In this latest episode of “The Week Ahead,” Tony Nash hosts David Cervantes, Albert Marko, and Tracy Shuchart to provide valuable insights on a range of topics, including recession indicators, China’s economic challenges, the natural gas market, and Europe’s energy supply problems.

Challenging Prevailing Narratives

David Cervantes sets the stage by reflecting on his accurate recession call made several months ago and his process of questioning prevailing narratives. He emphasizes the importance of construction activity and employment data when analyzing the correlation between the housing market and recessions. His research process involves independent replication of economists’ work to understand the underlying factors and ensure a comprehensive perspective.

Commercial Real Estate and Economic Impact

The panelists discuss the role of commercial real estate in the broader economy. David explains why it is not a major factor in the economic cycle, highlighting the strength of the construction industry and the scarcity of contractors. By shedding light on the limited impact of commercial real estate, the conversation emphasizes the need for a holistic approach when assessing economic trends and potential risks.

Tech Job Losses and Economic Outlook

Tony and David explore the current state of tech job losses and its implications for the overall economic outlook. David counters concerns with data, citing payroll and continuing claims data that do not support the narrative of significant job losses. The conversation also touches on the trend of individuals turning to do-it-yourself solutions for home repairs, adapting to tasks they would otherwise hire professionals for.

Factors Affecting Hypotheses

While acknowledging the potential risks to his recession hypothesis, David dismisses concerns about a credit contraction in the banking sector. Structural changes implemented after the global financial crisis provide safeguards against such an event. The conversation also explores the possibility of energy shocks and their potential impact. Falling oil and gas prices are seen as beneficial, but the panelists discuss how energy shocks could still play a role in shaping future economic scenarios.

China’s Economic Challenges

The discussion shifts to China’s current state, its economic challenges, and the implications of US economic officials’ actions. Panelists express concerns about China’s lack of movement politically and economically, despite slight retail sales growth. They delve into the influence of interest rates, inflation, and China’s desire to avoid becoming like the Soviet Union or Japan. The participants draw parallels between China’s situation and Japan’s experience in the 1980s, highlighting the complexities and geopolitical considerations at play.

Geopolitics, Governance, and Natural Gas

The panelists delve into geopolitics, governance, and the natural gas market. They discuss China’s fear and arrogance regarding its future and Japan’s bureaucrats apprehensive about following the path of the Soviet Union or China. The conversation also touches on China’s challenges, including demographics, environmental issues, and water scarcity. Differences between the US and European markets are highlighted, with a focus on Europe’s energy dependence, climate concerns, and political decisions impacting market volatility.

Europe’s Energy Supply Problems

The discussion highlights the supply problems in Europe related to air conditioning demand during summer. While Europe is not a major consumer of air conditioning compared to the US, increasing temperatures lead to energy supply drawdowns. The panelists highlight the impact of low water levels in rivers like the Rhine, causing difficulties in transporting crude and gas products to Europe. The water scarcity issue extends beyond northern Europe, affecting the Mediterranean region as well.

Energy Costs and Industrial Dynamics in Europe

The conversation explores the impact of high energy costs and environmental policies on European industries. The participants discuss the relocation of companies to countries like China and the US, which offer lower energy costs and potential incentives. Deindustrialization in Germany and other EU countries leads to the loss of market share. The participants also touch upon Europe’s approach to energy policies and the potential regrets that may arise in the future.

The latest episode of “The Week Ahead” provides invaluable insights into key economic topics shaping our world. The discussions on recession indicators, China’s economic challenges, the natural gas market, and Europe’s energy supply problems offer a comprehensive understanding of the complex dynamics at play. By challenging prevailing narratives and encouraging critical analysis of data and methodologies, this episode serves as a guiding light for navigating the ever-changing economic landscape. Stay tuned for more thought-provoking conversations that empower us to make informed decisions in an interconnected world.

This is the 69th episode of The Week Ahead, where experts talk about the week that just happened and what will most likely happen in the coming week.

Follow The Week Ahead panel on Twitter:

Tony: https://twitter.com/TonyNashNerd

David: https://twitter.com/pinebrookcap

Albert: https://twitter.com/amlivemon

Tracy: https://twitter.com/chigrl

Trascript

Tony

Hi, and welcome to the week ahead. I’m Tony Nash. Today we’re joined by David Cervantes, Albert Marko, and Tracy Shuchart. Guys, thanks so much for joining us. Been a really interesting week with the Fed meeting and with it seemed like a reacceleration of markets.

Tony

One of the things I really wanted to talk about and I’m so pleased to have David today is his no recession call, or at least not right now call. This is something he did six, seven, eight months ago, and he’s been very consistent since then. So I want to dig into that. I also want to talk about China. We’ve had a lot going on in China with the upcoming blinken trip and some Chinese economic data and other things. So I want to talk with Albert about that. And then we want to talk a little bit about Nat Gas. We’ve seen a bounce in Nat Gas over the past couple of days, and Tracy’s obviously the expert there, so I want to get her thoughts on that as well. David, thanks for joining us. I know this is your first time, and and I promise you’ll, you’ll emerge unscathed afterwards.

Tony

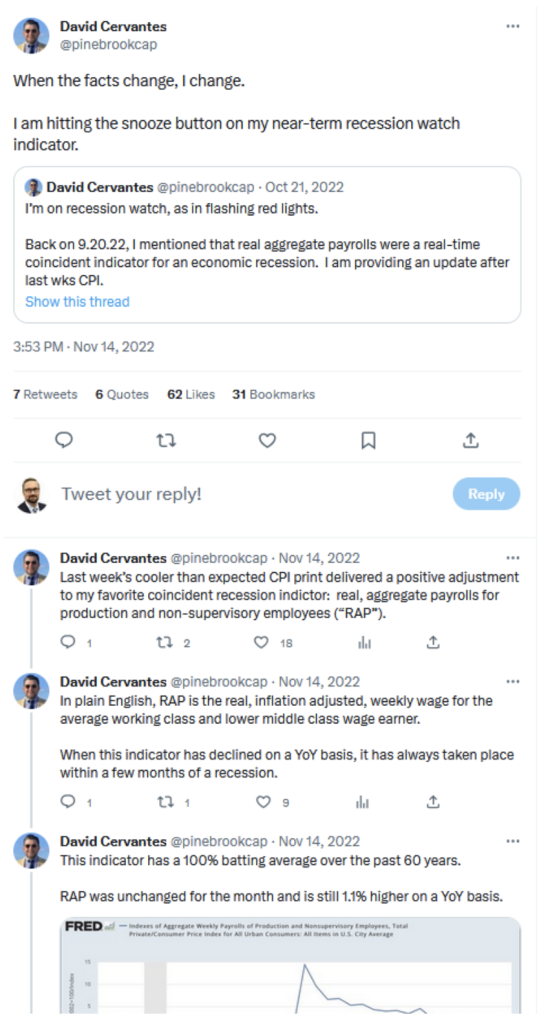

We’re were you called a recession back in on November 14 of 2022. I couldn’t find an earlier time that you did that. But if you look at the tweets we’ve got from the 14th, you went into kind of a fair bit of detail on why you called that.

And you’ve been very consistent since then, as we’re showing, kind of in this first series of tweets, you’re talking about really, as you say, in plain English, why you changed your view, and then you reinforced this on January 6, and then you’ve been very consistent since then, despite a lot of pushback. ‘

And so I really admire that. And I think all of us here have some pretty non consensus calls pretty regularly. So I think that’s a great call. But what I really want to learn about is your process because we have a lot of kind of retail investors who watch us. And so can you talk to us a little bit about your process and how that process fed into this recession call? Because I think people underestimate having a consistent process.

David

Yeah, sure. Well, first of all, thanks for having me. Really excited to be here. I’ve been following your work for a while, you and Albert and Tracy, the rest of the whole team. So I’m really pleased to be here. Just getting back to the question of the process. Look, we’re all reading the same information, have access to the same media set and tools. So the question is, how do you step out of that and develop views that may run counter to that? And if they do, are they right or are they wrong? So just as a general matter, I like to just question the implicit and explicit assumptions that underlie the thesis or the dominant narrative. So it’s not so much drilling into the numbers as it is to understanding the argument, the logic, and just kicking the tires and seeing if it makes sense. So back in October, I don’t know if you saw this tweet, but back in October I said, hey, I’m going on a recession watch. One of my indicators flipped yellow, and that indicator is the, I call it Wrap real average weekly payrolls for non managerial employees, basically the vast majority of W two wage earners.

David

So that kicked off in October. And the indicator rule is as long as we’ve stayed positive year over year, we’ve never gone into recession. It’s an indicator that has a 100% batting average in the post war period. So that flip yellow. And at that point, recession hysteria was kind of peak. The 210 yield curve inverted back in July in October, 3 month ten year, which is kind of the gold standard that inverted as well. And oh my God, we’re going to go into recession. But as with anything, I had to check what was the dominant narrative that was feeding this. Well, the big narrative obviously was the rate hikes. But housing, it was like all of a sudden the bull market and housing came to a stop. House price appreciation stopped, sales volumes tapered off and then eventually being a turn down. So a little light bulb, my head went off and it was, oh my God, it’s housing. So I started digging in. Look at Ed Lemur’s work. He’s an economist who coined the phrase the housing cycle is the business cycle. Read his work and then I basically replicated his work doing it.

David

I did it myself. So instead of just taking what he said as a fed out complete, I said, you know what, I’m going to rebuild this model on my own and really get into the weeds and see if it clicks. And it did. We don’t have to go into the model process. But what I came to learn was that seven out of eleven post war recessions originated in the housing market, okay? And specifically, it wasn’t just house prices or house sales volume. It was construction activity and construction employment. And it wasn’t just the employment at a level, it was the volatility of that economic activity. So I basically wrote this paper for myself just as a thought exercise, and I basically had a predetermined thesis. The housing market will once again be ground zero for a recession. And as I was going through that process, I was looking at the data, I had an insight, and it’s no the housing market. If we have a recession, it won’t be because of the housing market. And the reason was housing construction and housing employment were very robust for a variety of reasons. One was all the stimulus money that got pumped into the system, people were still buying houses, rates were obviously on the move up.

David

But when you need a home given the structural home shortage in this country, you make whatever trade off you have to make to house your family. Even if you move somewhere else, you buy less house, pay more interest and buy less house. Whatever you got to do. You need a roof over your head, and you’ll do it. So I didn’t see the typical causes of a housing downturn to be in the works. And then we got the big inflation pullback in the November report of the October data. And if you recall, after that report came out, we had a huge short squeeze. We were up, I think, 2% on that day. And that raised took my yellow flag on the wrap, real aggregate payrolls back to a green. So between the inflation story supporting aggregate payrolls and coming to the conclusion that the housing sector would in fact not be the cause of a recession, the ODS were that we would not have a recession. When you have a seven out of ten being in the housing market I’m sorry, seven out of eleven and the remaining four well, if it’s not from housing, then your ODS are just less.

David

And between my indicator and I use a variety of indicators, but that was the one that was most prominent between that indicator and what I saw going on in the weeds of a housing market, not sales, not volume, but an actual economic activity that rolls into GDP accounts, if you recall. Prices and sales don’t. They might benefit the buyer and seller, but they don’t roll into GDP accounting. Construction activity does. Employment activity does. And that was moonshotting. That was doing great. So I said to myself, we’re not having a recession. Obviously, I continued to monitor the data, but that was the basis of the call.

Tony

Great. I love you understand the initial conditions. You understand the prevailing narrative. You understand the data I see regularly on your feed where you kind of question the data. You understand the details of the data. You did more research on your own to identify where we actually are, and then you changed your view. So I think it’s easy for us on Finn, Twitter, whatever, to see what the prevailing narrative is and be panicky about. We have to position a certain way because of where the narrative is. But I like the way you kind of pulled apart from that and you really looked at the underlying data and then came up with your own hypothesis. It’s fantastic. And I like the way you continually re change that. We don’t talk about that enough. We’re kind of talking about what are people doing in markets, what’s happening in markets? But going back to these principles and coming up with your view and having that being a rolling view, right? You’re not stuck in that. Sure, of course. No, you’re checking your views as new data come out.

David

I’m sorry, Tracy. Go ahead.

Tracy

I wanted to ask you about what your thoughts were on commercial real estate, because literally, if you go on FinTwit right now, everything is you are all going to die. Commercial real estate is going to crash. We have nobody going back to work in office buildings. New York. You’ve got New York. Even you’ve got San Francisco. That’s a whole different story. So what are your thoughts on that as far as how it factors into this real estate narrative?

David

In terms of the economic cycle, I really don’t pay a whole lot of attention to the commercial real estate part. And here’s why. The construction activity of the actual building of a construction of a building does feed into GDP accounting, but what we’re seeing now is a collapse in commercial real estate prices. And some people are going to take their lump. There will be some tiers, there will be some PNL losses. As long as it doesn’t feed into the credit markets and into the broader economy. As far as the cycle goes, I think it’s for the most part, not an issue. Investors will get burned, someone will get hurt. But in terms of GDP accounting, I just don’t see it really being a factor. Now, again, I mentioned actual construction. So fine, maybe new building development takes a pause, but we have record amount of money going into other types of non residential construction. Back in May, we got some data for the April release on non residential construction, and these numbers were completely off the charts. I have some threads up. I can’t recall them right now. But the idea was that with the Onshoring and the IRA, the Inflation Reduction Act, we’re going to see a lot of infrastructure, a lot of money pumped into infrastructure development.

David

And I think that’ll fill the hole that’s being left by any development in the commercial real estate space.

Albert

That’s interesting because a while ago we noted that when we’re talking about layoffs, one of the most robust sectors was the construction industry, specifically housing. We mentioned that verbatim. We’re like, where are all these layoffs? If we’re going to a recession, where are the layoffs in that sector? They just weren’t coming.

David

That’s right. So one of my recessionary indicators is the thumb rule where you basically get a 1% I’m sorry, I believe it’s a 0.5% increase in U three within six months of its most recent peak. And then there’s other recessionary studies, but my basic metric is 1%. If we see a 1% loss of non farm payrolls and employment, basically 1.6 million jobs, that’s where you start getting recession. Not just recession vibes, but it’s pretty much you’re into recession because history has shown it doesn’t stop at 1%. Once you have 1% job losses, it keeps going. But the question in my mind is what’s going to trigger this employment extinction event? What’s the economic media that’s going to come out here? Have you tried hiring a contractor? Have you tried getting someone to fix anything? Good luck. I’m looking personally. We’ve got three bathrooms to do. In our best case scenario, they’re going to be done in the spring. Okay? That’s our best case scenario. Between backlogs and supplies and just bodies that can hold a hammer and use a drill, they’re just not there. The bodies aren’t there. So what’s going to trigger the employment extinction event?

David

It’s not going to come out of construction. It’s not going to come out of any other sector that would have that much of an impact.

AI

With CI Markets, you can access AIpowered market forecasting for as low as $20 a month. Get 94.7% market forecast accuracy for over 1200 assets across stocks, commodities, currencies, equity indices, and economics. With weekly updates and one-month and three-month error rates, you can rely on CI Markets to help you make informed decisions. Join a growing number of satisfied users who already transform the way they invest and trade with CI Markets. Don’t miss on another opportunity. Start forecasting with confidence today for as low as $20 a month. Visit completeintel.com markets to learn more.

Tony

So when we hear about tech job losses, you’re not really all that worried about that.

David

Just on the numbers alone. The answer is no. If you go back to weekly payrolls, you go back to continuing claims. It’s just not there. It might make it for a great headline, but we’re not seeing the numbers. Obviously, weekly payrolls have softened a little bit, but the four week moving average is still well within my comfort zone. My comfort zone is when we see the four week moving average break at 330,000 and we’re, I think right now at 245 or something like that. So we’ve got a while to go.

Tony

And your answer on hiring contractor David is I’ve been watching a lot of YouTube videos, so for anybody who follows me on Twitter, I replaced my wife’s brakes last weekend. So that’s an incredible amount of trust from her to allow me to do that. But I think people are coping. They’re trying to cope to figure out how to do things for home repairs and for their car and other things when you can’t find I kind of joke about the brakes thing. I was just more curious about how to do it. But I think a lot of people are trying to figure out how to do it on their own because they don’t want to wait for seven to nine months to get something done right. And mean, that’s just that.

David

But I mean that’s for planned things. But you also have unscheduled things. What if you have a broken window or you need locksmith? I think is pretty easy. But something that happens and your HVAC goes down in the middle of winter, your heating goes down, what do you do?

Tony

Yes, very expensive. Okay. So if you just take a different position and let’s say there were something to happen in the next, say, three to six months to break down your thesis, what could some of those things be? Because a lot of people out there going, oh, this can’t continue to happen, it’s not this strong, things are going to break down. What could it be to break down your hypothesis in the next, say, three to six months?

David

I think the problems that we saw in the banking sector, if they were to expand and roll over into the general economy and really cause a credit contraction, but we’re just not there. I mean, part of that is just structural. After the global financial crisis, all the rules were rewritten the banking system and the economy had somewhat of an existential moment. The adults in the room said, never again, we’re just not going to allow this. We’re going to rewrite the rules. So now you’ve got the two big to fail banks that control most of the credit in radiation. A lot of some credit is local, particularly construction. Construction lending, real estate lending is very local. But for the most part, the credit flows that drive the economy come from the g SIBs. They’re too big to fill banks. So it’s out there as a possibility, but I see that more of as an economic meteor. Can it happen? Yes, likely. I don’t place high odds in it right now, is the answer. Okay, so that’s one area of concern though. Things did get a little dicey back in March, but it seemed like it’s contained for now.

David

I know that’s a four letter word after 2008, contained, but I think that’s where we are now.

Tony

Okay, so we could see a gradual deterioration in economy, but you’re not really seeing any near term shocks. That’s a question statement. Yeah.

David

I think the other shock could be obviously an energy shock because that energy is very inflation is very energy sensitive, and Headline in particular. So if you recall back to 2008, we were looking at $140 a barrel oil. That was, I think, the primary catalyst for a policy mistake with the ECB when Trisha raised through Europe into a double dip recession. I’m sorry, not double dip. First step was in 2008, the second was in 2011. But oil was really the catalyst. So we’ve been lucky where if you look at the price of oil and gas, they’ve come down significantly. I know Core is separate from that, but headline has been helped tremendously by a fall in gas. So if we have some geopolitical event or some kind of energy disruption, that could be another factor, I think.

Tony

Yeah, I think you’re right. I mean, geopolitical events, these are things that really can’t predict. Even geopolitical forecasters, it’s really hard for them to predict this stuff. Right. Except Albert, of course, because he’s got a great record. But I don’t know of anybody else who really predicts them as well as Albert. Okay, David. Thanks so much. For that. It’s an incredible call you made. You’ve stuck with it even when it was really not popular. And so I really wanted to highlight that and really underscore, how did you come up with this? And I think I’m hoping people look at that and really kind of check their initial conditions and look at their assumptions and then really run their own data, because we can’t take it from social media. We can’t take the narrative from other people. We have to check this stuff out on our own.

David

I think that’s absolutely right. I could have taken the Lemur study at face value and just gone with it. I think forcing myself to replicate the study made me get into the weeds and understand everything that I had to understand to make the call.

Tony

And every time you dig into methodologies, you find flaws and you find things where in some cases, it’s more detailed and effective than you assume. I love tearing apart methodologies so you understand that stuff. So that’s great.

Tracy

Okay.

Tony

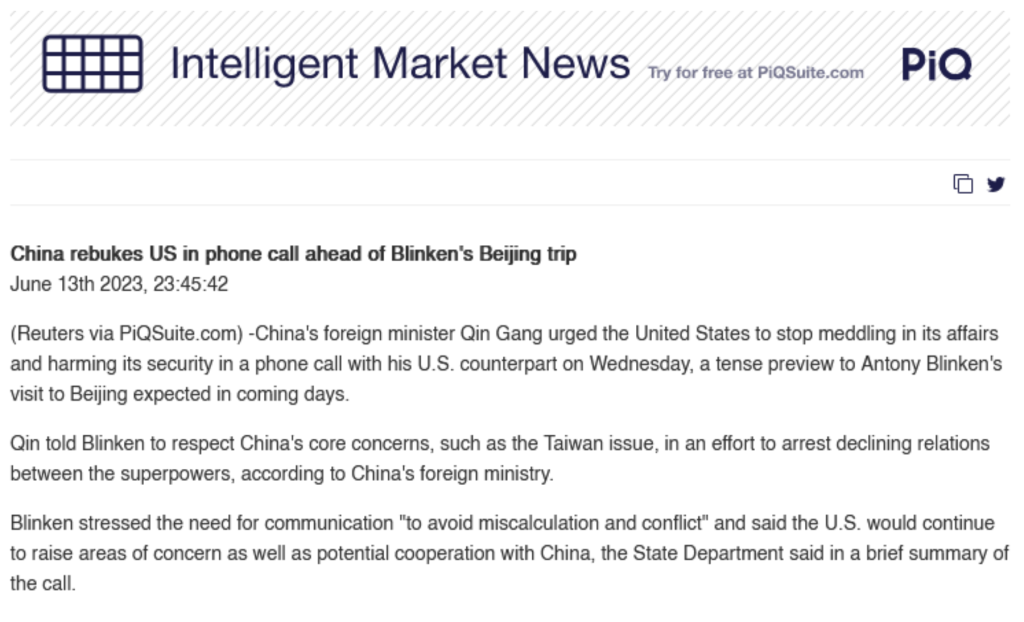

Thank you for that. Hey, Albert. Let’s move on to China. China kind of seems to be in a little bit of kind of an inertia state. I mean, there’s just not a lot of movement. There’s not a lot of movement politically. There’s not a lot of movement economically. We saw the kind of sputtering restart in Q One. They’re still kind of not moving that much, although we saw retail sales grow, like, 14% or something like that. Although, admittedly, it’s on a closed economy. But we have things like youth unemployment over 20%, which should terrify the Central Committee. And we have this Blinken trip coming up this weekend, which I don’t really understand the point of this. And we have things like China’s foreign minister. We’ve got a story on screen where China’s foreign minister pretty much spanked Blinken on Wednesday before the trip, saying that the US.

Needs to change and other things. So, first of all, I know there’s a lot to cover here, including the plunging CNY. But first of all, is there a point to Blinken’s trip to Beijing this weekend?

Albert

I mean, in Blinken’s mind, there might be, but not in anybody else’s. He’s not going to be meeting with anyone of significance. I mean, she certainly will meet with him, and I don’t even think the foreign minister might meet with him. They might give him to, like, a third or fourth string official just for photo ops, but that’s about it. Blinking has shown that in the foreign affairs world that he is a lightweight and destructive to the United States interest. So I don’t care, and I don’t think anyone else in the world cares about Blinken’s visit to China.

Tony

Right. And I just want to kind of direct people back to, say, 2021, when he went to Anchorage and we were talking about this, and he really didn’t look strong in that meeting. He really didn’t look like he was carrying a potent message then and again, the the foreign minister kind of spanked him in front of everybody, and he really hasn’t come back from that. He’s tried to take a hard line on things like Taiwan and other things, but he’s really looked more like an academic than a secretary of state.

Albert

Is that fair to yeah, that was intentional. I mean, the Chinese tested him and he failed, and he never recovered, and nor will he recover. He’s failed pretty much everyone in the world. So, like I said, besides Blanking, there’s a lot of things going on in China right now.

Tony

He’s done well in Europe, though.

Albert

Yeah, well, I mean, it hasn’t blown up yet, so I guess that’s okay to say.

Tony

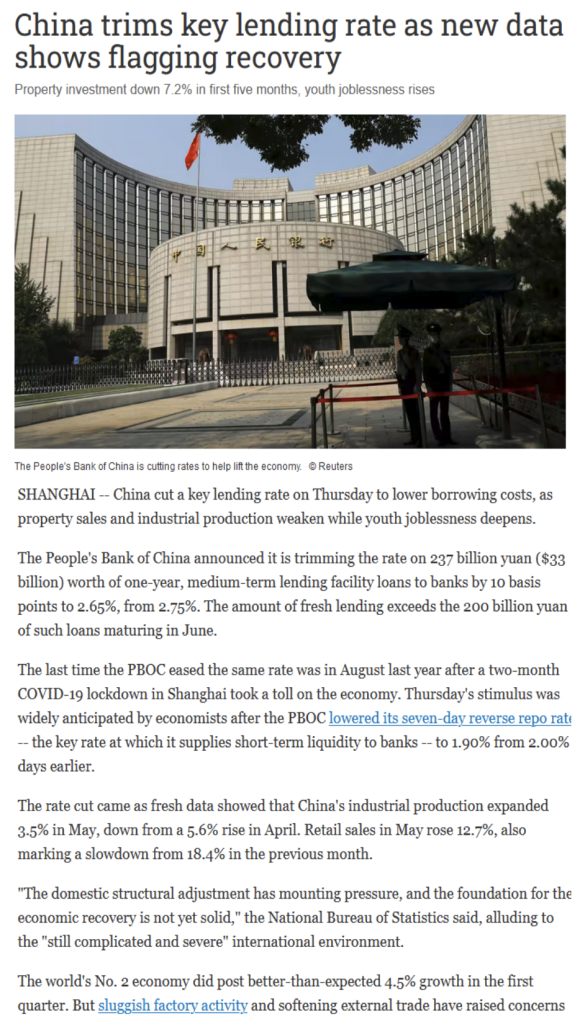

Right? We don’t know. Right? Exactly. Okay. So I wanted to cover that off really quick, just in terms of what to expect from the blinken trip. Maybe there’s some surprise, but I don’t have huge expectations because I don’t think the purpose is clear, really, to anybody. As we look at China on the economic front, they’re desperately trying to get things back on track after that slow reopening. And we spoke in December and agreed that it would kind of sputter, and that’s what we’ve seen happen. As I said, retail sales came in strong. Youth unemployment is pretty terrifying, and we see the PBOC coming in with kind of a small loosening.

But why has China been so slow to act? And what moves do you think Xi’s regime can do to accelerate things?

Albert

Well, they’re right now facing an economic warfare against the United States. The Federal Reserve, with Powell and Yellen at the treasury and some of the blinking officials, along with Wall Street, have a concerted effort to push China down for political and economic reasons. How are they doing? Well, because they’re keeping rates up so high right now, 4.5% on the tenure is game over in China. I’ve been told by analysts in China and Singapore that it’s game over. They certainly weren’t ready for 6% Fed Funds rate, which everybody in Wall Street is talking about right now. And I think that’s absolutely coming. We’ve talked about it on this, that 6% should probably be where they stop, and it looks like it’s going to right now. The Federal Reserve with Yellen can keep us here at 5% rates for the long run, maybe two years, keep the economy between zero and half percent growth, and maintain where we are right now. And hats off to David that saw this data well ahead of anybody else in terms of keeping a recession away from the political scene here in the US.

David

Can I jump in there on your point, Albert, about the US. Economy? The strength, I think, is being underestimated, underappreciated. So going back to the housing call, I looked at fixed residential. I went to the GDP, national accounts line by line, and fixed residential investment was the catalyst for it. Was net GDP subtracted from GDP in 2022 in late winter early spring I did a thread discussing fixed residential investment. My hypothesis was that we didn’t need it to get better. We needed to get less bad. And if it got less bad, given the resilience of the economy, that could potentially moonshot. Things fair enough. Q one GDP comes out. We were expecting I believe -0.6 subtraction GDP and we got -0.4 so there was a marginal less bad, marginal improvement and I think that’s going to continue. And if that continues, I do think that this whole idea we’re going to cut rates that gets kicked out farther than we think. So I’m just trying to go back to your point that this economy is going to run a lot hotter than people think rates will stay higher and that’s going to put the pressure on that you were discussing.

Albert

Yeah. Let’s be clear here. Four and a half percent on the ten year and 6% Fed fund rates means that all the money in Asia is going to come right back into the United States, which is bullish for equities. And we can discuss about what that really means for the market, I mean, for the economy overall, but that’s what’s going to end up happening. And from their perspective, it’s better for China to defend themselves from going over in the abyss than actually take on the United States globally. And that’s the general thinking right now. When it comes to inflation, they got it somewhat handled because they have a team that deals with commodity inflation in the futures market.

Tony

Chinese or the American?

Albert

No. The US. Has a team of like two dozen guys that handle this in terms of commodities in the futures market. And it’s under the whole national defense sort of mantra. But with inflation somewhat in the four and 5% area and wage inflation gaining steam, that keeps the populace at least at bay and not have pitchforks and torches coming for congressional members.

Tony

When you say economic warfare, is that intentionally against China or is it something where US. Economic officials are really just trying to keep the job market in a good position and put a damper on inflation? And then a secondary effect is the impact on China.

Albert

I’m 50 50 on that one. Right, because it’s certainly directed towards China. But Yellen knows that if you attack China and Asia in general, all that money comes right back into the US. Economy and the US. Market. It’s a little bit of 50 50 from my perspective.

Tony

Okay so from your perspective what can China do to all these headlines over the past couple of weeks talking about China needs to rally they need to circle the wagons and figure out what they’re going to do with their economy. What can they do just spend more money domestically build more bridges and high speed rail and all that stuff or.

Albert

Devalue the one that’s the only option to do it. That comes with other ramifications that a little bit over my pay grade, but that’s their only option is to devalue.

Tony

Well, it’s domestic inflation in China. Right? So they’re going to goose their exports to compete with Japan and Taiwan and Korea. But that comes with more inflation at home. Is that fair?

Albert

Yeah, it is. But inflation there is kind of tame. They have control over the economy more so than anybody else does. So they can tame inflation, at least on a numbers basis of what they put out, because we all know that data. That data is all the time inflation.

Tony

Data in every country. There is no country inflation data is accurate.

Albert

Yeah, of course. Even in the United States. I mean, they manipulate things with unemployment, inflation data and CPI all the time. But it’s interesting you mentioned Japan. This is eerily similar of what Japan went through in the 80s.

Tony

Tell us more about that.

Albert

No, I’m just relaying what I’ve been discussing with clients and friends in Wall Street, and this is exactly what the Japanese had gone through in the they’re pushing it onto the Chinese. The Chinese could have an inflation problem. Their growth is stagnant at the moment. Their demographics is not that great, and they’re fighting against the juggernaut in the United States.

David

China looks at the past 25, 30 years and they see two things that they don’t want to be. They don’t want to be the Soviet Union and they don’t want to be Japan. And I think both those things terrify them for a host of reasons. But those two things are the third row that they want to stay away from.

Albert

Yeah, that’s exactly right. And that’s why I’ve always dismissed any kind of Taiwan invasion, because that bring back the Soviet mentality of taking on the United States geopolitically. They don’t have the money for it. Let’s just be honest. They don’t have the money or even the nerve to do something like that. And when it comes to the Japan comparison, they really don’t want an economic collapse of their manufacturing sector.

Tony

Right.

David

David. What?

Tony

You mentioned about the Soviet Union in Japan. That’s absolutely true. They’re terrified of that. But when you talk to their bureaucrats, particularly, they’re also somewhat arrogant about we won’t be that because we’re different. And so there’s kind of both arrogance and fear about becoming either one or both of those. And it’s kind of weird because they’re moving in the direction of both. They’re going to fight really hard not to become one or the other. And I’m not saying they will, but I think that the possibility of that is becoming more real by the quarter, let’s say.

David

I think that’s right. China’s biggest problems are problems that they can’t resolve through war or through geopolitics, whether it’s their demographics and their birth rate that’s falling off a cliff, whether it’s water, their environmental issues are horrific. The Gobi desert. Continued when I was in Beijing, back when I was in graduate school, living in Singapore. Took a couple of trips to Beijing. There are always sandstorms in Beijing because the Gobi Desert is encroaching upon Beijing. It’s just one environmental catastrophe after another, going back to water. This is why they got their eyes on the Himalayas, for that Himalayan clean water source, which, aside from food, you also need for manufacturing. And I think this is where the United States has a huge geopolitical edge. We are very geographically advantaged versus most of the world, if not the entire world. Our water resources. We got the Great Lakes. We have the watershed that goes through the Appalachian Mountains, the watershed that runs through the Rockies. We have all these massive watersheds that we could leverage off of for both food and for manufacturing. China does not have that, not even close.

Tony

Well, and as China tries to take the Himalayo Mountain watershed, they’re upsetting everyone in India. And all of those tensions taken together are just a nightmare for China. China as a governance subject is incredibly difficult. I think most people on this side of the world look at China and believe it’s this monolithic government, and Xi Jinping makes a decision, and then it happens. It’s not that way at all. It’s just chaotic. And so, given all of these challenges they have, as well as the challenges within governance, it’s incredibly, incredibly difficult for them to tackle one of these, much less the gamut of all the challenges.

David

They have their governance. Really, the basis of governance in China is patronage, whether that patronage is family or whether it’s friends or political cronies, but it’s patronage. So the things that make governance good, such as competitive politics, don’t really exist in China. Obviously, the Communist Party’s monopoly on political power. But without that kind of competition, you have a lot of patronage favor occurring that might not lead to optimal outcomes. And then you magnify that across the country, different levels municipal, provincial, national it’s just like a real cluster bomb of bad governance and bad incentives.

Tony

Oh, it’s a competitive political environment, all right. But if you lose, you die. Like, literally.

Albert

I’m glad David pointed out all those things. Very few people actually in the financial sector actually take into consideration all these other things like water, fresh food, defense, and all these other components that make a superpower what a superpower is. I mean, all we’ve been hearing is that China is the next superpower. It’s taken on the United States, ABC and D reasons and so on and so forth, but they completely forget that they don’t have any kind of arable land at the moment to feed themselves. They’re in a battle with India, which is a nuclear power, for God’s sakes, for water that supplies a billion people on one side and a billion people on the other side. And these things are not to be taken lightly. I mean, you can’t just gloss over these things and say, oh, well, China is just going to take over Taiwan and US can’t do anything about it, and so on, and they’re going to move into Africa and South America and this and that. It’s far more complex and the details that they but actually pointed out, it’s spot on.

Tony

Great. Okay, guys, thanks for that. Tracy, let’s move on to natgas because we’ve seen some real interesting activity in natgas over the last couple of days. We’ve seen an interesting bounce. And so you put out a tweet on China’s natgas traders this week, surprised by the bounce in the market. So that’s very interesting to me. It looks like they were caught off guard.

We saw natgas up 9% this week.

But if we put that in context, that’s kind of a slight rise. It’s not like it’s completely market changing. What are your thoughts on this? And are we finally seeing some strength come back into the Nat gas market?

Tracy

Well, I mean, to be honest, this is a non sequitur for the US. Market. At this juncture. We’re going to have to see major drawdowns in either Asia or Europe to really get this market going. Yes, we saw a bounce, but if you look over the long term out to the US nat gas futures markets when this contract started, we’re still in that same long term trend that we have started in since 1996, when this contract started. So we’re still in that very comfortable zone in the US. Where we’re one dollars, $3. We have seen spikes over the last 30 years, but we’re still in a very comfortable zone just because of the amount of natural gas we produced. Yes, we did see a spike in prices in the TTF contract, which is the European contract that was due to Norway. Norway had to shut down one of their processing plants. And then we also had that news that the Netherlands was shutting down their largest natural gas field, but we did see price rise 70%, but it came back down 20%. I think that altogether, if we look at this Nat gas situation altogether, I just don’t see still at this juncture where we’re going to see natural gas prices rise.

Tracy

The United States, if that’s where we’ll be looking at Nest, has nothing to do in the immediate term. Let’s just say that because we’re just still producing a lot of natural gas, and even though we’re exporting to other countries, we still don’t have those long term contracts. We still are spending money building out export facilities in the Gulf. The United States in particular is a very different situation than we would see perhaps in Europe right now. And so I think looking at their particular situation, we’re going to see higher volatility in those kind of markets. Because if production goes down in one country or is mitigated in one country, they’re going to see a price spike. Unlike the United States, if we see, say, the permian doesn’t produce as much as they usually do on one week, that’s really not going to change the overall situation in the United States just because of the amount of natural gas reproduces the whole. So if you’re looking for this bump in natural gas prices in Europe and in Asia, I don’t think that’s really going to manifest itself exactly right now in the US.

Tony

Okay, so let me go back to something you said. Why are the Dutch shutting down the largest field in Europe?

Tracy

Well, because without I don’t want to.

Tony

Make no, just be yourself.

Tracy

Say what the situation is. The climate activists are saying this is causing earthquakes and everybody’s dying. And we all know kind of where the Netherlands is kind of down as far as if we look at the farmers and what they’re looking at as far as shutting down farming and fertilizer production, ammonia, et cetera. So I think this is, again, without upsetting anybody, I think that this is just another step where we see a little bit of hysteria that kind of causes a backlash as far as what we’re looking at as far as energy security is concerned. And actually, if you go to Hilltower Resource Advisors, one of our analysts just posted a great post on that.

Tony

Okay, great. Hill Tower Resources. Advisors. Right.

Albert

Yeah. These are just born from bad political decisions for politicians in Europe trying to safeguard their seats and their parliament. That’s all it is. They cater to the Green parties and they come up with bad economic policies.

Tony

Okay, go ahead.

Tracy

Sorry. What I’m thinking is I’m addressing this towards you, Albert, actually, because you just brought this up, is that if we’re talking about do you think that with elections coming up, that we’re going to start seeing a backlash? Because we just saw like, say, the Green Party in Germany fall from 22% to 14% over a very short period of time. So do you think with upcoming elections we’re going to see sort of a change in stature of these parties because they’re going to lose votes?

Albert

It depends. It depends on the country and the situation and the parliamentary makeup of each of the countries. Let’s just take Holland, for instance, one of my non favorite countries in the world. But Root has a liberal majority in his parliament. For him to stay in power, he needs that liberal majority. So in order to keep those seats, he’s going to have to cater to those people, and that means more Green initiatives to the extreme. Now, of course, if the economy starts to tank and inflation takes hold in Europe and the banking sector starts to falter, those are scenarios where, yeah, it could tip a lot of elections over back to the right. But the problem is the European elections and the way they do their government is a parliamentary system. So they don’t necessarily need to win the majority for their party. They just need to have a coalition that takes a majority.

David

Albert, what impact do you think going on? What Tracy mentioned and this whole topic of Green politics with the war in Ukraine and Russia, I think it’s the energy dependence that Germany in particular saddled itself with with respect to Russia that just kind of blew up in their face. And that has implications for a lot of the Green policies that were championed, namely getting rid of nuclear. So do you have any insight on how the war is impacting? Is there going to be a revisit of these green policies to maybe not repeat the same geopolitical mistake or experience?

Albert

Well, that’s going to really depend on what happens in the winter of this year. They had a mild winter, so it kind of eased up on the pressure that the European politicians had to deal with. But let’s just be clear that Europe is, like I’ve said, for weeks now in a zombie state in terms of their industrial output. Right now, they’re not really working. There’s not very many things being built over there. They have a drought that’s still pretty significant in Europe and actually getting worse. So that’s going to affect the shipping, like Tracy mentioned, I think, like six months ago up the river of the Rhine. They can’t ship materials back and forth because the water levels are too low. So there’s a lot of things that have to be taken into account. So it’s not really, let’s wait and see how the winter goes and then we can readdress what policies they’ll probably have to look into concerning green initiatives.

Tracy

We’re already seeing problems as far as supply is concerned with summer coming along. Right. Although Europe is not a big consumer of air conditioning like the United States is, we’re still seeing a large drawdown because temperatures are over 20 C there. We laugh in the US. I know, but that’s a big deal for them. We’re seeing this in the UK, we’re seeing this in summer is just really starting. And again, I think I mentioned this and everybody was skeptical about it. I mentioned this on this podcast months ago, that we should look to summer because air conditioning would be a big drawdown for this. And I saw a lot of the comments saying, but they don’t have a lot of air conditioning. It’s not like the US. But yet we are seeing this happening. So I think we need to pay close attention to this. I think right now, especially again, we’re seeing a drought again. So from Rotterdam to Germany, we’re going to have a problem on the Rhine again this year that’s going to mitigate heavy vessels that carry crude and gas products to Europe. People don’t understand when water levels are low, you can’t have those heavy vessels coming.

Tracy

So this is what we had. This is part of the problem that we had summer of 2022. And this looks like this might be a problem again.

David

I was visiting family in southern France last summer. I was in Provence just outside of Avignon, and the Roan was really low. There are parts of the Roan where you could basically flatbed looking some boats that were just on their side. So this water crisis is not just in northern Europe, but it’s also on the more Mediterranean south as well.

Albert

Italy’s had a big problem, too, with water levels. I think the Pole was showing, like, historical markers from, like, four or 500 years ago of droughts. It’s a problem. And the mild weather kind of mitigated how much pressure the Russians could really enact on the energy market. But they get a cold winter and the Russians want to get nasty. Look out for Europe.

Tony

Yes. So, Tracy, if they can’t transport product by river, do they transport it by rail or truck or do they just not transport it?

Tracy

Well, what they do is they have to take that product and put it into lighter vessels. In other words, through there you can’t get an apple. You got to go the smallest. They start taking that product, they’re not going to let people go without energy. So what you have to do is you just have to start putting that project into smaller vessels that can transverse that river.

Tony

Okay.

Albert

If it’s not lighter vessels, it’s actually one third of the cargo capacity to keep the boat lighter and afloat higher. But that increases the cost of shipping.

Tracy

Which increases inflation, which also creates another problem. Exactly.

Tony

Okay, then just kind of final question is I’m really interested in this closing of the field in Holland. And I know that sounds a little bit pedantic, but it kind of reminds me of the reactionary close of the nuclear stations in Germany in 2012. So are we watching Europeans do things that they may regret in 5678 years and then reverse trend on this stuff?

Tracy

Well, absolutely. All you have to look at is the deindustrialization that is happening exactly right now in Germany and then take that model and place that across every country in the EU that is following those exact same protocols. Right. And we’re seeing that we’re seeing chemical production flee to China.

Tony

Yeah, you’ve talked about BASF and other.

Tracy

Companies that have so we’re seeing all these people go to other countries that are much more amenable to this kind of business because it’s too expensive.

Tony

So when you talk about these guys moving, is it the access to energy? Is it the kind of environmental arbitrage they can go and do things in China environmentally, is it a number of things. Is it wages?

Tracy

It’s a number of things. It’s the cost of doing business as far as energy is concerned because obviously, industrial manufacturing, et cetera, is very energy intensive. So it’s the cost of doing business. They asked companies to limit their energy use 15% last winter. That hasn’t been lifted yet. And it’s costing them ten times the amount that they were paying before. So of course, they’re leaving to other countries that may incentivize them. And that’s not only China. This is what Europe is also worried about is that industry is going to move to the US. Even, right?

Tony

The Inflation Reduction Act.

Tracy

Well, yes, which is reduction, which is not reducing any sort of inflation, but it does provide incentives to companies to move over to the United States if they want to because they get a bunch of tax credits. Now, that doesn’t influence us as taxpayers. But as far as business is concerned, if you’re looking to pay less, your options are China and the US. Mexico mexico is great, but that’s a whole nother subject.

Tony

Love to dig into that at some point. So let me ask one final question of all you guys. Albert talked about how us Officials, Fed, treasury are either directly or indirectly conducting economic warfare on China. But as we’ve talked about with Europe, they’re a little bit handicapped with their drought and their electricity prices and power and all sorts of things. And we have the economic policies of the US. Is that same kind of economic warfare kind of activity is that also impacting Europe in either a direct or indirect way? And how do the Europeans feel about that?

Albert

Of course it is. I mean, the Europeans, let’s be clear, it’s really Germany and France and maybe Holland, but they’re the economic engines of Europe. And right now they’re so blinded to where they think that China is the only emerging market share that they have available to them, which is just incorrect. But that’s their goal right now, is to safeguard that market share in China by any means necessary. And that means it’s going against the United States, which they’ve been clearly vocal on for the past six months or so.

Tony

David, what do you think about that?

David

Yeah, I don’t have any real insights into that. It’s kind of above my pay grade.

Tracy

I don’t want to speak for the people. And all I can say is what we’re seeing in companies within countries is that we are seeing transverse from obviously we’re seeing industry move from Europe to China and to the United States. Again, I don’t know how these people in these countries feel about this. I can only speak to what we are seeing business wise and trends.

Tony

We are seeing great guys, thank you so much. This has been really fantastic. David, thanks for joining us for the first time. I appreciate that. Hope we can ask you back. And Albert, Tracy, guys, thank you very much.

Albert

Have a great week and a great weekend.

David

Thank you. Thanks for having me. Take care. Have a good weekend. Bye.