Our CEO and founder, Tony Nash, joins the BBC Business Matters podcast to discuss mainly the anniversary of the US Capital riot — and why most Americans don’t really care anymore. Also discussed are the patent-free Covid vax and the CES 2022 and the coolest thing in the event.

FN: Let’s go to Tony and the view from Texas. And I’m just wondering, Tony, we talked about, you know, viewing this from outside the nation’s capital. What have people been talking about today?

TN: Fergus, I gotta be really honest. No, nobody cares. I talked to students. I talked to business people. I talked to people across the country, and this is a DC event, and it’s drama that DC has conjured up and nobody in the rest of the country really cares. It’s just not a big deal for people.

FN: Okay, I’ll tell you why. I find that interesting. One thing. People travel to DC, right? For this event, whether they attended the rally or whether they actually went to the capital and took part. They weren’t DC residents, all of them. And the second thing is it’s a political thing right now, surely, across the country, there are politicians running on this event as a mandate. No?

TN: I don’t think so. No, I don’t think there are politicians running on this. You may have some politicians who are trying to run on this, but honestly, I just spoke to a couple of College students an hour ago and asked them what they thought about it. They didn’t care. I spoke to business people today and they just didn’t care. And they shrug it off as just something that’s in DC, and they shrug it off as the administration trying to distract attention. That is in the middle of the country.

That is the view from Chicago down to Texas and across the middle of the country. Nobody cares. And even in the capital building. So if these guys really wanted to overthrow the government and harm Congress people, they would have gone to the administrative buildings. I mean, these aren’t stupid people, but nobody else cares.

KA: I’m sorry, that’s not accurate. They were in the capital building.

TN: It is. Absolutely. We were in the administrative building.

TN: There were Congress people who weren’t even close to the administrative building.

FN: So, demonstrators sitting in the Speaker’s chair. Right.

TN: The demonstrators were there. The Congress people weren’t there at the end of the day. Fergus, look at the end of the day here’s what we’re talking about. We’re talking about trespass and we’re talking about property crime. Okay. That’s why people don’t care.

FN: There were five fatalities.

TN: Yeah. The Capitol police shot a woman. Right.

FN: Tony, I want to pick up on your point about people in Chicago down to Houston, not caring. This is what you’re reflecting to us about. Hang on. Let me please ask. Does that mean that nobody from Houston up to Chicago, et cetera, in the middle of America believes the message that was behind this campaign because it strikes me that 48% of the Republican Party believe the message behind what happened a year ago.

TN: What message is that, Fergus?

FN: That the election was stolen. This is the message that President Trump continues. A former President Trump continues to put out and the message that those demonstrators sought to enact as they see it. When you say people don’t care, you’re suggesting that it’s done and dusted. And I’m suggesting to you that’s far from the case.

TN: I think it is done and dusted. And I think if you look at people like Ashley Babbitt, who was shot in the back as she was entering like she was unarmed and shot at the back, these were not people who were fighting for something. Right.

FN: All right. Tony, come in. You want to jump in there?

TN: Yeah. I think Rachel is absolutely right. With the Pelosi’s support of the storming of the entry into Ledgeco in 2019, I think the Apathy in the US is really just more exhaustion than anything. I think Americans are just tired of the partisan nonsense. They’re just exhausted by it. And I think people don’t care because they don’t see this coming to an end. And DC is a world unto itself. And most of America just doesn’t care anymore. Honestly.

FN: But at that point and Rachel’s point, I was just reflecting on some of Carrie Lam’s comments exactly a year ago. And this phrase double standards, she said foreign audience should set us. Do Americans recognize that as double standards?

TN: Oh, absolutely. Yes, absolutely. They do. Well, most do not all, of course. But I think most do. If you were to rewind to 2019 and show those tapes to many Americans, they would completely get it. We’re not the Cretans that everyone tries to make us out to be. We understand that.

FN: Tony Nash is with us from Houston, may well be familiar with many of the names we’ve been discussing in the last five, six minutes. Tony, let’s focus on the philanthropy first. Presumably, that’s something you recognize that when you don’t get federal funding, you don’t get the big sort of specific targeted funding that a lot of big Pharma got back at the beginning of the pandemic. You reach into donor sections.

TN: Sure. Yeah, absolutely. And I think the Baylor College of Medicine did fantastic work here with the resources they had, and everyone here is proud of them. Texas is a huge force in medical like in public health, in oncology in many areas of healthcare. And this is just a very public view, public way of doing it. I love what they’re doing. It’s hard not to love what they’re doing.

FN: In terms of the generic issue. We’ve heard a lot about big Pharma is, I guess, easy to demonize, because a lot of the companies are making some very big returns on vaccines, and these people seem to be ready to maybe not give up the whole game, but essentially go for the generic version so that it can be spread more quickly and more cheaply.

TN: Well, all of the private sector vaccine developers, I think they got $20 billion from the US government in 2020, so those medicines have been paid for. They should give them out for free. All their IP should be open source. There should be nothing secret. The American people paid for the ones that were developed in the US. And I think as a foreign policy, we should open source that and let every country develop it at whatever cost they can.

FN: It would be a fantastic kind of diplomatic soft power, too. Wouldn’t it be?

TN: Absolutely would.

FN: And, Tony, I’m not sure how much you heard. There a quick thought from you as we end the program on the survival of Tech despite the pandemic?

TN: I think tech has thrived in the pandemic. And I’m glad to see shows like CES happening where people can go in person or be remote. I think it’s great to be in person. So I’m really happy to see it. And the coolest thing I saw at CES was a car that could change color because of nanotechnology in the paint. That was the coolest thing I saw there.

FN: Yeah, I saw that one online as well. That’s the purple thing I was referring to. Kind of Sci-Fi is real, I guess. All right, Tony, thank you very much. Indeed. Glad we got you back. Briefly. Sorry we lost the line halfway through there.

Continuing the discussion with Patrick Perret-Green of PPG Macro. This second part focuses on China’s role globally and what it will look like in 2022, especially considering the real estate industry? With the US economy, why is Patrick so skeptical about it recovering and what does the stimulus have to do with that? And what about taper tantrum? Why does he believe it already happened?

PPG started in 1997 in research where he learned how bank balance sheets work. He also run the strategy for Citi for rates and effects in Asia and at one point worked out in Sydney. And in the past five years now, he’s been focused on the global macro environment.

📊 Forward-looking companies become more profitable with Complete Intelligence. The only fully automated and globally integrated AI platform for smarter cost and revenue planning. Book a demo here.

This QuickHit episode was recorded on December 16, 2021.

The views and opinions expressed in this The year ahead: What have we learned from 2021? (Part 2) Quickhit episode are those of the guest and do not necessarily reflect the official policy or position of Complete Intelligence. Any contents provided by our guest are of their opinion and are not intended to malign any political party, religion, ethnic group, club, organization, company, individual or anyone or anything.

Show Notes

TN: When you look at what’s happening in China domestically, with the economy and with the political structure, I’m also curious about their outward political projection. And I do worry about Northeast Asia. Not just China, but Japan, Korea. And I’m curious, since you have such a historical background, I’m curious what you think about China in terms of political projection, say for 2022. Are you worried that they’re going to become aggressive in ’22?

PPG: Not ’22. You’ve got enough crap on your own doorstep at home without exacerbating the situation. And if you actually look through what’s going on, well, you can read what the Global Times says and things like the Wegar bill is clearly going to cause some short term aggravation. But overall, my sense is over the past few months, we’ve had a more of a nuanced approach that we need to just tone it down a bit, just dampen down the Wolf Warriors a little bit.

TN: They’re getting it.

PPG: You know what I mean? Down the line, ultimately. Clearly, Japan is arming significantly. Australia. We’ve got the whole quad or whatever you want to call it.

TN: Right.

PPG: One of the biggest problems, of course, has been the abject failure of US foreign policy over the past 20 years. So apart from Gulf War 2, worst disastrous war in history ever when we look at the consequences. Then the GFC.

So everyone they’re all focused on various different things. China’s love the vacuum and it’s been able to get away with loads of stuff, And Biden’s foreign policy towards China is not just China, obviously, but other places abject. Much as it irritates, so over here, I told people people, they love ranting about Trump.

Well, presentationally, he was awful. Foreign policy actually was the best foreign policy that came from the US in decades. Well, okay, assisted by people calling the establishment as well.

TN: But. The difference there is it was outcomes based foreign policy. Right. And I think what Americans have forgotten, particularly over the last 30 years, is it’s really been input space, foreign policy, values and other stuff, which is great. But we had, I think, through the probably 50s, a very pragmatic output based foreign policy. What are the outcomes? That’s the objective. And diplomacy school, my graduate work was in diplomacy, they’ve really focused on the other side of the equation with a fuzzy idea of the outcomes.

And I think what Trump brought, like him or hate him, what he brought was a focus on, a dogged focus on the outcomes of foreign policy. Right. A lot of people hate him. That’s fine. But it was a very pragmatic foreign policy environment in the US.

PPG: Yeah, going forward. And I think there’s a legacy of that now. The one thing the Congress, the only bypass is an issue on the hill is China. And Trump didn’t give a damn about human rights in Uighurs or Hong Kong. They veto proof majorities that he wasn’t going to go through the humiliation of being having a veto overturned. So he just had to roll with it. It actually was more of an inconvenience for him, I think. And then he’s people like Pompeo and military as well.

Overall, I think China, going back to the South China Morning Post article. They were saying that China could hit 5% growth with all the stimulus. Now, if you look at what will GDP activities now and the fixed asset investment. This year, forget about the year-on-year number because that’s the source, but it’s only grown. So I go through the data. I do a lot of data mining. I’m not particularly quantitative. I just sit there with some excel one plus times that times that times that.

TN: Sure.

PPG: Well, there’s only growth nominal terms, 1.6% year to date.

TN: Right. That’s a developed economy number. That’s not a growth economy number.

PPG: That’s a nominal number. Don’t forget. So given the fixed active effort uses lots of steel and cement and commodities which have all gone up in price. Actually, that number is a big fat, real negative. That’s sort of 49 year to date. I think the MBS came out year to date, that’s 49 trillion CNY. So pretty much still out there. That good 4 to 5% of GDP. Retail sales are only up 3.9%. That allows CPI at 1.6%. Either number is still like the lowest on record outside of the immediate pandemic shutdown.

So you sort of wonder where on Earth they come up with their growth numbers for the year? And for it, they’ve got a bit of boost to their exports from the trade surplus and a lack of collapse in tourism because Chinese is a big tourist. So the current account is being boosted. So that flatters the GDP. But even the Chinese next year expect net exports to come down. And if I’m right about the durable goods argument, then that’s even worse for the Chinese trade surface.

TN: Sure. I think you’re right.

PPG: So you’re left with what can they do?

TN: Can I ask you also something because you mentioned retail sales and consumer goods. I’m curious. With all of the real estate woes in China, how much of consumer debt in China is secured by real estate assets? Is that an issue? And how much of a crimp will that put on consumer spending?

PPG: That’s a tough one, because we know overall, the LTVs are very low. But we also know there’s 50 to 60 million vacant apartments. Chinese have a surreal concept about owning. They count as an investment property.

And if you rent it out, it sort of loses its original status. For what’s the description. But the problem is if you’re introducing these property taxes and you’re going in like that, well, then you are seeing second hand homes. I mean, the official home numbers are nonsense when we know full well that developers are sending stuff at big deep discounts.

TN: Right.

PPG: But by large, I think Chinese will just, it will affect sentiment. And some people are highly leveraged. So there are. Personal bankruptcy is still an infant industry in China. It’s not really established in the courts.

TN: There’s so much around it. It’s terrible.

PPG: It clearly is already dampening consumer confidence. And if the real estate is slowing in production, so we know that new sites, new land sales collapse. So that tells you going forward over the next two years, new construction activity is going to be much reduced. And if you’re not building homes, then you’re not going to be filling them with washing machines.

TN: Right.

PPG: I was actually looking at I think it was a big lift manufacturers like Otis and stuff like that. And you’re just going like, you look at the stock price and I think they’re up there and you’re going, like, well, Chinese real estate can’t go down there. You’re just thinking like, yeah, I mean, I basically have a big aversion to anything related or household good related book stock, but I’m not an equity man. I’m a bond man through and through. That’s what I do.

TN: It all makes sense. The logic is there. And given the direction we’re headed, all of this makes a huge amount of sense, especially for kind of ’22. I think 21 a lot of it’s behind us. And there are a lot of questions and a lot of I think, still skepticism around what we’ve heard globally in ’21 about the impact of spending and monetary policy.

But, Patrick, if you don’t mind, you had mentioned US foreign policy. So let’s focus on the US for a minute. And with the midterm elections in the US, and you seem to be skeptical about kind of positive momentum in the US economy, I’m really curious what your view on the US is for the year ahead?

PPG: Well, we got two things. One, we’ve got a big fiscal contraction. We shouldn’t underestimate how much the fiscal expansion has flattered the US economy because it was so large and that’s clearly massively in reverse.

One of the things, I don’t know the exact details of it, but something that US equity analyst convenience to ignore when it comes to earnings is if I ask the question, well, don’t you think 800 billion of PPP loans might have flattered your fingers as a whole? All the other loans to Airlines or stuff like that? US Airlines basically got extremely generously treated. UK Airlines haven’t. Like VA or Virgin Aircraft.

TN: All Americans are really unhappy about all the money the airlines got because the quality of service is terrible.

PPG: Yes. But, for example, the distortions, it’s really like they’re still echoing through. Like, I was talking about the monetary stimulus. It takes longer to pass through the economy. What’s the analogy? It’s like a python eating an elephant.

TN: Right.

PPG: It just takes longer to digest.

TN: Right.

PPG: Probably, extreme example. You get the point. When we look at all the fiscal front, we know that’s much less the hope for fiscal stimulus if you think where we were at the beginning of this year and everyone was going, oh, wow. It’s great. Biden’s going to push so much through. Well, we only just got the infrastructure bill through.

TN: Underwhelming infrastructure bill.

PPG: Yeah. And Build Back Better is still not through. And the fact the centrist Democrats are resisting not just Manchin, but overall, there’s much more of a realization that just look at Biden’s approval role. But the good thing is it’s supposed to be damping down the progressive, different word for them.

And then clearly Virginia shot the dams. And it’s basically long standing. Congresspeople are retiring in record numbers because they don’t want to have the humiliation of losing their district coming up. So let’s presume that the form book is correct. That basically Republicans probably take both houses. Certainly the House. Well, that stymies everything.

The administration has got a window doing stuff, plus dealing with inflation and stuff like that. And it’s always like, well, now you’ve got the administration going, well, we want to do this. But actually, Holy shit, the inflation has got out of control. We need the Fed to come in. And lo and behold, the Fed has just had, we’ve had a big move in short term rates pricing to the point when you’ve got 60 basis point increase in the dots, which we’ve never had before.

And if you said to someone a year ago, what do you think would happen if 60 basis points was added to the dots? Between what quarter? They say the dollar would surge. The curve was flattened. In fact, what we’re seeing is because so much is priced in that the curve is steepening and the dollar is softening. But there are other elements going on there as well.

And if the US economy in the great, you know, between the greatest economy ever couldn’t handle rates going back to two and a half percent and a minor reduction in the size of the balance sheets. And my view was that Fed should have probably stopped at one and three quarters rather than two and a half at most, because they forgot about the lags that they keep on telling us about. That the idea of the US economy with so much more debt, normally, it’s gone from 240%, 250% of GDP to 275 now.

TN: Right.

PPG: Basically, we’ll bring that down a little bit. But it’s gone up by 10% share GDP. So how sensitive is the US economy going to be to 150 basis points? Certainly. This is what the Fed is talking about now, by the end of 2023. Another 50 in ’24 plus balance sheet reduction as well. I just can’t see it getting there. So I’m skeptic that we’ll necessarily see Fed funds getting back to 1%.

TN: Two years is a long time.

PPG: Two years is a long time.

TN: I think, in general terms what I’m seeing. And I’m not sure if this is what you’re saying, but for the past two years, we’ve seen a private sector that’s been fixated on the public sector. Meaning the Covid regulations, the Covid stimulus, all this stuff. And it seems to me that with that stimulus disappearing and with the chaos in DC and at the state level, private sector will start focusing on the private sector and their customers instead of government. Does that sound fair?

PPG: Yeah. Although let’s not be too nice on the private sector. There’s large parts of the private sector that clearly gouged. The interesting one is, of course, global shipping. So if global shipping really disrupted and the costs have really gone up so much, how come is it that people like mask have made more money in the past year than they’ve made in the past 15 years combined? Because it’s clearly capitalized. Oligopoly is going on there, and they are gouging people. That will fade over time.

My biggest concern is actually what is the risk of a demand shock? So the Fed starts draining liquidity and we forget just how sensitive the US and the global economy is to the flow of the US money. And I think it’s the flows that is the thing. So it’s this whole point about there’s a sort of delicate tipping point in terms of if you think about it. I’m a big one for analogies. It’s been like an artery. How low does the blood flow have to get before you faint?

TN: So you’re saying that the flow will stop, but the stock will remain. Are they going to start selling off those balance sheet assets?

PPG: The Fed at some point. Sorry, the Fed.

TN: But not in ’22?

PPG: No, but I think they’ll see. But clearly the fact that they were already talking about this in terms of let’s reduce assets that. Well, fine. If we do the 75 basis points, we’re not going to wait until we get to one and a half, or as it did last time around. We’ll probably start reducing the balance sheet earlier because it’s a nice little tool. And actually, it’s quite a good tool if you want to crumble down on mortgages.

So what was noticeable in the last Redux was because the Fed was buying such a large share of them pretty much 100% of all mortgage where I stopped buying 100% all treasury issuance. But once they started reducing the mortgages, that was when mortgage spreads versus the 30 year mortgage versus the loan bonds actually really started to widen out.

TN: Right.

PPG: And then that mortgages are really the underlying credit of the credit market.

TN: Of course.

PPG: So everyone knows all the Treasuries, actually. And I think mortgages are a better reference than OAS or something. I’d rather look at a mortgage than bond against credit, and that filters through to the whole credit market. I’m never left with a situation where you have record shares of US business debt. If you look at the flow of funds reports, US business debt is a record share of GDP.

So I love the bullshit we get from the corporate. So again, the equity analysts who basically, I think should just should not be left in a room with any hard surfaces. So they go out and they say, oh, yeah, we got record amounts of cash on the balance sheet. So you had I think it was Viacom back, Wall Street Journal normal. Sort of. Yeah, on the corporate sector. Wonderful. Viacom CFO going, oh, yeah. We’ve got like 10.7 billion of liquid assets on a balance sheet. At the same time, Conveniently forget to mention that they had 170 billion of debt. Right? You don’t have any billion of debt. Things go wrong. Your ten or billion doesn’t go that far.

TN: I’ve heard over the past few months as talk of tapering has intensified. And I bring up the taper tantrum to people from 2015, and there seems to be a resistance that we’ll have a taper tantrum this time. And I kind of find that a little bit rose-tinted. There has to be a backlash.

PPG: Well, I think we’ve already had it. Quite honestly. I think we’ve already had it. If we look at some of the moves, if you’re a rate trader and you specialize in rates, we had some big swings. Look at the curve. So 530s in the bond curve before the tipping point was the minutes from the April meeting. So Powell being going on about we might be talking about paper. And then actually the minutes come out and said some participants said it’s time to maybe start discussing taper. And then the 530 was at 155. We’ve been down to 55 now. A 100 basis points with a big long. So there’s been a sort of subtle taper.

I also think you have to go back to the psychology of 2013, really, when we had the taper tantrum when rates exploded. We were still very much in a mindset. And central bankers were, too that we revert to normal, that rates would revert to where their previous level was. And it’s the educational experience. You think about all those Fed objections, all their dot points, and it took them to the the end of 2015 to do the first 25 basis point hike. It took them another year to do the second 25 basis point hike.

So I think we’re scarred by experience now. So there’s not the taper tantrum as of such at the same time, equities. It’s all fine, but they don’t realize how sensitive the economy is to the marginal changes in money.

TN: Very good. Patrick, thanks so much for your time. This is really a level of depth that I think everyone will appreciate. And I think the views are fascinating because it’s view of ’22 that I don’t think they’ll get anywhere else. So thank you very much for your time and just wish you all the best for ’22.

PPG: Yeah. Thank you. Happy Christmas. Happy holidays. And you have politically correct happy.

Patrick Perret-Green of PPG Macro joins us for a QuickHit episode to reflect what 2022 brings. Patrick got not only the Covid call, but a lot of inflation calls right through the pandemic. As we wrap up 2021, what does he think about right now and how does that set the stage for his view on 2022?

PPG started in 1997 in research where he learned how bank balance sheets work. He also run the strategy for Citi for rates and effects in Asia and at one point worked out in Sydney. And in the past five years now, he’s been focused on the global macro environment.

📊 Forward-looking companies become more profitable with Complete Intelligence. The only fully automated and globally integrated AI platform for smarter cost and revenue planning. Book a demo here.

This QuickHit episode was recorded on December 16, 2021.

The views and opinions expressed in this The year ahead: What have we learned from 2021? (Part 1) Quickhit episode are those of the guest and do not necessarily reflect the official policy or position of Complete Intelligence. Any contents provided by our guest are of their opinion and are not intended to malign any political party, religion, ethnic group, club, organization, company, individual or anyone or anything.

Show Notes

TN: So, Patrick, you’ve got not only the Covid call, you’ve gotten a lot of inflation calls right through the pandemic. And as we wrap up 2021, I guess what I’d really like is, what are you thinking about right now and then how does that set the stage for your view on 2022?

PPG: Well, there’s a whole lot of multiple issues. So I was rewatching Powell’s Q&A this morning. And clearly there is the energy side of things. There is the good side of things, the demand for goods, and they are responsible for big chunks. And I was quite surprised by the ECB’s massive upward revision for inflation for 2022 in the press conference earlier on today. But base effects are very powerful. So we always knew we were going to get peak base effects. We’re going to come in around October, November time. Oil average WTI average below about 39 to $40 last October, November. And by January are up to, or early February, we were early 60s. That base effect will tumble out quite dramatically.

I also think that the durable goods effect is also going to tumble out dramatically. We’ve had record purchases, but I remember talking joking with people last year. It was about the middle of last year, and I was saying I was just as an experiment going on ebay and seeing what I could pick a Peloton up for. So everyone got their Peloton or they bought a flat screen TV. They did the house, they did the kitchen because everyone was at home.

And I think when you look at durable goods purchases in the US and this is chart I’ve posted many times on Twitter. They are off the charts and they’re off the charts relative to disposable income as well, which is now falling. Okay, due to inflation as well. But in the US, we’ve also got this remarkable thing that it’s very different to other countries.

So you look at the UK. We had the employees taken out the other day. We’ve now got more people on payrolls than we had prepandemic. Non-farm payrolls are still down 3.9%. And in Europe employment has been much better. So the great retirement, the great resignation seems to be a US phenomenon.

But I think next year the risks are that everyone that goods purchases collapse and pricing power similarly collapses with that. And even things like autos as well will pass. So we know for well that the auto manufacturers have got lots full of 95% completed cars, and the chip shortage is actually a thing. It’s not that the world has run out of chips. There’s some papers recently looking at chip supply.

So the supply chain disruptions are being true. Yes, there’s still log jams with ports in the US, but in Asia, around Singapore, they’ve largely cleared into chain. Yeah, we’ve still got subjects very pandemic risks of problems with changing over ship crews and things like that. But overall, I think that side of things will ease down.

Okay. The pandemic is of pain, but we all know that. And there’s a lot of we’ve got Omicron now, but there is some cause for hope. It’s incredibly infectious. But all the people I know have got it. I don’t know anybody who’s had it really bad. Whereas I know people who even had Delta and they were really late. I don’t know anybody hospitalized, really. But could this be, like a bit of a bushfire?

It goes through very quickly. But actually, then we have the benefit because it’s so infectious. So many people get it. That herd in unity becomes higher. And actually, by February we’re back and everyone not giving a damn.

TN: Which is what I love. I love it. I love it. Let it be. So I hope it happens.

PPG: But let us go. But let’s not forget the underlying reality. People seem to stare in sort of my a rose tinted glasses and look back and think like, oh, wasn’t it wonderful prepondemic? No, it wasn’t. The world central banks weren’t cutting rates in 2019 because we were in good shape and there wasn’t a load of excess capacity. My concern is now that actually we talk about capacity being built. So records for containerships is less.

However, the volume of global trade actually is not particularly higher. It’s more because of disruptions. An empty container has been trapped in places. So people are building more containers and they’re building more factory space. But once the supply chain disruptions come down, then you’re going to be left with even more excess capacity.

TN: Right. Well, it’s the other side of letting all those old containerships and book carriers retire in kind of 2011 to 15. Right?

PPG: I’m still left with an image of a world that, compared to 2019, has more debt, it’s older and the capacity hasn’t gone away. And then we’ve also got the geopolitics and the politics and all that sort of stuff as well.

Watching Powell last night, I was struck by how amazingly sort of confidently was about the outlook for the US economy. Two, how he seemed to have lost all recollection of the effect of the last tightening cycle on what was a much healthier economy. So here we’re talking about, we got a 150 basis points of tightening by the end of 2023.

Okay, tapers. We all knew that’s going to end quickly. It’s going to be done by middle of March, in 10 weeks time.

TN: Just words, Patrick. It’s just words.

PPG: And then they do Redux. And he admitted at the end towards the end that they had their first discussion about the balance sheet. So I think they’ll start balance sheet reduction much sooner. But the problem is if we go back to last time when debt was so much lower, the Fed overtightened.

My reckoning, was they should have only really gone to one of the records. They completely underestimated the impact of balance sheet reduction on liquidity. I did quite a lot of work on the plumbing, and the irony is that the Fed is in charge of a mandatory systems. They’re not a very good plumber. They seem to actually understand how their own system works properly. So you end up being like the repo crisis. No, it’s not QE. We’re just buying bills and then we’re buying coupons. But it’s not QE it’s just liquidity management.

All these various issues and the other aspects I think about inflation is, there’s a lot of similarities with what happened with China in 2008, 2009. China had this. It was only a $7 trillion economy. A trillion dollars of stimulus. M1 was up 40%, M2 was up 30%. And rather than normal lags of six to eight, nine months, M2 growth peaked at the end of 2009 or late 2009. But inflation didn’t peak until the end of 2010, early 2011. So such was the volume of stimulus that came through. It just reverberated along. You dropped a Boulder in a pond?

TN: Sure.

PPG: So the ripples effect just last for much longer. And I think that’s one of the things we’re seeing, but obviously, what we also are seeing is global money growth as a whole has slowed very dramatically. And even when I look at things like excess reserves or where we are now or currency and circulation within the US, the sort of three to six month annualized rates are backed down to rates that they were at pre crisis.

So the year on year base effects are all fading out. And ultimately, unfortunately, most central bankers aren’t monetarists. They seem to have banned monetary economics. Greens bank scrapped M3 in the US. He’s a great scenery as far as I’m concerned.

TN: So when do you see this stuff really taking hold? Is it kind of mid 22 or?

PPG: The second quarter it really picks it. And we got the other side of it. So we got a US that’s doing okay or brilliantly, as far as pounds and the Feds… Europe, that actually is doing all right as well I mean, everyone’s got perpetual downer in Europe. But I think Europe could be the surprise next year.

And we got China, which is everyone still gets on this sugar high. They’re doing stimulus. And I keep on trying to explain to people, it’s not stimulus. This is dialysis.

TN: That’s a great statement.

PPG: I had a long term view on China, and it really goes back to sort of 2014. Once Xi really took control, got rid of all the rivals, started centralizing the power.

And there’s a long term rationale behind that. So, yes, in terms of the Chinese are great at some long term thinking. In other ways, I describe them to people as like, yeah, China is like a linebacker. He’s like 250 pounds. He’s six foot six tall, but unfortunately, he’s got the brain of an 18-year-old.

TN: I think the latter is more accurate, actually. With that in mind, as we move from inflation to say another obvious kind of what’s ahead for 22? What do you see for China in 22? Do you see ongoing stimulus? Do you see a roaring Chinese economy? What does China look like for you in 2022?

PPG: Well, the interesting one is that we look at everything that’s come out of the recent Central Economic Forum, all the going. The whole emphasis is on stability. None of this grandiose stuff about we’re going to be strong. It’s about stability.

Think tank South China Morning Post, which is owned by Alibaba, which is effectively controlled by the state nowadays. So there’s the G 40 Economic Council, whatever they are think tank. But it’s next PVoC governor or deputy governor on it as well. A big article. Nothing is said without less it’s approved.

So they were talking about monetary and fiscal stimulus next year and by that moderately lower interest rates. Central government stimulus because it can’t come from local governments because they’re bankrupt and they’re not getting the land sales revenue and they won’t because the collapse of the real estate.

TN: That’s an important point, though, if you don’t mind holding on the SCMP article for a second. I see people on social media say all the time, well, local governments will always come in with stimulus. But from where? I don’t understand this fallacy, that local governments can always come in with stimulus.

PPG: Well, no, they can’t, because I think even Goldman come out and say that local governments have got hidden debt of about 40 trillion CNY. And all their various financing vehicles. They’re screwed.

They don’t have the money. But over time over the past few years, we’ve probably seen this greater and greater central control. Come on them anyway. They’re more and more dependent on central government forward expenditure. And the rationale comes to this because I think the regime has always recognized that the debt or we’ll keep playing the game of Jenga is unsustainable.

TN: Right.

PPG: And therefore you have to get to a point where we’re going to take some pain. So if you look back at what Xi’s been talking about over the past few years, it’s all about struggle, the Long March. I mean, this is like really going in. That is the story of China. He conveniently forgets to mention, the Long March was actually really a long retreat and basically hardly anybody who started it survived. But that’s completely ignored.

But there is this centralization of power because they know that things have to be dealt with and there will be there’s a potential for trouble. So you become a super authoritarian super, you know, look at all the moves about data.

It’s all about the Chinese government having much more control, much more visibility, a greater ability to snuff out any sort of signs of opposition at the very earliest time.

TN: But my worry there is that China, actually, I think, is becoming fairly brittle. Meaning the Chinese government is becoming fairly brittle.

Under previous regimes, you had a fair bit of flexibility where you had the different levels, not with a lot of autonomy, but with a fair bit of autonomy. Now you have a huge amount of centralization and that creates a fairly brittle government, both economically and politically.

I’m not saying it’s necessarily going to break, but I do worry about what they’re creating.

PPG: Well, I agree with you. I’ve made sneak it past my then investment bank employees. When I came out 2014, I wrote about the stylinization of Chairman Xi.

So you have the centralization of power in one man. But then you also get that fear of slightly Tsar Russia. Nobody wants to be the bearer of bad news. So you had African swine fever. Everyone covered it up. Which was one of my concerns about Covid, because, like you saw in Wuhan, local police shut up the doctors on the 1 January.

And similarly, so you have this culture of paralysis, even pre crisis, Xi comes out and says, oh, we need to reduce coal fire stations. So good party figures, party Chiefs, local party Chiefs. We shut it, shut it down. And then they realize, actually, we haven’t got anything to heat the homes or schools.

Oh, by the way, then we have to divide the energy from the gas from the aluminium shelters to actually do that. You got this sort of, whereas, if you look back to China and Zheng and other leaders, China sort of thrived on its basically Brown envelope culture. We just get it done. Ignore central government. Okay, but at the same time, we are putting loads of cadmium into the ground and killing ourselves. But so be it.

TN: When you look at what’s happening in China domestically, with the economy and with the political structure. I’m also curious about their outward political projection. And I do worry about Northeast Asia, not just China, but Japan, Korea, Taiwan.

And I’m curious, since you have such a historical background, I’m curious what you think about China in terms of political projection, say for 2022. Are you worried that they are going to become aggressive in ’22?

BFM 89.9 asks Tony Nash from Complete Intelligence on how China’s PBOC adoption of looser monetary policy will affect the yuan and the broader Chinese economy.

SM: BFM 89 nine. Good morning. You’re listening to the morning run. I’m Shazana Mokhtar are together with Philip See. It is Christmas Eve, Friday, the 24 December 9:06 in the morning. But in the meantime, let’s take a look at the activity on Bursa Malaysia.

PS: It’s flat like Coke without any bubbles.

SM: Oh, no, that’s the worst kind of flat.

PS: Yes, the foot sabotage. Malaysia is flat slightly down .09% at 1515.

SM: So still above 1500.

PS: Still above 1500.

But it’s been yoyoing a bit green and red so far. But the rest of the markets across Asia are in green territory. The Straits time is up at 3100. Cosby also up 58% at 3015. Nikkei also up zero 6%, 28814. Now, just to bring your attention, looking at the crypto Bitcoin 5998.65 above the 50,000 mark. Theorem also uptrend 4114115.184. Now, if we shift over to the currencies, ring it to US dollar 4.11988. You’re seeing some strengthening there. But across the other two currencies pound and sing dollar, we’re seeing some weakness there.

Ring it to pound 5.62967. Ring it to Sing dollar 3.0922. Now, looking over to the value board. Really. Smattering of small caps actually driving it, but cost number one Ata IMS at .72 cent unchanged, followed by SM Track up 13% at .13, followed by Kajura Tran asphas flat at .26%.

SM: Okay, so that is the snapshot of Bursa Malaysia at 9:09 this morning. We’re taking a look now at how global markets closed yesterday.

So if we look at the US markets, they closed in the green. The Dow was up 0.6%. The S&P P 500 was up zero 6% as well. The Nasdaq was up zero 9%. So a lot of optimism going into the Christmas weekend. Joining us on the line for analysis on what’s moving markets. We have Tony Nash, CEO of Complete Intelligence. Tony, good morning. Thanks for joining us today. Now 2022 is just a week away. And given the triple headwinds of Fed tapering, Omicron and a China slowdown, will there be a difference in how developed and emerging markets in Asia are going to be impacted?

TN: I think with the tightening in the Fed and with what emerging markets are going to have to do, meaning in the near term, like China is going to have to loosen. So I think you’ll have a strengthening dollar and more of a rush for capital into the US, so that should at the margin, kind of help US markets stay strong across debt and equity. Other things. I think in emerging markets it could eventually China loosening. The PVC loosening could help demand in emerging markets, but it’s going to be hard to get around the hard slowdown that started in China around Omicron.

PS: I see.

And so when you contrast that to the Fed tightening, right. You said China PBOC is adopting a looser monetary policy. How will this affect the UN in relation to those Asian currencies in which there’s a lot of trade between these two countries?

TN: Yeah. CNY has been strong for a protracted period, and it’s made sense on one level, so China can import the energy and food, particularly and some raw materials that it needs in a time of uncertainty. So the PVC has kept it strong through this period. What we’ve expected for some time. And what we’ve shown is that after Lunar New Year, we expect the PPOC to begin to weaken the CNA. We don’t think it’s going to be dramatic, but we think it’s going to be obviously evident. Change of policy, Chinese exporters, although they’ve been producing at not capacity, but then producing pretty.

Okay. China is going to have to devalue the CNY to help those exporters regain their revenues that they’ve lost over the last two years. So we’re in a strange period globally of moving from kind of state support back to market support, whether it’s the US, Europe, Asia, we’ve really had state supportive industries, state supportive individuals as we move beyond covet. Hopefully we’re moving more into a market orientation globally, and there will be some volatility with that.

PS: Yeah, but I was wondering for China, especially, I’m interested to know what the state of the Chinese consumer will be in 2022 because the government is worried for slow down. Right. And wouldn’t they want to expedite and give a bit more ammunition to the Chinese consumer?

TN: They would. But the problem is with Chinese real estate values declining, a lot of consumer debt is secured against real estate. And so the ability of Chinese consumers to expand the debt load that they’re carrying. Is it’s pretty delicate? It’s a fine balance that they’re going to have to run. So either the economic authorities in China push real estate markets up to allow Chinese consumers to keep debt with their real estate portfolios, or they make other consumer debt type of rules that allow Chinese consumers to hold more debt.

Real estate is the part that’s really tricky in this whole equation in China, because if real estate values are falling, the perceived wealth of those consumers is falling pretty rapidly as well, and the desire to consume excessively, it’s just tempt out.

SM: And I suppose still sticking to our view of China looking at metal commodities, what metals have been affected by the slowdown of demand in China? And do you foresee a recovery for them in early 2022?

TN: Yeah. We’ve seen industrial metals like copper and steel, and those sorts of things really slow down dramatically compared to where they were earlier in 2021. We’re seeing reports of, say, copper shortages at the warehouse level at the official warehouses in China, but that’s not real. What we’re seeing and I speak to copper producers in Australia and other places. What they’re telling us is that those copper inventories are being shifted to unofficial warehouses to create a perception of shortage. So we may see a run. We may see an uptick in, say, industrial metals prices in early 22, but we don’t expect it to last long because the supply of constraint is not real.

So until demand picks up for manufacturing and goods consumption. And the other thing to remember is we’ve had a massive durable goods wave through covet. Everyone’s talked up on durable goods. Okay, so there is almost no pent up demand for durable goods. And this is the stuff that industrial metals go into on the demand side, there are some real problems on the supply side. There seems to be plenty of supply in many cases. So we don’t necessarily see the pressure upward, at least in Q1 of 2022 on industrial metals.

PS: And that’s why I’m quite interested where you say that this demand is, I think slowly going to dissipate because yesterday key US inflation gauge sharpest rise in nearly 40 years, right? Personal consumption expenditure surged 5.7% in November. How long do you think this elevator level will last?

TN: Well, US consumers are pretty tapped out. So I think inflation happens for a couple of different reasons. Some people say it’s only monetary. Not necessarily true. We’ve seen real supply constraints that contribute to inflation. We’ve seen demand pulls because of overstimulating economies, and those two things together have accelerated inflation. And so we have to remember at the same time in 2020, we saw prices. If things go down pretty dramatically around mid year, say a third of the way through the year to mid year to just after mid year.

Some of these inflationary effects have been a little bit base effects because prices fell so hard in 2020. But we have seen consumption ticking up because of government stimulus. And we have to remember if the Fed is tightening things like mortgage backed securities, their purchases of mortgage backed securities will slow. Okay, so if people can’t refinance their house or buy new houses again, those wealth effects dissipate if you have a home. If your home price is rising, whether it’s the US or China or elsewhere, the wealth perception is there and people have a propensity to spend.

But if the Fed is pulling back on mortgage backed securities, then you won’t necessarily have that wealth effect that will dissipate. So government spending will decline marginally because build back better didn’t pass. We won’t have that sugar rush of government spending flowing into the economy early in 2002, although we may see something later. I believe governments love to spend money. So I believe the US government will come with some massive package later in the year to bring government spending back up.

SM: Tony, thanks very much for speaking to us. And an early Merry Christmas to you. That was Tony Nash, CEO of Complete Intelligence, giving us a quick take on what he sees moving markets in the final year. In the final weeks of 2021. Looking ahead to 2022.

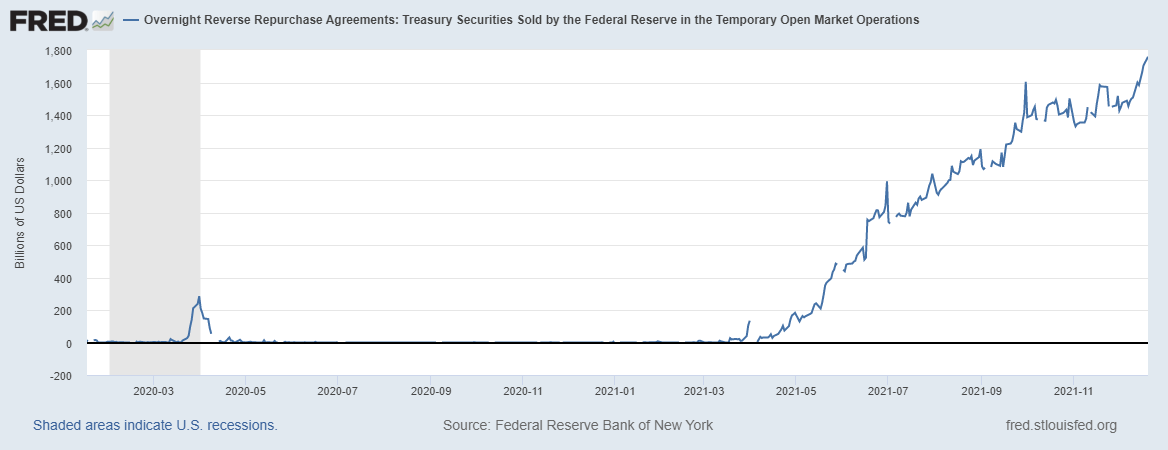

In the wake of the financial system’s cash glut and collateral shortage from the Fed’s quantitative easing program, the Secured Overnight Financing Rate drops to 0.04% from 0.05% on Monday, the first decline since October.

Even with asset purchase tapering underway, “it’s largely the same set of circumstances as in October,” TD Securities Strategist Gennadiy Goldberg told Bloomberg. “Lots of cash in the system and not a lot of collateral and that’s weighing down repo.”

Meanwhile, U.S. commercial banks park yet another record $1.75T at the Fed’s overnight repo facility, implying the banks are drowning in excess reserves, while searching for yield – which is scarce as most of the Treasury yield curve trades in net negative territory on an inflation-adjusted basis.

There’s an “incredibly large amount of cash sloshing the market,” said Complete Intelligence Founder Tony Nash via Twitter.

In August, the Fed’s overnight repo facility took up more than $1T.

Get 94.7% accuracy on your markets forecasts with CI Futures. Subscribe for only $50/mo for a limited-time only: http://completeintel.com/2022Promo

In this second part, Mike Green explains what will happen to Europe if China invades Taiwan. Will the region be a mere audience? Will it be affected or not, and if so, how? How about the Euro — will it rise or fall with the invasion? Also, what will happen to China’s labor in that case, and will Chinese companies continue to go public in the West?

📊 Forward-looking companies become more profitable with Complete Intelligence. The only fully automated and globally integrated AI platform for smarter cost and revenue planning. Book a demo here.

This QuickHit episode was recorded on December 2, 2021.

The views and opinions expressed in this What happens to markets if China invades Taiwan? Part 2 Quickhit episode are those of the guest and do not necessarily reflect the official policy or position of Complete Intelligence. Any contents provided by our guest are of their opinion and are not intended to malign any political party, religion, ethnic group, club, organization, company, individual or anyone or anything.

Show Notes

TN: So we have a lot of risk in, say, Northeast Asian markets. We have a lot of risk to the electronics supply chain. I know that this may seem like a secondary consideration. Maybe it’s not.

What about Europe? Does Europe just kind of stand by and watch this happen, or are they any less, say, risky than any place else? Are they insulated? Somehow?

I want to thank everyone for joining us. And please, when you have a minute, please follow us on YouTube. We need those follows so that we can get to the right number to reach more people.

MG: No, Europe exists, I would argue, as basically two separate components. You have a massive export engine in the form of Germany, whose core business is dealing with China and to a lesser extent, the rest of the world. And then you have the rest of Europe, which effectively runs a massive trade deficit with Germany. I’m sorry. Germany is uniquely vulnerable in the same way that the corporate sector is vulnerable in the United States. That supply chain disruption basically means things go away.

They are also very vulnerable because of the Russian dynamic, as we discussed. In many ways, if I look at what’s happened to Germany over the past decade, their actions on climate change and moving away from nuclear, away from coal into solar, et cetera, has left them extraordinarily dependent upon Russian natural gas supplies. It’s shocking to me that they’ve allowed themselves to get into that place. Right.

So my guess is that their reaction is largely going to be determined by what happens with Russia rather than what happens with China. Right. In the same way that Jamie Diamond can’t say bad things about China. Germany very much understands that they can’t say bad things about China.

Europe, to me, is exceptionally vulnerable, potentially as vulnerable as it has ever been in its history. I agree. It has extraordinary… Terrible way to say it. I don’t know any other way to say it, but Europe basically has unresolved civil wars from 1810, the Napoleonic dynamics all the way through to today, right. And everybody keeps intervening, and it keeps getting shoved back down into a false equilibrium in which everyone pretends to get along, even as you don’t have the migratory patterns across language and physical geographic barriers that would actually lead to the type of integration that you have with the United States, right.

Now ironically, the United States are starting to see those dynamics dramatically reduce geographic mobility, particularly within the center of the country. People are becoming more and more set in their physical geographies, et cetera. Similar to the dynamics that you see in Europe, which has literally 100,000 more years worth of Western settlement and physical location, than does the United States. But they’ve never resolved these wars. Right.

And so the integration of Europe has happened at a political level, but not at a cultural level in any way, shape or form. That leaves them very vulnerable. Their demographics leaves them extraordinarily vulnerable, the rapid aging of the populations, the extraordinarily high cost of having children, even though they don’t bear the same characteristics of the United States, but effectively the lack of land space, et cetera, that has raised housing costs on an ownership basis, et cetera. Makes it very difficult for the Europeans, and they have nowhere else to go now. Right. So the great thing that Europe had was effectively an escape valve to the United States, to a lesser extent, Canada, Australia, et cetera, for give or take 200 or 300 years, and that’s largely going away. Right.

We are becoming so culturally distinct and so culturally unacceptable to many Europeans that with the exception of the cosmopolitan environments of New York City and potentially Los Angeles, nobody wants to move here anymore. Certainly not from a place like Europe. I think they’re extraordinarily vulnerable.

I also think, though, that they’ve lost sight of that because they’re so deeply enjoying the schadenfreude of seeing the unquestioned hegemony of the United States being challenged. Right. It’s fun to watch your overbearing neighbor be brought down a notch. Right. You tend not to focus on how that’s actually adversely affecting your property values in the process.

TN: Sure. Absolutely. So just staying on Europe, what does that do to the importance of the Euro as an international currency? Does the status of the Euro because of Germany’s trade status stay relatively consistent, or do we see the CNY chip away at the Euros, say, second place status?

MG: Well, I would broadly argue that the irony is that the Euro has already peaked and fallen. Right. So if I go back to 2005 2006, you could make a coherent argument that there was a legitimate challenge to the dollar right.

Over the past 15 years, you’ve seen continual degradation of the Euro’s role in international commerce, if I were to correctly calculate it, treating Europe as effectively these United States in the same manner that we have with the US, there’s really no international demand for the Euro. It’s all settlement between Germany, France, Italy, et cetera.

If I go a step further and say the same thing about the Chinese Yuan or the Hong Kong dollar, right. They really don’t exist in international transactions. To any meaningful degree. The dollar has resumed its historical gains on that front. Now that actually does open up a Contra trade.

And I would suggest that in just the past couple of days, we’ve seen an example of this where weirdly, if the status quo is maintained, the dollar is showing elements of becoming a risk on currency as the rest of the world basically says some aspect of we’re much less concerned about the liquidity components of the dollar, and we’re much more interested in the opportunity to invest in a place that at least pretends to have growth left. Right. Because Europe does not have it. Japan does not have it. China, I would argue, does not have it. And the rest of the world, as Erdogan and others are beginning to show us, is becoming increasingly dysfunctional as a destination for capital. Right.

Brazil, perennially the story for the next 20 years and always will be right. Africa, almost no question anymore that it is not going to become a bastion for economic development going forward. And we’re broadly seeing emerging markets around the world begin to deteriorate sharply because the conflict between the United States and China creates conditions under which bad actors can be rewarded. Right.

If I sell out my people, we just saw this in the Congo, for example, if I sell out my people for political influence, I can suddenly put tons of money into a bank account somewhere. Right. China writing a check for $20 million. It’s an awful lot of money if I’m using it in Africa.

TN: For that specific example, and for many other things, the interesting part is China is writing a check for $20 million. Yeah, they’re writing a check for €20 million. They’re not writing a check for 20 million CNY. It’s $20 million. All the Belt and Road Initiative activities are nominated in dollars.

So I think there’s a very strange situation with China’s attempt to rise, although they have economic influence, they don’t have a currency that can match that influence. And I’m not aware, and you’re such a great historian. I’m not aware of an economic power that’s come up that hasn’t really had its own currency on an international basis. I’m sure there are. I just can’t think of many.

MG: Well, no. I mean, the quick answer is no. You cannot project power internationally unless effectively the tax receipts of your local population are accepted around the world. Right? Broadly speaking, I would just highlight that the way I think of currency is effectively the equity in a country right now. It’s not a perfect analog, but it’s a reasonable analog. And so, what you’re actually saying is the US remains a safe haven. It remains a place where people want to invest. It remains a place where people believe that the rule of law is largely in place. And as a result, anyone who trades with the United States is willing in one form or another to say, okay, you know what? I can actually exchange this with somebody who really needs it at some point in the future.

I think one of the reasons that we tend to think about the dollar as having fallen relative to the Euro or the CNY is we have a very false impression of what the dollar used to be. Right. So we tend to think about the dollar was the world’s reserve currency following World War Two and everything happened in dollars. Right.

People forget that half the world, certainly by population, never had access to dollars, never saw dollars. There was a dollar block. And then because of their refusal to participate in Bretton Woods, there was a Soviet ruble block and then ultimately far less impactful things like a Chinese Yuan, et cetera. But the Soviets, for a period of time, had that type of influence. They could actually offer raw materials. They could actually offer technology. They could offer things that had the equivalent of monetary value to places like Cuba, to places like Africa, to places like South America, et cetera. China right.\

That characterized the world from 1945 until 1990. Right. I mean, the real change that occurred and really in 1980 was that Russia basically ran out of things to sell to the rest of the world, particularly in the relative commodity abundance that emerged in the 1980s after the 70s, their influence around the globe collapsed.

And I think the interesting question for me is China setting up for something very similar. Right. It feels like we’re looking at a last gasp like Brisbanev going into Afghanistan, right. And oh, my gosh, they’re moving out and they’re taking over. Well, that was the end. They make a move on Taiwan. And I think a lot of people correctly point to this. It’s probably the end of China, not the beginning of China.

I just don’t know that China knows that it has an alternative because it’s probably the end of China, regardless.

TN: Sitting in Beijing, if you bring up any analogues to the Soviet Union to China in current history, they’ll do everything to avoid that conversation. They don’t want to be compared. Is Xi Jinping, Brezhnev or Andropov or. That’s a very interesting conversation to have outside of Beijing. But I think what you bring up is really interesting. And what does China bring to the world? Well, they bring labor, right. They’re a labor arbitrage vehicle. And so where the Soviet Union brought natural resources, China’s brought labor.

So with things like automation and other, say, technologies and resources that are coming to market, can that main resource that China supplied the world with for the last 30 years continue to be the base of their economic power? I don’t know. I don’t know how quickly that stuff will come to market. I have some ideas, but I think what you’re saying is if they do make a play for Taiwan, it will force people to question what China brings to the world. And with an abundance of or, let’s say, a growing influence of things like automation technologies, robotics, that sort of thing, it may force the growth of those things. Potentially. Is that fair to say?

MG: I think it’s totally fair. And I would use the tired adage from commodities. Right. The cure for high prices is high prices. If China withdraws its labor or is forced to withdraw its labor from the rest of the world, there’s two separate impacts to it.

One is that China’s role as the largest consumer of many goods and services in things like raw materials, et cetera. That has largely passed. Right. And so as we look at things like electrification, sure, you can create a bid for copper. But at the same time, you’re not seeing any building of the Three Gorges again. Right. You’re not seeing a reelectrification of China. You may see components of it in India. And I would look to areas like India as potential beneficiaries of this type of dynamic. But we’re a long way away from a world that looks like the 20th century. And you’ve heard me draw this analogy. Right. So people think about inflation.

The 20th century was somewhat uniquely inflationary in world history. The reason I think that happened is because of a massive explosion of global population. Right. So we started the 20th century with give or take a billion people in the global population. We finished the 20th century with give or take 7 billion people. So roughly seven X in terms of the total population. The labor force rose by about five and a half X.

If I look at the next 100 years, we’re actually approaching peak population very quickly. And if I use revised demographic numbers following the COVID dynamics, we could hit peak global population in the 2030s 2040s. Right. That’s an astonishing event that we haven’t seen basically since the 14th century, a decline in global population. And it tends to be hugely deflationary for things like raw materials. Right. People who aren’t there don’t need copper, people who aren’t there don’t need houses, people who aren’t there don’t need air conditioners, et cetera.

I think the scale of what’s transpiring in China continues to elude people. I would just highlight that we’ve all seen examples of this. Right. So go to any Nebraska town where the local farming community has been eviscerated with corporatization of farms, and the population has fallen from 3000 people to 1000 people. What’s happened to local home prices? What’s happened to the local schooling system? What’s happened to deaths of despair, et cetera. Right. They’ve exploded. China’s facing the exact same thing, except on a scale that people generally can’t imagine. The graduating high school classes are now down 50% versus where they were 25 years ago. That’s so mind blowing in terms of the impact of it.

TN: That’s pretty incredible. Hey, Mike, one of the things that I want to cover is from kind of the Chinese perspective. Okay. So we’ve had for the last 20-25 years, we’ve had Chinese companies going public on, say, Western exchanges and US exchanges. Okay. So if something happens with Taiwan, if China invades Taiwan, do you believe Chinese companies will still have access to, say, going public in the US? And if they don’t, how do they get the money to expand as companies?

Meaning, if they can’t go public in the west, they can’t raise a huge tranche of dollar resources to invest globally. So first of all, do you think it’s feasible that Chinese companies can continue to go public in the west?

MG: Yeah. Broadly speaking, I think that’s already over. Right. So the number of IPOs has collapsed, the number of shell company takeovers has collapsed. So the direct listing dynamics. I just had an exchange on Twitter with a mutual friend of ours, Brent Johnson, on this. Ironically, that would actually probably help us equities for the very simple reason that the domestic indices like the S&P 500 and the Russell 2000 do not include those companies. Right.

So if those companies fail to attract additional capital or those companies are delisted, it effectively reduces competition for the dollars to invest in US companies and US indices. Where those companies are listed and are natively traded, at least are in places like Hong Kong, China, et cetera, those are incorporated in emerging market indices. And I would anticipate, although it certainly has not happened yet. That on that type of action, you would see a very aggressive move from the US federal government to force divestiture and prohibit investment in countries like China.

I think that would very negatively affect their ability to raise dollars. Again, and I mean, no disrespect when I say this. I want to emphasize this, but we tend to think of Xi Jinping as this extraordinarily brilliant, super thoughtful, intelligent guy. The reality is he’s kind of Tony Soprano, right? I mean, it’s incredibly street smart, incredibly savvy, survived a system that would have taken you and I down in a heartbeat. Right. You and I would have been sitting there. Wow. Theoretically, someone would have shot. Congratulations. Welcome to the real world, right. He survived that system. But that leaves him in a position where I do not think that he’s actually playing third dimensional chess and projecting moves 17 moves off into the future. I think he very much is behaving in the “Ohh, that can only looks good.”

I think it’s really important for people to kind of take a step back and look at that in the same way that Japan wasn’t actually forecasting out the next 100 years. The Chinese are not doing that. It’s a wonderful psychological operation. One of the best things that people can do is go back and relisten to the descriptions of IBM’s Big Blue computer or Deep Blue. I’m sorry beating Gary Kasparov. Right. So one of the things that they programmed into that computer was random pauses. So the computer processed things and computed things at the exact same speed. But by giving Kasparov the illusion that he forced the machine to think, he started to second guess himself.

Well, what did I do there that made it think, right. He didn’t do anything. It was doing its own thing and designed to elicit a reaction from you. I think China’s done probably a pretty good job of getting a lot of people in the west and elsewhere. And I think Putin is even better at this, of second guessing our capabilities and genuinely believing that we’re second rate now.

It’s fascinating. There was just a piece that came out from the US Space Force where they’re talking about the rising capabilities of China. And if you read the public Press’s interpretation of this, China is moving ahead in leaps and bounds. And what actually he’s saying is, no, we’re way ahead. But they are catching up at an alarming rate.

TN: That’s what happens. Right.

MG: Of course, it is always easier to imitate than it is to innovate.

TN: Right. When I hear you say that it’s easier to imitate than innovate. I know you don’t mean it this way, but I think people hear it this way that the Chinese say IP creators are incapable of creating intellectual property. I don’t think that’s the case. I don’t think you mean that to be the case. They are very innovative. It’s just a matter of baselining yourself against existing technology. So it does take time to catch up. Right. And that takes years. Your TFP and all the other factors within your economy have to catch up. And it takes time. It takes time for anybody to do that.

MG: Well… And I think also it’s important to recognize that things like TFP, total factor productivity, tends to be overstated because we don’t do a great job of actually correctly defining it.

TN: It’s residual. I can tell you.

MG: Exactly right. And just to emphasize what that means, it means it’s the part that we can’t explain with the variables we’ve currently declared. Right.

TN: Right.

MG: And so when I look at TFP in the United States, I actually think TFP is quite a bit lower than the data sets would suggest, because I think that we are failing to consider the fact that we’ve introduced women into the labor force. We’ve introduced minorities into the labor force. Right. So the job matching characteristics or the average skill level of people has risen.

People live longer, so they get to work in different industries and careers for a longer period of time. The center of the distribution is now starting to shift too old, and that’s showing up as a negative impact. But we failed to consider that on the other side. And the last part is just again, remember going back to the start of the 20th century, the average American had three years worth of education at that point. Third grade education, where a year was defined as three months, basically during the non harvest season. Right.

TN: It’s the stock of productivity. Correct. We’re adding to that stock of productivity, and the incremental add is large compared.

MG: But small compared to the stock. Absolutely correct. Right.

TN: Okay. Just to sum up, since we wanted to talk about the impact on markets, I want to sum up a couple of things that you’ve said just to make sure that I have a correct understanding.

If China is to invade Taiwan, we would have in Northeast Asia a period of volatility and uncertainty. That would go across equity markets, across currencies, across cross border investments and so on and so forth. Okay. So we would have that in Northeast Asia.

MG: And I would just emphasize very quickly. So we’ve seen this rolling pattern of spikes in volatility. Right. So we saw it in 2018 in the equity markets. We saw it in late 2018 in the credit markets and commodity markets. We’ve now seen it in interest rate markets. What’s referred to as the Move index. The implied volatility around interest rates has reached relatively high levels of uncertainty.

The one kind of residual area where we just have seen no impact whatsoever has been in FX. That has been remarkably stable, remarkably managed. That’s kind of my pick for the breakout space.

TN: Okay. Great. Europe also appeared of volatility because of their exposure to both China and Russia. Since both China and Russia have a degree of kind of wiliness, especially Russia, I think almost a second derivative. Europe is volatile because of both of those factors. Is that fair to say? And that has to do with the Euro that has to do with their supply chains? That has to do with a number of factors.

MG: I would broadly argue that’s a reasonable way to think about it. I mean, almost think about it. Flip the image and imagine that the continents are ponds and the oceans are land. Right. What we’re describing is a scenario where a rock gets dropped into Asia or a rock gets dropped into Europe. You will see the waves spread across. There’s potential for sloshing over, and it’ll absolutely impact the United States. But in that scenario, we literally have two giant barriers in the form of the Pacific and the Atlantic Ocean that separate us.

And while our supply chains are integrated currently, in a weird way, COVID has been a bit of a blessing in starting to fracture those supply chains. We’ve diversified them significantly in the last couple of years.

TN: Okay. And then from what I understand from what you said about the US is supply chains will definitely be a major factor. Corporates will likely keep their investments in China until they can’t. They won’t necessarily come up with, say, dual supply chains or redundant supply chains.

US equity markets could actually be helped by the delisting of Chinese companies. Or we’ll say, US listed equities, meaning US companies listed could be helped by the delisting of Chinese equities, potentially.

MG: Certainly on a relative basis. I might not go so far as to say in an absolute simply again, because you do have people and strategies that run levered exposures. And so anytime asset values in one area of the world falls, you run the risk that the collateral has become impaired, and therefore there’s a deleveraging impact.

TN: Yes. Understood. And then the dollar continues to be kind of the preeminent currency just on a relative basis because there really isn’t in that volatile environment, there aren’t many other options. Is that fair to say?

MG: Well, again, I think there’s an element of complication. I would prefer to argue volatility. I think it is hard to argue that the dollar wouldn’t appreciate, but I also think it’s important, and this is why I go back and say we can’t actually stop Russia from taking Ukraine. We can’t stop China from taking Taiwan.

If they were to actually do that, then there is kind of the secondary loss of phase dynamic associated with it that may you could see and you’ve already seen Myanmar. You could see Thailand. You could see Vietnam. Say, you know what? We got to switch. I’m skeptical, but I’m open to that possibility.

TN: Interesting. Okay. Very good. Mike, thank you so much for your time. I really appreciate how generous you’ve been with what you’ve shared. I’d love to spend another couple of hours going into this deeper, but you’ve been really generous with us.

I want to thank everyone for joining us. And please, when you have a minute, please follow us on YouTube. We need those follow so that we’ve we can get to the right number to reach more people.

So thanks again for watching. And Mike Green, thanks so much for your thoughts on China’s invasion of Taiwan.

Tony Nash gave the BFM 89.9: The Morning Run his thoughts on how the sooner-than-expected Fed rate hikes could affect global markets. Will inflation derail hastening of the tapering talk? How does crude oil look like in the next few months? As the Christmas season is coming, how much of a concern supply chains will be for the consumers and the economy? When the Fed begins normalizing rates, which currencies will be vulnerable if or when this happens?

❗️ Discover how Complete Intelligence can help your company be more profitable with AI and ML technologies. Book a demo here.

Show Notes

SM: BFM 89.9 good morning. You are listening to the Morning Run. I’m Shazana Mokhtar together with Khoo Hsu Chuang and Philip See. It’s 9:07 in the morning. Thursday, the 25 November. If we look at how the US markets closed yesterday, the Dow was down marginally by 0.3%. The S&P 500 was up 0.2%. Nasdaq was also up 0.4%. So for some thoughts on where international markets are headed, we have with us on the line Tony Nash, CEO of Complete Intelligence. Good morning, Tony. So the Fed minutes revealed that the pace of tapering may be hastened, while macro data points from personal spending to job data suggest that the US economy is in quite the sweet spot, but will inflation derail this?

TN: Yeah. There was a statement from one of the Fed governors today talking about that inflation is not transitory in their mind or could potentially not be transitory in their mind. That’s a real danger to people who are thinking that we’re really in a sweet spot right now because it could mean Fed intervention, meaning tightening sooner than many people had counted on. So I think people had counted on some sort of intervention, maybe in Q2, but it may be happening sooner. That would have a real impact on the dollar. The dollar would strengthen, and that would have a real impact on emerging markets all around Asia, all around Africa. People would feel it in a big way where there is US dollar debt.

KHC: We are seeing that strengthening US dollar in our currency now. But I just want to get your perspective on crude oil because various countries from the US to China are now tapping into their strategic crude reserves to alleviate the present energy crisis. But if you look at crude now, it’s not really being responsive, right to these actions?