“The Week Ahead” episode combines the wisdom of Tracy Shuchart, Chris Berry, and Corey Lavinsky, as they explore peak oil, battery technology, and biofuels. Tracy shares insights from the recent IEA study, predicting peak oil around 2028. Though oil demand may decline, it won’t vanish entirely. The talk shifts to electric vehicles (EVs) and Tracy’s reminder that their power source in China is still primarily coal, underscoring the significance of considering the energy mix behind EVs.

Transitioning to EVs poses challenges, particularly with grid infrastructure. Tracy stresses the need for substantial investment in grid systems, particularly in the United States, to support the surging demand for EVs. China and India boast differing grid systems with potential for growth, albeit with their respective hurdles.

Chris Berry adds his perspective, emphasizing the crucial role of raw materials in battery production. Securing a sustainable supply of lithium, cobalt, and graphite becomes vital to meet the surging demand for EV batteries. The hurdles of domestic sourcing and the time required for new mining operations are discussed.

The episode unravels the complexities surrounding the energy transition and the multitude of factors shaping the energy sector’s future. It highlights the need for a holistic approach that encompasses technological advancements alongside infrastructure, grid systems, and raw material supply chains, all critical for sustainable energy solutions.

The episode further delves into battery metals’ impact on battery affordability and supply chains. Chris discusses the price volatility of battery metals, particularly lithium, and their limited influence on battery economics. Lithium prices fluctuate significantly but constitute a small portion of the overall battery cost. However, the concern lies in potential price hikes of metals like nickel, which could disrupt supply chains and pose challenges for automakers and battery manufacturers. Managing price volatility necessitates battery chemistry innovation and metal substitution.

Regarding lithium sources, Chris clarifies that lithium is not scarce and can be found in multiple locations, including North America. However, refining processes, mainly conducted in China, pose supply chain bottlenecks. The urgency to secure raw material access surfaces, exemplified by General Motors and Ford investing heavily in lithium projects. Partnerships between American and Chinese companies underscore automakers’ concerns about potential supply shortages and the need to secure critical metals for battery production.

The discussion discusses the conflict between climate goals and the North American mining permitting process. Tracy highlights the protracted and burdensome permitting process, hindering climate goal attainment. Chris raises the issue of coal’s use in nickel production for EV batteries, contributing to carbon footprints. Environmental impact considerations extend to mining, refining, and transportation within the supply chain. Alternative solutions like lithium-ion battery recycling and direct lithium extraction are explored, yet acknowledging their own CO2 footprints.

Shifting gears, the dialogue focuses on refining’s role in corporate mining investments. While Liontown concentrates on mining, Lithium America’s plans include refining. Presently, China dominates the lithium refining industry, with most raw materials sent there. Chris mentions upcoming lithium refineries in the United States, aiming to lessen reliance on China. The discussion culminates with Tony suggesting using biofuels for transporting lithium, potentially mitigating the CO2 footprint.

In another segment, Tony engages Corey in a conversation about biofuels and the recent EPA announcement on biofuel mandates. Corey reveals that biofuels are derived from biomass or organic matter, predominantly ethanol in the United States. Biofuel sources range from corn, sorghum, and sugar cane to biodiesel derived from fats and recycled oils. While biofuels presently represent a small fraction of diesel and aviation fuel markets, their growth prospects are promising.

The dialogue explores biofuels’ potential in aviation and the challenges posed by electric-powered long-haul flights. Corey highlights biofuels’ remarkable growth in the United States, propelled by the Renewable Fuel Standard program, which has fostered ethanol and biodiesel production expansion.

The EPA’s biofuel mandates encompass various categories like renewable fuels, biomass-based diesel, advanced biofuels, and cellulosic fuels. Corey discusses the reduction in proposed mandates for corn-based ethanol, causing discontent among biofuel companies. Biomass-based diesel mandates exhibit sluggish growth, despite substantial investments in renewable diesel and sustainable aviation fuel facilities.

The episode delves into biofuels’ current state and future prospects, specifically focusing on ethanol and sustainable aviation fuel (SAF). Tony initiates the conversation, underscoring conventional fuel production’s plateau and potential Midwest disappointment due to sluggish biofuel requirements. Corey envisions a reduced demand for ethanol in gasoline-powered vehicles due to increased electric vehicle adoption. However, he views SAF production as a promising opportunity for the industry. Corey highlights ethanol’s potential as a SAF feedstock, enabling aviation decarbonization. Tracy raises concerns about SAF’s cost for consumers, prompting Corey to mention existing SAF mandates in Europe and planned future mandates in the United States. Limited SAF availability stems from technological development and the absence of past SAF mandates. Corey predicts increased SAF production as airlines enter offtake agreements with renewable fuel producers.

Lastly, Tony moderates a discussion with Chris, Corey, and Tracy on near-term opportunities in battery metals, biofuels, and oil. Chris emphasizes battery technology advancements, specifically advancements in cathode and anode formulations. He spotlights the intriguing investment potential in the refining aspect of the battery supply chain. Corey accentuates ethanol’s utility as a sustainable aviation fuel (SAF) feedstock and outlines federal and state incentives propelling SAF facility advancements. Tracy highlights how some traditional oil refining companies invest in biofuels, noting that oil and gas industries differ from mining metals, oil, and gas. She reveals that many oil companies remain unaware of alternative energy sector developments, allocating funds to avoid falling behind. Chris adds that historically, oil and gas companies hesitated to invest in battery metals due to the limited market size, but changing political dynamics are now driving exploration into such opportunities.

Key themes:

1. Peak Oil in 2028

2. Batteries

3. Biofuels

This is the 70th episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

Tracy: https://twitter.com/chigrl

Chris: https://twitter.com/cberry1

Corey: https://twitter.com/biofuelslaw

Transcript

Tony

Hi everyone, and welcome to The Week Ahead. I’m Tony Nash, and today, we’re joined by Tracy Schucart from Hilltower Resource Advisors, Chris Berry from House Mountain Partners and Corey Lavinsky from S&P Global.

Tony

I want to take the opportunity really to talk about energy. We’re going to talk about peak oil with Tracy. We’re going to talk about battery technology and battery minerals, metals with Chris Berry, and then we’re going to talk about biofuels with Corey. So really excited about this show so we can get really deep in one sector.

Tony

Before we get started, I’d like to take a second to talk about our subscription product called CI Markets. CI Markets is our AI platform that forecasts stocks, ETFs, commodities, currencies and economics on a weekly and monthly basis. Stocks include the S&P 500, Nasdaq, FTSE, Nikkei as well as the top 50 ETFs. We forecast over a twelve-month horizon and we show one- and three-month error rates, so you understand the likely risk associated with our forecast data. Subscriptions to CI Markets start at $20 a month and you can find out more at completencel.com.

Tony

So guys, thanks. I’m really excited about this show.

Tony

Tracy, I want to talk a little bit about peak oil. There was this IEA note that came out last week saying that we’ll see peak oil around 2028.

They said demand for the chemicals industry will continue to drive oil demand, but demand for transports will shrivel. That was their wording. So 2028 is pretty soon, and it seems like a really quick time frame to change oil consumption. So can you talk to us a little bit about this IEA study and just tell us what some of the key takeaways are?

Tracy

Yeah, absolutely. So first, IEA estimates that global demand reaches 105.7 million barrels per day in 2028. That’s up 5.9 million barrels a day compared with 2022 levels. But really what they said is growth is to flow from there, not decrease. So it’s just the rate of change or the rate of growth is to decline is what they are saying. So they’re not actually saying that peak oil demand. That said, like all of the other forecasts, I do think this is wishful thinking more than anything. And they did, as you are correct, they did include a caveat which included biofuels, petrochemical feedstocks and other non energy uses, which is up to a broad interpretation really, if you kind of work through this report, the only expected growth decline is in Europe and the United States and with increases elsewhere led by China and India. And given that if we look at this study, europe has 742,000,000 people, that’s 9.27% of the global population. North America has six, 4 million. That’s 7.55 million portion of a global population. So really that’s not a lot as a whole, considering there are 8 million people on the planet and many of which are in emerging economies where fossil fuels are necessary to reach levels above poverty.

Tracy

I mean, if we look at Africa, for instance, we have 600 million people alone in that country without electricity, and they’re going to need fossil fuels for a very long time. In addition, again, I can bring up China and India because both of them are expected to increase their consumption. Even if, adding in renewables, their consumption is set to increase together, their population is much larger than Europe or the United States.

Tony

Okay, great. So it sounds like it’s really a both, and it’s not just kind of fossil fuels or, say, renewables, it’s a both and kind of way going forward. But it doesn’t sound like oil is going to collapse in 2029 or anything like that.

Tracy

Correct.

Tony

Okay, so they talked a bit about transports and how much are EVs impacting the expectations around Ice vehicles. So you talk about India and China as being the big growth vehicle. So are EVs, let’s say, in India, going to displace ice cars?

Tracy

Not at this juncture. Not even close. And yes, in China, it’s huge growing industry. However, that’s not their main driver, because if you look at what is powering, their ice vehicles is coal because coal is their main power source. And so you have to take that into account when you’re looking at these things. Oh, yeah, China is the biggest growth in EVs. But what is powering the EVs? Where does that electricity come from? That electricity is basically still coming from coal, along with a mix of hydro, natural gas and crude oil. If we look at the United States, as far as feasibility is concerned, biden administration says he wants 50% of US EVs by 2030. We’re currently at 12%, and we don’t even have the chargers or the grid to even support this. So I have to still go ahead and say a lot of these initiatives are fantastic, but realistically, in seven years, it’s just physically impossible to get to 50% EVs even if people were forced to buy them. Right.

Tony

So we look at guys like Ford who’ve talked about losing billions of dollars this year, and they lose tens of thousands of dollars on every vehicle. And Chris, I want to get into this a bit with you in a second, but we’re not close to that goal yet and it seems very difficult. I want to go back just a second and talk about grids. So, Tracy, again, you talked about India and China. And can their grids sustain the EV growth that’s expected in those countries? Because we have difficulties with grids here in the US. Right. Sustaining. EV. Plugins. So is it first of all, can we hit that here in the US by 2035? 50% just on the grid alone? Second of all, what about India and China? Do they have the grid that can sustain EV growth?

Tracy

Well, we’re talking about two different grid systems, right? If we’re talking about the US. Or we can even include EU in this scenario is that we have particularly aging grid system, right? So really, to realize the goals and I’ll just use the United States as an example, to transition, we’re going to need to build we’re going to need to add over a million miles of transition lines, which first of all, there’s no money in the budget for that. Nobody wants to do that. We’re already hitting over 70% of our current lines are more than 25 years old, and the rest are well into their 50 year timeline. So we have to completely redo our grid system to meet these 20 30, 20, 35, 20 50 goals. And simply no government wants to spend that. And it’s just not in the budget for that right now. So, realistically, it’s just impossible for us to really get there. Now when we go to China and India, right, they’re more of, well, India is an emerging market. I can argue that China may or may not be anymore, but that’s besides the point. But they can grow their grid system because it’s not as advanced or not as mature as our grid systems are.

Tracy

And so, sure, they can add a lot of capacity as far as renewables is concerned, but that doesn’t mean that they’re giving up their power mix. I mean, coal is still really huge in India and China, so it’s natural gas. Hydro is really big in China, which is renewable. It’s easier to transform a country’s grid that is just not aging like ours are.

Tony

Yeah, I would add that I think a lot of the regulatory environment here in the US. Makes grid build out a little more difficult. Maybe Chris or Corey, you guys know more about that. But in China, it’s pretty straightforward. I think they can really build their grids out wherever they want in India, actually, from a regulatory perspective, really complicated. So I think it’s not that easy in India to build out new power lines, to take new real estate to make that more robust. So some of these things, I think, are going to be difficult. I think people will innovate the way around it. I don’t know how they’ll do it, but I think it’s going to be difficult to build out that infrastructure in some of these places. Chris, do you have any thoughts on that?

Chris

Not so much on the infrastructure side. I mean, I certainly agree that that is a limiting factor when we talk about electrification. Whether or not it’s a million miles or whatever it is you use, just from an EV perspective. I mean you use four times as much copper in a single electric vehicle that you do in a traditional or comparable internal combustion engine car. And so my angle on all of this really comes a little bit less from not so much the policy side of the infrastructure side, but where are all these raw materials going to come from? The lithium, the cobalt, the graphite and I’m happy to get into that here in a couple of minutes. I know that’s kind of the topic here, but the infrastructure is certainly, maybe, in my view, a secondary limiting factor or a lack of the infrastructure. But in my view, before we even start thinking about, okay, where are we going to build these lines or the charging stations, or what have you? Where are we going to get the millions of tons of lithium or millions of tons of copper. If we’re talking from a domestic perspective here, when it takes ten plus years to build a brand new mine in the United States, So those, I think, are some of the initial issues.

Chris

And again, we can get into some of those details for sure.

Tony

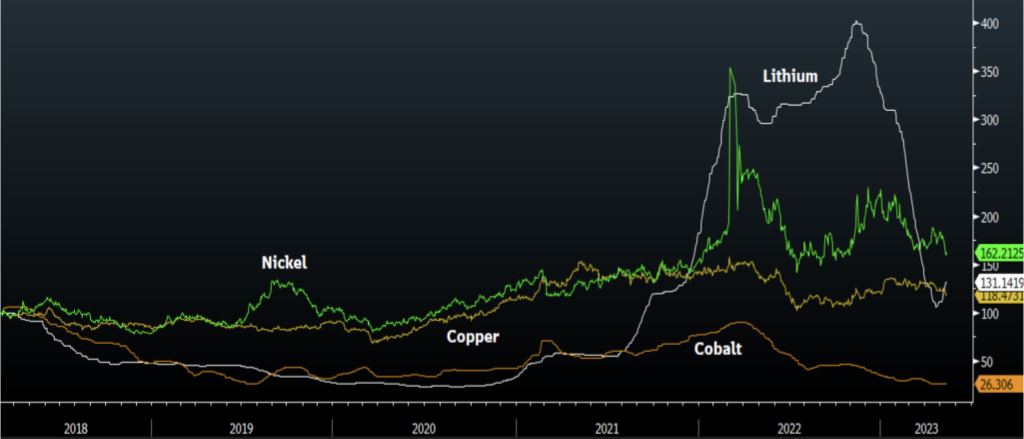

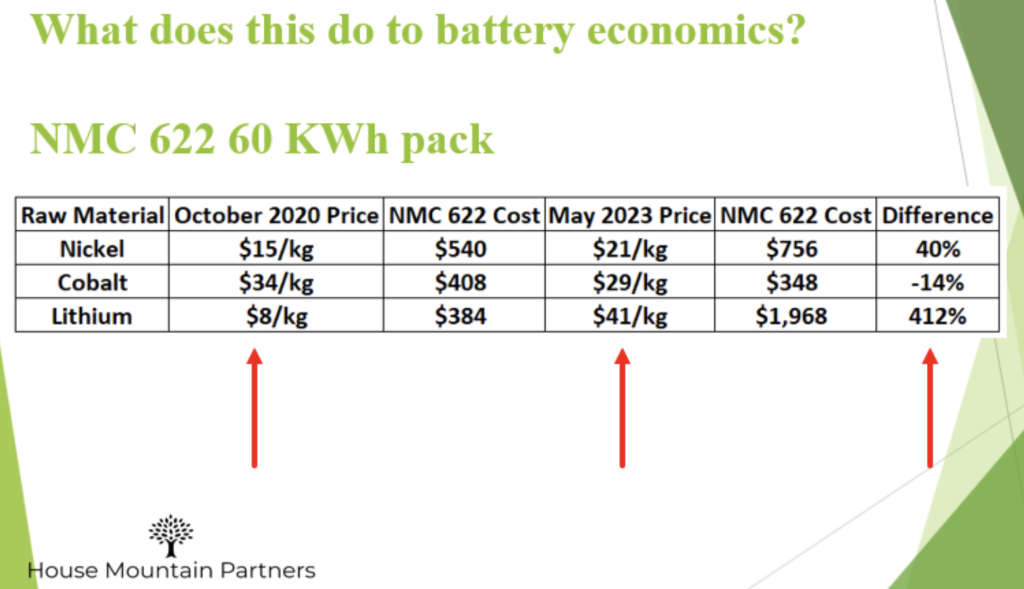

Great. Okay, let’s do that. Let’s jump there. Tracy. Thanks for that, by the way. Chris, obviously, batteries are a growing share of energy for transports, and you talk about the availability. I also want to talk about the affordability of some of those battery metals. So can you talk us through where, I guess prices first, before we talk about supply, where have those prices been? We have a chart showing nickel, copper, coal, and lithium.

Where have those prices been? How does that impact the overall battery prices? And I guess most importantly, what’s impacting the way companies are investing in their supply chain? So I guess let’s talk about price and availability at the same time. That would be really interesting.

Chris

Sure. I think when you think about the price impacts of the battery metals on lithiumion batteries, it’s a relative discussion. In other words, you sort of need to think about what has gone on with lithium, what has gone on with copper, nickel, cobalt, manganese, graphite, sort of the big Six, as I like to call them. And in the chart that I had sent over from Bloomberg, basically what it does is it looks at what I call the Big Four. Big four battery metals. And I stretched the chart back to early 2018, and the reason why I did that was that was the peak of the last battery metals cycle. And so it just gives you, as the viewer here today, an idea of what I think we’re just seeing, the tip of the iceberg of which is battery metals, price volatility. And there are a number of reasons for that that we’ll get into. But I think, again, we could spend all day long talking about specific metals. Lithium is clearly the bell of the ball, for lack of a better phrase. That’s the one that gets all the press. And there are reasons why you have seen so much lithium pricing volatility.

Chris

Again, back in early 2018, what we call battery-grade lithium carbonate hit a price of around $24,000 a ton, up from historically, around $6,000 a ton. And then things kind of went to sleep. The cycle ended in 2019. COVID came and sort of froze everything or allowed everything to restart, I guess, depending upon how you think about it. And then, as you can see from the chart, things have absolutely exploded. Lithium went from about $8,000 a ton to a peak of about $85,000 a ton, and then crashed down to around 22. And now it’s sort of on its way back up. It’s at about $45,000 a ton on a spot price basis today in China.

So to your point, Tony, what exactly does that do? Okay, well, the interesting to battery economics, the interesting response there is with respect to lithium, it really doesn’t affect battery economics all that much. Okay? The price of lithium in a full electric vehicle battery, really, even at a price of around $80,000 a ton, was about maybe twelve or 13% of the cost of that battery. So not enough to really make these automotive manufacturers say, wait a second, this isn’t affordable, or this is unaffordable.

Chris

The issue is, and this is what purchasing managers at Ford and General Motors and Tesla and BMW are all worried about. The issue is what happens when lithium price goes crazy. Nickel price goes to $100,000 a ton. Everything sort of goes up in the air. It’s very, very difficult to manage. So what that has forced automotive manufacturers and battery manufacturers to do is really innovate, I should say, around battery chemistries, and think through, okay, what is truly irreplaceable, what can be substituted, and quite frankly, the only metal here that can’t be substituted without making some very, I guess, significant issues with respect to performance is lithium. Okay? You can use less nickel, you can use zero cobalt again, et cetera, et cetera. And so, from the standpoint of mobility, again, whether or not we’re talking about cars, trucks, buses, scooters, I don’t think anything is going to challenge lithiumion from a market share perspective for the next ten to 15 years. Okay? It’s a much more interesting conversation when you think about what we call long duration energy storage. So putting batteries in with solar farms and so on and so forth, there’s a lot of competition over there, and again, a lot of it has to do with price and performance.

AI

With CI Markets, you can access AIpowered market forecasting for as low as $20 a month. Get 94.7% market forecast accuracy for over 1200 assets across stocks, commodities, currencies, equity indices, and economics. With weekly updates and one month and three month error rates, you can rely on CI Markets to help you make informed decisions. Join a growing number of satisfied users who already transform the way they invest and trade with CI Markets. Don’t miss on another opportunity. Start forecasting with confidence today for as low as $20 a month. Visit completeintel.com markets to learn more.

Chris

Go ahead. Sorry.

Tony

Yeah. With lithium, we hear maybe I’m misunderstanding, but like China and Chile or something, are the two big sources of lithium. Is lithium in other places? And what other places are there? There’s this perception that it can only be sourced from a limited number of places. What are the bottlenecks there?

Chris

So the bottlenecks are in the upstream, in the mining and the refining. And so lithium can be found either in traditional hard rock sources, primarily in Western Australia. There’s a lot of it in Africa, too, and then traditional Brine sources. You may have heard of the Lithium Triangle, which is, if you’re looking at a map of South America, where Bolivia, Chile, and Argentina sort of converge, there’s an awful lot of lithium. About 50% of global lithium comes from that part of the world. So the interesting thing about lithium is that it’s not rare at all. Again, you could actually extract lithium from seawater if you wanted to. I wouldn’t recommend it because it’s very difficult and costly. But my point is, lithium is not rare. The issue with China, and China isn’t even a major lithium mining source at all. They only produce around 13% or mine, I should say around 13% of lithium globally. And just for the sake of perspective, today lithium is about a 900,000 ton per year market, okay? So compare that to copper at 24, 25,000 tons a year. Excuse me, but the issue is the refining. In other words, taking that raw material, whether or not it’s in the form of liquid Brine or the hard rock concentrate and producing, converting it into what we call battery grade lithium salts, either carbonate or hydroxide.

Chris

Now, about 65% of that happens in China, okay? And then as you go further down the supply chain, when you think about the cathode of the battery, so nickel, manganese, cobalt, lithium, iron phosphate, these different chemical formulations, about 65% to 70% of cathode is produced in China, about close to 100% of the anode. The other side of the grephidic side of the battery is produced in China, and they also have a lock on battery production, overall cell and pack production. So this is one of the things that I think the Inflation Reduction Act is designed to try to counteract over the course of the coming years. But again, coming back to my original point, if we do want to compete with China and sort of level the playing field, the one thing that really isn’t addressed in all this legislation is where will the raw material come from? There is no sort of streamlining of mining permitting or anything like that in the Inflation Reduction Act, and that is one pretty significant limitation, quite frankly.

Tony

So are there lithium sources in North America? I mean, would it be possible to mine it in North America, 100%?

Chris

Absolutely. Again, lithium is not rare. I live in Washington, DC. Now. I used to joke when I lived in New York, I could get a shovel and go to Central Park and start digging, and eventually I would find trace elements of lithium.

Here’s a perfect example. And this is maybe a good way to tie in what corporate America or the OEMs are doing. And so, look, the automotive manufacturers, Ford, General Motors, just to use them as an example, finally woke up, I think, and realized, okay, we are going to have to produce electric vehicles whether we want to or not, regardless of the economics, to Tracy’s point. And so they should have been making multimillion or multibillion dollar investments in supply chain development 5, 6, 10 years ago. And so they’re just doing that now. And got a couple of examples. So General Motors has agreed to invest about $650,000,000 in, I should say, a development stage lithium project out in Nevada run by a company called Lithium Americas.

And so, again, I’ll just cut right to the chase. The bottom line is the lithium that is being produced today is pretty much spoken for. Okay? The question becomes, if we are going to get to 50% EV penetration or anything even remotely close to that by 2030, you need to be making those upstream mining investments today to try to accelerate that.

Chris

And so the interesting thing about that General Motors example is that that mine probably won’t even be in production before 2026. And so it just, I think, speaks to the desperation on the part of General Motors to say, listen, we are willing to pay a very large sum today in this high risk mining environment for the chance to negotiate for offtake by 2025 or 2026.

Tony

Okay, so looking at this graphic, you’ve got Ford with Lion Town. I guess that’s a lithium investment as well.

Chris

Yeah, Liontown is a development stage hard rock lithium mining company development, meaning they’re not in production yet. But again, I think it just speaks to maybe I don’t want too much hyperbole here, but the desperation or the focus on the part of these automotive manufacturers, they finally woke up, probably again, five years too late, and realized, hey, we have a raw material problem. We can get our hands on the intellectual property to build batteries or build gigafactories or what have you. And of course, you’ve got the Department of Energy and the Inflation Reduction Act providing a pretty strong tailwind there. But what good is building a gigafactory or a recycling facility if you don’t have the feedstock for it? And so, again, there are nuances here that we can get into in terms of accessing that feedstock. But all of these players that you see on the screen, again, see a lot of General Motors and Ford and LG Chem there. They’re just very concerned right now about raw material access. And again, it goes beyond lithium. I mean, you can see in the lower right hand corner there ford Valet and Hawaiia Cobalt. Interestingly enough, you’ve got an American automotive manufacturer entering into a multibillion dollar nickel sourcing deal with one of the largest Chinese cobalt players in the world.

Chris

So it just, again, is a sign of, I think, how worried these OEMs are about. They see the tea leaves or the winds shifting or whatever the phrase is, and they don’t want to get left behind.

Tony

Right.

Tracy

I had a question.

Chris

Sure.

Tracy

Okay, so we already know that we have a permitting process problem here in North America. It’s not only in the United States. Canada is facing that same issue as well, where it takes ten years to even get the permit, basically. And so in what ways or how do you think that climate goals are in conflict with sort of this process? Right? We already know we need these metals. We already have this red tape that already existed before. This is like an old problem. Right. And so now we have these climate goals, which is adding to the problem. How do you see this panning out?

Tony

Basically?

Chris

Yeah, no, it’s not a comfortable conversation, quite frankly. And I’ll just give you a perfect example. I mean, when you had talked earlier about China and coal growth to feed the grid, indonesia is going to be one of the largest nickel producers. They already are one of the largest raw nickel ore producers in the world today. They’re expanding capacity there dramatically. And in terms of what is the energy source to build these mines and operate these mines, it’s coal. So all of this nickel that is going to go into these millions and millions and millions of electric vehicle batteries is going to be coal fired. And so you have to take to your point with respect to climate goals and thinking about how green the process is. You have to take that into account. And that’s kind of the uncomfortable part of the conversation. And so a lot of my inbound calls coming from investors are, we understand, like, there’s commodity price risk, there’s ESG risk with mining. Mining industry, quite frankly, doesn’t have a sterling reputation when it comes to hitting things on budget and on time. And so what else is out there?

Chris

What else could feed or should say plug any kind of structural gap in metals demands, number one. And number two, do so in such a way that you hit these ESG goals, which again, are very, I think, fluid in some ways. And so I do a lot of work in lithiumion battery recycling and do a lot of work in a certain type of lithium extraction called direct lithium extraction. Again, don’t want to get too much into the weeds today, but even those processes have their own CO2 footprints. And so, at the end of the day, I sort of look at this as, like, the paradox of green growth, which is everybody wants to decarbonize, and we want to have clean cars or a clean grid or whatever. It is. But there is a price to be paid to get there in the first place, and you’re just not going to do it through recycling or innovating with battery technologies. It’s going to take a lot more raw material, and that is going to have kind of a basic carbon footprint that needs to be accounted for.

Tony

Hey, Chris, before we move on, when you talk about these corporate investments and supply chain investments, it looks like a lot of this stuff is on the mining side. Are these say lithium America’s. Lion town. Are they refining as well, or are they only mining?

Chris

Excellent question. Liontown’s intention is just to mine. Okay. Lithium america. It’s an interesting question because neither of them are in production today. And so we just have to rely on their feasibility study and their stated plans. So lion town is a hard rock asset, or they’re developing a hard rock asset in Western Australia. Their initial intention is just to mine the concentrate, the hard rock concentrate. Where will that go to be refined into battery grade salts? It’s going to go to China, probably.

Tony

At least initially, like we’re going to mine it here, ship it to China, have it refined and send it back.

Chris

This is the issue with well, again, the fact of the matter is the Chinese has spent the last ten or 15 years building a consolidated lithiumion supply chain. I’m not saying it’s going to take us ten or 15 years, but we have the mining issue to think about. We have the refining issue. And to be honest, you could get a lithium refinery here in the United States. And there are actually perfect example, tesla and Corpus Christi, they’re building a lithium refinery company here on the slide, piedmont Lithium. They’re actually building two lithium refineries, one in Tennessee. Again, the source of the feedstock is kind of an open question there, but nevertheless, these companies are going to build these refineries in the next three or four years. It’s much easier to permit midstream to downstream portions of the supply chain than it is the mine. But, yeah, again, think about a lithium molecule, right. Maybe it comes it’s mined in Western Australia, it’s concentrated there. It goes to China, where it’s turned into battery grade salts. Maybe it then ends up in Japan, where it’s turned into cathode. Maybe then it goes to Fremont, California, where it’s put into a Tesla.

Chris

I mean, the journey of a lithium molecule has a rather significant CO2 footprint associated with it. And again, this is, I think, what, the inflation reduction act. And a lot of this legislation, this kind of near shoring or friend shoring legislation is designed to do is to minimize the CO2 footprint. But, yeah, it’s kind of a long winded answer saying some of these guys are going to refine and some of them aren’t. But at the end of the day, for the foreseeable future, everything’s going to go through China.

Tony

But if that lithium was transported with biofuels, Corey, it would really help that CO2 footprint.

Corey

Right. Nice segue, the same thing.

Tony

Thanks, Chris. Thank you. I really appreciate it.

Tracy

That segue was excellent.

Tony

Corey, hey, thanks for joining us. There was a big EPA announcement on biofuels this week, and I want to understand what all of that means. I’m not an expert here at all. So can you please tell us what is a biofuel?

Corey

Sure. A biofuel is a fuel that’s derived from biomass or organic matter. The most common ones in the United States are ethanol. Ethanol is about 98% of the gasoline in the United States has ethanol in it. It’s mostly made from corn or sorghum. In the United States, it is made from corn and wheat. In Canada, it’s made from sugar cane. In Brazil and other areas of the world. Other biofuels that are common are biodiesel and renewable diesel, which are substitutes for diesel as well as sustainable aviation fuel, which is a substitute for jet fuel.

Tony

Okay, so when we hear the words biomass, what does that mean?

Corey

Once again, I’m just re saying organic material, organic plants. Biodiesel is also made from fats, recycled oils and greases. Those are the soybean oil, veggie oil. So that’s kind of what we’re talking about.

Tony

Okay, great. So when you talk about things like biodiesel or aviation biofuels, how much of, say, biodiesel in, say, North America or Europe, or how much of diesel in, say, North America or Europe is biodiesel?

Corey

I would say about five to 7% of the total diesel pool is biodiesel. Renewable diesel. It is a growing percentage primarily because with this EPA announcement, there’s mandates that require refiners and importers to use the fuel, as well as states with low carbon fuel standards that have increasing targets that require increased uses of these fuels.

Tony

Okay. And aviation fuel, bioaviation fuel, how much of the market is biofuel?

Corey

Next to nothing. And that’s where the big opportunity is. I think right now it’s like less than one 10th of 1% of the total jet fuel pool is sustainable aviation pool. And I think production in the United States was less than 16 million gallons last year. When we’re talking about targets of like 3 billion by 2030 and 35 billion by 2050, we’re talking minuscule mounts at this time.

Tony

Okay. I think it’d be much more comfortable in a biofuel powered jet than an electric powered jet at this point. I don’t want to get to that 300 miles limit and have the jet engine just stop.

Corey

That’s very common. I don’t think anybody wants to fly from Los Angeles to Singapore in an electric jet, but maybe if you’re hopping from island to island, then you would be comfortable with those smaller ranges.

Tony

Okay, so can you also tell us on these general segments that you’ve talked about in terms of biofuels, how quickly are they expected to grow? Generally like 400% a year or 20% a year.

Corey

No, I mean, the renewable fuel standard is what jump started the industry. Right? So ethanol was used as an oxygen for gasoline was basically like a 4 billion gallon per year. Industry in the United States. Then the Renewable Fuel Standard came out 2005. It’s been around for around 15 years or so or active. And during that time ethanol has gone from 4 billion gallon industry to a 17 billion gallon industry. So there’s already been the extensive growth for ethanol and biodiesel. Right now there seems to be a transition where more of the construction is going into renewable diesel and SAF. Those fuels can be produced from the same facilities. Like you said, it’s such a small percentage of the total jet fuel market that there’s an increased focus now on decarbonizing it. So if we have over 10% of the gasoline pool that has ethanol, around 5% to 7% of the diesel pool has biodiesel and renewable diesel. Now we’re just kind of making that transition of why is such a small percentage in aviation. And so the Biden administration has had setting these goals of production targets as well. As I know that Chris mentioned the Inflation Reduction Act a few times, that there are incentives for SAF that are better than some of the other fuels.

Corey

There’s higher blending credits for sustainable aviation fuel. And then in 2025, when there’s a new clean Fuel production credit in the Inflation Reduction Act, SAF has preferential treatment as well, where it gets a higher credit. So that’s the tool being used by the government to jump start SAF, just like ethanol and biodiesel were jump started with the onset of the Renewable Fuel Standard program.

Tony

Okay, great. So I understand those are all basic questions and most viewers are probably way beyond me in their understanding biofuel. So thanks for doing that. Can we walk through some of the EPA information that came out yesterday? You sent this great table, and if you could walk us through what that stuff means, I’d appreciate it.

Corey

Sure. Okay, so the intent of Congress was for refiners and importers to use a growing amount of biofuels each year. And there’s four separate categories that are depicted on the chart to the left that they need to blend a certain amount of renewable fuels, they need to blend a certain amount of what’s called biomass based diesel, which are the diesel replacements, a certain amount of advanced biofuels and a certain amount of cellulosic fuels. And what Congress did is that they would set a mandate and every year EPA would look at it and adjust it based on the available domestic supply. The mandates were set by Congress through 2022. And this has really been the first set of mandates where the EPA was setting mandates without the guidance of Congress. And essentially the only guideline that they had was try to keep up with the congressional intent. And essentially the congressional intent was for mandates to get higher and more stringent every year. So if we look at the chart, you can see how volumes are constantly going up a little bit. If we focus on this table, one of the takeaways from the announcement was a lot of biofuel companies were unhappy with it.

Corey

There was a proposal in December of last year followed by a public comment period and taking them about six months in order to finalize these mandates. The ethanol industry got a number less than what was proposed in December. So if we look at the conventional biofuels column of that table, we can see that about 15 billion gallons was basically reserved of a category that corn based ethanol can satisfy. The proposed volume was 15.25 billion and it was reduced to 15 for 2024 and 2025. So the ethanol industry is very upset about that. The higher the mandate is, the more than the greater likelihood there would be higher blending. The ethanol industry wants to move up from the standard of E Ten. The vast majority of the fuel in the country is E Ten, and they are pushing to have more E 15, E 85 and other higher grades. And part of the Inflation Reduction Act too was giving half a billion dollars in order for service stations to update their equipment, update their infrastructure, to enable them to sell more E 15. In terms of the biomass based diesel column, that’s something that you can see that it gets progressively higher each year for the mandates that were set for 2023, 2024 and 2025.

Corey

But it’s growing at a very slow pace and it doesn’t mirror the amount of investment that has been going into the sector. There’s already enough reduction right now to satisfy the mandates in 2025 and hundreds of millions of dollars are going into converting existing oil refineries to produce renewables. So we have renewable diesel facilities being constructed, we have sustainable aviation fuel facilities being constructed, and the actual capacity is going to be way higher than these biomass based diesel mandates, which has upset a lot of companies because historically, the EPA usually has looked at the availability of supply as the guide for setting these mandates. And when these mandates are considerably less than what they expect supply to be, then that has upset a lot of people. And the cellulosic biofuels, there was going to be a really big change in 2023, 2024 and 2025. The EPA was going to include EVs in this renewable fuel standard program. EVs do reduce emissions and they aren’t allowed to generate compliance credits like all these other fuels. And they had proposed a system or proposed regulations that would allow EVs to generate credits under the Renewable Fuel Standard and they were quite complicated.

Corey

The only companies that would be able to generate these valuable Rins are valuable credits known as Rins were EV manufacturers and there was just great opposition to it during the public common period. So the EPA punted having EVs generate these types of credits. So the cellulosic fuels are basically very small amounts of liquid biofuels coupled with biogas.

Tony

Interesting. Okay, so you covered this already, but I’m very interested to see that 15 billion gallons of conventional fuels just kind of plateau. And there must be a lot of disappointed people in the Midwest of the US. About that. And it does look like things are slowing down in terms of biofuel requirements. Maybe too much is strong. But is there more capacity than needed today, or is it just the investment that’s going in? Is planning to have more capacity than is outlined in these regs?

Corey

Well, it depends what type of capacity you’re looking at. If you look at just individual fuels, ethanol, if you kind of look ahead, if you look in the medium term and we’ve been talking about EVs during this discussion, that it’s clear that the increased penetration of EVs is going to take a lot of gasoline powered vehicles off the road. And when you take millions of gasoline powered vehicles off the road, there’s going to be less on road demand for fuel ethanol. So we’re going to reach that stage of what are you going to do with all that ethanol. We have about 17 billion gallons of capacity. So this is where sustainable aviation fuel is a godsend to the industry because one of the technologies that’s being developed to produce SAF is using ethanol as a feedstock for SAF. We talked at the beginning of how veggie oils can be used for biodiesel and corn and sorghum and wheat can be used to make ethanol. Right now they’re developing technology where actually ethanol itself can be used as a feedstock for staff. And once again, when there’s going to be massively declining demand for on road ethanol, the prospect of using ethanol to make something that could help decarbonize the aviation sector is extraordinarily exciting for the industry.

Corey

And also, it’s not a one to one ratio. It takes about 1.7 gallons of ethanol to make one gallon of SAF due to density issues. And so SAP is really opening up a tremendous opportunity for domestic and domestic ethanol producers and also imported fuel.

Tony

Go ahead, Tracy.

Tracy

Sorry, I had a question. So we’ve seen a lot of the aviation industry kind of push back on this state, saying that we can’t do this right now. This is going to cost us a lot of money. We’re going to have to pass these costs on to the consumer. So how do you look at this as far as I mean, obviously this is in the invancy stage, but how do you see this panning out? How long do you think this is going to take until this becomes like a viable fuel for aviation where it doesn’t cost us another $200 per flight to pay for?

Corey

Well, look, there’s already countries that mandate SAF in Europe. France mandates AF Norway and Sweden mandatesf. Already the EU directive is going to institute mandates starting in 2025. So it’s a real thing in Europe right now. Right now, once again, construction is going on. We have very minimal SAF production right now there’s a SAF producer called Montana Renewables in Montana that’s operating. And we have a lot of big facilities that are going to be coming up soon in California, in Georgia, and elsewhere. I’m seeing differently. We’re talking with airlines and more. The public press releases, they say they’re excited about it. They’ve entered into offtake agreements with these renewable fuel producers. They’re part of airline associations that have specific targets. Many of them have targets of 10% SAF by 2030. Whether or not anybody believes that’s Achievable, they may say something as the time comes closer where perhaps they take the position that it’s not feasible because staff is too expensive and consumers are unwilling to bear the added expense. But I think that many airlines are looking towards decarbonization efforts and they’re waiting for the staff to be produced. It’s behind schedule. There’s supposed to be a lot more availability of sustainable staff by now, but they’re waiting for it and they have offtake agreements for when it comes.

Tony

Why is the availability not there?

Corey

The development of technology. And frankly, when we look at the mandates, when I said, hey, there’s mandates for advanced biofuels and biomass based diesel and ethanol can satisfy one of the categories. There isn’t a mandate for SAF. Had there been a mandate for SAF when the Renewable Fuel Standard was amended in 2007, then we would have seen technology being kick started. And back then there’s been over ten years of trials and testing and test flights. Everything would have been accelerated had SAF been a mandated fuel. So right now the Biden administration, they have a target. They have what they call a grand challenge for a certain amount of production. 3 billion gallons of production by 2030. And once again, they’ve had provisions in the Inflation Reduction Act which will support this program, such as blending credits and cleanfield production credits that are pro staff.

Tony

Tracy, I’m sorry, I didn’t mean to interrupt you. You were starting to ask a question.

Tracy

No, you actually almost asked my same question, just rephrased a little bit differently.

Tony

Okay, very good. So in Corey, it also sounds to me like on some level, and I don’t think this is fully level, but it almost sounds to me like biofuels is kind of seeding, say automotive to EVs. Is that fair to say or not?

Corey

There’s no seeding going along.

Tony

Okay.

Corey

SAP is like perhaps a backup plan or the way they’re looking at the future. The ethanol industry right now is trying to make sure that fuels have higher blends. And actually last year there was record sales of E 15. There’s record sales of E 85. Ethanol has been selling at a lower price point than petroleum based fuels. So when you blend, there’s a better economic incentive to blend. So E 15 was selling at a much cheaper price point last year, and E 85 in California was selling up to like $2.50 less a gallon than the normal E ten. So a lot of people, when times are tough and the economy was bad, a lot of people saying, look, I heard that my car can accept E 15. I could fill up my tank for $6 less. And they gave it a shot and the cars didn’t fall apart on the side of the road. So you had essentially a lot of millions of new customers who tried these higher blends for a first time because they didn’t really understand them that well. They saved some money and now we got some new adopters of this fuel.

Tony

Okay, interesting. I’m going to ask both you and Chris the same question about your respective areas of expertise. So what should we be looking for when evaluating companies that are well positioned in biofuels? And Chris, I’ll ask you the same thing about battery metals, but what should we be looking for with those companies?

Corey

The companies are leading the carbonization efforts. One thing I didn’t really focus on is a lot of the new renewable diesel and SAF producers are going to be traditional oil refiners, refiners like Marathon and Chevron and Philips 66 and CVR and HF Sinclair. These are companies that are taking existing facilities and converting them to start processing renewable feedstock in order to produce renewable fuels. They’re making this transition from the old oil stuff and they’re producing these new fuels. And now they could use and they could blend these fuels into their existing petroleum based products. But that’s what we’re seeing. We’re seeing decarbonization efforts and a lot of these big oil refiners that are doing the energy transition and moving towards renewables.

Tony

Great. Chris, how about you? What should we be looking for when evaluating companies that are well positioned in battery metals? What are the main things that you’re seeing?

Chris

Yeah, I mean, look on the upstream with respect to the raw material. I think as I look at specific companies, the whole lithiumion supply chain discussion has this huge geopolitical component to it now. And so when I think about assets, mining assets in particular, I think what I’m looking for first are companies that have what I would call geographic and geologic diversity. Companies that may have lithium assets in Western Australia and in Chile or just different parts of the world. That way if you have an asset in a country and all of a sudden they wake up one morning, the government says, hey, you know what, we’re going to look at those royalty numbers again. Or no more exporting of raw. Well, look at Indonesia, right? I mean, twice in the last eight years they’ve banned raw exports of nickel anyway. So geologic and geographic diversity, number one. And then number two, producing battery metals, in other words, hitting that spec. I’ve talked a couple of times about battery grade lithium carbonate or cobalt sulfate or whatever it is. That is not something that’s easy to do. And while the know how is out there.

Chris

You want to find those management teams that I always like to say they have the right blend of sort of financial markets, acumen, how to raise the capital and manage the balance sheet and manage the capital structure, but also how to produce these chemicals. Because what we’re going to be doing if we are going to get to 50% Ed penetration or whatever the number is in the future, we’re going to be going after lower grade, lower quality assets. And those are more problematic in terms of hitting that battery grade spec. So, again, it’s geologic and geographic diversity, number one. And number two, it’s just management teams that have that technical capability to produce these materials of scale.

Tony

Yes. And I’ll ask you both the same question as well. What do you see as the best near term opportunity, Chris, around battery metals, around that supply chain? What’s the biggest near term, say, three to five year opportunity in that area?

Chris

I think from a higher risk tolerance perspective, I look a lot at battery technologies and so innovations around different cathode formulations. In other words, either using an equivalent amount of lithium or nickel or what have you, and increasing energy density. So I look at a lot of different cathode and anode technologies on the anode side of the battery, really interested in what we call silicon anode technology, which is effectively doping that anode with silicon. And that can increase the energy density up to around 30%. Okay. So you can drive 30% further, charge a little bit faster. So I look at a lot of those types of opportunities. Again, kind of alluding to or going back to what we talked about earlier, the refining aspect of this whole theme and this whole thesis. I mean, Elon Musk will tell you that he thinks that the bottleneck is in refining of these materials, and I think he’s partially right. I think, again, it’s also just getting your hands on the feedstock in general. So building out that refining capacity again, to your point, over the next three to five years is a really interesting place to be as well.

Tony

Right, okay. Corey, how about you in biofuels? What is the biggest opportunity in the next three to five years?

Corey

I’ve already mentioned it. The biggest opportunity is the use of ethanol as a feedstock for SAP.

Tony

For aviation fuel.

Corey

Yes, I’m sorry, I’ve been saying SAP. SAP is short for sustainable aviation fuel. That seems to be a great opportunity. We have once again, they generate Rin credits that can be used for the federal Renewable Fuel standard. They’re beneficial for these state low carbon fuel standard programs like in California, Washington and Oregon, and they’re developing state credits that are incentivizing it as well. So if you there’s a SAF purchase credit in Washington state and Illinois now where they’re adding on tacking on additional incentives to sell staff into those states. So I think ethanol to SAF and the advancement of the construction of these facilities is quite exciting to the industry.

Tony

Okay, thank you. And Tracy, let’s end up where we started out on oil. We’ve talked over the years about the lack of investment in the upstream, in oil and in the downstream in oil and gas. Right. And it sounds like battery metals and biofuels are getting a lot of investment. So are these large energy firms, are they taking funds that could be put into the upstream and substituting them into biofuels and battery materials? Or is it not substitutional? Are they just not doing that capex on energy upstream and they see this as a completely different thing?

Tracy

Well, there are two totally different things when we’re talking about mining for metals and mining for oil and gas. But if we look at the biofuel side of it, of course there are a lot of refiners that have allotted a lot of money to changing over, particularly California to changing over. Some of their refineries to include biofuels. Marathon is one, valero is one for a couple to look up. I definitely think that this industry is they’re not aware of what is happening and where this industry is going. And so, again, like I said, in particular, if we were looking at the refining industry, there are a lot of traditional oil refining companies that have already allotted a lot of money into biofuel technology and refining biofuels because they don’t want to get left behind.

Tony

Great.

Chris

Sorry, Tony. Just as an example of an oil and gas company looking at the battery metals is exxon. There was a story in the Journal a couple of weeks ago about how they’re looking at getting into the lithium production business and the smackover formation in Arkansas. The reason I think why a lot of these oil and gas players have shied away from battery metals or diversifying away from their business from a capex perspective is quite simply because most of the battery metals markets are too small. I mean, I mentioned that lithium is a 900,000 ton a year market that’s I don’t even know at elevated prices, is it 20 billion a year or something like that in revenues? I mean, that’s probably the capex budget for one of these super majors in a specific year. So the battery metals have never really moved the needle from a financial perspective for these guys and that’s one of the reasons why they’ve steered clear of it. But again, with the way the political winds are shifting, you’re starting to see the exxons of the world say, hey, we’ll give this a closer look. So I don’t know what’s going to come of it, but it’s something that is interesting.

Tony

Great. Okay, guys, this has been really helpful for me, really educational, informative for me. So thank you so much for spending your time. Thanks so much for helping us out with this. Have a great weekend and have a great week.

Corey

Ahead.

Tony

Thank you.

Tracy

Thank you.

Chris

Thanks you me out.