Explore your CI Futures options: https://completeintel.com/futures

In the latest edition of “Week Ahead”, Tony Nash is joined by Daniel Lacalle, Chief Economist at Tressis, Albert Marko, and Ralph Schoellhammer from Webster University in Vienna to discuss the key themes in the market. The trio begins with a discussion on market optimism, macro earnings, and money growth, and how the market participants are overly optimistic despite interest rate rises, bank failures, and persistent inflation. Lacalle highlights the factors that are driving this optimism and provides insights into how investors can navigate the current market conditions.

Moving on, the discussion shifts to the Fed’s stance on interest rates. Albert Marko shares his view that the Fed would likely stay strong given the inflation environment and predicts two more rate hikes. He explains why he expects two more hikes and what it means for the “higher for longer” duration. The conversation provides a comprehensive analysis of the current state of the market and offers practical insights into how investors can stay ahead of the curve.

Finally, Ralph Schoellhammer takes the floor to discuss the nuclear power industry’s future, specifically the differences in approach between Germany and Japan, and other countries. The discussion offers a unique perspective on the challenges facing the industry and the potential solutions that could be implemented.

Key themes:

1. Market optimism: macro, earnings, & money growth

2. 2 more Fed hikes?

3. Nuclear: Germany vs Japan (& others)

This is the 62nd episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

Daniel: https://twitter.com/dlacalle_IA

Albert: https://twitter.com/amlivemon

Ralph: https://twitter.com/Raphfel

Transcript

With CI Futures, you can access AI-powered market forecasting for as low as $20 a month. Get 94.7% market forecast accuracy for over 1000 assets across commodities, currencies, equity indices, economics, and stocks. With weekly updates, one-month and three-month error rates, and top-ten and bottom correlations. You can rely on CI Futures to help you make informed decisions. Join a growing number of satisfied users who have already transformed the way they invest with CI Futures. Don’t wait. Start forecasting with confidence today for as low as $20 a month.

Tony

Hi everybody, and welcome to The Week Ahead. I’m Tony Nash. We’ve got some great guests this week. We’ve got Daniel Lacalle. He’s the chief economist at Tressis. We’ve got Albert Marko, and we’ve got Ralph Schoellhammer from Webster University in Vienna. There’s been a lot happening this week, guys, and I think what we want to start with is Daniel had talked about market optimism and how it may be a little bit off and inappropriate for where kind of some fundamentals and other things are right now. So we’re going to jump into that at the start. Albert’s talked about two more Fed hikes. So I want to see kind of where that is and what he’s thinking and what the conditions are for that. And then for Ralph, we’re going to look at European energy. There have been some movements around nuclear energy in Germany this week and so we want to talk about that and a little bit of kind of the European environment for energy defense, those sorts of things. So guys, thank you so much for joining us.

Tony

Daniel, you had this great video out early this week talking about market optimism.

And I’d really like to kind of get some of your thoughts on that. Where is that optimism now? Is it overly optimistic? Why is it overly optimistic? And where do you think things go from here?

Daniel

Thank you so much for inviting me to start. I think the first thing that we need to understand is that we have gone from a moment in which if you look at the greed and fear index that CNN publishes, we went from extreme fear to extreme greed in less than a month. This was basically triggered by the Federal Reserve’s decision to make whole all of the depositors at Silicon Valley Bank and to implement this incredibly outrageous policy of purchasing at full price the sovereign bonds and the asset base of lenders in exchange for immediate liquidity. So that immediately reversed the reduction in the balance sheet. Federal Reserve Federal Reserve’s balance sheet has basically consumed 70% of the tightening that had happened in prior months. And with that, the market went back to extreme optimism. But interestingly, it has happened in a period in which the earnings season has started and the earnings downgrade cycle has actually accelerated. So we are not seeing it’s not like we are seeing a great earning season. It’s probably one of the worst earning season in terms of sales surprise, earnings surprise is relatively acceptable. However, it comes fundamentally from buybacks, as all of the people that are watching us or hearing us know.

Daniel

So what we are back is in multiple expansion mode and viciously in multiple expansion mode because it started with technology and it started with more cyclical stocks to the point that despite the fact that, after and we will talk about energy afterwards. But despite the production cut from OPEC and the limits to exports from Russia, oil prices are still down WTI 5% on the year. And the energy sector has seen the largest multiple expansion of them all because the earning season in energy is coming with an expected year-on-year first quarter results that will be down between 20% to 30%. Yet the market still seems to be very optimistic about that. So my concern, we’re going to be talking about maybe couple of rate hikes that very few people expect in the near future. And what most people are estimating is that the reason to buy the market in this environment is because there’s not going to be any further rate hikes. Actually, the market is discounted rate cuts in the second half of the year and because the effect of the Federal Reserve balance sheet coming back to the levels where it was prior to the tightening might reduce that liquidity crunch.

Daniel

So I’m concerned about that because the combination of multiple expansion greed and a lack of understanding of the reality of where rates are going to be may create a very significant level of volatility, probably in May, if, as we will probably discuss later, those rate hikes, which I would agree actually happen against consensus estimates.

Tony

Danielle I feel like with earnings season, when we saw banking earnings, certainly for the globally systemic banks, but with some of the regionals as well, there was a huge sigh of relief that oh gosh, it wasn’t as bad as it could have been. And I kind of feel like we’re in that zone in markets where people are like, well, everything’s fine, it’s not as bad as it could have been. Is that kind of where your head’s at, what you’re thinking? And are people positioned for things being great when we just kind of like escaped something? Are people thinking things are really good when we just kind of barely escape something?

Daniel

We need to start by this completely erroneous concept of everybody’s bearish completely. One thing is where people investors are saying in surveys, which is rubbish, okay? And the other thing is where they’re positioned and everybody is positioned for things going great, not going well, going great. And yes, you’re absolutely right, earnings were not as bad as feared. The economy might not get into a recession, but consumer confidence ism PMIs all show a very weak level of growth. So yes, I’m happy to understand why investors would be positioned for a not so bad environment. My concern is that investors are positioned for a hugely positive environment. It’s very cyclical, very involved in the stocks that plummeted in 2022 and therefore getting in those that actually require multiple expansion. So my worry is that the narrative becomes, well, things are not as bad as the doomsayers were predicting. Let’s go crazy. And that’s not obviously.

Albert

One little comment on the earnings season. And the whole not so bad sentiment of the market is how much of that is reliant on inflation? Because a lot of these companies passed on the inflation numbers to the consumers 20, 30, sometimes 40%. But now, as consumers demand destruction has taken hold, those companies can’t pass those numbers along. So how much of those earnings were affected by just inflation tailwinds versus the reality of it?

Daniel

It’s very evident what you just said, and it’s a key element because many people blame corporate profits on inflation, which is stupid, because corporate profits don’t cause inflation. They are a symptom of inflation. But when demand destruction is happening, as you’re saying, then those corporate profits and margins go back very, very quickly and people are not taking into account demand destruction. I would agree with that.

Tony

So when you talk about demand destruction, one of the things I think about is auto loans. Auto loans in the US have really started to look terrible with defaults and other things coming along. I don’t have the numbers in my mind, but I’ve seen this over the past couple of months, whereas we saw in 2021 used cars and auto loans just booming. So to me that’s one indication, especially in the US where people are in their cars all the time, when we start to see destruction in auto loans, that tells me there’s something really concerning about consumers. But what Albert just said about companies passing on inflation to consumers and Sam Rines, who’s here regularly talks about price over volume, where we’ve seen volume destruction at the expense of price rises. Are consumers starting to be tapped out? I see evidence every day of people saying, oh, consumers are tapped out, look at auto loans, look at other things. I see evidence on the other side where people say consumers aren’t tapped out, they have plenty of capacity left. So what are you guys seeing in terms of where the consumer sits in the US and in Europe?

Ralph

I would just add one thing kind of alluding a little bit to what Albert and Daniel said. When we look at the potential rate hikes, and this has been truth in the past as well, but it’s a little bit different. I would argue now is the central banks are not just hiking against inflation or market inflation, they’re also hiking against government inflation because governments try to offset inflation with more government programs, which then of course leads down the road to more inflation. So central banks, and this is probably worse in Europe because they’re the central bank is kind of an external actor for many national governments. So this is a little bit of an additional twist. I mean, this has always been a little bit the case, but I think in Europe this time, austria has been, in a recent statistic, the country with most handouts over the last three years. And this was really it was, quote unquote, “helicopter money”. It was government giving checks. I had it myself. I opened up my bank statement and there it was, the energy bonus, €500. And then there was the heating bonus, €1000. So me adapting my spending behavior according to inflation was psychologically very difficult because I got these extra 500 here, these extra thousand there. So that makes it also, I think, harder to get inflation down because the central banks have to react both to inflation from the market and inflation from central government.

Albert

Yeah, but let’s differentiate central banks versus economic policies versus the political realities where these politicians need to be reelected so they’re more than willing, for short term gain to sacrifice long term outcomes.

Daniel

You bet they will. Absolutely. Yeah. I think that the reason why the consumer is behaving relatively in a more positive way than what many would have expected comes down to the fact that we still have negative real rates and that credit is abundant. And if you look at Europe, consumption in real terms is down in absolute terms. If you look at GDP of the eurozone, you look at the part that’s the consumer the only reason why consumption was slightly higher than zero was because the GDP deflator is lower. The inflation print, which is the typical way in which governments boost GDP. The GDP inflator is lower than the real inflation rate. So the nominal number adjusted is actually coming higher in real terms. But I think it’s basically because of credit. For example, with employees and with people that work with us, we find that a lot of people are finishing the month taking short term credits, and that’s a sign. And the reason why they’re doing it is because they believe that inflation is going to come down dramatically very quickly. And that’s not what is happening. What we’re seeing is a deceleration in the pace of growth, which is very different.

Tony

So, Daniel, in this environment…

Albert

Real quick, Tony, real quick. I’m glad that you said that, Dan, because Daniel because that’s one of the Fed’s tools now is calling up the banks and telling them to restrict credit and tighten that way because there’s no real liquidity left in the market outside of corporate and the financial sector. So their plan on tightening involves bank lending and stopping it, of course.

Tony

So the capping off the transmission mechanism or one of the transmission mechanisms, which right now just makes things harder.

Tony

CI Futures is our subscription platform for global markets and economics. We forecast hundreds of assets across currencies, commodities, equity indices and economics. We have new forecasts for currencies commodities and equity indices every Monday morning. We do new economics forecasts for 50 countries once a month. Within CI Futures, we show you our error rates. So every forecast every month we give you the one and three month error rates for our previous forecast. We also show you the top correlations and allow you to download charts and data. You can find out more or get a demo on completeintel.com. Thank you.

Tony

So Daniel, where do you, since there is this optimism in the market that remains and seems to me that it’s people trying to eke out that last kind of, that last trade right before things maybe head down. How would you recommend people take a look at this in terms of positioning or strategy or something like that?

Daniel

Well, the first thing that I would do is to tell everyone that is being told that “now is the moment to buy long duration in bonds” is not to fall into that trap. The second thing that I would do is to avoid the view that commodities are going to go through the roof because monetary contraction, fundamentals matter, but the biggest fundamental is the quantity and the cost of money. And, and if monetary contraction is going to continue, commodities may not fall, but certainly not go through the roof, which is what many people expect. And I see a lot of people betting on one thing and the opposite. And we discussed this this morning with my team, how on the one hand, people are betting on energy commodity prices going through the roof, buying emerging markets, buying commodity linked assets, and at the same time betting on inflation coming down very quickly. What the hell are you talking about? So I would make people sit down with their portfolios and say, okay, maybe I’m wrong, but at least don’t bet on one thing and the opposite. Don’t bet on inflation coming down at the same time commodities going up.

Daniel

Don’t bet on central banks normalizing, and at the same time buy long duration assets. I think that all those things are the ones that worry me. So I would avoid long duration bonds, I would avoid ultracyclicals, and I would stick to stocks, to be fairly honest, I would stick to gold. And I always like to have US dollar exposure, because when the market corrects, having US dollar exposure gives you the cushion to look for opportunities. And we need to be, I have to start with this. We need to be 100% invested all the time. We don’t come in and out of the market.

Tony

Very good.

Albert

I think that’s important. That’s the key point. I mean, I talk to a couple of Eastern European governments all the time, and they talk about the de dollarization nonsense. And I always tell them you have to have dollars in your reserves just to combat hyperinflation. That’s just the reality of the story. No matter what some cockamania financial analysts want to talk about there’s no such thing as the dollar station if you want to combat hyperinflation.

Tony

Great points.

Daniel

I agree with that.

Tony

Great points. Okay, let’s move on to Albert.

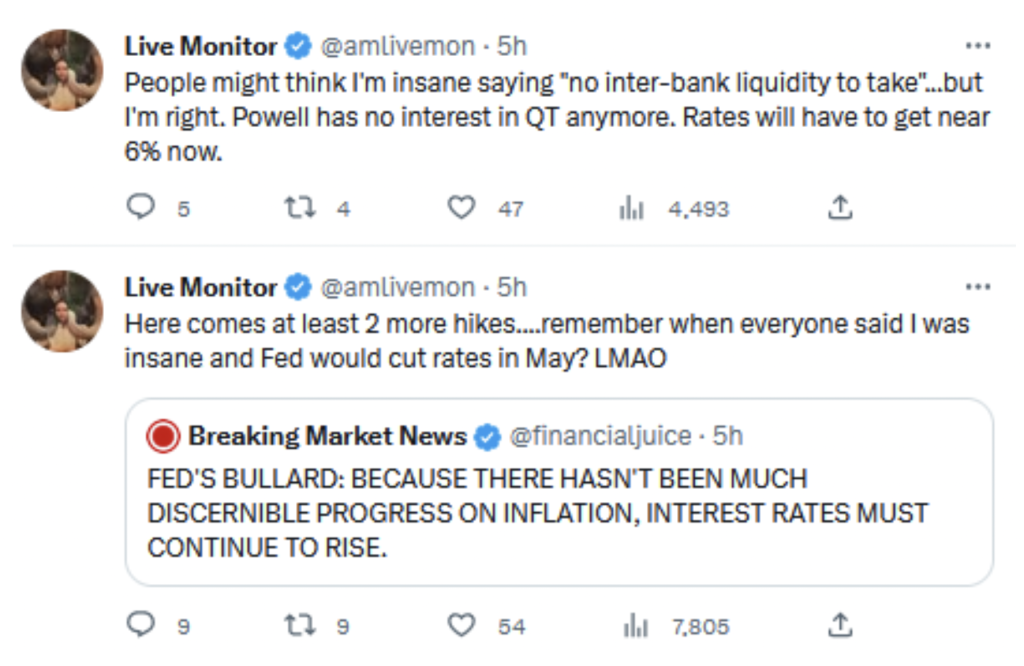

Tony

Albert, you had earlier this week sent some tweets out about Fed hikes.

And I think the conventional view right now is that we’ll see one more hike, one more 25 basis point hike in early May. You’re contending that we’ll likely see two more. Can you kind of talk us through some of your thoughts there on why that’s happening and what some of the impacts will be?

Albert

It’s really basic. It’s the inflation issue. It’s not going away at the moment, and Europe being in a zombie status, China opening up in a staggered sense and slower than expected. Inflation still hasn’t come down. Forget about the top line numbers that you see in the media and the politicized number that goes out everywhere. But if you look at SuperCore and core inflation, it’s trending up again. It’s not coming down. Since a lot of the central bank’s tools have been already expended, the only thing they have left, really, is rate hikes. And for that reason alone, I think that we’re looking at at least well, one for sure in May, but we’re probably looking at at least another one after that, at the very least.

Tony

Okay, and then Daniel talked about how stimulating the banks has really kind of offset a lot of the QT that had been done over the last year or so. Do you see any movement on the Fed to tighten their balance sheet, or are they kind of just in this holding position until there’s 100% confidence that the banking system is stabilized?

Albert

The whole banking crisis was completely, in my opinion, falsified. I mean, they needed something to stop QT, and they got it. They unwound nine months of QT in a week. It was absolutely stunning to see that. And this is why you actually see a lot of the people in the market talk about, no, this is the new QE. This is New QE. No, it’s not QE. It’s just the stopgap measure and trying to place status quo until they hope that inflation stabilizes in the next three to six months. However, I don’t see that happening. I think that we’re looking at probably at a secondary inflation event, not as high as it was last year, but marginally higher from this point on.

Tony

Okay, so when we see rates rising, say, another 50 basis points, and we see banks not lending, and we see some of these credit issues coming up, how does that impact things like housing? We continue to see house prices stay pretty stable, actually.

Albert

The problem that we have is, although the banks are tightening from the West Coast of the United States and New York Fed, but the middle part of America and southern part of America, the banks were still lending. I mean, you can still go out in the housing market and still see an appreciation in prices in housing at the moment, right? You don’t see that in New York, you don’t see that in California, but everywhere else in the United States, it’s happening. So the problem I see is that it’s a patchwork. They’re trying to do a comprehensive policy for tightening specifically the housing and consumer markets, but it just doesn’t work because it’s so fragmented at the moment. You can’t tell banks not to make money after six months. It’s just not going to happen. I mean, they’re going to find ways to give loans out to people because they’re banks. They rely on margins.

Tony

Right. And you also mentioned SuperCore and kind of the inflationary aspects of that. What are you seeing on wages and what will slow down wage growth, especially in the middle of the US.

Albert

Nothing. I mean, the tourist season is upon us now in the United States and also coming up in Europe, and I don’t see wage inflation slowing down one bit. And this is actually something that Janet Yellen and Brainerd wanted. They wanted wage inflation because it’s politically advantageous to them.

Tony

Okay, so the Fed is looking at SuperCore. Wages aren’t slowing down. Wages are a big contributor to that through services prices. So it feels like we’re in this continuous loop that just doesn’t stop. What is that? Is there kind of just no end to this or at least for the next, I don’t know, six months or something?

Albert

This is what we’ve talked about numerous times on this podcast, is this doom loop of, like, Fed policies and then political policies intermixing and muddying up the waters, and you just get an inflationary loop over and over again. I mean, nothing’s been actually fixed. I mean, the supply side okay, a little bit. It’s come back online to a marginal degree, but like I said, European in a zombie status. They’re not even really opening. I mean, manufacturer is not opening in Europe again. China is staggered in their opening. So we’re just going to get this doom loop until political policies start coming back into more realistic terms.

Tony

Okay, so, Daniel, you had mentioned something about May around some events potentially happening in May. So with more Fed rate hikes, do you expect markets to take a bit of a turn in May?

Daniel

I think so. I think that if all these things that we’ve just mentioned are absolutely critical because it’s the opposite of what the average of the market thinks. The average of the market thinks that inflation is coming down dramatically and that, yes, core inflation is rising, but core inflation lags by they invent these things that core inflation lags by months with headline inflation. It’s something that has been completely she just gets so angry as an economy. No, the reason why core inflation is rising is because all those secondary effects of the previous inflationary wave are building in the economy, and ultimately the money supply growth is coming down, but money supply growth continues to be above real GDP. In May, you will probably have a few things now. To start with, the base effect that has given these headline positive numbers on inflation fades Away, because basically everybody oh, inflation is coming down. Yes, of course, over a 9% number. The second one is that right now there is this very optimistic view about the global growth. I find it amazing to see that the Chinese slowdown, that the Chinese recovery being virtually in existence is not something that has created more headlines.

Daniel

In fact, it’s rather the opposite. And the stagnation that Albert was just mentioning is something that is not embedded in people’s estimates. People are estimating 3% growth for the global economy with the Eurozone escaping recession with a one and a half percent growth, the United States not entering into a recession, despite all of the indicators that we have mentioned before. So all those things tend to happen between May and June because also, if you remember Tony, is that a lot of people that sell the bullish argument for the economy always talk, every year, the tale of, oh, but from June onwards, it gets better. Okay, so people do the back half of the year.

Tony

The back half of the year in every economy is the back half of the year.

Daniel

It’s a tale of two of two years. I’ve been an investment banker as well, but with the point that I’m trying to say is that for those first five months, there’s a lot of confidence in that story. But then reality bites and we see consumption stagnant, growth stagnant, persistent inflation. And central banks have only one tool, which is rate hikes. They’re not tightening the balance sheet because they can’t. So this is like the Pringles advert once you pop, you can’t stop.

Tony

Yeah, it’s interesting you mentioned 3% growth. My view of these IMF releases the world economic outlooks. They’re PR. They’re not necessarily solid economics. And our view has been, is China going to grow at 5.3 or whatever? The IMF is saying no. Is the US. Going to grow at 1.8 or whatever? No. Our view is the US. Is going to grow maybe at one kind of right around there. Q2, Q3 are going to look really difficult. And so we do get these kind of pump pieces out of the IMF saying, and they always say global growth is going to be better unless the prevailing sentiment is totally negative. Then they’ll be really bearish just to align with that. But these are really PR pieces, more than solid kind of economic outlooks. Is that kind of your view?

Daniel

It’s absolutely spot on. The IMF has hundreds of top-notch economists looking at all sorts of models and analysis of the economy. But ultimately, and I’ve worked with a few of them, ultimately, when they have to put together the estimates for the world. Each country goes to each of the analysts and says, “wow, come on, you’re not going to put 1%, it’s going to be 2%.” And what are they going to say? “Okay, fair enough.” Have you ever seen a government say, we’re not going to grow this year? Never. So the IMF has, interestingly, a tremendous level of predictive capacity of recessions, but never predicts it publicly. Predicts them publicly because as you said, it’s hugely diplomatic. So that’s why it’s always a downgrade of growth story. And now what they do is that we have to do with the CFO and C meeting is that we have to read between the lines. And what they do now is that they maintain the polish argument, but they give sort of subliminal messages about weaker things here and there. And it’s usually buried between page 20 and page 30 of their release. And between page 20 and page 30 of their release, what you have is that credit impulse is plummeting in developed economies.

Tony

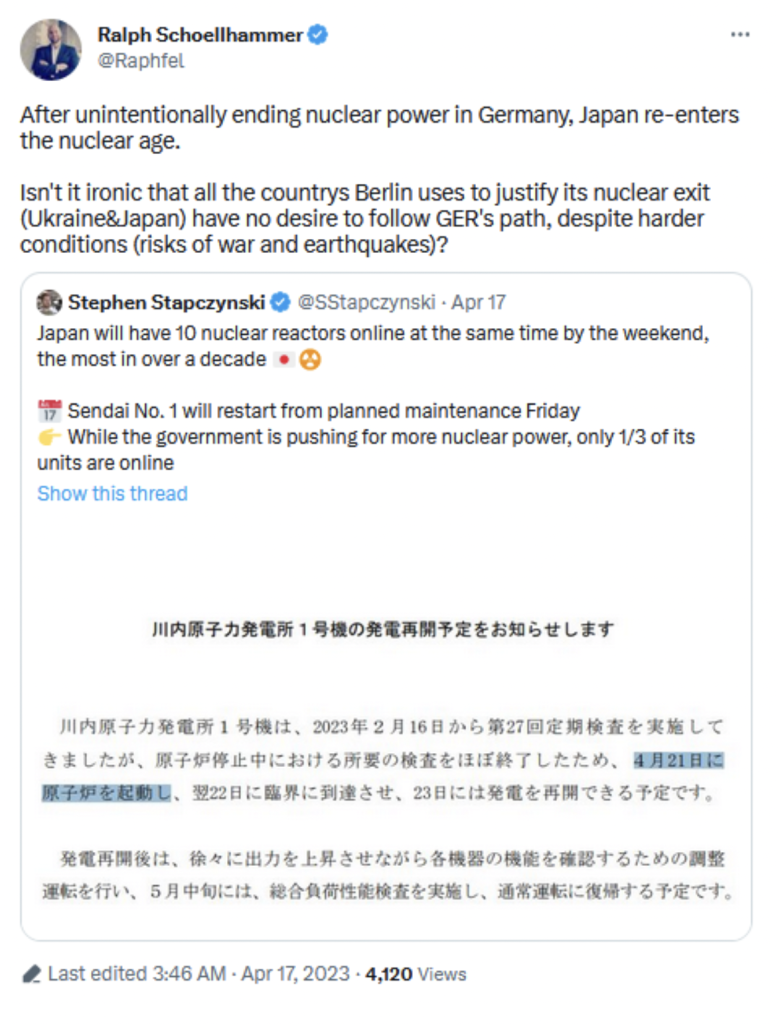

That’s right. So far, very happy show, very optimistic show, guys. I just want to thank you for that. It’s been awesome so far. So, Ralph, let’s move on to Germany and energy in Europe. So the Germans announced this week that they’re halting or that they stopped their nuclear plants.

Tell me about that. Why is that happening?

Ralph

Well, they did, right? So this was on April 15, they shut off their last three nuclear power plants. So Germany is, at the moment of us speaking here, is a nuclear power-free country. I mean, inside the country, Europe has an integrated electricity grid. So they still on occasion get plenty of nuclear energy from the Czech Republic and from France. But Germany has left the world of nuclear power. And that’s of course the problem. It’s an integrated grid. So some people pointed out, why is everybody making such a drama out of this? Germany was a net electricity export the last year. That is all true. But this is the problem. So it’s not just a problem for Germany. It’s a problem for the entire energy situation in Europe. And just to put a few numbers on this, at the moment the average megawatt hour in Europe is still about twice as much as the average megawatt hour in China. So that is a problem for manufacturing. And if you take the United States, you have this absurd situation that in the shale patch, right? The oil production has natural gas as kind of a side product.

Ralph

So they literally have to burn natural gas because they don’t know what to do with it. So natural gas prices are down. So to quote Emmanuel Macron, he wants to make Europe the third superpower. But if we look at energy prices in these hypothetical three superpowers, Europe is at the dead end. Energy here is still much too expensive. And if we look at the manufacturing sector versus the service sector, the service sector in Europe is not doing so bad at the moment. It’s even expanding, but manufacturing is suffering. And some and I think those people are not entirely wrong, would say that manufacturing is in a recession and it makes a lot of sense. And we kind of enter now what Albert mentioned, we enter this doom cycle because now you have in Germany and other European countries this idea, “oh, this is not a problem.” We’re going to make a special industry energy price where the government guarantees a specific price per megawatt hour, but the government guarantees a specific price for the access to energy. But that energy still must come from somewhere. Currently you have the German energy minister and the chancellor traveling all the coastal cities in Germany because there’s a lot of local resistance against new LNG ports.

Ralph

But those LNG ports are the promise how they’re going to solve the problem of having abandoned nuclear. So a lot of the things that are supposed to replace nuclear are things that are currently in planning that haven’t materialized yet. So I would argue that for the foreseeable future, whether we will call it an energy crisis kind of overdramatic, but there’s definitely going to be a lot of pressure on prices in the energy market because energy production, whether it’s electricity or other areas, is not keeping up. Will there be a shortage? I don’t think there will be a shortage. Europe is still rich enough to buy it, but it’s going to be more expensive. And that price is going to end up one way or another on the bills, on the monthly bills of the consumers.

Tony

So I had dinner last night here in rural Texas with two Germans and a Belgian, and I was asking them about this.

Ralph

That’s the beginning of a great joke.

Tony

It is. It really is. But when I asked them about started asking about energy and nuclear in Germany, they said, we’re going to stop here and we’re only going to give yes no answers because they were so annoyed by the policy and so annoyed by kind of just how crazy some of these decisions are. So it sounds to me like it’s kind of just a nod in my backyard, a NIMBY type of deal where Germans don’t want nuclear energy in their country, but they’re happy to take energy derived from nuclear, not their countries.

Ralph

Not not at all. That’s what the really frustrating thing about the story is. The majority of the German population is by now this was not the case five, six years ago, but by now, after the energy crisis of last year, a majority, according to the most recent polls and I think Tracy talked about this in one of the most recent episodes of The Week Ahead as well. A majority is now pronuclear. There’s even now an idea that the German states, Bavaria particularly, they want to keep them running. They want to basically buy them from the federal government and keep them running on their own. And even for that there would be a majority. There is a broader issue. Albert tends to allude to this, and Daniel also kind of talked a little bit about it when he talked about kind of politicians or certain forecasters, not necessarily saying the truth. In the last decades, the economic expansion and the globalization under US and Germany was so comfortable and ran so well that we could afford to have very unrealistic politicians and elect them into office. And with the Greens in Germany, that is the case. But now we have kind of a reassertion of reality.

Ralph

And I think many governments, I would argue also in the United States, struggle with that. And I don’t mean this to be facetious or provocative, but we also have a problem in recruitment, let’s say in civil service. And these.

Tony

Oh my gosh.

Ralph

Bureaucracies in some areas they are good, right? Finland, I think, is very well managed. Denmark does a pretty good job. So there are some that are well managed. But areas in the United States, the major powers at the moment, like France and Germany and Europe, they have a problem. Their bureaucracy is not what it was in the course my favorite time span in the 19th century. And they still live off the capital. They still have their reputation, right? When you say Germany, you think about clean streets and a well run bureaucracy and all these kind of things. But we saw during the COVID Pandemic something that Tony and I we talked about before the show, that it was not that well run like the Germans, for example, the way they communicated throughout the country, the numbers of infections, they did it via fax machines because the entire health system was not fully digitalized.

Ralph

So that is a problem that’s a little bit under the surface. But given a world, let’s say that is where politics becomes more important because countries are becoming more risk averse and kind of very often want to hedge their bets. I think some countries are not at the moment in a position to do that because we have neither the politicians nor the civil service to do this. I mean, just a quick example, no offense towards the United States.

Tony

Be offensive for the US. It’s okay.

Ralph

If you look at Congress, I mean, you literally have people that are either demented or at the brink of dementia or who had recently had a stroke. Nothing against these people personally, but that’s a luxury you can afford when everything is going well. I think that once somebody said we’re rich enough to be stupid, I think we’re no longer that rich to be that stupid. And I think that’s going to be a bigger problem. I know it’s a little bit metaphorical, but I think that’s going to be a bigger problem going forward.

Tony

No, it’s true. I tell people all the time, our people in congress and in the federal government. They’re all like, 124 years old, and they just can’t relate to people who actually work. But we elect these people. I don’t understand why. European Bureaucratic in Aptitude. I’d like to introduce you to Washington DC. Because Europe is perfect compared to what we have in DC.

Ralph

And it’s there’s one thing I think Albert is going to love this. I don’t know if it’s true, but supposedly in this leak document from last week, it turned out that two thirds of employees at the Pentagon are under 30 years old. And one would argue that at least in some ways, if you look at foreign policy and diplomacy as it is conducted, again, also by Europeans at the moment. Right.

Ralph

I think there is a lack of skill. There is a lack of fine tuning. Again, I don’t think that these are bad people. I don’t think they do it because they’re ill intentioned. I think they simply do not have the required skill set.

Tony

But let me push back on that a little bit. If they’re young, at least they have a stake in their future. When we look at US politicians who average 124 years old, they don’t have a stake in their future. Okay? They’ve been in these roles for decades. And honestly, will they be around in five or ten years to deal with the ramifications of their policy? I just don’t believe they are, and I don’t believe they care.

Albert

Yeah, Tony, but the problem is they don’t have the experience and they’re ideologically biased. This is the problem when you start working in diplomacy, is you have to be very fluid and very gray area, and a lot of people aren’t. Whenever you take a position based on your political ideology, it hurts things. I mean, look what Blinken did in Brazil and Colombia. Shifted them over to the left, and then now they’re sitting there talking, damning, the United States at the UN for perpetuating wars and stuff. Like I said, when you lack experience and overly politically biased, it’s a problem in diplomacy, it’s on both sides of the aisle.

Tony

Yeah, absolutely.

Daniel

It’s the worst combination. You have 120 year old people in the leadership positions that don’t want change, and you have all the ground staff and the people that are doing the work that are less than 30 years old and that have been told that two plus two equals 22, and that the money making machine will solve everything. So I’m like, oh, my God. The condemnation. However, I will say one thing in the defense of the United States, the massive bureaucratic machine doesn’t weigh more than 50% of the economy in the European Union.

Ralph

It does. Oh, yeah.

Daniel

And what you were mentioning before is scary because think about this. You have a massive energy crisis. You have the evidence that you have to rely more on, that Germany had to go and suddenly depend more on late night on coal and massively import energy from the United States. We have been saved in the eurozone of a massive recession by an extremely mild winter. Despite having all the luck and understanding that you have made a massive mistake, you double down on the mistake. This is the same, by the way, it’s happening in Spain, it’s happening in Italy, where they’re trying to completely overrule the shareholders decision on the major utility company. And you’ve mentioned a critical thing is that you cannot expect the European Union to provide growth and manufacturing improvement with those levels of energy costs. Today’s, PMI manufacturing PMI is at 43 month low after the next generation EU, massive monetary and fiscal expansion and all the subsidies you could imagine to industries, as you very well mentioned.

Tony

So it feels like we’re facing a bit of a hangover. So this is kind of a very doomy episode, guys.

Albert

It’s the free money policies that’s been around for decades. And everyone thinks, especially the younger, under 30 people, they listen to Bernie Sanders and say, oh, everything should be paid for by the government and this and that. But they don’t want to talk about the ramifications 15 – 20 years down the line. They see money now and that’s it.

Tony

Right? Yeah. Okay. So, Ralph, you and Albert talked about US DOD, and we had a viewer question come up on Twitter when I talked about this episode, asking about Europe paying for NATO and Europe paying for their own defense. And the question said the Trump administration tried to get Europe to pay more of their NATO costs, and the Biden administration is trying to get Europe to pay more of their NATO costs. Is that something that will ever happen? Will Europe ever pay their own way fully of their NATO costs?

Albert

Well, go ahead.

Ralph

With few exceptions, right. Poland does Greece, of course, for different reasons. Greece does because they feel threatened by yet another NATO member in the form of Turkey, which has a certain irony to it. And I think there’s two Baltic states to do as well. But, yeah, I agree. I agree with Albert. You see, it even there was all this excitement about Sweden’s joining NATO, but one of the first things the Swedes said was, well, but we’re not going to meet the 2% of GDP target before 2028, which means when the new government is probably going to be in power. So they’re already pushing this forward to the next government. And Albert also tweeted about this. Even in Germany, they asked the parliamentarian in charge of the armed forces, and she said they haven’t seen her words, like I’m quoting here, “we haven’t seen a single cent of the promised additional 100 billion for the titan vendor.” The time change. So this has been in Germany, at least a lot of this has been talk, but not much have happened. And even if you look at European military spending, for some of them, not all of them.

Ralph

But again, if you take Germany and some others, if you subtract pensions and wages and all these kind of things, the kind of money that really goes into military readiness is very small. I always argue this always gets me a lot of hate, but I argue I think the United States should make I don’t know what the English word for this is but a kind of cold turkey for the Europeans and say, we have provided defense for you long enough. You have the economic power. You can provide it for yourselves. As Albert well knows, and I’m sure Daniel as well, from the occasional Twitter fight, there are so many Europeans who claim we are on the US occupation and Macron means we are the vassals of the United States. All right? I mean, if we are that good as Europeans, if we can do it on our own, I think the Americans should call our bluffs. And then there will be a rearrangement, right? Poland will become more important. Germany will become less important unless they step up their game. But I think this idea that if you tell Europeans the Americans will always continue to pay, you create zero incentives for the Europeans to pay more.

Tony

Right?

Daniel

But even if you do say the Americans are not going to pay any, the problem in Europe is that that ship has sailed, is that people are still going to think that we are going to get the level of security that we have out of thin air, that you don’t need to spend in military. That problem is not easy to solve. The only way that I see it is that if the United States looks at it as a vendor financing scheme, as in the sense that it continues to provide the support for the military in NATO, et cetera, and quid pro quo, that means opening agriculture, automotive, et cetera, et cetera, of all of those hyper protected industries in the European Union. The problem, from my perspective of the United States policy, is that it continues to pay for NATO and all the military spending and continues to allow, one by one, each of the US presidents, the European Union, to enter into bigger and bigger and bigger protectionist measures under the disguise of environmental requirements.

Albert

I’ll make this quick, Tony. Europe has a decision. Either they fund their military or fund their social programs. They can’t do both. And if you want to win an elections in Europe, you cannot cut social programs. As simple as that.

Daniel

Okay?

Tony

I hear that. With such a large gray cohort in Europe, can they continue to pay for those social programs? Do they have wage earners who can pay for that? Is there too much of a demographic issue? So is it not one or the other, but is it neither of them? Right?

Albert

Well, the problem is then you start talking about best swap lines and the political aspects of those things keeping Europe afloat. That’s where that comes into.

Ralph

I think that we again have the problem, and I do it too, but I try always to kind of get myself to stop doing it. We talk about Europe in very general terms, but to give you one example, in Sweden, for example, the retirement age is directly tied by law to average life expectancy. So in Sweden, automatically the retirement age goes up if life expectancy goes up. Now, as you see in France right now, it’s absolutely impossible. This is a little bit due to the unpopularity in many areas of Macron, but it’s basically not possible to increase the retirement age from 62 to 64, which is absolutely necessary just to make it somewhat viable. I mean, I would argue that’s a problem all Western nations in a sense have. I mean, at some point because in the United States the whole debt ceiling debate is breaking out again. But at some point Medicaid and Social Security will need one way or another to be reformed because that also cannot go on forever. But Daniel said, I think another very important point, and that always bothers me in these debates both about so called multipolarity and dedolarization, there is this idea that all of this could hypothetically happen and yet nothing would change.

Ralph

It’s mostly Europeans who talk about this. You have Europeans who say other new multipolar world and the dollar will be replaced, but none of this would be great for Europe. In a sense, I’d rather be the European Athens to America’s Rome than to be some province squeezed between the Middle East, the US. And China. That both economically and militarily is not as strong as we might like to be. But as Albert pointed out, we’re also not willing to put the money would have to go in order to be that powerful.

Tony

If you had to put a probability on the latter scenario, do you think that’s probable? Do you think that’s 40% probable that Europe becomes squeezed between China, US and Middle East, given where things are going?

Ralph

Well, I think what we got to increasingly see is the EU will always remain as, “always” I take that back. Will remain as an institution for long because as you all know, institutions and bureaucracies have a tendency to perpetuate themselves. But what we, for example, saw last week when Romania, Bulgaria, Slovakia, Hungary and Poland announced that they going to basically ban all imports of Ukrainian agricultural goods into their countries. This was in direct violation of an authority that was given legally to the European Union. And the EU has a quasi free trade agreement, particularly in the area of agricultural goods, with Ukraine. So what they did was they basically ignored one of the key competences of the European Union and the European Commission. And I think we’re going to see this more often in the future. So the EU will remain in one way or another, but I think there will be certain areas where countries occasionally go it alone. And what we also then, and this is going to depend on the United States, but there are already talks, whether they’re going to be fruitful or not, to something else, whether the United States should refocus, let’s say, more on Poland as their main partner in Europe, whether they should focus more on Central and Eastern European countries.

Ralph

So I think there is something is going on. I cannot yet say what exactly, how it’s going to end, but something is going on in Europe. And this started in 2004 with the expansion towards the east because that was a new kind of countries in many ways good, but definitely different from the Western European Union as it existed. And I think this is increasingly more difficult to keep together.

Tony

So maybe Blinken will adopt a very Rumsfeldian view of old and new Europe.

Albert

Maybe don’t hold your breath on that.

Tony

Guys. Gosh, this has been such an optimistic discussion. Thank you so much for your time. I really appreciate it. Seriously, this has been really informative. I can’t wait to see what happens over the next week with regard to some of these things, Daniel, especially with your market kind of optimism. So, guys, thank you very much for your time. Have a great weekend and have a great week ahead. Thank you.

Daniel

Thanks a lot.

Ralph

Thank you.