no… I mean, it’s debatable whether it’s a real recession or not, but on paper, it’s not. That’s where we’re at here.

Tony Nash

Good. So let’s dig into that a little bit. Let’s first talk about inflation and growth. You tweeted this statement from Nick Timareos from the Wall Street Journal about PCE inflation. We saw both headline and core PCE rise in July. You’ve been talking about a resurgence of inflation in H2 for six months or something, I think. Let’s talk about this data a little bit and tell us what happens from here. Does this get steeper? Does this taper off? What do you think happens here?

Albert Marko

Well, it’s a double-edged sword. We’ve talked about this a few times where inflation right now has given tailwinds to corporate earnings, which has driven the market up, which is exactly what Yellen and all her other cohorts want to see because the market is the economy, as they keep saying nowadays.

Albert Marko

But. That has after effects, second and third tier effects of commodities rising, cost of goods rising, wage inflates and rising, which in turn spurs CPI inflation. And the Fed’s done a… Well, the Fed and Treasury has done a magical job of concocting whatever data they want to give some headline number. We’re in the threes again, and we all need to be back down to two, but Supercore and Core keeps rising. It’s not going anywhere but up from here on in.

Albert Marko

Honestly, it’s been summer. Europe has been completely on vacation and in a zombie state for six months to a year now, the US is getting back to work. The holiday seasons are coming. Demand’s going to start stepping up. I saw Keith McCullough had a chart out showing that luxury good spending was down. Of course. But that coincides with people on vacation not doing much, the service industry, it was just still strong, but the consumers were still out there spending, but not as much as they were. But now here we come into the fall, the second half of the year, and into the first half of next year, and I expect demand to go right back up to where it was eight, nine months ago.

Tony Nash

Well, budgets are tightening. It’s hard to argue with the fact that budgets are tightening generally, but that doesn’t necessarily mean that the economy takes a nosedive, right?

Albert Marko

Yeah, of course. Budgets are tightening for what? 60, 70 % of America. But realistically, the top five % of the ones that are actually spending absurd amounts of money on luxury items, and they still will. When you go to a Gucci store or a Chanel store, you have lines out the door of people that probably shouldn’t be buying that stuff.

Tony Nash

Yeah, Leo, do you want to chime in?

Leo Nelissen

Yeah, I think that’s a great point. There’s this debate, is the consumer strong or is the consumer weak? That’s been going on for over a year now. I’ve always been on the site of we have a weak consumer, but I think it’s really what Albert says. On one hand, we have the more wealthier people, people who pretend to be wealthy, who are still spending and they keep not… I think Ferrari also had new all-time high earnings and a great outlook in all these companies.

Leo Nelissen

On the other hand, the Maas are actually in a very poor state. Yesterday I tweeted to the chat of one of my investments, Norfolk Southern, which is one of the biggest intermodal railroads. It’s just a mess right now. Demand for intermodal and all these things. And the dollar general is seeing massive demand issues and shrink, people stealing stuff.

Leo Nelissen

I think in general, the consumer is in a very weak state. But as Albert already said, the upper 10%, 20%, maybe 40% is keeping the economy alive. But I think we could get to a point where we are seeing more weakness, especially with inflation improving or increasing again. If the Fed needs to keep rates elevated, that’s going to really take a toll, especially with housing weakening and all these issues. I’m not bullish on the consumer for the next few months.

Albert Marko

Yeah, it’s another devil-headed sword here because it’s like double a sword because the consumers are spending, but not in as much demand as they were maybe a couple of years ago. But companies are getting away with inflated prices because they know they can at the moment and still can. But at some point…

Leo Nelissen

But it’s weakening, Albert. If you look at PepsiCo and its competition, even Wall Street they said we don’t care for these companies that use only pricing to boost revenue. They really want companies that are somehow able to boost volumes. And it’s actually happening a lot. General Mills and all these companies are struggling now big time. I think for 2020 they were so able to boost volumes a little bit, but now that’s completely gone.

Albert Marko

I agree for the general and the fundamental aspect of it, I totally agree. But when you have inflationary numbers pushing prices of services from the tech industry, which really is what the market is basing on, it gives you a skewed view of everything. Everyone thinks that earnings are great because NVIDIA posts some horse shit number out there that they can’t even justify. Then the market rally is 70, 80 points, and everyone’s, Oh, the market’s great, the economy is great, so on and so forth. 80% of the US consumers can’t buy bread. They have to choose between meals.

Tony Nash

Albert, when you say inflation is persistent, you’re talking about services inflation. You’re not necessarily talking about goods inflation.

Albert Marko

Is that right? I think goods inflation is starting to taper off as supply chains have become better. No question about that. But services has just gone through the roof and housing has gone through the roof. It’s a shelter, which is a 30% component of CPI, is just still sky high. Right now.

Tony Nash

Yeah, we’ll talk about that in the last segment. It’s really interesting to look at housing prices. I can’t wait to talk through that.

Tony Nash

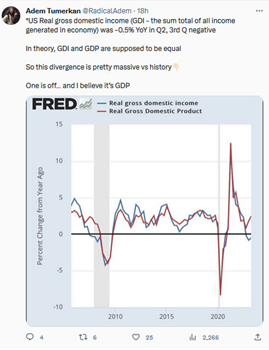

Let’s move over to growth. Adam, I’m really concerned about your… You tweeted a GDI versus GDP chart this week. We’re told that the Atlanta Fed GDP now is close to 6%. I never believe the Atlanta Fed. When people tweet the Atlanta Fed, it just erodes their credibility to me. But we’re seeing GDI at negative 5%. What’s happening here and how could the acceleration of inflation, particularly services inflation, impact GDP and GDI?

Adem Tumerkan

Yeah. GDP, GDI is just in theory, they should equal the same thing. For anyone who doesn’t know, GDP is gross domestic product. It’s what the economy produces essentially, the output. GDI is gross domestic income, the take in money from what was produced. In theory, one-to-one, they should still be equal. But there are times in history where you see them start diverging and we haven’t really seen…

Adem Tumerkan

There’s a lot of empirical evidence. Some St. Louis Fed individuals came out and they said actually, GDI may be a better indicator than GDP because historically, GDP revisions drop down to match if GDI is below. The GDI predicted 2008, three quarters before GDP did. There’s a lot of good evidence for why it’s good or worthwhile to use. Right now, the US real GDI, gross domestic income has been negative the last three quarters straight. By those standards, technically, we should be in a recession.

Adem Tumerkan

Obviously, there’s an accounting difference between the two, but still. Lacey Hunt does a good job. He posts, If you average the two out, real GDP and real GDI. It’s basically showing that the US is growing at like 0.5 for the last two questions. It’s basically been flat if you average out the two.

Tony Nash

That honestly sounds about right.

Adem Tumerkan

Yeah.

Tony Nash

On a real or nominal basis?

Adem Tumerkan

On real.

Tony Nash

Okay. Honestly, that’s about right. Half of the growth is…

Adem Tumerkan

I mean- The nominal gap…

Tony Nash

Between the two. I look around, that’s what it seems like. When I look around in my daily life, that’s what it seems like.

Adem Tumerkan

Yeah, I know. It’s interesting because we’re seeing it fade. Granted it was 0.5 and Q2 negative 0.5, and it was down over a percentage, the last two, so it’s down a little. But we also saw GDP recently. Q2 got revised down from it was about 2.4 to now 2.1. That narrows the gap between the two. But still, yeah, even if you average them out, it’s 0.5. I just don’t see how the Atlanta Fed is 6%. I don’t know if you saw yesterday’s data also, the personal income and spending. Personal income came in very weak. It’s been fading all year. It’s now just 0.2 month over month for households. But then personal spending was at 0.8.

Adem Tumerkan

Clearly, you have to use debt to subsidize that gap or excess savings. Well, the St. Louis feds posted a bunch of research. J. P. Morgan recently, the… You’re saying that the excess savings is sub 500 billion at this point from June. J. B. Morgan actually thinks that’s already exhausted for most Americans. I don’t see what the continued boom will be. Consumer credit change, if you look at the year-over-year of credit change in the US, it’s been declining the last seven months pretty sharply.

Adem Tumerkan

If your real wages can’t justify your spending, and it can’t, like a big ticket item like a home, they’re trading at a record high. The median home price right now is like 7.75 to household income. That means it would essentially take you eight years of pre-tax household, that’s two or more people, all money just to buy a house. Cars, I think it’s about 45 weeks right now, average household income. If you just use all your money from 45 weeks on a two-person household.

Adem Tumerkan

Clearly, these items, you need credit to subsidize the difference. It puts the producers, like Leo was saying with Pepsi earlier, he brings up a good point, and we’re seeing it in China too. You get to a point where if the consumer is not borrowing as much because they don’t want to either they’re getting more nervous or they’re just feeling tapped out, whatever the reason is. If they’re not going to be taking on credit to buy these big ticket items, the producers have two things. They either have to let prices collapse or sink to invite more demand, but they usually don’t want to do that, obviously, because it’ll crush their margins.

Adem Tumerkan

Then you have the other option is that they will extend credit at favorable terms. We’ve seen this in the housing market. New home builders, mortgage buy-downs because you have to choose one or the other. You have to extend the game, keep the credit game going at a lower rate to move your inventory, or you have to let prices sink enough to move the inventory organically. No one wants to do that option.

Adem Tumerkan

China is dealing with that right now actually. Now America is doing this and we’re seeing Ford, all these companies trying to push credit to move their own inventory. I guess we’ll see if the consumer really wants to go on to it. I mean, it’s better than what they can get at a bank right now.

Tony Nash

For a couple of comments. First, I think you said the average car would be 10 months of household income, right? Something like that?

Adem Tumerkan

Yeah.

Tony Nash

The average car that Albert buys would probably be about five years of average household income, I think.

Albert Marko

That’s about right, yeah.

Tony Nash

That’s my first comment. Second comment, since we’re talking macro data, I’m thinking about a clothing line like truckers, hats, and T-shirts that say always wait for the revision. I know I’d have five customers, but when I see these GDP numbers, especially on this chart that you put up with the wide yawning gap between GDP and GDI, I mean, that’s not real. There’s no way GDP is a real number, and there’s no way that that can’t be revised way down in the coming quarters.

Tony Nash

I mean, this is just not real data. I’ve said several times on this, employment data, wage data, retail price data is not right in any country. I’ve done detailed studies of that year over year. Everyone complains about China data. It’s not just China. It’s Sweden. It’s the US. It’s Germany. It’s Japan. It’s Australia. It’s everywhere. Wages, retail sales, and so on. These are terrible data points. They’re not right and they’re not settled until probably three years after. Check the third revision on these things. In many cases, these will change by more than 50%. Okay, more than 50%. We cannot trust these data. It’s not just wait for the first revision, wait for the third revision for OECD countries.

Tony Nash

Terrible. Terrible, terrible data. Is it possible that we have an environment where we have services inflation and goods price deflation?

Albert Marko

Yeah, I think that can absolutely happen. I don’t know. It depends on what rates are going down and what rates are going up. But Itry to fully expect that to happen actually probably into the early next year.

Tony Nash

Yeah, Q4, Q1. So services going up, services prices going up, goods prices not just disinflating, but actually deflating.

Albert Marko

Yeah, because they have a lot of inventory to get rid of. The holiday seasons are coming up. That stuff’s got to get moved. They have other stuff coming in spring and the summer. It’s got to get pushed around. One of the other things is that, Adam, I don’t know if you talked about, but as wage inflation. That’s certainly problematic for a lot of corporations right now. They’re getting pressure to increase people’s wages. A lot of it’s from the Biden administration and the Labor Secretary, but the fact is they can’t keep up those margins. So something’s got to give. Either growth and margins are going to go down or unemployment is going to have to tick up. But we see that. We see unemployment ticking up, especially with the revisions.

Tony Nash

That’s a perfect segue, Albert.

AI

Heads up for a short break. Are you using the potential of AI in your portfolio management strategies?

With an impressive 94.7% forecast accuracy on average, you can confidently integrate AI into your approach with CI Markets. Visualize the potential volatility of your portfolio over the next 12 months and gain insights into specific assets that might experience fluctuations. This empowers you to make informed decisions on when to buy, sell, or hold. CI Markets covers a wide range of over 1,600 assets, including stocks, commodities, forex, indices, and economic indicators. Imagine running limitless portfolio scenarios to optimize your gains. Curious about the outcome of removing or adding certain assets? Wondering how your portfolio might evolve in the next 3, 6, or 12 months? CI Markets equips you with answers to these crucial questions. Whether you seek a streamlined portfolio analysis, wish to explore diverse scenarios, or aspire to track your investments with precision, CI Markets is the ultimate tool for you. Ready to learn more? Visit us at completeintel.com/markets.

Thank you. Now back to the show.

Tony Nash

Let’s talk about jobs now. Leo, speaking of somethings got to give, you’ve been looking at the US jobs market and you tweeted about the challenge your job cuts as well as the US jobs data. As you look at this, what is this telling you? Are we closer to what the Fed may be looking for in terms of slowing down persistently hot jobs markets or do we have a long way to go?

Leo Nelissen

If you look at jobs data only, I think you can make the case that we are getting a soft learning, right? That’s jobs only. Jobs actually showed, I think it was the steepest decline in job openings, which isn’t very bullish. But overall there’s still 1.5 open jobs for every unemployed person. Even though temporary work is also rolling over, which is actually very a concessionary cycle, but you see that a lot of companies actually turn temporary workers into full-time employees because it’s so expensive to get new employees in certain areas. Then obviously, NFP numbers today you got somewhat slowing wage growth. Even though you got a pretty steep revision, you just talked about revisions of the past two months, which is quite interesting. I mean, household service showed I think, 12,000, 220,000 new jobs. I mean, it’s the softest layer planning, right? I mean, the Fed is seeing this wage growth is moderating, but still no very bearish data.

Leo Nelissen

I think we need to look beyond employment data. I think the bigger trend is bearish. If you look at temporary work is cooling off very quickly. I mean, historically speaking, I think in 100% of the cases where this happened, we were entering a recession after two or three quarters.

Leo Nelissen

I think this actually aligns with the gross domestic income we just talked about. I think, Eddie mentioned that gross domestic income had been negative for three quarters, which is nine months, if my mouth is correct. The ISM index, ISM manufacturing index has been negative since today for ten months. So it all lines up. Temporary work is slowing down. But I think just NFP numbers, I usually ignore them because it doesn’t mean so much. There’s so much data out there. Outrageous wages actually down a little bit. But if you look at the length of Fed data for job switching data and all these hourly wages, they’re actually up again. I think people who switch jobs get an earning spruce of 6.4%, which is up from 6%. That’s not what the Fed wants to see. If I were very bearish, I could make a very bearish case using this data. If I were really bullish, I could make a case. I think in general, it’s not a pretty picture. It could slow down really quickly if you see cracks in housing.

Tony Nash

A few weeks ago we saw the Michigan consumer sentiment survey, which I don’t really put a lot of stock in, but evidently the Fed looks at that and things are starting to turn sour there as well.

Leo Nelissen

Yeah, I think Michigan is interesting. I think last month it went down again. In a month prior to that event, it had a really steep increase. If you break it down into the bottom half and the top half, I don’t know exactly what they use, but only the higher income earners actually push it up. It’s actually what we talked about. The lower spending class is still in trouble and it’s not even worse because the entire index went down again. I think it’s with the bigger picture.

Adem Tumerkan

It had its biggest drop in two years. It’s the largest month over month drop. And you bring up a good point to what you and Al were talking about earlier with the wealth inequality in the country in America, the whatever, upper, middle, bottom poverty level. Mariner Eccles, who was FDR’s former Fed chairman—and I know this might sound obtuse on this, but in his memoirs, when he was reading back on how they handled the Great Depression, there’s a really good chapter in his book where he has a great quote. He says, Mass production requires mass consumption.

Adem Tumerkan

He said, And when you have the wealthy, the money flowing to the few, the hands, it acts like a huge suction pump because it’s taking buying power from the mass consumer. He’s like, The top 10% are net savers, not net consumers, hence why they’re rich. They essentially, the bottom 90% has to borrow credit to keep their spending going because their real wage is can’t justify it. Then very directly at the very end, and as soon as the credit stops, the game ends. I think it’s really important for today too because we have wealth inequality is pretty bad. It’s the upper middle class income right now that’s acting like a suction pump. You see the people post data points, they’re like, Oh, the Fed is paying so much interest on bonds. It’s going as a net asset into the economy. It’s like, Yeah, but who’s getting that money? The bottom 90% are net debtors. They have more debt than assets. But usually mortgages, student loans, all these things. So it doesn’t help them. They’re not net savers.

Adem Tumerkan

Any money they have left over that’s disposable, they can’t save relative to parking and debt. If the rates go up higher that it’s paying off on bonds to the rich, that means consequently, credit card rates have gone up, auto loan rates have gone up. The net debtors are actually feeling that it’s offsetting it. I think it’s important actually going forward, seeing how the dynamics are between the income groups. We’ve seen the bottom 75% pretty much get squeezed out over the last 20 years. It’s dropped pretty bad. I do think this is going to play a role in demand later. And I think that’s why we’re going to see continued pressure from the administrations to boost wages and keep doing things like buy now, pay later. You know what I mean? Just roll over the student loan pauses and deferments, all these things. They’re going to just have you to keep rolling the credit game over to keep that consumption going because otherwise they can’t get it.

Albert Marko

Yeah, we’re seeing that now, Adem. Literally you’re seeing that right now and it’s probably the second or third ending of what’s been going on. They’re just trying to keep this train, this locomotive going while the top 10% of earners are just holding back at the moment.

Leo Nelissen

Would you agree? When you look at construction spending, the Inflation Reduction Act, I think that’s one way to actually boost the income of lower wage earners. I think construction spending and manufacturing alone is like 200 billion on a seasonal annual basis. I think that’s one of the reasons. Obviously, onshoring technology is important, but I think… I think that’s one major driver of income in the lower income levels. I wonder what happens if these construction projects are finished. I mean, 200 billion on annual basis, that’s massive. I think if these run out and they don’t have new spending, I mean, these factories don’t need to rebuild every year. I think that could be an issue at some point. Am I just obstating this?

Albert Marko

No, I think you need to divide it in two separate parts. One is industrial scale construction, where government contracts last 10, 15 years, so on and so forth versus the smaller scale construction of homes, remodeling, plumbers, electricians, so on and so forth. The problem is as those prices go, as those wages have gone astronomical high, that hits the consumers. It costs almost double to redo a kitchen nowadays than it did five years ago. All those expenses have to be calculated in and what the consumers can do going forward.

Tony Nash

I got to tell you, I have watched more YouTube videos on how to do things around my house and with my air conditioner and with my sprinkler system and all that stuff because these guys, you’re going to spend at least 600 bucks for somebody to come out and fix something.

Albert Marko

Yeah. If you’re handy now, it goes a long way.

Tony Nash

That’s doubled over the last couple of years. The other part of this is, even at restaurants, I have some friends who have franchises, and it’s really hard to keep staff. When they come, the wages have not gone down at all. I’m in Texas, I’m not on the coasts, but those hourly wages generally are doing very well. Leo, this challenger data and the employment data you’re seeing, is this mostly impacting, say, small and mid-size, say, non-services, non-let’s say restaurant jobs, tourism jobs, that thing? Where are the layoffs hitting?

Leo Nelissen

Actually, if you look at jobs, it’s a company who cut vacancies. It’s mainly in services, I think professional services were mentioned. I think that makes sense because with rate inflation, a lot of these white-collar jobs will actually see… We are still far from automatisation and AI adoption. That’s still a long way, but we are starting to see the beginning of this. I think if inflation remains high enough on a long-term basis, you’re going to see more losses in these white-collar jobs than the blue-collar jobs. I think that’s one of my thesis, especially if economic growth returns in the future, you will see a lot of demand for the jobs you just mentioned. I think that’s the main takeaway.

Tony Nash

We see things grinding ahead with these lower-level jobs, but we see weakness in the mid, high, and higher-level jobs. Is that fair? Is that what you’re seeing?

Leo Nelissen

Yeah, exactly. Also what you just said in Germany, it’s quite interesting. Germany is now actually starting to see an increase in unemployment because of the weak manufacturing sector. But still it has a lot of structural labor shortages. We didn’t have that in the great financial crisis and in the other recessions. But now the government also plays a major role in these issues. I think they just boosted unemployment income for the unemployment by 14% in Germany. You just basically paid to stay at home. It was bad during the pandemic, but it’s still very bad, especially in Germany.

Leo Nelissen

I think the average family, if you have two or three kids and both parents are unemployed, I think you have €35,000 per year that’s after tax. The government pays for your heating, electricity, rent, everything. I think to solve these social issues, we really need to fix these things, but that’s probably not going to happen anytime soon. But it’s just what we’re seeing now, this mix between pressure on employment and structural labor demands.

Tony Nash

We started the show talking about how these extreme views, either extreme positive or extreme negative. What I’m hearing from you on labor, to be honest, it doesn’t really sound that good. Is the labor picture worse in Europe than it is in the US?

Leo Nelissen

I would say so, yes, because I think the most important labor are the ones that are most value in Germany, for example, which is the industrial heart of Europe. It’s just the entire automotive supply chain. These people, they’ve made good money for decades. They got special bonuses. They made really good money. And that’s ending now. There’s not really an incentive for companies like Mercedes or BMW to invest in Germany anymore or in Europe in general because they always used to invest in Germany because there were a large markets for automotive demand, but they stopped caring about it. I think all German automotive companies, except for Volkswagen, are now saying we’re going to drop cheaper models. We’re going to focus on margins and sell in China and the US. I talk to someone who is now building homes in South Carolina to lease them to BMW executives and that’s happening over everywhere. They’re just moving out. And if these jobs start to fail in Europe, that’s going to hurt. And we’re already seeing this now. The chemical industry is another one. I mean, people in the chemical industry, Germany is a country with relatively low wages on the receiving end.

Leo Nelissen

I mean, employees pay a lot in Texas, but the chemical industry has always been like an industry with very high wages, and that’s going to end soon. I’m not saying it’s going to end for everyone, but growth is gone, definitely. People are divesting. So for the next few years, we’re going to see some significant changes in European employment. The US is in a much better position. It’s not even close to my opinion.

Tony Nash

Interesting.

Adem Tumerkan

Okay. Just to add on that real quick. Leo, don’t you see that as a problem? Because I agree. I mean, the problem with China, Germany, Japan or the Eurozone, essentially three of the four largest economies in the world, they have no demand. They have no internal demand. They’ve all depended on exports for the last 30 years. They all run these chronic surpluses. That’s the problem. I was debating about this a year ago with a gentleman in the Twitter space because I was saying, I was like, Look, China cannot consume what they make. Germany can’t either. They don’t have the demand in that economy. So you have to depend on exports to get that growth. That’s where it’s going to come from then, because if you can’t consume it at home, you export it abroad. But once the exports start declining and US real imports of services and goods is actually negative year over year now. It’s like negative 5%. I just want to put it on the record, it’s only ever really drops negative when there’s a recession. That’s another signal for America. But we’re seeing that in the reflection of data with China. China’s exports are down double digits.

Adem Tumerkan

The only reason they run a surplus is because their imports are down even lower or further. But with these other economies not able to consume what they make and they’re trying to offload it, they’re stuck with either deflation and rising unemployment. We’re seeing that in China, youth unemployment. They’re not even posting the data anymore because it’s gotten so bad. I think Germany is probably going to be right behind them. Japan’s recent GDP was pretty big. But one thing to note, it wasn’t from their domestic economy. Their household share, yeah, it was literally external demand. Their internal demand actually declined quarter-over-quarter. I do think it’s an issue because it’s usually the US and the UK are the big two deficit-running countries in the world. If they start slowing, which we are seeing now, everyone’s like, Oh, the US trade depth’s it narrowed. But to me, that just says like, okay, that means the US is obviously pulling back on goods. Like Albert was saying, we’re moving more towards services. But that’s going to affect these economies far more because basically we have no outlet for those things.

Albert Marko

Yeah, right, Adam, that’s correct, and it’s compounded by the fact that the European, specifically Germany, has just made error after error on social and economic policies.

Albert Marko

For the past two, three decades. When Merkle was in power, she just gave away all of Germany to the Chinese with no foresight to see that they’re copying their stuff and cutting into their exports. Now the European Union, which they should have done, and I think we talked about this two years ago, Tony, they should have pivoted towards Latin America and Africa using their old school networks and rebuilding those supply chains for their products to sell out. But instead they did. They just got lazy. They got used to free money, and then here we are.

Leo Nelissen

They make it even worse always. I know that in the EU they’re basically saying we’re not going to buy soy and corn from Brazil if they cannot prove that it wasn’t part of deforestation. I mean, nobody can prove that. They’re basically saying then we won’t buy much need agriculture products from South Africa.

Tony Nash

We hear principal European statements all the time, right?

Leo Nelissen

Yeah.

Tony Nash

Exactly. I’m sorry to be I might be.

Leo Nelissen

Skeptical there. Yeah, but it’s true. But you know what Albert said? I think this week the IAA, the biggest automotive show in Europe is starting. I think it’s in Munich this time. 60% of car companies are actually foreign, with most of them being Asian, and they’re exporting so many cars to Europe right now. I think China is exporting more cars than Japan, and the quality of these EVs is actually quite good. That’s another issue. Not only is Europe losing exports, but actually there’s more consumption of Asian cars right now, and the production is in Asia. That’s just total worst-case.

Tony Nash

What you guys are telling me, what it sounds to me is we’re going to have Europe and Asia continue to export deflation. Going back to our earlier discussion, that will put serious deflationary pressure on goods. I would think in a quarter, two quarters, we really start to see some of these goods in Western markets, especially in the US, specifically goods prices go down dramatically. That’s what it says to me. I could be wrong here, but I think this working thesis has some legs to it. While in the US we see persistent wage levels. I don’t know. I could be wrong, but I don’t know that we’re going to see wages dive like we’ve seen in some previous.

Albert Marko

No. We’re not going to see wages dive. This is a political game that they want. They want wages up. Listen, it’s been 40-some years since the US worker has had a wage increase in reality, and they’re getting it now, but it’s coming at a cost.

Tony Nash

Okay. We have deflation in goods. So a lot of these companies, as you were saying, Albert, earlier, these companies that have goosed their stock prices based on margin jumps, they’re going to see some pain, right?

Albert Marko

Oh, yeah. Oh, without question.

Tony Nash

And so for consumers, if we’re seeing goods deflation, we may actually have to see. And I’m not really in the feds going to ease camp, but we may actually have to see that the Fed maybe slow down QT or something to make things easier on consumers.

Albert Marko

Oh, yeah. It’s an election year. I think it’s in election year, of course we’re going to see that. They’re going to spend. They talk about cutting spending and whatnot, they’re not doing that in an election year. They’re going to cut QT, they’re going to boost the markets, boost inflation because they know it gives tailwinds to earnings and make everything look all hunky-dory for the 2024 election.

Tony Nash

Okay, so here’s the biggest concern that I have, and this is the segue to our final segment on housing. The most significant wealth effects for Americans are felt with the value of their house.

Albert Marko

For boomers.

Tony Nash

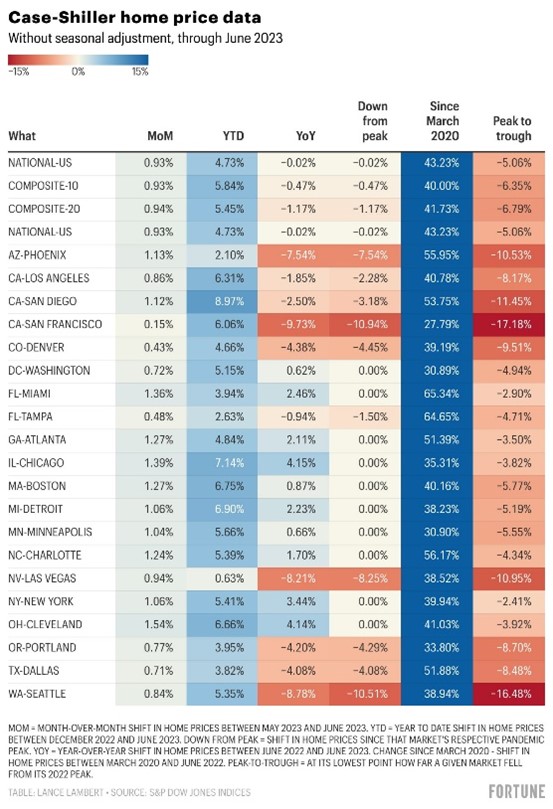

Yes, for boomers. For boomers and ex-res, I believe. Millennials don’t own houses. I’m kidding. But housing is the biggest wealth effect, right? Now that crypto is dead, it’s housing really, even for millennials, I think. Now, we’ve seen… We have this chart on the K. Schiller home price data where we show from peak to trough, houses in San Francisco are down 17%. In Seattle, they’re down close to that almost 17%. But many of these home prices are up 40%, 50% from March of 2020.

Tony Nash

Adem, you were talking about US housing markets earlier this week, and they seem to be breaking their off some amazing highs. If you look at this, US housing is still up 43% on average from 2020. That’s insane. But it’s good because it’s helping people to stand. You posted this other tweet about how the Fed has broken the market based on their MBS purchases, both on the supply and demand side. Is how is the Fed’s destruction of those markets likely to be resolved? Is there a possibility that we can have a soft landing in housing? I mean, especially going into an election year, those are serious issues for voters.

Tony Nash

What do you think happens here?

Adem Tumerkan

Two things on it, and I agree. I think the housing market has been completely screwed by, to put it nicely, between the Fed and the government. After ’08, essentially the government, we all know they went out and they were like single-family zones, HOAs, greater bureaucracy, effectively restricted supply of home construction. Right there, you take away the supply, you already put a floor under the price. Then you have the Fed, which in my opinion, financial historians are going to be scratching their head looking back at the COVID era about the mortgage-backed security buying, the two-plus trillion they bought. I think they’re literally going to look at it and be like, What the hell were they thinking? Because when the yields were so low, how would those mortgage-backed securities work? They’re buying them. When yields drop, you can refinance and you can down pay it faster. But they bought at record-low yields. Now our yields are going up and they’re not repaying them. They can’t refinance them to roll the mortgage back, secure those older. They’re stuck holding them longer. As we saw with SVB, they’re pretty illiquid, a lot of them, unless you plan to hold them until maturity.

Adem Tumerkan

I really think that you’re seeing it on both sides. The government needs to get out, allow more construction out of the way. There’s actually a good report that came out by Brookings Institute I found fascinating a year ago. The cities with the strictest building loss have the highest home prices like Portland, San Francisco, et cetera. It creates a dual incentive. They want to build properties. Like you were just saying it’s a politically sensitive topic. But if you’re a homeowner, the last thing you want is more supply because it weighs down your home price. If you just took out a $500,000 mortgage and then the government’s like, Hey, we’re going to build more supply in the area that could weigh down your home value relative to your debt, you’re not going to vote for that. You create these perverse incentives against each other like, Hey, we’re trying to do some more housing to get more individuals in. Oh, but the people who are voting don’t want that because then it’ll weigh down their home prices. It’s created this really toxic combination that there’s really no easy way out of. I think that the Fed… I really don’t understand the post-COVID thing again.

Adem Tumerkan

If anyone has better insight, I get it. People aren’t paying it, people are panning, but the government already paused mortgage deferments and essentially paused mortgage payments to give out stimulus. I didn’t see why the Fed had to come out and say, Hey, let’s just buy 2.4 trillion in bonds, mortgage bonds to pour gas on the fire. As a wealth effect, it’s created definitely like you said, it’s in theory, yes, rising asset prices is meant to stimulate more consumption. But there’s a catch to it because you can only spend more, is if you borrow against your house or if you sell your house. But the problem is if you sell your house, there’s no net difference because if you sell your house, you’re probably going to have to buy another house and the prices are up everywhere. That money just shuffles from one hand to another. It doesn’t really leave you with a massive amount of purchasing power. The idea is that, hey, you can borrow against your home because the asset price went up so high. That creates new deposits, which is inflationary because if you hold the asset and you’re borrowing against it, you’re creating more demand while holding on to what you already have.

Adem Tumerkan

I don’t know if households want to do that. There is a huge amount of home equity that could be borrowed against. But I still think individuals remember post-2008, and they’re cautious about doing that.

Tony Nash

No, I don’t. I don’t think they remember. I don’t think they care. I think we’re going to see deregulation of bond and stuff like that.

Adem Tumerkan

Yeah, that’s true.

Adem Tumerkan

We could see that. You’re right. That’s my big thing because I think the consumer right now, consumer credit change, like I was saying earlier, it’s been fading for seven months. It’s just been sinking bank loans. Your auto loans are negative. It’s the first time it’s actually been negative since they started counting the data year over year. Loans and leases are down half. It’s already below pre-pandemic levels. Bank credit is negative. It’s only been negative since 2008. Mainly it’s from securities, obviously their bond holdings, but also 75% of that bank credit rating is their loan book. Banks are tightening lending. I don’t know if individuals want to borrow at such high rates against their home when the whole market, there’s essentially an liquidity pocket. You have people who don’t want to sell because they’re locked in at a sub 3%, and you have individuals who are wary about buying because of the high prices. So something has to give one or the other, otherwise we’re just going to sit in this illiquidity pocket. I think that’s something that the government broke in the housing system. For sure.

Albert Marko

You know what I would say, Adam, and what bigger minds than me, perhaps yourself and those data is I would look at the actions of, who is it? Blackrock that bought up so many homes and have them into some portfolio. For what reason and what returns are they? What are they doing with these things? And a lot of them are not even for rent, they’re not for sale. So what are they doing with these things? Are they acting on behalf of the Fed or the Treasury or whoever to help assist on those mortgage-backed security purposes? I don’t know. That’s something that I would be really keen on hearing who’s got some perspective on that.

Adem Tumerkan

It’s interesting you bring that up because them helping the Fed, that could be a good angle actually. I’m going to look into that. But I did read a good paper from the Chicago Booth economic review and they were essentially showing that there’s a massive savings in the US post 1980s. There’s just been the top 1%, the corporations, the current account, surplus economies, they have so much savings that when it floods into the banks, it’s crushed return on investment just because you’re obviously more supply than demand.

Adem Tumerkan

The banks, they obviously more savings, they owe interest on it. That’s always compound. It’s like you always have to pay more and it keeps getting rolled over. They had to be more creative with buying the outlets for this money for some return to pay these liabilities. They said housing became attractive after 2015. It started becoming more attractive. They said big institutional money that were just drowning, trillions of dollars like black or our controls, Banker, they have literally trillions of savings that they owe. They had to find places to put it. They were looking at housing for a way to have any appreciation, but also to rent.

Adem Tumerkan

But you’re right, I haven’t really seen them renting it out.

Tony Nash

Do you think there’s any serious option if you use housing other than kicking things down the road a few years? Are we really going to see mortgage rates continue to rise? Because if consumers are as crushed as they are right now in terms of their liquidity. They’re going to have to refi, and they’re going to have to refly, and they’re going to have to refly at higher rates. We hear all these great stories about people at 3% 30-year mortgage rates, but consumers, according to the data, seem like they’re running out of money, so they’re going to have to refi. To me, it tells me that there’s going to have to be some deregulation around home equity lines of credit. People can keep their 3% loan, but they can get incremental loans at this higher rate or something like that. Does that seem plausible?

Adem Tumerkan

Yeah, definitely. I do think it’s plausible. I mean, because something has to give you. You either have to have lower prices or more supply. But like we were saying earlier, that’s going to be a bitter pill to stomach for anyone who owns property, who bought property. We’re seeing the auto market already. Negative equity is already soaring for anyone who bought it. If you do refinance, which is another problem at a higher rate, it’s very deflationary long term because you can only do two things with your money: spend or save or deliver or pay down debt. The higher your interest rate, that’s less money or less disposable income for you to spend.

Adem Tumerkan

Which will trickle into other sectors. I think that’s the big problem right now is that there’s a lot of debt, there’s a lot of higher interest rate debt revolving credit outstanding is pretty high. I don’t know if you saw recent data from the Fed… I’m sorry, the conference board. The delinquency rates on revolving credit auto loans. They’re already way past pre-pandemic. They’re the highest they’ve been actually since a decade ago. You’re having more defaults. I don’t know how much more individuals can handle it because you’re getting squeezed on mortgage.

Adem Tumerkan

Assuming you’re locked in, but now you have student debt, then you have your credit card debt, personal loans, et cetera. I don’t see how they can really get out of it easily. I think whichever one they try to choose, it’ll be politically unpalatable. I’m assuming they’ll just try to kick the can down the road or like you said, there’s going to be some deregulation, some reimbursement, some… The government is going to figure out something that they’re going to just say like, Hey, we’ll put on the taxpayer and just to keep the game going.

Tony Nash

Yeah. Very good. That doesn’t sound very… It doesn’t sound like we’re ending on a good note, but I think we’re ending on a realistic note. Housing prices are very high and they’re way above where they were a few years ago. With interest rates rising, this rarely ends well. But I think we’re going to see the feds try to extend this as long as they can and they’ll come up with really interesting ways to do it.

Leo Nelissen

I actually heard that bigger buyers and institutions, I know about BlackRock, but they’re actually building a war chest because they expect a situation where somewhere down the road, the Fed is forced to cut rates more rapidly than expected with elevated unemployment. Because at that point you can borrow really cheaply from bigger projects and you don’t have competition from people who are unemployed. I think you will see massive institutional buying if that scenario were to occur. That’s actually why I’m looking to buy in a home builder stocks. But I think that that’s the next ball case for these industries. But I agree with everything else.

Tony Nash

Yeah, Leo, I think you’re probably onto something. I think that would be very difficult to allow in an election year because America-

Leo Nelissen

I think after next year, but yeah. As Albert already said, they probably have already planned out how next year is going to go. But after that, who knows?

Tony Nash

At the end of the day, BlackRock will win. We all know that, right? But maybe not. Maybe I’ll be a little patient in ’24.

Albert Marko

Sure.

Tony Nash

All right, guys. Hey, thank you very much. Thanks for all these great insights. I really appreciate your time. This is incredibly valuable. So have a great weekend. Have a great week ahead. Thank you, guys. Thank you.

Leo Nelissen

Thanks for having me.

AI

That’s it for this week’s episode of the week ahead. Please don’t forget to rate us and review on whatever platform you are watching or listening to this. Thank you.