Be a more intelligent trader/investor with CI Markets. AI-powered market forecasts. Transparent error rates.

Join host Tony Nash and experts Michael Gayed of @leadlagreport , Adem Tumerkan @AdemTumerkan , and Leo Nelissen in this latest episode of The Week Ahead. They discuss pressing economic topics, providing valuable insights into global markets.

Michael Gayed explains the looming credit event, highlighting widening credit spreads and underperformance of high-yield junk debt. Leo Nelissen shares European market trends and inflation concerns.

The panel discusses deflation and reaccelerating inflation in the US. Michael suggests deflation risks while considering a potential surge in money velocity that could reignite inflation, challenging the Federal Reserve’s target. Adapting views based on evolving information is crucial amid uncertainties. Tony presents a hypothesis on deflation followed by reaccelerating inflation. Michael draws parallels to past deflation pulses, like the 1987 crisis.

Adem discusses China’s lack of an opening boost and the prevailing deflationary atmosphere. The US banking system’s challenges, including declining borrowing and impact on net interest margins (NIMs), are explained. Concerns arise over banks’ heavy borrowing and the implications of an inverted yield curve. China’s economic challenges are examined, including its net exporter status and low consumer demand leading to a deflationary environment. The high savings rate, excessive household debt ratios, and declining consumer confidence are discussed. Parallels with Japan’s balance sheet recession caution against China’s potential trap. Housing sales decline, reserve hoarding, and hidden debts exacerbate challenges, emphasizing the need for debt restructuring and a shift to a household sector focus.

Germany’s negative prints and prevailing pessimism are explored as it serves as Europe’s manufacturing hub. Long-standing issues, such as deindustrialization and nuclear reactor shutdowns, impact the economy. Declining demand and China’s automotive dominance pose challenges. The quality of Chinese exports and outsourcing of chemical production are scrutinized. Germany’s anemic consumer base and low-interest rates impact consumer confidence. A comparison between Europe and the US underscores the role of the Federal Reserve and the potential for deflation followed by inflation.

Key themes:

1. Looming credit event

2. China weakness

3. German pessimism

This is the 71st episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

Michael: https://twitter.com/leadlagreport

Adem: https://twitter.com/RadicalAdem

Leo: https://twitter.com/Growth_Value_

Transcript

Tony

Hi everyone. And welcome to the Week Ahead. I’m Tony Nash. Today, we’re joined by Michael Gayed, Adem Tumerkan, and Leo Nelissen. Guys, thanks so much for being here. I really appreciate your time. I know it’s been a pretty hectic week and we’re headed into, at least in the US here, we’re headed into a holiday weekend.

Tony

Today we’re going to talk about a looming credit event. Michael’s been on this for probably seven, eight months, maybe longer. I really want to dig into that. Adem has been talking about China weakness, and we’ve all seen that over the last six months. That’s something that we can dig deeper into as we’re starting to see that really get some traction. And then Leo is going to talk to us about Germany. So I think that’ll be really exciting.

Tony

Before we get started, I want to take a second to talk about our subscription product called CI Markets. CI Markets is our AI platform that forecasts stocks, ETFs, commodities, currencies, and economics on a weekly and monthly basis. Stocks include the S&P 500, Nasdaq, FTSE, Nikkei, and others, as well as the top 50 US ETFs. We forecast over a 12-month horizon and we show you our one-month and three-month error rates so you understand the likely risk associated with our forecast data. Subscriptions to CI Markets start at $20 a month and you can find out more at completeintel.com.

Tony

So guys, thanks again for joining us. Michael, let’s start with you if you don’t mind. I’d like to talk about this credit event that you’ve been tweeting about. You posted this very diplomatic tweet this week about the melt up, which you were early on board with that, and this looming credit event.

You’ve been on this and the deflationary bus for quite a while, as I’ve said. Can you talk us through your view? Why is this important right now?

Michael

First of all, I think we have it just to define what the credit event means. Credit event means a sequence whereby credit spreads widen, high yield junk debt ends up performing significantly worse for a moment in time than higher quality Triple A bond paper. And that tends to coincide with a fixed spike. And most fixed spikes tend to mark the end of a major volatility swing. So I’ve said many times before, I believe, oddly enough, we’re probably still in a bear market, which is not a popular opinion, but we can go through some of those reasoning. And the bear market probably ends in that fashion. Now, to your point, I’ve been saying that for a year now. Back in June of last year, I said every duration crisis eventually becomes a credit crisis. Now, there are lags, and it can take time to play out as we know. But that’s I think the major point. Now, the fact that you have a lot of these loans rolling over next year and the year after. A lot of these companies are going to be suddenly faced with higher financing costs on the rollover of their existing debt, which were at low rates post COVID.

Michael

They roll over that debt, that may not be able to survive. If they don’t survive, that’s when you end up having a lot of stress. Now, the thing is, if you’re going to have a lot of refinancing of loans next year, the stock and bond markets have to respond off of it this year because it’s a discounting mechanism of the future. So I think if I’m right that there is a crisis coming and it’s going to be around the debt rollovers of next year, this is going to be a year that a lot of people are going to be surprised by for like, what do you say?

Tony

What comes first is it do we start to see deflation appear first? Do we start to see equity market action first? So that VIX spike. What really comes first? Because if that refinancing is next year, and is not refinancing. I know there’s a number of questions here and apologies for that. Is that refinance commercial? Is it residential? Is it corporate? First of all, what are those refinance things you’re talking about next year? Then let’s get into the other.

Michael

Yeah, it’s primarily on the corporate loan side. We’re having to even touched the commercial real estate risks, housing risks, which I think are still out there. But just to be clear, I’m not like a firm or bear. Actually, I would argue that I’ve been wrong on the Melta this year. Okay, so early October last year, I said, I made that point, the end of the world is at hand. That’s why stocks are about to have a Melta. And I said that word because at the time, the speed with which yields were rising would have suggested that in a month, mortgage rates would have been like 20 %. So you can’t bet on that. So you might as well bet on stabilization of the bomber, which causes the move higher in equities. December, I said there’s a risk of a crash. You didn’t have a crash. 50 % of it was December in history. And then early January, I said back to melt up. But I think I’ve been wrong in the sense that if you look at what’s happened in terms of leadership, it’s not a broad melt up. It’s a melt up really just a select number of stocks which are driving the market at weighted averages.

Michael

You play at retailers, they’re not a melt up. You look at dividend stocks, they’re not a melt up. You look at merging markets are not a melt up. You look at small caps are not a melt up. So it’s like in Europe, in some parts it might be in a melt up. But for the most part, as I’m sure we’ll get into, right? Not so much. So my point is, people are focusing on the wrong thing. The market is already not following the pre election year script. And all that means to me is nobody knows what the hell is going to happen next. A lot of people are pulled up. It could very well be that everyone’s going to get surprised at the downside.

Tony

I have people ask me regularly, so what’s going to happen? And I can honestly say right now I can make a case for anything happening. We really are in one of those environments. And that type of environment to me is a little bit scary because I can normally look at a market and go, Okay, X is going to happen, then Y, then Z. And generally, it’s pretty straightforward. But right now, you can really make a case either way. I like that you said the point that you’re not a perma bear because it’s easy to… Because you’ve said this for a while, it’s easy for people to say, Oh, Michael’s a Pro of error. Let’s just dismiss what he says. But you do… First of all, I watch you change your outlook regularly. You calibrate it, of course. You don’t change it 180 degrees.

Michael

I flip flopped, is what people say, which is like…

Tony

Sorry?

Michael

People say I flip flopped. My answer is, you’re supposed to flip flopped. When there’s a new information, you’re supposed to adjust.

Tony

Your assumptions change. The context changes. You have to change with that. And so okay, so what happens first? Deflationary indicators? Is it equity markets changing? Is it more on the debt side and treasury side? What do you see changing first?

Michael

The bond markets that you’d see a more aggressive in credit spreads. Actually, I pushed the question to Leo, just bring Leo in because I think if you’re going to talk about the parallel of what comes first, you’re seeing it already happening in Europe. The ESB has to keep on hiking rates. You saw UK inflation brutal.

Leo

Oh, it’s brutal. Core inflation is a mess. I think it was today, coin inflation is actually up again in June. It’s an incredible mess. I think Spain inflation is below 2 %, but that’s only because of government measures. So that’s not sustainable. Not once, as you already said, credit, especially in commercial real estate, there are some incredible risk brewing over here, actually, because I’m in Europe. But yeah, that’s an issue. We have on one side weakness and on the other side high inflation, which is so keen on fighting. So it’s a trickier situation.

Tony

So do you see inflation reasserting itself in the US, Michael?

Michael

No. Well, let me put it that way. It’s all about probabilities. So I would argue that you’re much more likely to have left tail deflation risk for moment in time. And by the way, if you believe that the Fed is going to be effective in reaching the average of 2 %, you have to believe in a period of outright deflation. Because if you’re going to have an average of 2 %, you have to go past 2 %, given how high inflation was to smooth it out. So I don’t think it’s actually inconsistent from the way people think about it. But let’s talk about the other side for a second, though. There is a possibility that really what surprises people is exactly what happened in Europe. It happens in the US, meaning inflation reaccelerates. And what would cause that? It will be the thing nobody’s paying attention to anymore, which is the velocity of money, which has been in its downtrend for a really long time. Remember, inflation is more than just money supply, it’s transactions. So if you end up having conceivably a bottoming and picking up in the velocity of money, that’s going to be scary.

Michael

It’s not a base case, but that’s where it’s like, this is where we get.

Tony

Out of it. A pickup in the velocity of money is scary. Is that what you’re saying?

Michael

Yes. It would be against the backdrop of what the Fed has already done, hiking rates.

Tony

Okay. So let me just put a hypothesis out there. Last summer, a year ago, we saw crude spike, we saw inflation really start to pick up, other things. Now, we’re seeing a lot of downward pressure on crude. And of course, there’s the secondary and tertiary impacts of crude markets. So is it possible that we start to see that deflationary impact permanently? And then once that passes, we start to see a re pickup of inflation, meaning, say, late Q3, early Q4, we start to see a reacceleration of inflation. Is that a plausible, say, path for the next, say, six months?

Michael

Every credit crisis is a deflation pulse. That would make sense, actually, from a sequencing perspective, which is why I keep saying, for all you know, this year could play out a bit like 1987, where you had DAO up 38 % towards the peak, then a crash, then a Fed pivot all in one year, and all in a pre election year. So if that sequence is about now, that’s a good transition I’d argue to Adem because the part of this equation is what the PBOC and the fiscal side on China does. Perfect. Given that inflation has been actually much the opposite of everybody else. China reopened and inflation just is not trending up at all. The reopening trade is nowhere near looked like everyone else’s experience.

Tony

Yeah, a lot of slack in the market. Before we go on to Adem, Michael, I think it’s a huge factor that it is the year before an election here in the US. And I don’t think that should be discounted by anybody. The election cycles are major factors in the economy and in Fed policy here in the US. I like that you raised that and I like that you put that forward. With that, Adem, good morning. It’s pretty early where Adem is this morning, so I’m grateful that he got up to have the discussion. Good morning, Adem. Let’s start talking about China because what Michael raises is a good point. We obviously haven’t seen that China opening boost, and that’s obviously a lot of people have talked about that. You’ve posted some great stuff on Chinese incomes and house values this past week.

Can you talk us through some of that? And within the context of the deflationary vibe that we’re getting in China?

Adem

Yeah. And just before we go on to China, I just wanted to add to what Michael was saying. Also in the US banking system right now with the credit risk and deflation, we’ve seen bank lending pretty much grind to a halt over the last few months. And in a credit-driven economy, which is like the 1980s world at this point, that’s pretty deflationary. You’re having more debt being repaid than new loans, and that will probably weigh down growth, the prices and increase bank instability. The Fed stress tests yesterday pretty much showed how they’re all borrowing from the federal home loan banks and BTP at very costly rates. So as the NIMS gets spread, I think it’s going to be pretty deflationary in the US. But sorry, back to China.

Tony

Sorry, before you move on, there was a lot that you just said. When you talk about the NIMS, you’re talking about net interest margin, right? So could you talk to us, first of all, about the magnitude of the fall of borrowing, and then can you talk us through net interest margins a little bit?

Adem

Sure. Yeah, net interest margins is basically how a bank makes money. They make a loan, which is an asset for them, and then the equivalent deposit is the liability. And like we saw with SVB, they had pretty good assets. But the problem is, once you have capital flight.

Leo

Or.

Adem

Etc. Come in, you have to persuade depositors to stay. And we can see how a liquidity crisis can start and happen extremely quickly and wipe out bank capital ratios, which usually hover around 10 %, capital ratios for anyone that’s basically bank equity. Once you have non-performing loans or asset prices drop 10 % in aggregate on the balance sheet of the bank, they’re essentially insolvent. And then you have to liquidate assets to meet the liabilities, which pushes the loans below their book value. And once you get below insolvency or wipe out that 10 %, you can’t lend anymore. I don’t think banks are done. We saw the recent stress test. They tested or they looked at 84 banks under the analysis, and Bloomberg did a good piece on this. And they showed that banks have been borrowing heavily from the federal home loan banks. Federal home loan banks are basically government-sponsored enterprises in the US. They don’t have access to the interest on excess reserve market, so they arbitrage their money, like they lend to other banks, and then they can park it as reserves, collect it from the Fed, or lend out. But it’s costly right now.

Adem

It’s about 5 %. So the end of the yield curve right now is what? I mean, it’s inverted, essentially. So banks are finding it very costly to hold this money. And we actually just saw for the first time in eight years at least, banks now in the last quarter paid more in net interest income… I’m sorry, net interest than they made in quarterly profits. And yeah, I’d imagine that. And this was pre SVB or right up to that late March. And this is when they’re already borrowing heavily from the federal home loan banks and the BTP. So I’m assuming that it’s going to probably get worse in the coming quarters because nothing’s fundamentally changed.

AI

With CI markets, you can access AI-powered market forecasting for as low as $20 a month. Get 94.7 % market forecast accuracy for over 1200 assets across stocks, commodities, currencies, equity indices, and economics. With weekly updates and one-month and three-month error rates, you can rely on CI Markets to help you make informed decisions. Join a growing number of satisfied users who already transformed the way they invest and trade with CI markets. Don’t miss on another opportunity. Start forecasting with confidence today for as low as $20 a month. Visit completeintel. Com markets to learn more.

Tony

Great. With that train over, let’s move on to China.

Adem

Yeah, China’s stuck. I know a lot of people thought… I actually remember being in a space with Michael a few months back, and everyone was talking about inflation, and they were saying when the China reopening happened, and me and Michael were the only people saying, That’s going to be deflationary just because China is structurally in balance at the point that they’re a net exporter. They have no demand in that economy. So when you see everyone say like, Oh, when they reopen, there’s going to be a big consumption boom. The problem is they don’t really have the buying capacity that the US… For the second largest economy in the world, China’s revealed GDP per capita, it’s about 12,000. It’s very small and their gross savings rate is a % of GDP. It’s 45 %. It’s excessively high. To put it in context, Japan’s and Germany, which also have anemic consumers, they’re about 30 %. Saudi Arabia is 30 %. South Korea is around 30 %. So you can see a trend. All these net surplus running countries have very high savings rate. So China now has a crisis of confidence in the consumer, and their solution is, Let’s cut interest rates.

Adem

And we’ve seen the Yuan get obliterated over the last few months. And that’s going to make things worse for the Chinese consumer because a weaker currency is a tax on imports. And that’s exactly China’s problem right now. So they’re trying to get exports to grow their way out of whatever situation there is of slowing growth. But how much more can you depend on the rest of the world to absorb your excess if you can’t fund it domest? And Germany, same thing. All these other countries are in the same boat. South Korea, etc. Japan. So China now is in a thing, in my opinion, called a balance sheet recession and a balance sheet recession, BSR. It’s a term by Richard Kueh. He’s the head of macro analyst at Nomura. He wrote a great book on this called Escaping the Balance Sheet Trap about a decade ago. He was looking at Japan and he was seeing how basically in Japan in 1990, you had very high, the late 80s, household debt soared in Japan. Their currency, the Yen, appreciated about 40 %. It effectively popped their asset bubble. Their exports to GDP dropped from about it was about 12 %, 15 %, it dropped to about eight.

Adem

And that was after the Plaus Accord basically Ray in and told Japan and Germany, hey, we’re running deficits. You need to let your currency appreciate our dollars way too strong right now. Kind of like what Trump was doing with China. So you could see it’s very cyclical with these countries when they start absorbing their surplus, it means you have to run a deficit. So China, the whole theory behind China in the early 2000s, like you were talking about earlier is, they were very under invested back then when they entered the WTO. So savings flowed into the country. It made sense. The investment returns, the infrastructure was needed. But now they’ve hit that law of diminishing returns and you can see it in their debt ratios. If the amount of debt they were spending on these infrastructure projects and investment were matching growth, the debt ratios wouldn’t be exploding. Clearly, they’re putting more debt to get less returns, hence the ratio is widening significantly. China’s macro leverage to GDP, not even including local governments, is already 300 % of GDP. Household debt went from about 28 % in a way. Now it’s about 63 %. To put it in context, the US is about 73 %.

Adem

So they’re already right behind the US’s household debt to GDP for their entire economy, but their buying power is essentially one sixth of the US. And that’s troubling for China because if they cut interest rates here, and this is where the balance sheet recession comes in, they’re falling right behind Japan. Because if you cut interest rates, the idea is it will stimulate growth. In macro theory, it’s, oh, cut interest rates, it allows the production to go further out. You’ll have investment, more consumption in a rational market. But in a balance sheet recession, it’s when the consumer’s confidence is shaken and they stop borrowing. When you stop borrowing, interest rates and deflation… I’m sorry, inflation sinks, interest rates sink to zero until you find equilibrium. So China is cutting interest rates to effectively try to spur consumption and investment. But the business side, the private side of China’s investment is way down. And it makes sense because if you have a weak consumer, why are you going to invest domestically? That was the same problem Japan had. If you have no consumption in your economy or it’s very weak, you’re not going to keep investing in your own private business.

Adem

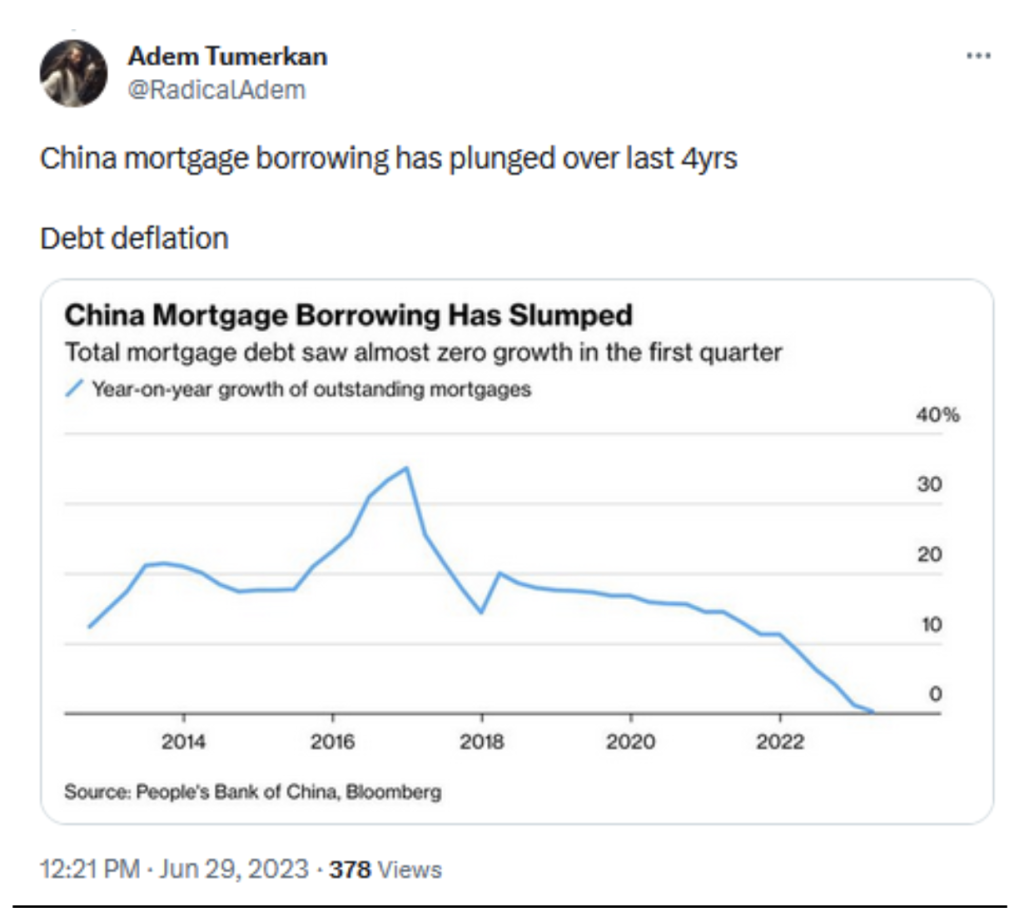

So we’ve seen that state own enterprises in China stepping up. But the government subsidies are very high there. The investment to GDP is very high there. They would have to reverse that entire balance of their entire economy to the household sector. And I don’t think China wants to do that. Or it’ll be very painful to do it because you’d have to let GDP fall and let household incomes rise for multiple years. And that’s a painful process. And yeah, so the Chinese consumer is a big saver right now, clearly, and they don’t have safety nets. So cutting interest rates will probably aggravate the problem, like in Japan, because they have a huge demographic problem coming up. They need to save for retirement. Home prices are essentially there… I think home prices in China are the world’s largest asset class. It’s about two plus times bigger than the US’s, and they are depending on that for future investment. You retire, you sell your home, you have the cash. Now, if home prices are falling and they can’t get confidence back up, we’ve seen mortgage loans taken out in China, just they’ve collapsed. It used to be about 10 %, 15 % per year.

Adem

It’s zero now. It’s actually literally dropped over the last six months all the way to zero. So they’re just not borrowing. I mean, if you look at China’s household debt to GDP, it’s been flat, essentially flat for three years. And if you don’t have new credit coming out, I don’t see how cutting interest rates is going to fix that. And they’re just flying to the same trap Japan did.

Tony

Yeah. If you talk to any Chinese leader or senior bureaucrat, there are two things that they’ll say is, first, they will not become the Soviet Union politically, and they will not become Japan economically. They are paranoid about those two things. And so the case you lay out for China becoming Japan… In Asia, you have these four demographic waves. First was Japan, then was Taiwan, then was South Korea, and now is China, where they’re just aging so fast that it’s really hard to keep up the growth rates and the monetary and fiscal policies that they had when you had such a large working group and you had such a young, large young group that you could balance out those costs across age groups. And they just can’t do that anymore. They don’t have the growth of income, they don’t have the growth of foreign investment, they don’t have the growth of exports. As other markets get older, Europe and other places get older, their consumption goes down too. So it’s a huge problem for them. And so in the balance sheet recession in 2009, first of all, before we get to that, can we talk a little bit about housing sales?

Tony

You sent a couple charts across on housing sales. I want to make sure I know you discuss these generally, but I want to talk about these a little more specifically where you say there’s no signs of a pickup in housing sales.

Leo

The.

Tony

Income’s dropping, where do you derive the Chinese income’s dropping from that chart?

Adem

So yeah, the PBOC or the MBS, they do a survey on household wealth and confidence. And the latest one showed that it did below 50. I think it’s the first time it’s done that in a few years, actually. And it was one sixth of surveyed. And granted, it’s a survey, so keep it with a grain of salt. But they were saying that their incomes have actually been declining in China, which makes sense. The yuans been battered.

Tony

And it will get even more battered, right?

Adem

Yeah, I agree. It’s interesting, the PBOC is essentially letting it fall because they could step in. They have what, 3 plus trillion in reserves.

Tony

Supposedly.

Adem

Yeah. I think they have at least five or six trillion. I mean, if you look at the current account balance of trade, they’ve had 3 trillion for It’s been what, like a decade? It’s just been flat. But they’ve been running current account surpluses since then. I’m assuming they’re offloading it to the state banks or like a shadow banking with their reserves because they have way more than three trillion, which is a problem too, obviously, because they’re just hoarding the money. They’re just sitting on it. They’re not.

Tony

Investing it. Let’s look at that for a minute, though, because after the financial crisis, they had all these loans that they continued to evergreen and pass across to other banks. They’ve had to really pay off some of those loans. So all of these dollars that China has, they’re not necessarily being stashed away, they’re being used to offset those loans that have been evergreen for the last decade plus. Yeah, that’s true. There’s this global assumption that China has all of these dollars, but they have all of this debt that’s 20 plus years old that has needed to be offset on those bank balance sheets. So do they have all of the dollars that they claim to have? Maybe. Maybe they do, maybe they don’t. But that’s how they dealt with their balance sheet recession previously, was just evergreening these loans. And so this time around, they’ll likely have to evergreen these residential and commercial real estate loans at those lower rates. Does that make sense? Yeah. And so those new dollars that come in are going to have to have to be used on evergreening those Chinese real estate loans that have taken place over just the last 10 years.

Tony

That says nothing about the ones that are over 10 years old. Is that does that make sense?

Adem

Yeah. Well, that’s also a problem in China. I agree with you because they’re cutting rates is essentially just going to let these big toxic debt piles be rolled over. Banks in China now, their nims are below 2 %. I think it’s the first time it’s actually been below 2 %, it’s like 1.9 % right now. So they’re getting squeezed pretty hard. Nonperforming loans already up to about two and a half percentage points on a $52 trillion or one y ou on a banking system. So even if they have the dollar reserves, the local government debts, which are the real problems in China right now, no one knows what they really have. But I’ve seen estimates. They’re not going to be looked at it’s about 4 trillion, but they said hidden debts are another 6. So let’s say it’s 10.

Tony

It’s 10 trillion.

Adem

Yeah. So that’s 50 % of their GDP, if not more at this point. So we’ve had to see them now they’ve been doing big fees. And this is a structural problem with China is that they’re taking more away from households, which is exactly the opposite problem. As the local governments now are straining under land sales and property values, we’ve seen record fines and taxes right now actually happening in China. There was some restaurants that their fines for serving a certain dish away, they got fined like $700 US dollars or something because they’re trying any way they can to raise capital at this point. But the thing is, when you’re taking money away from… I mean, it’s a subsidy to the government, right? And that’s the problem. You’re taking the money out of the consumer and you’re moving it back to the state.

Tony

And.

Adem

Then what does the state use it for? To roll over debt, use it on wasteful investment. So everything China is doing now is just making the anemic consumer worse. And that’s why the last six months I’ve just looked at it and I’ve just said there’s no way that you’re not going to see a booming economy with this imbalance. They have to rebalance.

Tony

And this is why it’s important to have the bad bank, right? I mean, the old archetypal, I guess, bad bank, it started, I guess, here in the S&L crisis, and Korea did it pretty successfully. And you’ve got to have a bad bank to take all those debts and then offload that onto the public so the value can be discounted so that those loans can come to some conclusion, right? Otherwise, they continue to be carried by the government. And in a.

Adem

Central crowded state… You need some restructuring.

Tony

And in a central planning state as government, if there isn’t really an actual value of money, this is why the C&Y, at least for now, can’t be a global currency because there is no actual market to market value of loans, of financial instruments, of the currency and other things. Great. I love the chart that you put up on mortgage borrowing as well. As that becomes more anemic, what that says to me is not only are people afraid of the economy, but they don’t really trust the institutions around homes generally, banks, even the real estate companies, and so on and so forth. That’s where a lot of the wealth is kept, retirement wealth and other wealth is kept is in real estate.

Adem

Yeah. The confidence is very shaken in China consumer, and that’s going to be a big problem for them.

Tony

Well, and that’s a great point. Confidence is, once the flow slows down, you can’t play musical chairs anymore. That’s the real problem with mortgages in China because you can’t the Ponsy has to stop once the flow stops. Great. Okay, so I’m really pessimistic on China now. Thanks, Adem. I really appreciate that. Let’s go to Germany, where I think we’ve had some really negative prints, and sentiment prints, Leo, over the past week. One is on business expectations and the other is on manufacturing export expectations. Leo, why are these two prints so important? First and second, what is driving that pessimism?

Leo

Well, they’re so important because Germany is essentially the manufacturing hub, actually the manufacturing hub of Europe. Just the other day, I saw that Dutch politicians were saying, Germany is struggling and that’s going to have a big impact on us as well, whether it’s transportation or services. The economies are so well connected. What I find so interesting about these indicators, I said, they just tell a story. I was just googling the other day the IFO index that you are referring to, EFO. I googled it and I saw that multiple news articles from 2019 and 2018 already said, Germany is actually headed for a recession. They’re obviously in a recession right now and it’s self inflicted. So all these issues, everyone is talking about deindustrialisation, they are right, and all these issues that Germany has, but none of these issues started after the pandemic. I think they started in 2011 after Fukoshima when Merkel decided to take these nuclear reactors offline. And that’s when it started very slowly. I think Germany peaked in 2017 when automotive production peaked. And since then, things have gone downhill quite rapidly, especially after the pandemic. I noticed in late 2020, early 2021, everyone was talking about pent up demand, which was right.

Leo

There was a lot of pent up demand. And sentiments started to come down because of the weakening economy. And everyone said, Yeah, but that’s not an issue because supply chains are easing supply chain bottlenecks. So that’s good for Germany. I was always a bit skeptical because yes, supply chains are getting healthier, much healthier, but demand is struggling right now. So I actually looked it up from the EFN and they said backlogs are a huge issue. So demand is basically gone at this point for cars, chemicals, and that’s what they’re saying. So chemicals in a very bad place, machinery, which is essentially 50 % of Germany’s export chemicals, machinery, and stuff related to this. And then transportation and logistics are struggling right now. So Germany was, especially after the Euro crisis, one of the strongest players in Europe. And now it’s the only G7 nation with negative growth expectations for this year. So that’s a big problem. And now you’re seeing export weakness again, which is triggered because of China weakness and in general, the global economy is quite bad, or it’s weakening. What I need to add as well is Germany has rapid population growth.

Leo

Last year, population grew by 1.4 %. Obviously, a lot of refugees, Ukraine, Syria and refugees and everything, but Germany isn’t handling these things quite well. Most of these people are unemployed. The government is basically paying people to be unemployed. There are no incentives for people to get into work. Germany right now is a structural mess. It’s incredible. And then China now, we’re talking about China, China is getting stronger in automotive. Essentially, Germany helped China grow after the 1970s. They saw a nation wanted to grow with manufacturing. They needed machinery for construction and everything. And then once China’s middle class started to grow, Germany saw an opportunity to sell cars, Volkswagen and luxury cars like Mercedes and BMW and whatnot. But now China is saying, Hey, we want to take this market back. So especially in electric segment, the test drive is quite a big player, but the vast majority of cars are Chinese that are sold right now in the EV space. And China controls EV related commodities. So the Europeans actually, in another problem, they’re just now pushing for EVs. I think they want to ban fossil fuel cars after 2035 or something. Not entirely sure on that one.

Leo

But they would essentially now give China more power and harm their own economies because China is now starting to export cars. I looked it up the other day and it’s just wild. Germany is now exporting fewer cars than China. Last year, Germany exported 2.6 million cars and China exported 500,000 cars more than Germany. And that’s almost 400 % growth in the past seven, eight years, China. These developments are just incredibly bad for Germany.

Tony

It’s easy for people to go, Yeah, but those China exports are low value, low quality exports, and German exports are high quality, high value exports. I think that’s the knee jerk reaction to that. Is that the case?

Leo

In general, a lot of products from China have inferior quality. German companies already said for over decades, we want to work with the Chinese, but the workforce and the equipment we get, I want to work with what we need for our production. Quality has always been a Chinese issue and I expect it to continue. But in EVs, China is actually doing quite well. There are a few brands that I never heard of that just came popping up in the past few years that are now flooding. Growth is high, but they’re not dominant right now. But the quality of these cars is great. People actually, great reviews and everything. That’s a big problem. The EV quality is great and that’s the thing that hurts. Then chemical production is going overseas as well. That’s one thing that really started to accelerate after the invasion of Ukraine. Big companies as BISF, they are just outsourcing now. They made crystal clear, we’re not going to invest in Germany anymore. So production, I think BISF is accelerating investment in Texas, Louisiana, in China. That’s a big issue, especially because chemicals are so important in pretty much every supply chain. That’s probably coming from structural inflation.

Tony

Yeah.

Adem

Go.

Tony

Ahead, Adem, sorry.

Adem

I was just going to ask Leo, a lot of people call the UK the sick man of Europe, but I’ve actually argued that post 2000, Germany has been the sick man of Europe because their consumer is so anemic. Their current account surplus is… I don’t know if you guys have seen that chart after the Hartz reforms in Germany, early 2000s. It’s enormous how much they’ve been excess dumping their savings and unconsumed goods abroad. So I was just curious what you thought about that.

Leo

Yeah, I think that was one of the things that I think some Germans actually enjoyed when the UK went pretty much south after Brexit vote. I always so argue that the UK is somewhat of a mess right now. But yeah, Germany is a stick man. I mean, the UK has become way more flexible when it comes to international trade deals and geopolitical play. Uk is quite dominant and Germany is lacking all of these things. And just another number that I looked up, outside investments in Germany last year were actually 11 billion. And German companies invested more than close to 150 billion outside of Germany. And add to this, as you said, the consumer is in a pretty bad spot because not just because of inflation and higher rents and everything, but because of low interest rates after the Great Financial Crisis. People just spend it all. Germans, just like us Dutch, we barely spend. We are very frugal, but still, people spend a lot. And everyone was saying, Yeah, it’s because rates are so low. That’s one of the things that’s now hitting us in the back. That’s really stinging. If you look at consumer confidence, it has bounced a bit, but I think it’s close to or even below the 2020 pandemic laws right now.

Tony

Right now.

Leo

In Germany? Yeah, right now in Germany.

Tony

So business confidence and consumer confidence are? Consumer confidence is the thing that’s the difference. I wasn’t aware of.

Leo

Consumer confidence.

Tony

What’s inflation in Germany right now?

Leo

I don’t know the numbers on top of my head, but I had to look it up. But core inflation is actually coming up again. I mean, food inflation is high. Energy inflation is down everywhere, but I don’t know the numbers exactly, but it’s way above where the ECB wanted to be.

Tony

Hearing Michael’s views at the start, and he pointed to Europe as a leading edge of what could happen here in the US, do you see that happening in Europe right now, particularly in Germany?

Leo

It’s tricky. I think because a lot of what’s going on depends on the Fed. I think they’re way more powerful than ECB. The ECB now, they’re way more reactionary. Europe is different because we have a lot of structural issues. Right now, Italy and Spain, they’re just complaining about high rates, obviously. And still, a lot of the debt issues, they have just been massed by cheap money prior to the hiking cycle. I think it’s a difficult situation to compare. But overall, I think it’s similar. If you get a situation where deflation were to occur, I think it could, but it would be a very short period because it would probably be followed by quantitative easing, rapid rate cutting, and that would be unwind some of the structural issues, especially in energy. So I think you would get a second wave of inflation very quickly, even if deflation were to happen, both in Europe and in the US.

Tony

Interesting. Okay, very interesting show today, guys. I really appreciate this. Thank you so much for your time. I really appreciate it. Have a great weekend and have a great week ahead.

Leo

Thank you very much, guys. Thanks for having me.

Adem

Yeah, thank you. Bye. bye..