Experience the power of AI in forecasting Markets. Subscribe to CI Markets Free: https://completeintel.com/markets

Welcome to another episode of the Week Ahead! Today, we’ve got a fantastic lineup with Mike Green, Tracy Shuchart, and Albert Marko getting into some of these hot topics.

🚀 Bitcoin ETFs, Inflation, and Labor Data with Mike.

Mike breaks down the recent approval of spot Bitcoin ETFs, the surge in Bitcoin prices, and contrasting views from Cathie Wood and Vanguard. We’ll discuss how these ETFs could shake up the crypto landscape.

Plus, Mike shares insights on inflation and wage growth, exploring whether inflation might take an unexpected turn this year. And of course, we’ll touch on the intricacies of US jobs data and the impact of flawed birth/death adjustments.

🛠️ Industrial Metals and Junior Miners with Tracy.

Tracy explores the recent rally and subsequent dip in prices, keeping an eye on the copper futures and the Sprott Junior Copper Miners ETF. Tracy breaks down the factors influencing these markets and what to watch out for in the near future.

💼 The Yellen Factor with Albert.

Albert discusses the Yellen factor as he explores recent developments, such as the potential end of negative rates in Japan and Lagarde’s stance on the ECB. Albert raises a thought-provoking question: Are the BOJ and ECB statements influencing the Fed’s dovishness? We’ll unpack the global economic chessboard and how it might impact the USD.

Transcript

Tony Nash

Hi everyone and welcome to Week Ahead. I’m Tony Nash. Today we’re joined by Mike Green, Tracy Shuchart and Albert Marko. We’ve got some key themes today, of course. Late this week we saw the US fire submissive of Yemen over the Red Sea issues. We’re going to jump into that a little bit in Tracy’s section on industrial metals, and we’ll talk a little bit about crude, a little bit about shipping, that sort of thing. But we’re going to first cover bitcoin ETFs, inflation, labor data with Mike. Mike covers everything. So we want to kind of jam a lot in there. With Tracy, we want to talk about industrial metals and some of the junior miners, which she’s been paying attention to. And with Albert, we want to talk about central banks and really the influence of Yellen on some of these, on, obviously the Fed and some of these other central banks.

Tony Nash

So before we get started, I want to let you know about a new free tier we have within CI Markets, our global market forecasting platform. We want to share the power of CI Markets with everyone. So we’ve made a few things for you. First, economics. We share all of our global economics forecasts for the top 50 economies.

Tony Nash

We also share our major currency forecasts as well as Nikkei 100 stocks. So you can get a look at. What do our stock forecasts look like? There is no credit card required. You can just sign up on our website and get started right away. So check it out. CI Markets free. Look at the link below and get started ASAP. Thank you.

Tony Nash

So, guys, exciting evening. There’s stuff going on in the Middle East. It seems like the punchline always ends. Earlier this week, we saw a lot about the bitcoin ETF and the approval of that. First the non approval of it, and then the approval of it. Mike, you and I first spoke about bitcoin, I think, a couple of years ago when the PLA in China was the largest miner of bitcoin. Of course, bitcoin is up, what, 75% since October, which is totally normal for an asset. Right.

Tony Nash

We have Cathie Wood saying that the base case for bitcoin is $600,000. We have vanguard and a bunch of other firms saying they won’t allow crypto ETFs on their platform. So what happens with this? Even with a spot bitcoin ETF, does it still stay this kind of fringy, exciting, volatile asset, or does it really come into being kind of a normative type of asset that people invest in? I’m not pro or anti bitcoin here. I’m just trying to really understand what’s the implication of this bitcoin ETF?

Mike Green

Well, I think what the bitcoin ETF does is exactly what the bitcoin proponents highlight is that it makes it available to more individuals at lower effort. So those who are very interested in owning bitcoin would have made the effort to put themselves onto coinbase or onto alternative exchanges to obtain it, or they would have mined it. Now, suddenly, it’s easily available in an ETF framework, right? It’s not dissimilar. A lot of people have compared it to the introduction of the GLD ETF that made gold easily available for many retail investors relative to going to a coin store and buying physical gold, or arranging for wholesale delivery in some way, shape or form, or buying miners. Right.

Mike Green

And so one of the things that we’ve already started to see is a derating of many of the proxies for bitcoin. Things like the miners, things like MicroStrategy, et cetera, have derated fairly sharply in the immediate lead up to this, even as they benefited from the appreciation of bitcoin. By the way, I think the bitcoin appreciation is more than you’re actually highlighting.

Mike Green

That underlying dynamic I think is likely to play out here as well, where if you were buying through a proxy, this now allows you to buy, theoretically direct access to bitcoin. I personally think that this is going to be more of a sell the news type framework. That certainly seems to be what’s playing out. And so it’s adverse for both things like Coinbase and MicroStrategy, as well as bitcoin itself. Candidly. People purchase in advance of an event that’s as easily available and well known as this. I gotta be honest with you. I don’t know that there’s going to be that much dramatic volume that actually transits over to bitcoin. As much enthusiasm as we see on Twitter, et cetera, for bitcoin at this point, the Google search volumes the interest in it. The actual utility of bitcoin has fallen and not substantively changed in any meaningful way over the last couple of years. And so I just kind of see this as a nothing burger. I had a joke where I was going to pull up the scene from Jerry Maguire where Cuba Gooding Jr. Says, you know, people can have the coin, but they can’t have the Quan.

Mike Green

I think bitcoin has lost the Quan. I don’t think anyone really cares or really believes that this is the future of finance.

Tony Nash

And something I was saying earlier this week is, I don’t understand. If there’s such inherent value in bitcoin, immutable inherent value, then why is everyone pumping it up pre the ETF? I just feel like there’s this expectation that because it’s an ETF, it’s going to multiple x. But if the inherent value is already there, why aren’t we already close to the inherent value?

Mike Green

Well, when you talk about the inherent value, I mean, again, it, beyond the question of what is intrinsic or inherent value actually mean.

Tony Nash

It has the intrinsic value of a cell in my excel workbook, is what I believe.

Mike Green

Yeah, that’s basically what it is. I mean, look, bitcoin itself is the token that is released as payment to the accountants on the blockchain. Bitcoin. Blockchain. That’s it. That’s all it is.

Mike Green

And everything else we’re engaged in is secondary trading of those tokens. Now, at some point, under a proof of stake type framework, people might actually value those bitcoins as a mechanism for providing collateral to prove transactions or to underwrite transactions. But that’s not the current configuration, right? I mean, that’s what’s happening in staking or other components, but that’s not what is actually happening in the bitcoin network itself. And so we’re now ten plus years in. And in contrast to something like AI that I use on a daily basis now.

Mike Green

Other than speculative trading, I still am not at all sure what anyone thinks we’re getting out of bitcoin.

Tony Nash

Yeah, it’s not a currency. I mean, we’ve talked about this before. It’s an asset. It’s not a currency. Right?

Mike Green

It is a speculative asset that, in my opinion, remains largely inflated on the basis of a flawed underlying belief system.

Tony Nash

But I think you just don’t get it, Mike.

Mike Green

Yeah, that’s it. No, well, I haven’t done the work.

Tony Nash

And you don’t get it.

Mike Green

And I’ve accepted that I’m not going to make it. So I’m just not sure what else can be thrown at me.

Tony Nash

Right? Not going to make it. Albert, jump in.

Albert Marko

Mean, I don’t even know if I want to jump in here. I’m happy for Mike to take all the blowback that’s coming from all the crypto guys because I’ve taken heat for it for years saying that things are speculative asset and not a reserve currency and all that other Ponzi nonsense that gets spouted out there. And I think Mike is absolutely correct. This is a sell the event type thing. I mean, most likely helping those big clients that hold crypto for exit event.

Mike Green

Absolutely.

Albert Marko

Yeah. But then the whole bitcoin appreciation to $1 million, like Cathie Wood is spouting out there is a belief system like who’s the next bag holder? And having an ETF takes that away completely for these people. So this is know, I can’t really add on to what Mike said. He’s spot on.

Tony Nash

Right. And until bitcoin has a global military presence, it’s really not easy to enforce.

Albert Marko

Yeah, but we can make a joke like that. But that’s actually accurate. And on top of that, bitcoin doesn’t even do anything. It needs government systems to transact, whether it’s the Internet, financial institutions, so on and so forth. So it’s not its own entity that’s living outside of the central system. It doesn’t do that.

Tony Nash

Okay, good. So again, people who are going to hate what we said about bitcoin, we’ll take it on. We’re not going to make it. We’ve already accepted that. As Mike said.

Mike Green

How can you take. Seriously anything coming from a guy who’s drinking coffee, from a little mug that has a little birdie on the handle? Come on.

Tony Nash

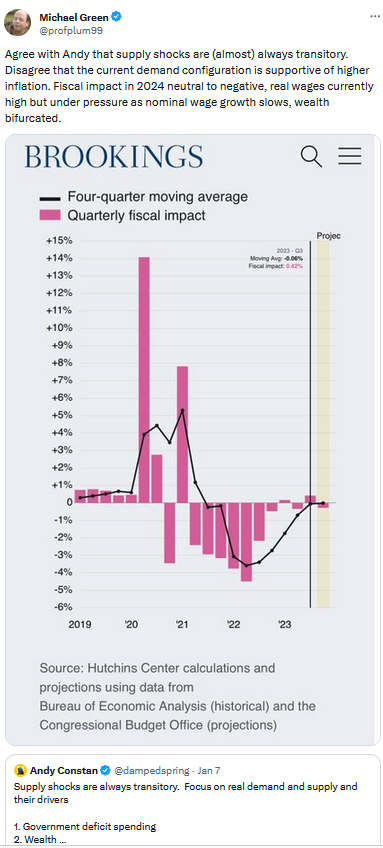

That’s right. Exactly. Okay, very good. Next, I want to hear a little bit about your inflation outlook, Mike. So earlier this week, you said that demand configuration for the US is not supportive of higher inflation and that wage growth presents headwinds for inflation. So do you think inflation stalls out and potentially goes negative for a short period this year? You had this great Brookings graph you sent out. So what’s your thinking? And kind of, I guess also in terms of maybe the timing, where do we hit that point where the headwinds are strongest against inflation in 24?

Mike Green

Well, so there’s a number of things that are going on in terms of the lagged components in the inflation dynamics. Right.

Mike Green

So many people have correctly highlighted the dramatic increases in insurance rates, for example, which are now basically driving all of the increase in transportation services, for example. Those are a distinctly lagged component that’s tied to the dramatically higher costs of vehicles and tied to the higher cost of parts and service.

Mike Green

So if I total my car or if I crash my car, the insurance company has to replace it with an equivalent vehicle. If the price of those vehicles is dramatically higher, guess what? The insurance policy is going to have to increase because the frequency of accidents hasn’t changed.

Mike Green

If anything, it’s increased as Americans have become nuttier and nuttier over the past few years. And candidly, watching my own Gen Z children drive, I’m terrified for the future of the roads and eagerly awaiting the self driving vehicles. So you’re looking at a situation in which what’s happening today in many of these categories reflects asset price changes that happened last year. And as I look forward to next year, what’s the rationale other than an extreme expression of market power, which candidly is likely to be reversed by a variety of regulatory decisions that basically put pressure on the insurance agencies for doing stuff that’s very distinctly unpopular right now.

Mike Green

And I’m not arguing that’s good, but I’m just acknowledging that that’s highly probable. You’re actually looking at a situation where what’s going to cause it to increase by a similar magnitude next year? I can’t really identify why that would happen.

Mike Green

In housing, we’re seeing similar components again. The frequency of burning your home down has not changed to any meaningful degree at the same price that the cost of replacing that home has gone up dramatically. We’ve also seen dynamics of concentration, et cetera, some market power components, but it becomes very hard to imagine that we’re going to see anything that looks remotely like what we saw in the past twelve months, in the next twelve months. And so all of those create headwinds. And the thing that I’m talking about in terms of the configuration for inflation is, remember, when a supply chain disruption occurs, you basically need to recover an element of the lost production, right. If I choose to not replace my car because it’s expensive, I will ultimately have to replace that car. I just want to be very clear. I’m not going to replace it one and a half times to make up for that lost component. I’ve just used my old car, or I’ve figured out how to borrow somebody else’s car over that time period. But there is an element of catching up that ultimately has to happen. The configuration I’m referring to is if you have very rapid population or labor force growth, what that means is that demand is going to rise in the interim period, right?

Mike Green

So not only are you going to have that catch up, but you’re going to have to match that next part. And that’s what was really unique in the 1970s, was every time you encountered a supply disruption, supply would fall 5%. Demand in terms of the number of people was rising in the neighborhood of three to percent five, which meant that you had to make up 10% as much production in order to just get back to the base case. And that is a very different configuration that we have today, where the population is really not growing at all. In particular, the high consumption labor force components are just not growing in any meaningful fashion. And so the headwinds are dramatically less than people are used to thinking about in terms of the dynamics of inflation. So the flip side, the counter to my argument at this point, is many of the cyclical components, things like oil, et cetera, have been under distinct pressure. Those will likely emerge. There certainly will be times over the course of the year, particularly if we’re engaged in combat with Houthi’s and the Red Sea, et cetera. As Tracy has pointed out in our pre conversation, this is going to slow the transit of oil.

Mike Green

It means that more oil needs to be in inventory, which means all else equal, we need more production, et cetera. But those, while they certainly can be a temporary influence, once you start making it around the horn or start making it around the cape instead of going through the Red Sea, once you solve that once, once that inventory is out there and there’s no shortage of OPEC production capability, as you’re well aware, you’ve resolved the problem.

Mike Green

It just doesn’t work in quite the same way. And yes, I know that there’s slightly more use of oil tankers this year, longer in transit, et cetera, but we solve supply problems very easily unless demand is taking off, and we just don’t see any signs that demand is taking off in any meaningful way.

Tony Nash

Right. Okay. So there are two components. One is the good side, which you’ve talked about with crude and manufacturing, and demand kind of more people in the workforce or whatever. I think the other side is the services side. And that seems to be moderating.

Tony Nash

That’s what you’re saying with the wages.

Mike Green

Well, you’re seeing them moderate on two fronts.

Mike Green

So one is that the unemployment rates for the least skilled in our society are beginning to rise as immigration has picked up dramatically and those jobs are increasingly, there’s increasing competition for those jobs. That’s an important component to it. The second is when you have this type of extreme move in services, you actually start something, or shortages in labor, you start something in motion that you can’t stop once it started. And the only other time, I just want to emphasize the only other time we saw a contraction in services employment. And the ISM services employment is a warning sign, in my opinion. When you see a contraction in services employment, that’s a really bad thing because that has been the underlying growth engine of the US economy for the past 70, 80 years, has been the continued share gain of services in the economy. But people forget that that’s coming off of an extremely high level of what we would call marketable activity beforehand.

Mike Green

So we talk about GDP and we think about the sale of washing machines. Well, what did we have before the sale of washing machines? We had services called washer women that would go around and do your laundry for you. What were the 1920s and 1930s all about? They were actually about the introduction of electricity and automation into the home, where many of those services that had been outsourced to low end workers were suddenly productized. And we’re seeing this same underlying dynamic.

Mike Green

How many people, I don’t know if anyone on this call has a robotic vacuum, but that’s a big innovation along the lines of something like a dishwasher.

Mike Green

They’re now incorporating mopping capabilities, et cetera. Our alarm systems are increasingly not installed by ADP or ADT. I’m sorry. You order them from Amazon and you plug them in. Right. All of these services that we have traditionally thought of as being recession resistant suddenly being replaced by products. I actually think this is a really underappreciated and important feature of the current environment.

Tony Nash

I think you’re exactly right.

Mike Green

Same thing, by the way. Walk through a McDonald’s. I mean, go to a McDonald’s, don’t eat the food, but go to a McDonald’s.

Mike Green

And actually look at the difference versus where it used to be.

Mike Green

You now go to a kiosk. You don’t even have to interact with a human being. The labor content in the kitchen, the franchises are gaining versus the local diner because there’s a shortage of workers. There’s been a relative shortage of workers that’s encouraged McDonald’s and Burger King and others to engage in labor saving devices that they can take advantage of but are very hard at this point for the local diner to take advantage of. That’s led to share gain. It’s led to relative price improvement for them versus others. And as those things filter through society, it’s no different than replacing the washer woman with the washing machine. It’s no different than replacing the 37 piece orchestra with a victrola. Right. It’s no different than the radio or the television introducing dramatically more forms of entertainment. But that can be broadcast to everybody else. These innovations roll out very quickly once they hit that threshold and the one that, candidly, everyone’s kind of poo pooing it now, but it’s getting closer and closer. Are things like self driving vehicles?

Tony Nash

Oh, yeah, that’ll be amazing once it happens. I mean, I want everyone else to go first, but viable, I think it’ll be incredible. So I hear what you’re saying on the services low end, and I think that’s fascinating in terms of a lot of those low end services workers. I do keep hearing about how, say, retail stores who’ve done self checkout, some of them are going back and not doing self checkout. That seems like a process that needs some calibration rather than a fundamental kind of reversion back to using people. I just don’t know. But I also think about, and I know this has been talked about for a year now, but when I was with larger research firms and I had to hire an entry level master’s educated, say, analyst, and I’d pay them 70 plus thousand dollars a year, most of that stuff can be done through a $20 subscription for some sort of AI platform now, right? And so it’s the low end, say, customer services jobs. It’s also, I think, a lot of the low end white collar jobs that are being innovated. Are they ready to be fully innovated and fully automated right now?

Tony Nash

Probably not. But we’re at this point, as you mentioned, where that stuff is plausible now. And it wasn’t just two or three years ago, is that right?

Mike Green

Yeah, I think that’s right. I think that’s absolutely correct. And I think, again, this is the inevitable march of technology. Once you create this type of impulse, nobody wants to change unless they’re forced to. Right?

Mike Green

And when you encounter the type of disruption that we’ve actually encouraged, it forces people to rethink business models, it forces them to redesign kitchens, it forces them to make choices that are accommodative for a shortage of labor. And they don’t reverse that when the shortage of labor reverses.

Mike Green

You don’t turn around and you’re like, oh, you know what? A very real example. The push for the invention of the horseless carriage in the 1870s. It led to the prizes to Carl Benz and others for the creation of horseless carriages was created by the great episodic plague that led to roughly a third of the horses worldwide dropping dead in the streets.

Mike Green

When you have that type of event and you end up replacing the horses that are in shortage or creating the technology to replace it, it’s not like suddenly people sat there in 1910 and like, oh, my gosh, look at all the horses around, right? We really should go back to those things, right? Let’s stop using cars and trucks and let’s go do lots of horses. I’m sure people are tempted to do that, but I have yet to see people saddled cowboys on the highways with me. I think people just forget this stuff once it happens, once it’s been sold. It applies to human labor as well as commodities. The cure for high prices is high prices.

Tony Nash

Yep, that’s right. Okay, let’s move on to jobs data and NFP and labor data. And I know this isn’t a new topic for you, Mike, you’ve been talking about it for years, but obviously NFP gets a huge amount of attention every month when it comes out. I’ve got a tweet from 2023, but I’ve seen them from you from 2020 and before commenting on, say, the accuracy or misrepresentation of things like birth death adjustments within unemployment data. Can you talk us through that? Kind of on a little bit of a novice level so that people can understand, because we’re hearing about jobs data.

Tony Nash

We’ve heard about it for the last two years about how things are amazing. And this isn’t a partisan thing because it happened before this administration, but can you talk us through that and how it impacts, say, the unemployment rate and the number of, say, new jobs created, that sort of thing?

Tony Nash

Hey, I’d like to make sure you know that you can access our AI driven market forecasting tool called CI Markets for free, no strings attached, and it does not require any credit card information. Go to completeintel.com/markets to subscribe.

Tony Nash

CI Markets is the perfect addition to your analysis toolbox. This free account includes Nikkei stocks, major currency pairs, and global economics. Of course, we offer much more in our paid account, but this lets you experience CI Markets before making a financial commitment. CI Markets uses the power of AI to help you make better trading investment decisions. It’s absolutely free. Again, go to completeintel.com/markets to subscribe to CI Markets free.

Mike Green

Sure. So what you’re referring to is what’s called the birth death adjustment. This is an attempt by the BLS that was introduced originally, I believe, in 2000 and then reconstituted in 2012 and again in 2020. That attempts to model the new business formations that lead to employment but would not necessarily be captured by survey methodology.

Mike Green

It’s hard enough for most of us to figure out who startups are, add on a layer of government bureaucracy. There’s absolutely no chance they’re going to figure out who they are. So they make an assumption that there’s a certain pace of new business formations that’s occurring.

Mike Green

There’s all sorts of adjustments that are made. And I encourage people to just be very careful in the treatment of the data. The birth death adjustments are non seasonally adjusted. They need to be applied to the non seasonally adjusted numbers. And even when you do that, it’s not really quite as simple as everybody thinks because every month has its own unique characteristics to it. But you can be pretty safe by looking at something like the trailing twelve month contributions to the birth death adjustment. The second thing that’s really important is to remember that the birth death adjustment, this modeling of new businesses, by definition, doesn’t apply to government jobs, right. Because there are new, new governments being founded. I’m unaware of a 51st state. Puerto Rico is trying to avoid it, but there are no new governments in process. Right? So there is no element of birth death associated with it. And so all of these assumptions are tied to the private sector. And so what we’ve actually seen is we’ve seen a dramatic slowdown in hiring from the private sector. We’ve seen a dramatic decrease in new jobs coming from the private sector, with most of the jobs now coming from public or things tied to, like, medical care.

Mike Green

And as a result, it just gets crazier and crazier to be modeling that there’s a constant and continuing increase of new businesses that are happening in the private sector. And this methodology does a terrible job. I actually will just share the chart according to the BLS, right, this is the source of private sector jobs. This is the private sector payrolls numbers x birth death. This is the trailing twelve month net birth death adjustment, which gets rid of the seasonality, as you can see. And one of the features is, post Covid, we supposedly entered into a new era of entrepreneurship, et cetera. But those jobs are now accounting. Those quote unquote, made up, assumed jobs are now accounting for more than half of the private sector job creation.

Tony Nash

Everyone’s side gig while they’re working from home.

Mike Green

Yeah. And there’s also that second component you do have to be somewhat careful of, which is as an economy weakens and people face deteriorating finances in their household, they seek out a second job. And so we’ve also seen a surge in jobs that are secondary jobs, even for those with full time employment, as they effectively attempt to tap into what remains a robust labor market and improve their individual situation.

Mike Green

But as they do that, they increase the supply of labor that’s available, they begin to pressure wages. And that’s really what we’re seeing is that real wages, for all the hoopla about the fact that they turned positive, congratulations really, that’s more tied to falling inflation numbers than anything else. We’re actually seeing nominal wage gains deteriorate fairly significantly, and we’re seeing real wages on an effective basis, adjusting for reduced hours and everything else. Those are basically totally flat.

Mike Green

So there is no growth, there is no growth in employment outside of some government jobs. There is no growth in wages. And that’s stagnation. That’s creating an economy that’s heading into a recession. And I don’t think it’s a coincidence. Obviously, this is a relatively short data series, but when you see this crossover, when you see this slow moving, effectively fixed component become the majority of jobs, they’re not really happening is kind of the easiest way to put it. And I think this is a big chunk of the revisions that we’re seeing, et cetera. We also just saw the household survey, and this is actually important. The household survey just saw a dramatic change, a decrease in full time employment and jobs overall that’s tied to population adjustments. It’s not like the survey suddenly went out and like, oh, look at all these people lost their jobs in December. People tend to underappreciate that. But what that actually is, is confirmation of my concern around these components, because when you restate the household numbers or you do the household numbers, they’re not restated in the same way. The revisions are done for the NFP. It basically is just telling us that the employment gains for 2023 were largely fictitious.

Tony Nash

Okay, yeah, let’s dig into that a little bit.

Tony Nash

We have seen for the last, what, six months? Or is it the last twelve months, the previous prints revised down always. And the way it feels to me is that they’re continuing to shuffle forward, say, 20 to 30,000 jobs. They take it from the past, put it in the future, take it from the past, or take it from the past, put it in the current, take it from the past, put it in the current, and it’s this statistical shell game of moving things forward and then adjusting it down later on. Whether that’s intentional or not, that’s really the way it appears. So why is that happening? If your model doesn’t adjust after a while, you have to figure out what’s wrong with your model, right, rather than just keep continuing to move these things. So what’s going on there? I mean, honestly, to me it appears very manipulative.

Mike Green

First of all, I don’t think it’s actually, and Albert could probably comment on this as well, but I don’t actually think it’s intentional. I don’t think that there’s green eye shade accountants in the BLS who are like, boy, I’m really looking to pump up the numbers for Joseph Biden.

Mike Green

The methodology is really critical here. So the non farm payrolls is an establishment survey where effectively a form is filled out, submitted electronically by businesses saying, we created x number of jobs.

Mike Green

The response rates to that survey have plummeted. They’ve fallen from about 70% pre Covid to today. They’re running in the 30% range. Part of that’s work from home. Part of that’s the fact that people just don’t care as much. Part of that is that there’s no penalty associated with it, so why would I bother? Et cetera, et cetera, et cetera.

Mike Green

When you fail to respond to that survey, the assumption methodology is that those who fail to respond to the survey expanded in the same way that those who responded to the survey.

Mike Green

So you’re effectively taking what had been a 70% response rate and forecasting 30% to get to that 100%. Today we’re taking 30%. And assuming that everybody else is there, that naturally leads to overstatements, because I’ll just be really straightforward. Who’s more likely to respond to a survey? Somebody whose business is going well or somebody whose business is imploding? And so when you talk about the change in the model, the irony is all of these models use what’s called an ARIMA methodology, which is an autoregressive.

Tony Nash

Just a moving average.

Mike Green

Correct. It’s a rolling regression, to be very precise.

Mike Green

And that’s the equivalent of you are driving your car in a straightaway and you see the turn up ahead, you have to start adjusting for it in advance. But if you’re only using your rear view mirror and incorporating the data as it comes, you’re going to be eternally late for that time.

Tony Nash

All they use is Arima. Like, I had no idea it was that simple.

Mike Green

It’s really that simple.

Tony Nash

Oh, my. So. And for people who don’t follow Mike, I’m sure everyone does. But Mike is very good at pulling out and explaining methodologies. So I’m a nerd about methodologies. I’m less vocal about it because it’s really hard to explain. Mike is very good at understanding these methodologies and explaining them in very understandable ways. So if you’re using government data prints, and I know a lot of government data prints are kind of trade the news, but you have to understand the methodology, and you have to understand the issues associated with those methodologies, I trust very few government data prints. Unemployment, retail sales, consumer spending. These are the worst data prints globally. GDP, of course, the worst data prints globally. But if you are not following Mike, look back on his historical tweets. He’s excellent at explaining the methodological issues associated with government data, especially in the US.

Mike Green

Yeah, well, I think that’s. First, you emphasize the right part, especially in the US. The second component is that because I’m not a natural mathematician, it’s important for me to really dig into these things and make sure that I can actually understand what the hell is going on. I think this is one of the challenges. People who are naturally gifted at math, they’ll look at a series like, oh, of course, right. But they often don’t then lead themselves to the question of, well, what does this imply and how does this model differ from the real world?

Mike Green

The model becomes the territory as compared to the actual physical territory becoming it. And candidly, just, I think being old, one of the primary skills that you bring, you can no longer bring computational intensity and speed. You can basically just bring a. Yeah, no, that’s wrong. Right. That can’t possibly fit the data sets that we’re seeing properly. And it would be exactly like an ARIMA methodology, as you’re going into a turn at high speed.

Mike Green

You know, and you have to adjust, and the ARIMA is telling you it’s basically a straight road.

Tony Nash

Right.

Mike Green

No, it’s not. I’m looking at it. Right.

Mike Green

But the second thing that becomes really interesting, though, is that a lot of the tools that we use for leading indicators, things like what the stock market is doing or what the credit market spread, the credit spreads are doing, those themselves have actually been turned into lagging methodology by virtue of the way we choose to invest in them now. So it used to be that you’d have a legion of individual investors or portfolio managers that were directing most of the assets on a discretionary basis. They’d see the data sets begin to change, they’d see things begin to slow, they’d begin to rotate their portfolios into higher cash allowances and into safety.

Mike Green

That became the dominant feature in the market. And as that was occurring, as thoughtful application of those principles was being applied, the stock market was a leading indicator. Today, the dominant flows into stock markets are simply passive allocations from 401K plans. So if you have a job, which is a lagging indicator, you are investing 100% of your normal proceeds into the market, unless you’re in the very rare minority of people who are changing your allocations. And that, in turn means that the stock market has now actually turned into a lagging tool. And as a narrative species, we still haven’t made that adjustment.

Mike Green

So we keep saying, well, what is the market pricing in the market’s pricing? Nothing in it has no idea what you’re talking about. There’s nobody at vanguard paying attention to the apple earnings call. There’s nobody, you know, doing any of this stuff anymore. And candidly, the rest of us have become increasingly nihilistic and throwing up our hands. We’re like, none of it makes any sense. Well, that’s because we’re thinking about it as lagging as compared to an increasingly mechanical tool that reflects the flows that are occurring tied to lagging indicators as compared to leading indicators. This is a super challenging and interesting time period, particularly in developed markets. We’re used to thinking about China data as being garbage, but it’s unusual to think about us data as being garbage. And when it comes out, and this is the last thing I would just say on this, Tony, is your suspicion of the like, it’s an unintended consequence of over indexing on the wrong.

Tony Nash

I want to go into that for a little bit, and I wasn’t planning to talk about this, but when I was working in China, I was talking to one of the data scientists from Baidu, and he told me that they have a better idea of daily GDP readings than the Chinese government does, than the BLS does. And they were considering developing something around like a daily economic activity reading. So I just don’t understand where we have say, I’m going to hate to do this, but Google or all the people who have all of this data, we could actually have a compilation of daily activity that doesn’t take a bunch of government statisticians. This just comes up kind of automatically segmented. Albert, you’re saying, no.

Albert Marko

No, you can do it, but they don’t want it.

Tony Nash

No, they don’t.

Albert Marko

Why would they want sort of transparency like that when they can use the BLS and coal adjustments and anything else to rally the markets or make growth look like it’s positive? I think Steiner from hedge eye went through how the federal and state government single handedly turbocharged the economy in Q1 last year through cola adjustments and other nonsense like the BLS, like Mike was talking about, accounted for 80% of the growth with Yellen and the treasury being 40% of it, and the reality that growth has been negative 20 last year, and we can go through all these government statistics like Mike was talking about. And start shredding them apart. But the reality is, perception is reality with the markets and these algos and, yeah, these algos and traders are just going to take whatever face value number is thrown at them and they’re going to trade it. That’s just the reality of it. No one cares about revisions. Nobody.

Tony Nash

Right. And this is the thing that I’ll just kind of, as a side note, say all the stuff that you’re hearing about company implementation generally of things like AI and machine learning, is just reactive to some of these headline numbers. And a lot of what you’re hearing about, say, enterprises deploying AI, as Mike said with the BLS, they’re ARIMA algorithms, which is just simply a moving average. So very few of these companies you hear about kind of deploying AI are actually deploying real machine learning algorithms. They’re deploying things like ARIMA to decide what their business is going to do. And you can do that in excel. Right now, before we get off of this really bad data, want to. You are notorious for talking about API data. So can you talk to us a little bit about. Because when we talk about, say, market data, that’s market clearing data, right? When we talk about government data, that’s statistically driven fiction. But when we talk about things like API data, that’s supposed to be kind of supply and utilization data. So how is that kind of stuff developed?

Tracy Shuchart

Well, I think, well, API, first of all, if you look at API versus EIA, which is the American Petroleum Institute, which is a private entity, compared to EIA, which is obviously government, if you look at the API data, the thing with that data, that why it’s kind of hit or miss is because it’s not mandatory. So it’s just voluntary reporting to a trade union. That’s it. And so if you don’t have time to report that week, you don’t have time to report that week.

Tony Nash

Okay?

Tracy Shuchart

So that’s where you kind of sometimes get hit or miss. I mean, most people do report to it, but again, it’s not mandatory. That said, it is mandatory to report to EIA. But I’ve been talking about this since, about, since 2020, we’ve seen a huge deterioration in the data because of some of the metrics that they have changed. Right. They had this adjustment and they kept kind of, which is literally a fudge factor. This is how much we plus or minus think we’re off this week because of the increasing amount of NGLs that these wells are producing. And so that number has, and then that number has been wild. Because they really can’t keep track of it. So that fluctuation week to week really is too much of a fudge. Like it shouldn’t be 1015 million barrels a week. And then they just changed the definition again. They fudged it a little bit again in September. And then we’ve seen their demand data has been off by the time they get to their monthly reports. So, guys, I would tell you it’s two months lagging, but the 914 monthly reports are much better as far as data is concerned.

Tony Nash

Okay, so a lot of this has to do with whether it’s the establishment data on labor or whether it’s EIA or whatever has to do with response rates, right? So we’re using, say, survey based methodologies that haven’t changed in, say, 2030 years and expecting that to reflect the market today. So again, as people who watch this use government data, use industry association data, other things that are not market clearing, they have to be aware that there are huge flaws in those data sets and in those responses. Now, Tracy, when you said that EIA changed their methodology, do they then do retroactive changes on the previous data sets?

Tracy Shuchart

No.

Tony Nash

Of course. Mean on some level that makes sense. So, Mike, you were about to add.

Mike Green

I mean, I guess I would just say a couple of things, right? When we say that the data is fiction or flawed, it’s a best attempt, but we tend to forget we look at things like averages. You mentioned a moving average, et cetera, and we don’t adjust those for the standard deviations around that.

Mike Green

So one of the things you’re seeing all over the place is discussions of the presidential cycle and all these components. The reality is that the variance or the variability of outcomes dwarfs the averages.

Mike Green

I can say yes. In Democrat third year or fourth year election years, there’s been outperformance over prior years in terms of the history. But remember, you’ve only got a few of those observations over any meaningful period. When people start saying things like in the data set since 1950. Well, there’s just not that many election years where Democrats were in charge. You just get this incredibly small n, right, which is number of observations, which tells you that the data sets are basically just designed. Like, what people are trying to do is grab your attention with interesting factoids that have no statistical relevance whatsoever. And then we get upset when the data reverses, like, oh, it was manipulated, or it’s just, I’m sorry, that just doesn’t actually mean anything. We’re over indexing on stuff that has no statistical validity.

Tony Nash

Exactly. Okay, let’s move on to looking at some industrial metals. Tracy, I want to talk to you a little bit about industrial metals and what’s happening, but first, I want to have a very quick conversation about what’s happening in Yemen right now, what’s happening in terms of impact on crude price and impact on shipping. So can we cover that real quick? We saw crude prices spike overnight. What do you expect to happen in the short term with crude prices?

Tracy Shuchart

I think that this has definitely put a near term floor under it, but we have to see how the next days and weeks sort of play themselves out. But for now, it’s kind of put a floor underneath it. We haven’t, certainly didn’t see oil prices spike as much as they did. Say when Russia invaded Ukraine. I think we were up like $7 on the day. We were up $3 earlier. We’ve come back down a little bit, so certainly we’re not getting that kind of a reaction, but I think that this is going to keep at least oil prices elevated. Now, the news that did come out this morning, I think that is more interesting is that by and large, mostly tankers have been transiting the Suez and the Red Sea, and it’s mostly been the container shipping market that has been avoiding it. The big MaRisk and all the big players as far as that’s concerned. But we had INTERTANKO, which represents 70% of the world’s oil and gas tankers, has told its members, know for the first time, warn its members that they should stay out of the Red Sea. Now, of course, it’s just a warning, right now.

Tracy Shuchart

It’s not, this is what you must do, but it certainly would make a difference if we started seeing these tankers. By and large, in the amounts that we’re seeing these container ships start rerouting, that will add a whole new dynamic, as in extra fuel consumption, things of that nature that might spook the markets a little bit. And I think that’s part of the reason we’re seeing elevated prices today, not only because of the attack, but because now tankers are being told, we don’t really think you should transit this area. Right. I think that’s probably the bigger news. And again, we’re going to have to see how this all plays out. But keep your eye on the taker market. Certainly even more ships having to go around the cape, adding ten to 30 days, depending on your export hub origination, is going to matter as far as extra fuel consumption.

Tony Nash

Interesting.

Albert Marko

Yeah, but the extra fuel consumption is actually equal to the Suez Canal toll so there’s not really a cost difference, it’s just a timing. And so that’s what I’d have to add to that.

Tony Nash

And so that’s mostly fuel for Europe. Right.

Tony Nash

So could we see a midwinter spike in energy prices in Europe?

Tracy Shuchart

Well, I think the seasonality really starts about mid February anyway, as maintenance season starts. And that’s generally just this seasonal kind of trend in oil. I wouldn’t count on it since 2020 and oil prices went negative and with COVID and the world economy shut down. So seasonality hasn’t been as regular as it has been in the past. But that is kind of when seasonality does.

Albert Marko

There’s also, Tony, there’s plenty of Russian oil floating around Turkey.

Tony Nash

Yeah, there is.

Albert Marko

The Dutch can buy as much as they want.

Tony Nash

Good, good. That’s good to know. Okay, let’s move on to industrial. You know, with rate expectations in the US moderating, we saw industrial metal prices and junior miner valuations begin to rally. I’ve got a chart of copper futures and the Sprott Junior Copper Miners ETF on screen, but we’ve really seen them start to fall off coming into January. Now, of course, today they’re up a little bit, but not as much as, say, crude. When you look at things like industrial metals, what are you looking at right now and how do you look at, say, the junior miners differently than you look at the raw metals prices themselves?

Tracy Shuchart

Well, I think really when we’re talking about industrial metals, to me it’s really an h two story of this year rather than h one. I think it’s going to be a little touch and go here because I personally don’t think that they are going to cut rates in March. Right. And I think that would be probably second half of the year. I could totally be wrong on that, but I just don’t really see that happening. I think the market is getting too ahead of themselves. But generally when you see rate cuts, that’s generally better for metals and for metal miners because their projects become a little bit more affordable. You have to understand these miners borrow a lot of money to get these projects off the ground. There’s a lot of financing. There’s also cost of carry, storage, things of that nature for the middleman when you’re talking in commodity markets. So that’s a very rate sensitive environment when you’re looking at borrowing costs that are so large. And so when you start cutting rates, I think that’s going to ease a little bit of that burden and of their bottom line. Also, we likely see USD to come off a little bit that’s always supportive or tends to be supportive of metals.

Tracy Shuchart

And so I think that’s more of an h two story. That said, if we look at something like copper, I’m very bullish on copper. I think that because of the renewable energy push, because of the mining supply disruptions that are going on right now and not coming back, and because of the deficits in the market supply demand deficits, I think as soon as we see rates come down and the dollar back off a little bit, I think that will be very supportive.

Tony Nash

Okay, now how much of your bullish, say, copper story is dependent on demand in 24? Because if we look at Mike’s jobs chart and the indication that a recession is on the way, how much of that is dependent on that innate demand factor versus, say, the EV growth factor and other things.

Tracy Shuchart

I think obviously that would weigh heavily across markets. But when we look at commodities generally, even when we’ve had a recession, like take 2008 over 2020, because that was a totally different kind of environment. But if you look at 2008 and you look at the commodity sector in particular, metals and energy bounced back faster than anything else in the market.

Tracy Shuchart

Because it’s still relatively inelastic. If you look at the energy sector, people still have to go to work, people still have to take their kids to school or to get the bus, or the nation still has to run, even if you’re. So we definitely see those demand numbers bounce back faster than anything else. And the same with industrial metals because manufacturing still happens and the economy still has to run.

Tony Nash

Okay, good. So there’s a baseline there. Okay. And we also saw China PPI numbers way down last night too, or this morning. So as we see those factory gate prices, that probably put some downward pressure on industrial metals as well, I would think, at least in the short term. No? Is that a factor?

Tracy Shuchart

Yeah, absolutely. Everybody looks at China when you’re talking about industrial metals just because of the giant manufacturing hub that they are. Right. So everybody looks at iron ore, everybody looks at copper, everybody looks at all the basic industrial metals that you need for manufacturing steel, for construction and things of that nature. And so I feel like everybody counts on China to sort of save the whole complex. But we are seeing demand in other places springing up in other asian nations, for example. And in Africa they’re coming up, and in India they’re coming up. So though we’re seeing losses out of China, we are seeing gains in demand in other countries.

Tony Nash

Okay, that’s good to know. Okay, thanks for that. So speaking of potential rate rise in March, Albert, let’s talk a little bit about a very interesting topic around central banks. Let’s talk about the Yellen factor. Okay. So just to cover a couple of central banks first, and then we’ll come back to Yellen. We saw earlier this week some test balloons coming out of the bank of Japan saying they’re going to end negative rates. In Q2, the former policy director said they’re completely ready to end negative rates. So one would assume strengthen JPY, which would be, I guess, interesting. And then at the same time, we had kind of who I think is among the world’s worst central bankers. Lagarde saying that Europe is not in a serious recession, which isn’t really all that comforting since she said serious. So it’s kind of a very nothing to see here moment. And she, of course, said the ECB won’t cut rates until they’re sure that inflation is conquered and all this other stuff. And so I think there’s this assumption that the Fed is really in charge of a lot, not just in the US, but globally.

Tony Nash

And a lot of these other central banks are dependent on the Fed. But we do have a person in the background who seems quite powerful, who knows both the Fed landscape and the US treasury landscape in Janet Yellen. So can you talk us through Yellen’s role, what she’s doing and kind of the power she has not just over the Fed, but over some of these other central.

Albert Marko

You know, I like to limit the central banks to the US and Anglosphere plus Japan, because those are the only really important ones, the ECB. Yeah, sure. But right now they’re in a zombie status for their economy. Lagarde talks about a serious recession. They’re in a depression right now in Europe. But aside from, you know, Janet Yellen has dialog with all these central banks, so does Powell.

Albert Marko

They sit there and they discuss what policy actions they’re going to throw out there. They don’t surprise one another. Nobody does that, especially in today’s interconnected markets. You can’t think that they act independently anymore. Sure, something could happen overnight and they have to act, react, so on and so forth. But when you’re talking about long term policy, know, the Fed and Yellen will sit there and pick up the phone and talk. I know for a fact they do. I know for a fact that they get information and they prompt the Australian central bank to do so on and so forth with their currency, whether they devalue it or raise rates or so on. And so I mean, Yellen, her desire is to keep the US markets elevated. And right now, it’s purely a political thing. And I know Mike’s going to chime in here a little bit later, but from what I know and plenty of people I talked to, it is purely politics in her eyes. Right. So she’s looking right now to use all of the remaining reverse repo for the election, simply for the election going into Q three. Right now, she’s looking to probably do about $1.2 trillion in bills by Q three, which is absolutely massive.

Albert Marko

And the fact that you said that she knows how things work in the Fed and how things work in the treasury, well, she wants to neuter Powell and the Fed and being able to raise rates and offset any kind of market pumps that she has planned. Right now, 1.2 trillion is at least $200 billion more than even the highest estimates that I’ve seen of anybody else. Right. Because the way I understand it works, that she gets her bills Bonanza, and QT is killed because QT is going to end this year. Right. We can talk about what that happens to inflation for 2024, but Mike is right about 2025 and going onwards, that inflation is probably going to taper off in those years. But for the election, I absolutely think that Yellen double pumps this market and gets the narrative that the economy is good simply by using our reverse repo and all these other narratives that she builds through the other central banks globally.

Tony Nash

Okay, so what is she spending that $1.2 trillion on?

Albert Marko

Honestly, that’s above my pay grade. Right. That really is. I mean, I can tell you what they’re doing. When you talk about the plumbing and the mechanics. Mike probably knows way better than I know that she uses investors in the reverse repo as a prime source of liquidity. Not all of it, but a significant. That’s as much as I know about.

Mike Green

I mean, just to offer a couple of mean one, when we talk about it being all political, it’s always all political.

Mike Green

Let’s just be really clear. The treasury does not have a policy statement that mandates their behavior. And so when the treasury is pursuing something, it is explicitly pursuing something in the interests of the administration.

Albert Marko

That’s exactly right.

Mike Green

It’s actually really important for people to understand. There’s nothing nefarious about that. It’s actually very different if the Fed gets involved and begins pumping a political agenda that may or may not happen. And I’m certain that it happens to a greater degree than we’d like to acknowledge. But the simple reality is she isn’t a member of Biden’s cabinet. Her objective is to push Biden’s agenda. That includes getting Biden reelected, in part because the Biden administration sees the election of Trump as one of the most concerning possible outcomes for the US over and above a traditional election type dynamic. Whether that’s correct or not, that is actually above my pay grade.

Mike Green

Because that requires looking in the future and something that we can’t just see. The second component is when you talk about what she’s going to spend it on, I actually think we largely know what they are going to spend it on.

Mike Green

They’ve already told us the inappropriately named Inflation Reduction act is going to continue to push domestication of supply chains, the investment in critical supply chains component. And that’s been one of the key drivers of the better than expected GDP, is that the US trade deficit has deteriorated or has improved dramatically over the past year or so.

Mike Green

So it’s actually like, I do think those things are important for people to understand relative to GDP. We’ve seen an seeing, you know, largely tied to the dramatic increase in oil production in the United States. We’re seeing the know, the US is now the world’s largest oil product producer, bar none. And that’s happening under a democratic administration.

Mike Green

The whole drill, baby, drill type framework actually occurred under. So I think it’s important to kind of identify that. The last point that I think you guys are emphasizing, which is the use of the RRP or the incentive to not fully fund, effectively drawing down non bank deposit reserves in order to fund the payments that go out from the US government. That is a liquidity. And from that standpoint, I think it’s important for people to understand that when you use bills or you use RRP as your source of financing, you’re using an asset that carries effectively zero volatility weight, right? So if I use 30 year bonds and somebody goes out and buys a 30 year bond to provide financing for the US government, they have to be very cognizant that the value of that bond can vacillate fairly significantly. That creates uncertainties in terms of asset values. That reduces my incentive to go out and spend those proceeds or to continue to spend, because I’m now like, well, I’m not entirely sure what my asset value is.

Mike Green

When you use bills, there’s none of that uncertainty. It actually goes even slightly worse. You don’t even need to put out because bills are discounted mechanisms just make life simple. If I buy a one year bond, yielding one year, bill, yielding 5%. I’m paying ninety five cents, and I’m getting a dollar back in the future that is absolutely cash that is being returned into the system at a lower cost to the system than if I had to fully fund a dollar purchase of a 5% bond, for example.

Mike Green

So all of these things matter. I just think we got to be a little bit careful in, like, this is uniquely Yellen or this is uniquely Manukin or somebody else.

Mike Green

That’s always the objective of the treasury, to serve at the pleasure of the president.

Albert Marko

Yeah. Their liquidity analysis is dubious at best. But the US bubble sucks in so much capital at this point that they may be running out of sources. I don’t know. I mean, $400 trillion is a lot of money. A lot of money to jack.

Mike Green

Nobody can do.

Mike Green

Just to be clear. But 400 billion, not 400 trillion.

Albert Marko

Oh, yeah, sorry. 400 billion.

Mike Green

We’ll get there eventually, don’t worry. The Bitcoiners are telling us that

Albert Marko

Doing liquidity analysis on 430 billion is not easy.

Mike Green

Right. I agree with that. And I also think the other component is. Remember that a lot. This goes back to the narrative type dynamic.

Mike Green

When the stock market goes up, we want to explain why.

Mike Green

And so all sorts of liquidity, blah, blah, blah. Well, liquidity can be used to fund lots of things, including money under the know you like. Just be aware that it doesn’t always mean exactly what people think it means.

Tony Nash

So I want to go back to one thing you mentioned, Albert. You said QT is definitely ending this year. So what, $8 trillion on the fed balance sheet? Something like that.

Albert Marko

The fed balance, more like 12 trillion when you take in all the swaps that they got with other banks and whatnot. But on paper. Yeah. It’s 8 trillion. Yeah. You want to use the paper number? Yeah, it’s 8 trillion.

Tony Nash

Sure. Okay. I guess normally around 2 trillion, something like that. Or at least has been for the past five, six, seven years, something like that. So 8 trillion is the new norm, is that what you’re saying? On the fed balance sheet?

Albert Marko

Yeah. I mean, it’s been elevated, been going up every year. We use excuses now, like Covid and Europe in 2012 and so on and so forth. They’ll find excuses to keep the balance sheet up. I don’t even take that even seriously anymore.

Tony Nash

Okay, Mike, what’s your thought on that?

Mike Green

I’m hopeful that Albert is wrong, but.

Tony Nash

Me, too. I’m on your side.

Tony Nash

I don’t know why they couldn’t continue to siphon it off.

Albert Marko

You know why? Because this is a purely political nonsense. This is the reason why inflation stays elevated and high is because the political policies get in the way of economic common sense. That’s why. Right. There is nothing that the Biden administration has ever shown me that they are willing to do something economically logical. That’s why. Right. That’s purely my baseline of reasoning behind all this.

Tony Nash

I mean, in fairness, we could say the same thing about the last two years of the Trump.

Mike Green

Yeah. I was going to say again, to me, you don’t need to assign one party versus another. Right. They both have behaved in economically irrational manners to prosecute their objectives. Part of it is it’s just that we don’t have a good model that actually explains this. I mean, deficits don’t matter. That comes, you know, from the Reagan and Bush administration.

Mike Green

You know, when I come back, I want to be the bond market.

Mike Green

James Carville with the Clinton administration, there is no political allegiance to any of this stuff. Simple reality is sometimes it matters and sometimes it doesn’t.

Mike Green

And it all depends on where you are in a business cycle and where you are in a capacity utilization cycle, et cetera. And that’s very frustrating for people who always want to hear that two plus two equals four, right? Sometimes it does and sometimes it doesn’t.

Albert Marko

Mike, I had a question for you. One of the main thesis I had is it doesn’t matter because Asia and Europe are just non existent at the moment.

Albert Marko

If we had some kind of counterbalance. Then the United States would have some problems. Right.

Mike Green

I totally agree.

Albert Marko

Yeah. Because they’re dead. Asia is dead right now. Right. Europe is. I don’t even know what Europe is. It’s just a vacation club. Sure, Japan’s different. Japan’s a little bit different. But I’m saying China itself, China and Europe are completely dead. For that reason, we have no accountability.

Albert Marko

Right. We can do whatever we want. I’m not saying it’s good, but in the short term, we can do whatever we want. It’s probably going to bite us in the ass ten years down the line. But for today, who’s going to hold us accountable?

Mike Green

I think in general, again, I think that there’s parts of what Albert’s saying that I absolutely agree with. Right. We all know, including myself, the overweight individual, who knows that there’s consequences associated with being overweight but doesn’t want to change their behaviors.

Mike Green

You can tell them that on Tuesday. You can tell them that on Wednesday. You can tell them that on Thursday and it’s not going to change their behavior. And for that matter, they’re going to sit there and increasingly be like, stop nagging me.

Mike Green

It’s only once they have the catastrophic heart attack and they recognize that there are actually distinct consequences. But at that point, their future as an athlete is finished.

Mike Green

There is like no real opportunity there. So there will be eventually a heart attack that hits for exactly the reasons that Albert’s saying. If we continue to make bad policy and basically consume Twinkies for breakfast. But in the meantime, man, Twinkies are tasty.

Tony Nash

Yeah, they are.

Albert Marko

They’re deep fried Twinkies.

Mike Green

Particularly if you deep fry them. Right, exactly.

Tracy Shuchart

And then cover them in chocolate.

Albert Marko

Yeah, exactly.

Mike Green

Right.

Albert Marko

Because we got them.

Mike Green

And at every stage in that process, somebody’s saying, oh, that doctor doesn’t know what the hell he’s talking about. I’m totally fine. Right. There’s no different with political administrations.

Albert Marko

That’s a perfect analogy. It’s like the Twinkie, deep fried chocolate covered Twinkie. Because we have Ozempic. Yeah. That’s not going to stop the heart disease. Right. Make it look good.

Mike Green

Well, the irony is that if you combine Ozempic and the Twinkie, right. You now have increased consumption and you’ve introduced innovative new technologies that you can value richly. And if they’re paid for with government deficits, that shows up as phenomenal to GDP growth.

Tony Nash

Let me ask you, the Twinkie, Ozempic and testosterone shots since we’re goosing the defense budget.

Mike Green

Right. My gut doesn’t look nearly as bad because I’ve pumped up my upper body. Right. Congratulations.

Tony Nash

So on that Twinkie note, let’s just end it on a happy Twinkie note. Okay.

Mike Green

There we go.

Tony Nash

This is great, guys. We could go on for hours. Thank you so much for this. I really appreciate your time, all the thoughts you put into this. Have a great weekend. Have a great week ahead. Thank you very much.

Tracy Shuchart

Thank you.

Mike Green

Take care.